Автор: 137Labs

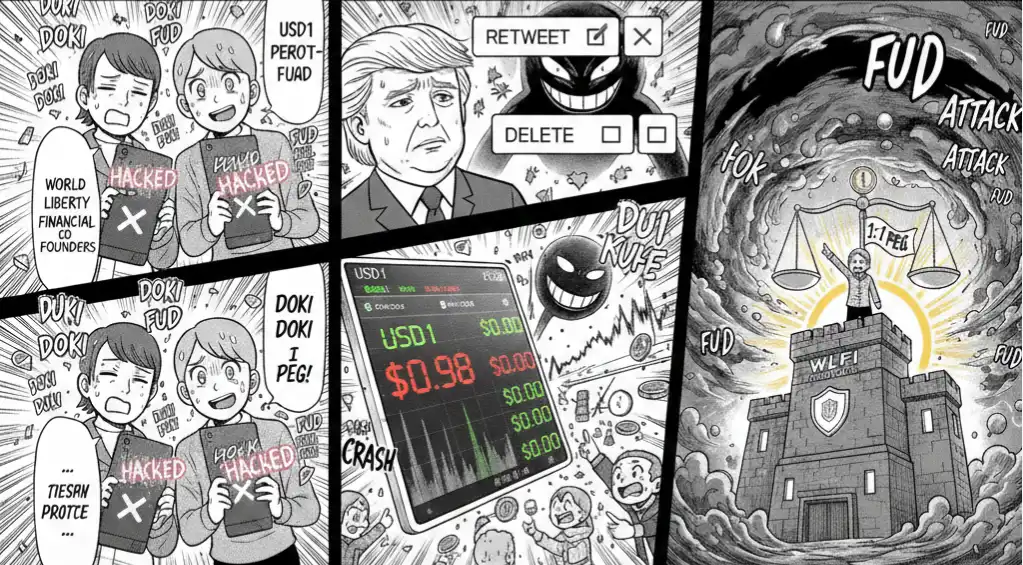

23 февраля стейблкоин под названием USD1 внезапно показал значительную скидку на вторичном рынке.

Котировки в сети упали примерно до 0,98 USDT, и в социальных сетях быстро началось обсуждение.

Сторона проекта World Liberty Financial (WLFI) впоследствии публично заявила, что это была «скоординированная атака (coordinated attack)», и подчеркнула, что резервы и механизм выкупа не пострадали.

Цена затем восстановилась.

Но проблема уже появилась —

Когда «стейблкоин» начинает торговаться со скидкой, это всего лишь трение ликвидности или предвестник трещин в кредитной структуре?

I. Хронология: от «спайка» до «версии об атаке»

По сообщениям CoinDesk, The Block, Decrypt, Wu Blockchain, PANews, ChainCatcher и других, последовательность событий大致如下:

1️⃣ Аномальные колебания на вторичном рынке

-

USD1 в некоторых торговых парах быстро упал до уровня около 0,98

-

Скидка длилась недолго

-

Затем цена восстановилась

В отличие от ситуации с USD Coin в 2023 году, который временно отвязался из-за банковских рисков, в данном случае не было явного системного банковского шока.

2️⃣ Официальный ответ WLFI

WLFI заявила:

-

Это была организованная короткая продажа и скоординированная медиаатака

-

Резервные активы в норме

-

Функция выкупа работает нормально

-

Структура привязки 1:1 не изменилась

Это заявление впоследствии было пересказано китайскими СМИ, включая Wu Blockchain и ChainCatcher.

3️⃣ Эффект усиления в социальных сетях

Событие быстро распространилось на платформе X.

Некоторые связанные твиты были удалены, что вызвало дальнейшие猜测 на рынке.

В нынешней высокоэмоциональной рыночной среде «действия по удалению» часто интерпретируются как сигнал, а не как случайная операция.

Таким образом, вопрос превратился из «отвязалась ли цена» в:

-

Существует ли риск по резервам?

-

Существует ли массовый натиск на выкуп?

-

Существует ли недостаточное раскрытие информации?

II. Суть отвязки: проблема ликвидности или проблема платежеспособности?

Ключ к определению отвязки стейблкоина заключается в различении двух совершенно разных структур риска.

Первый — это удар по ликвидности.

В этом случае резервы по-прежнему достаточны, механизм выкупа все еще畅通, но из-за недостаточной глубины рынка, ухода маркет-мейкеров или集中 давления продаж происходит кратковременный дисбаланс на вторичном рынке. После запуска механизма арбитража цена обычно быстро восстанавливается.

Второй — кризис платежеспособности.

