Компиляция: Ken, Chaincatcher

Легендарный инвестор Уоррен Баффет придерживается почти религиозной, непоколебимой оппозиции к концепции «сплита акций».

Акции Berkshire Hathaway класса А торгуются по цене более 700 000 долларов за штуку, потому что Баффет считает, что сплит акций — это всего лишь косметическая мера, которая не меняет фундаментальную стоимость бизнеса. В мире Баффета, если вы разрежете пиццу на восемь кусков вместо четырех, у вас не станет больше пиццы. Вам просто придется мыть больше тарелок.

Хотя с точки зрения оценки сплит акций может и не быть «крупным событием», это высоко регулируемая деятельность, контролируемая Комиссией по ценным бумагам и биржам США (SEC) и принудительно исполняемая биржами.

Когда компания объявляет о сплите, она должна подать форму 8-K и уведомить акционеров заранее до вступления изменений в силу. Этот ключевой временной промежуток позволяет трансфер-агентам скорректировать реестр акционеров, брокерам обновить внутренние системы, а поставщикам данных, таким как Bloomberg, обновить свои потоки данных — чтобы акция стоимостью 500 долларов после сплита 10 к 1 не выглядела так, будто она overnight рухнула до 50 долларов.

Сплит акций — не единственное корпоративное действие, требующее такого высокого уровня координации. Выплата дивидендов также создает аналогичные сложности.

В экс-дивидендную дату цена акции снижается на сумму дивидендов. Некоторые фонды, особенно фонды с высоким доходом, доводят эту практику до крайности. Они часто распределяют доход, но большая часть этих выплат является возвратом основного капитала, фактически возвращая инвесторам их первоначальные вложения, а не выплачивая инвестиционную прибыль. Хотя количество акций остается неизменным, стоимость чистых активов (NAV) фонда со временем неуклонно снижается.

Отслеживание эффективности этих фондов требует четкого разграничения доходности от изменения цены и общей доходности.

Предположим, у вас есть 100 акций высокодоходного ETF по цене 100 долларов за акцию (инвестиция 10 000 долларов). Фонд ежемесячно выплачивает доход в размере 5 долларов, 90% из которых — возврат основного капитала. Через 12 месяцев вы получили 60 долларов наличными на акцию (всего 6000 долларов), но NAV фонда упала со 100 долларов до 46 долларов. На этот момент общая доходность от изменения цены составляет отрицательные 5400 долларов, но общая доходность равна 10 600 долларов (оставшаяся NAV 4600 долларов плюс выплаченные 6000 долларов), то есть положительные 6%.

Именно эти проблемы и призван решить блокчейн.

Единый распределенный реестр, способный к атомарным обновлениям и видимый всем одновременно. Если все будут читать данные из одной цепочки записей, то такие корпоративные действия, как сплиты акций и выплата дивидендов, будут мгновенно распространяться по всей системе, устраняя утомительную и суетливую работу по сверке, которая в настоящее время ведется между изолированными посредниками.

Именно это обещание заставило рынок тепло приветствовать объявление генерального директора Robinhood (@RobinhoodApp) Влада Тенева в июне 2025 года о запуске стратегии токенизированных акций.

Прошло шесть месяцев, токены Robinhood официально запущены, данные постоянно поступают. Но, к сожалению, начали всплывать некоторые проблемы.

Плюсы

Заявление Robinhood стало катализатором для рынка.

Другие эмитенты быстро приняли меры, чтобы выпустить конкурентные продукты. Backed Finance (приобретенная Kraken) запустила xStocks (@xStocksFi) на Solana, за которой последовал запуск продукта токенизированных акций от Ondo Global Markets (@OndoFinance).

Данные RWA.xyz по состоянию на 23 января 2026 г.

Для токенизированных акций наступил поистине взрывной год. Только во второй половине 2025 года этот класс активов вырос на 128%, увеличив общую стоимость активов почти до 10 миллиардов долларов.

Данные RWA.xyz по состоянию на 23 января 2026 г.

