Deep Tide Digest: As Bitcoin recently rebounded to $70,000, a conspiracy theory linking Jane Street to "suppressing the price at the U.S. stock market open" went viral in the crypto community. This article deconstructs this claim from three dimensions: on-chain data, ETF structure, and options positioning. The conclusion is: the real issue is not Jane Street, but the black box of price discovery in the ETF era—the opacity of institutional hedging is making it increasingly difficult for retail investors to read the market.

Full text below:

As Bitcoin rebounded close to $70,000 in the past 24 hours, a familiar debate reignited in the crypto market: Do Wall Street institutions operating within the spot ETF ecosystem now have too much influence over price discovery?

The target this time is Jane Street—a quantitative trading firm that is both a key ETF intermediary and a defendant in a new lawsuit related to the 2022 collapse of Terraform Labs.

On social media, traders linked Bitcoin's recent rally to a claim: an alleged pattern of sharp intraday drops around the U.S. stock market open suddenly disappeared after the lawsuit became public.

This theory spread quickly because it combines two views that already resonate: distrust of large trading firms and unease about Bitcoin markets increasingly operating through traditional finance channels.

However, evidence supporting a "coordinated Bitcoin suppression" plan remains thin.

What this episode reveals clearly is this: the structure of spot Bitcoin ETFs has made it increasingly difficult for many investors to distinguish between genuine spot demand and market-making, hedging, and arbitrage activities.

In this sense, the Jane Street controversy goes beyond allegations against a single firm. At its core, it's about how Bitcoin's new institutional infrastructure shapes price discovery—whether the market is becoming more efficient or more opaque.

Origin of the Jane Street Bitcoin Rumor

The rumor took shape after Bitcoin rallied significantly for two consecutive trading days. Users on X began asserting that the so-called "10 AM sell program" had vanished.

Notably, the X account Negentropic, run by Glassnode co-founders Jan Happel and Yann Allemann, was a key driver in spreading this theory. They claimed: "The Jane Street lawsuit was made public, and the 10 o'clock Bitcoin smash miraculously disappeared."

This claim gained traction quickly because Jane Street is no unknown entity. It is one of the world's largest trading firms and a known participant in the Bitcoin ETF market, serving as an Authorized Participant (AP) for IBIT (BlackRock's spot Bitcoin ETF).

In practice, this embeds it tightly into the core mechanism that keeps ETF share prices aligned with the value of the underlying holdings.

Simultaneously, legal troubles for the firm further fueled the controversy.

The liquidators of Terraform Labs filed a lawsuit in Manhattan, alleging that Jane Street and other firms profited from material non-public information related to Terraform's liquidity operations during the May 2022 collapse of TerraUSD.

The complaint states that Terraform withdrew $150 million in TerraUSD liquidity from Curve's 3pool, and wallets associated with Jane Street withdrew approximately $85 million just minutes before this news became public.

Jane Street denied any wrongdoing, calling the case a desperate attempt to shift blame for losses caused by Terraform's own actions.

This lawsuit does not prove anything about current Bitcoin trading.

But it explains why traders were quick to link Jane Street to an observable market pattern. In the crypto world, trust is often fragile; an institution accused in one market event often becomes a suspect in the next.

Industry Insiders Refute the Rumor

Against this backdrop, some Bitcoin traders believed this top cryptocurrency had been mechanically sold around the U.S. spot market open for months, liquidating long positions and creating a liquidity vacuum in thin order books.

If this selling disappeared after Jane Street faced new legal pressure, perhaps the firm had been suppressing the market.

Furthermore, the firm's early association with FTX founder Sam Bankman-Fried cast a shadow over its image. Bankman-Fried worked at the trading firm before founding FTX.

This narrative is emotionally compelling but far easier to assert than to prove.

Checkonchain analyst James Check directly refuted the argument, writing that Jane Street did not suppress Bitcoin, and that long-term holders selling spot to the market better explains the price action.

CryptoQuant Head of Research Julio Moreno held a similar view, arguing the theory overlooks a more obvious driver: a sharp contraction in Bitcoin spot demand since early October 2025.

He added that the operational mechanics blamed on Jane Street resemble the delta-neutral position management common to many trading firms.

The value of these rebuttals is that they point to the core weakness of the rumor: Bitcoin was already under pressure from broader macro repricing forces before entering 2026.

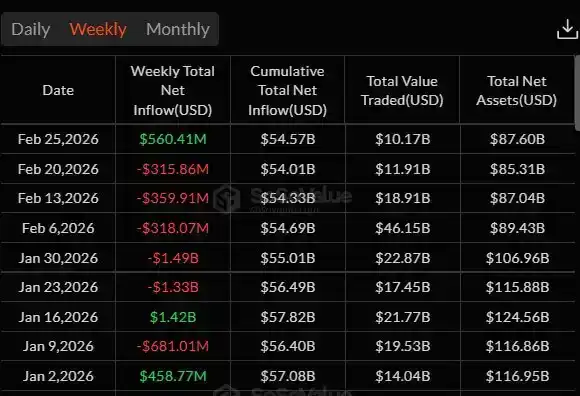

Data from SoSo Value shows institutional investors have cut Bitcoin ETF exposure for five consecutive weeks, with total outflows from spot Bitcoin ETFs reaching approximately $4.5 billion.