Если сами резервные активы проблемны, или активы имеют несоответствие сроков и не могут быть немедленно реализованы, то отвязка перестает быть колебанием на торговом уровне и становится переоценкой баланса. В этом случае скидка обычно расширяется и сопровождается задержками выкупа или потерей доверия.

Судя по currently раскрытой информации, USD1 ближе к первому.

Его крах полностью отличается от алгоритмической смерти螺旋ли TerraUSD в 2022 году. Крах UST был вызван отказом механизма, тогда как спайк USD1 больше похож на перекос ликвидности в короткий промежуток времени.

Но даже в этом случае это событие仍然 имеет значение.

Потому что настоящий якорь стейблкоина — это не только резервные активы, но и доверие рынка.

Как только доверие ставится под сомнение, цена реагирует раньше基本面.

III. Кредитная структура стейблкоинов: в чем именно их «стабильность»?

Стейблкоины по своей сути являются «базовой валютой» крипторынка.

Их кредитная поддержка в основном comes from трех моделей:

-

Алгоритмические

-

Обеспеченные (залоговые)

-

С централизованным резервным хранением

USD1 относится к структуре с централизованным резервом.

Риск этой модели заключается не в алгоритме, а в:

-

Прозрачности резервов

-

Ликвидности активов

-

Структуре сроков

-

Глубине маркет-мейкинга

Как только рынок начинает怀疑, что резервы имеют скидку или риск реализации, цена往往先行 падает.

Это очень похоже на «набег на теневой банк» в традиционных финансах — как только вкладчики начинают сомневаться, само поведение по снятию средств усиливает риск.

IV. Почему реакция рынка на этот раз была особенно чувствительной?

В тот день индекс страханы уже находился на экстремально низком уровне.

В среде, где ликвидность и так напряжена:

-

Уровень leverage снижается

-

Склонность к риску ослабевает

-

Рынок высокочувствителен к неопределенности

Стейблкоины — это не только инструмент торговли, но и краеугольный камень кредитования и ликвидности.

Как только появляется скидка, цепная реакция может включать:

-

Снижение коэффициента залога

-

Срабатывание ликвидации

-

Дальнейшее сжатие leverage

-

Отток средств с рынка

Поэтому, даже если цена быстро восстановилась, психологические震荡 не исчезли同步.

V. Состоятельна ли «версия об атаке»?

WLFI приписала эти колебания «скоординированной атаке».

На крипторынке короткие продажи и медиарезонанс并不罕见.

Когда глубина торгов недостаточна, а настроения рынка хрупки, цена легко поддается усиленным колебаниям.

Но может ли атака продолжаться, зависит от одного ключевого фактора:

Верит ли рынок, что резервы реальны, могут быть兑现лены и устойчивы.

Если структура резервов прозрачна, а выкуп продолжается беспрепятственно, атака往往 не может быть долгосрочной;

Если раскрытие информации о резервах недостаточно, паника легче自我强化.

VI. Различия между USD1, USDC и USDT и истинное значение этой отвязки

Исторически USDC в 2023 году一度 упал до 0,88 доллара из-за банковских рисков, его проблема была вызвана подверженностью рискам банка-кастодиана и ограниченным темпам реализации резервов.

А Tether несколько раз轻微 отвязывался, обычно на этапах экстремальной паники или under集中 давления на вывод, но ключом к最终 восстановлению было持续开放 механизма выкупа и проверка способности兑现 резервов.

USD1 в настоящее время больше похож на проходящий «стресс-тест доверия».

Это событие больше похоже на удар по ликвидности, чем на кризис платежеспособности.

Быстрое восстановление цены говорит о том, что системного натиска на выкуп еще не сформировалось.

Но то, что действительно заслуживает внимания, — это не та цена 0,98, а то, начал ли рынок переоценивать «риск-премию» «стабильности».

Стейблкоины — это денежная основа крипторынка.

Когда рынок начинает сомневаться в их безопасности, влияние распространяется по кредитной цепочке наружу:

-

Снижение leverage

-

Сокращение кредитования

-

Переоценка залоговых активов

-

Отток средств в основные активы или с рынка

Даже если само событие является лишь краткосрочным колебанием, оно повысит стоимость будущего финансирования и ликвидности.

Отвязка — это никогда не только вопрос цены, а вопрос ценообразования доверия.

Цена может быстро восстановиться,

но восстановление доверия требует времени.

Эта отвязка USD1未必 перерастет в системный риск,

но она напоминает рынку —

На этапе сжатия ликвидности,

кредит всегда меняется раньше цены.

И как только кредит начинает переоцениваться,

вся структура рисков也随之 меняется.