Токенизированные американские акции и ETF от Robinhood теперь доступны для европейских клиентов. Каждый токен выпущен в сети Arbitrum, полностью обеспечен акциями, принадлежащими Robinhood, и позволяет торговать 24/5 с нулевой комиссией. Соответствующие данные доступны на RWA.xyz.

Но точное определение показателей токенизированных акций Robinhood оказалось сложнее, чем ожидалось.

Минусы

Большинство платформ данных блокчейна при индексации токенов предполагают, что они следуют стандартным практикам. Для токенов ERC-20 это означает отслеживание эмиссии и сжигания, накопление предложения с нуля и расчет рыночной капитализации как предложения, умноженного на цену.

Это работает для тысяч токенов в Ethereum и других сетях EVM. Но ERC-20 изначально не был предназначен для ценных бумаг, которые подвергаются корпоративным действиям. Стандарт изначально не поддерживает сплиты акций, обратные сплиты или корректировки базиса, вызванные дивидендами.

Поэтому Robinhood пришлось использовать пользовательские контракты для правильной обработки этих событий, чтобы гарантировать права своих конечных пользователей. Эти токены работают корректно внутри приложения Robinhood, но их механизмы непрозрачны для внешних платформ данных и несовместимы с протоколами DeFi — поскольку и те, и другие предполагают, что имеют дело со стандартными токенами ERC-20.

Когда мы сравниваем предложение токенов, рассчитанное с использованием стандартной логики ERC-20, с фактическими данными в блокчейне, расхождения слишком велики, чтобы их игнорировать. Данные по некоторым токенам отклоняются в 10 раз, по некоторым — даже в 100 раз.

Почти все ошибки можно отнести к двум причинам:(1) эрозия чистой стоимости из-за дивидендов и (2) обратные сплиты акций.

Эрозия NAV из-за дивидендов высокодоходных ETF

Данные по состоянию на 23 января 2026 г.

Это высокодоходные опционные ETF, которые часто выплачивают дивиденды, причем 90% или более выплат классифицируются как «возврат основного капитала». Каждая выплата возвращает денежные средства инвесторам, но в основном это возврат капитала, а не инвестиционный доход. Количество акций остается неизменным, а чистая стоимость со временем неуклонно снижается.

Контракты Robinhood решают эту проблему, разделяя «акции» и «токены». Количество акций у держателя остается неизменным, но внутренний множитель корректирует сообщаемое предложение токенов в сторону уменьшения по мере накопления возвратов основного капитала, чтобы отразить сокращение базовой чистой стоимости.

Однако платформы данных, следующие стандартной модели ERC-20, просто суммируют эмиссию и сжигание. Этот метод не может уловить такую корректировку базиса, что приводит к завышению расчетного предложения токенов в обращении и, как следствие, к завышению报告的 рыночной капитализации.

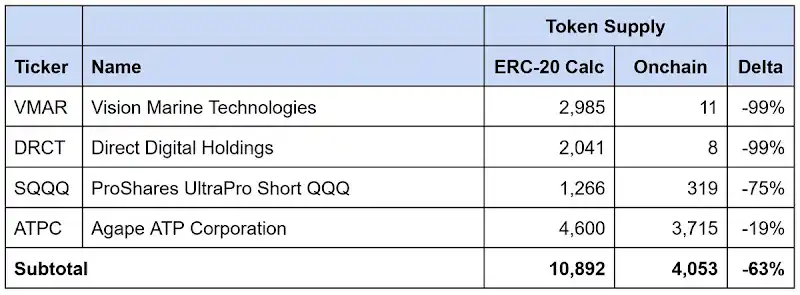

Обратные сплиты акций

Данные по состоянию на 23 января 2026 г.

Та же проблема возникает при обратных сплитах акций. Обратный сплит увеличивает цену за акцию за счет консолидации акций, обычно для соответствия листинговым требованиям биржи. Количество акций уменьшается пропорционально, но цена за акцию увеличивается пропорционально, общая стоимость остается неизменной.

Аналогичным образом, контракты Robinhood корректируют предложение токенов, чтобы отразить обратный сплит, в то время как сторонние платформы, следующие стандартной модели ERC-20, завышают оборотное предложение и报告ную рыночную капитализацию.