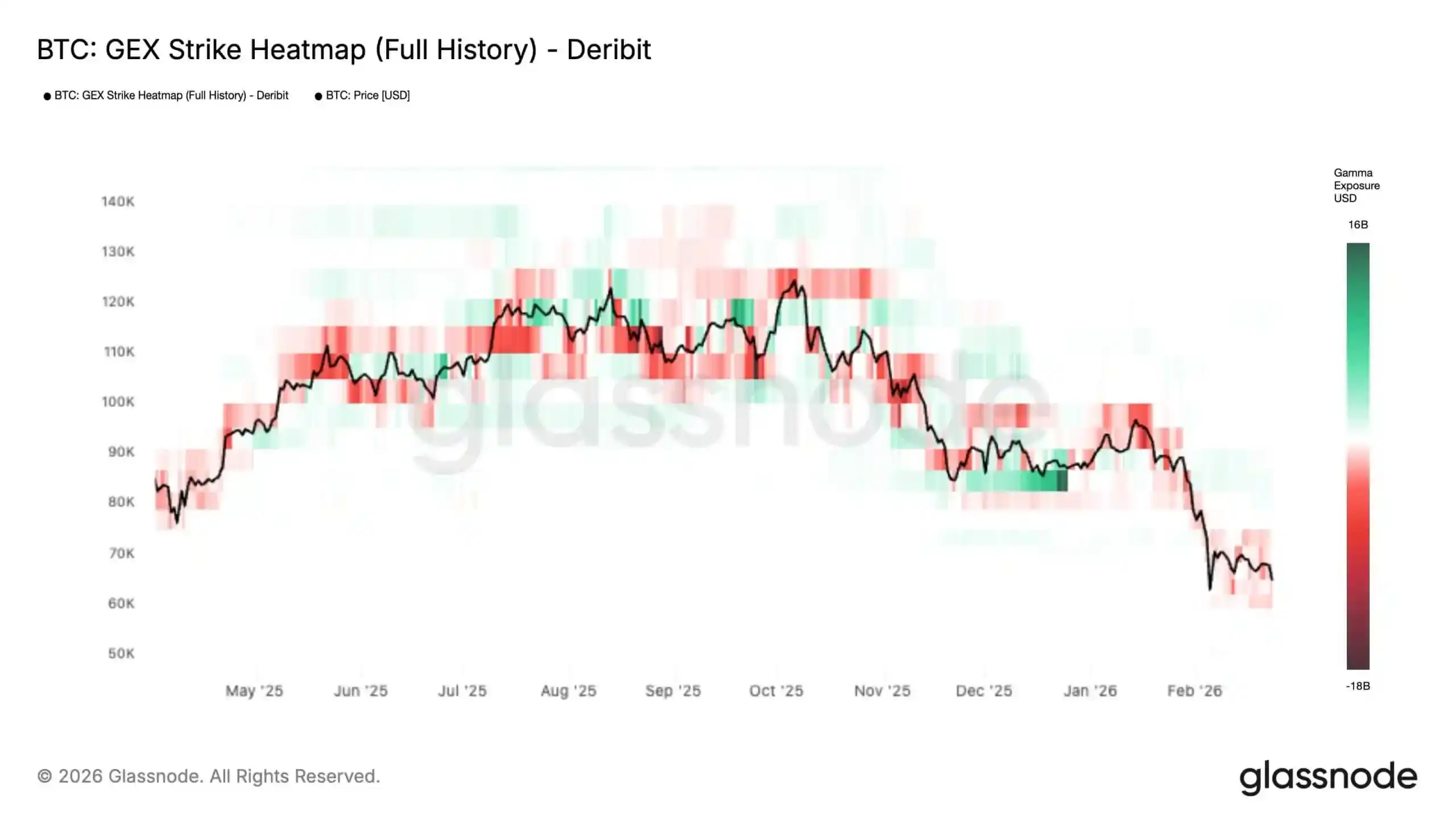

Meanwhile, Glassnode data shows that recurring market stress early this month triggered a structural shift in the Bitcoin options market towards a more volatile regime.

The firm noted that the all-history gamma exposure (GEX) heatmap shows negative gamma expanding at and below the current price, while the wall of positive gamma "resistance" above the spot price is receding.

In plain language: the option positions that typically act as shock absorbers are fading, and the market is increasingly in a zone where hedging flows no longer cushion declines but instead amplify them.

This dynamic is important: when the price is in a short-gamma regime, market makers' delta hedging tends to follow the trend, not sell on declines and buy on rallies.

The result: the market can move faster and further on relatively small catalysts—larger intraday swings and a higher risk of cascading moves through key levels—until Bitcoin hits the next thick "gamma wall," where hedging switches back to a buffering mode.