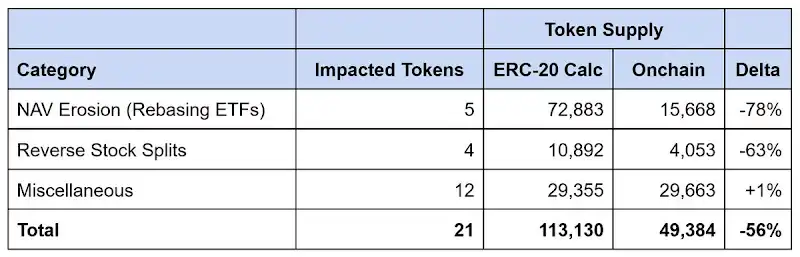

Суммарное расхождение данных Robinhood

Данные по состоянию на 23 января 2026 г.

Среди 21 выявленного нами токена с несоответствием данных,报告ное предложение было завышено примерно на 64 000 токенов, при этом расхождение достигло 56%. Эрозия NAV из-за высокодоходных ETF составляет около 90% этого разрыва, обратные сплиты акций объясняют оставшуюся часть.

Любая платформа данных, которая полагается на стандартную логику ERC-20 для расчета предложения, будет严重 завышать рыночную капитализацию токенизированных акций Robinhood, и часто в разы.

Решение

Таксономия токенизированных акций: Модели и инфраструктура

Эмитенты токенизированных акций采用不同的方法来处理 корпоративных действий. Их大致可以分为两类.

Модели с корректировкой базиса (Rebasing Models)

Модели с корректировкой базиса维持 паритет спотовой цены: 1 токен должен всегда торговаться по цене, близкой к цене 1 базовой акции. При возникновении корпоративных действий балансы токенов автоматически корректируются для поддержания этого соотношения. Эмитенты,采用这种方法,根据其与 базовым эмитентом активов的关系,分为两个 лагеря:

- Корректировка базиса (Сторонняя): Эмитент operates independently from the company whose stock is being tokenized. xStocks (@xStocksFi,隶属于 Backed Finance / Kraken) и Robinhood (@RobinhoodApp)都采取了这种方法. Токены обеспечены акциями на хранении, но поскольку нет прямой связи с базовым эмитентом, они仅复制经济敞口,而不赋予法律所有权.

- Корректировка базиса (Прямая): Эмитент сотрудничает с публичной компанией для токенизации ее акций. Opening Bell от Superstate (@SuperstateInc) и Securitize (@Securitize) operate as SEC-registered transfer agents and serve as the official shareholder of record. Поскольку токены выпускаются согласованно с компанией, токены сами по себе являются законными ценными бумагами, а держатели享有 права акционеров, которые недоступны при стороннем подходе.

Обе структуры требуют инфраструктуры множителя для отражения корпоративных действий в блокчейне.

Стандарт Token-2022 в Solana нативно предоставляет расширение масштабирования UI-сумм. Эмитенту достаточно обновить множитель, который adjusts the balance displayed in the user interface without changing the underlying token amount. Например, сплит акций 2 к 1 изменит множитель с 1.0 на 2.0; кошелек будет отображать удвоенный баланс, в то время как базовый подсчет исходных токенов останется неизменным. Поскольку стандарт является нативным для Solana, платформы данных могут напрямую запрашивать изменения множителя.

В сетях EVM в настоящее время нет эквивалентного стандарта. Таким эмитентам, как xStocks и Robinhood, пришлось создавать собственные механизмы множителя. Хотя балансы корректируются правильно, и кошельки отображают цену, согласующуюся со спотовой, эти реализации являются кастомными. Сторонние лица, полагающиеся на стандартные вызовы ERC-20, не могут обнаружить, когда множитель изменяется, или запросить его текущее значение. Следовательно,必须单独理解每个发行方的具体实现方案.

Именно поэтому Крис Ридманн из Superstate и Гилберт Ши из Robinhood совместно разработали ERC-8056, черновой提案,旨在为 ERC-20 代币引入标准化“缩放 UI 金额扩展”. Это предоставит платформам данных унифицированный интерфейс для отслеживания корпоративных действий across эмитентов.