In other words, traders are in an environment prone to seeing "intent" everywhere. When liquidity is thin and leverage is high, almost any sharp move can look organized.

The ETF Pipeline Is Harder to Read Than It Seems

The deeper issue raised by the Jane Street controversy is structural, not about a specific institution.

As argued by Jeff Park, Chief Investment Officer at ProCap Financial, the real question is not whether one company is "uniquely suppressing" Bitcoin, but whether the ETF market structure gives Authorized Participants discretionary space that is opaque to the public.

This matters because investors often habitually interpret ETF disclosure data as clean directional cues—but that's not the case. A 13F filing might show a large long ETF position, but SEC guidance clearly states short positions are not included, and short options are not netted against long positions.

In practice, the market might see the inventory but not the futures, options, or other hedges wrapped around it.

This opacity is compounded by how trust is built. BlackRock's documentation for IBIT shows the trust can handle share creation and redemption through Authorized Participants and can also trade with designated Bitcoin counterparties.

As of that filing, these counterparties included JSCT, LLC, an affiliate of Jane Street Capital, and an affiliate of Virtu Americas, Virtu Financial Singapore.

The filing also shows the list of Authorized Participants has expanded to include JPMorgan, Citadel Securities, Citigroup, Goldman Sachs, UBS, Macquarie, and others, with more firms gaining access to the ETF creation/redemption mechanism.

Park's point is that this structure distorts outsiders' reading of ETF flows.

Under the old cash model, creating ETF shares required the fund to buy spot Bitcoin. But after the SEC approved in-kind creation and redemption for crypto ETPs in July 2025, Authorized Participants gained greater flexibility in acquiring and delivering the underlying asset.

The SEC said this change would lower product costs and improve efficiency. But it also means APs' exposure can be managed through a wider array of instruments and counterparties, making it harder to judge when ETF activity reflects genuine spot demand versus inventory management, basis trading, or hedge construction.

None of this is evidence of abuse, and Park's argument does not rely on proving Jane Street or any other firm abused power. His sharper point is: Bitcoin's ETF era has inserted a black box between public holding data and the underlying price discovery process.

The start of a trade looks like ordinary market-making, and the end looks like it too. What's difficult to observe is the middle: whether hedging is done via spot, futures, swaps, or some combination, and whether natural arbitrage mechanisms truly transmit genuine spot demand to Bitcoin.

This is why the Jane Street rumor resonated. It is less an accusation against a specific participant and more a signal—revealing how little the market understands about its own operating pipelines.

Why the U.S. Market Open Feels Like a Selling Zone

The "10 AM theory" sounds plausible because, even without deliberate manipulation, the U.S. market open is a genuine window of volatility.

This period concentrates cross-asset rebalancing, equity-related risk adjustments, and derivative hedging operations.

In a market where ETF intermediaries can hedge inventory with futures or other instruments, futures can pull the spot price, not just follow it.

When order books are thin, these moves can look larger and more conspiratorial than they are. Bloomberg reported earlier this month that Bitcoin market depth remains more than 35% below October levels, highlighting how fragile liquidity has become.

Meanwhile, macro analyst Alex Kruger stated that available data does not support the "systematic 10 AM daily sell-off" claim.

He wrote that since January 1st, IBIT's cumulative return in the 10:00-10:30 AM ET window is positive 0.9%, while the 10:00-10:15 AM window is down 1%.

In his view, this is noise, not evidence of a repeatable suppression program.

More importantly, he said, the performance pattern in these two windows highly correlates with the Nasdaq, indicating a broad repricing of risk assets, not a Bitcoin-specific operation.

This interpretation fits the broader market context better than the viral story.

If Bitcoin is traded increasingly as a macro risk asset via ETF wrappers, then pressure at the U.S. open—especially in thin markets—repeatedly creating Bitcoin weakness in the same intraday window should not be surprising.

On-Chain Scarcity is Clear, Price Discovery is Not

Bitcoin's supply is fixed by protocol. No change in ETF market structure can alter that. What has changed is the channel through which an increasing share of demand—and scrutiny—now flows.

The Jane Street controversy reveals the crack between these two realities. On-chain scarcity is transparent; the institutional system layered on top is not.

Investors can see ETF shares outstanding and some disclosed holdings, but they cannot see every potential hedge behind a market maker's book, every internal net exposure, or every cross-market position.

This gap creates room for misunderstanding and distrust.

That Jane Street has faced scrutiny in other markets doesn't help. In July 2025, Indian securities regulators issued an interim order in an alleged index manipulation case involving a Jane Street entity, and Reuters later reported that SEBI barred the firm from the Indian securities market during case review. Jane Street also denied wrongdoing there.

The India case is unrelated to Bitcoin, but it explains why crypto traders were prepared to imagine the worst when Jane Street's name appeared in headlines again.

However, the available facts do not prove Jane Street executed a deliberate Bitcoin suppression plan.

They prove something else: the post-ETF Bitcoin market has become easier to enter, more deeply integrated with institutions, and harder for the average investor to read.