Автор: Nancy, PANews

В то время как участники криптопространства публиковали в соцсетях скриншоты заявок на подписку на SpaceX, делясь радостью от возможности урвать кусок супер-IPO, Trade.xyz на Hyperliquid оказался в центре рыночного скандала из-за правил ценообразования своего предшествующего IPO (Pre-IPO) перпетуального контракта на SPCX.

Спор о ценообразовании SPCX: Trade.xyz подвергается проверке на доверие

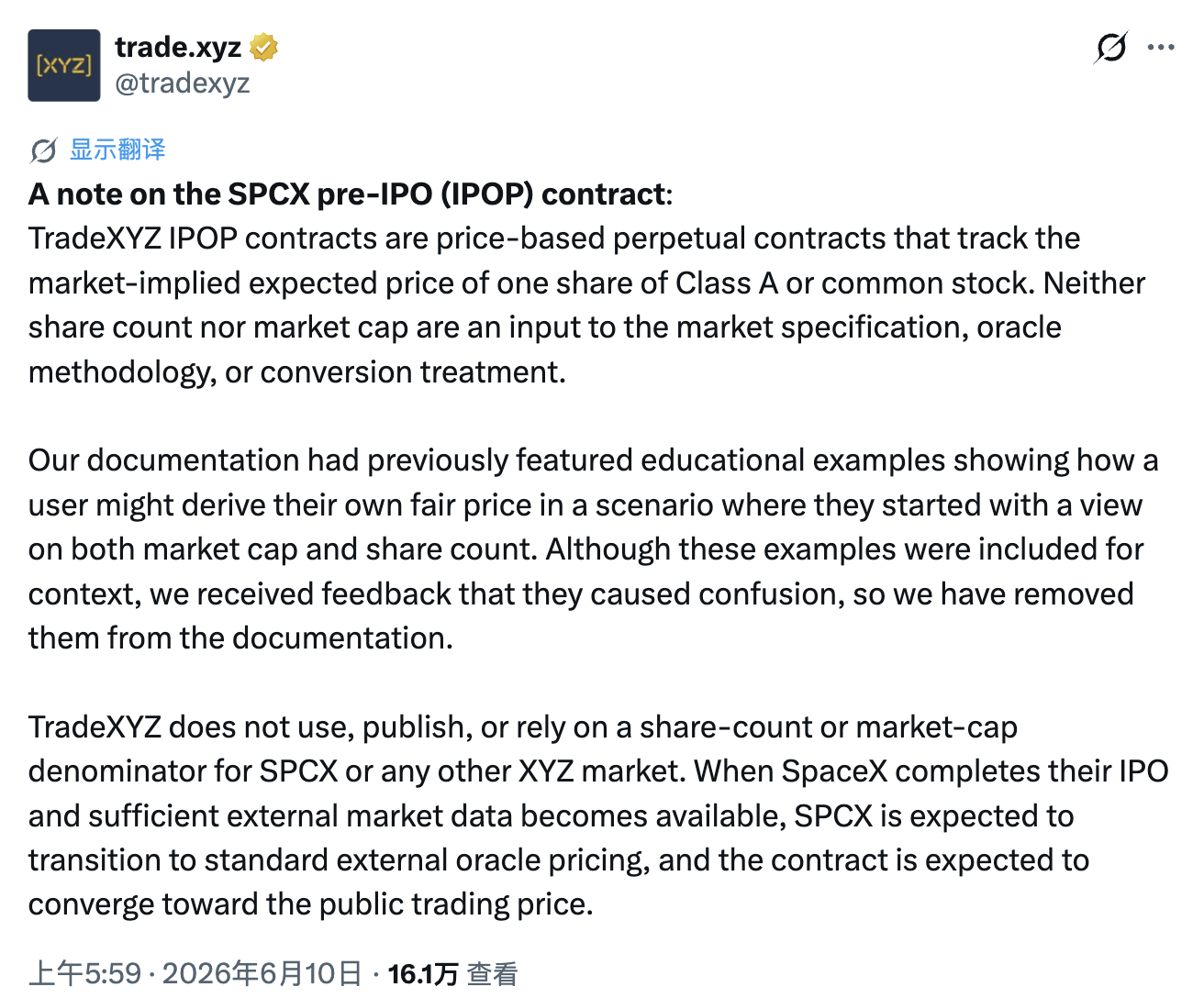

10 июня Trade.xyz опубликовал официальное заявление в ответ на споры вокруг ценообразования Pre-IPO перпетуального контракта на SPCX.

Согласно заявлению, контракт IPOP от Trade.xyz относится к ценовым перпетуальным контрактам. Его основная цель — отслеживать рыночные ожидания цены за одну акцию класса A обыкновенных акций, а не отражать общую оценку компании. Таким образом, информация об общем количестве акций компании, рыночной капитализации и т. д. не является частью правил контракта, логики ценообразования оракула или механизма будущей конвертации контракта. Другими словами, цена SPCX на Trade.xyz больше похожа на индикатор, отражающий рыночные настроения и торговые ожидания, а не на теоретическую цену акций, рассчитанную на основе фундаментальных показателей компании.

Trade.xyz также отметил, что в ранней документации к продукту приводились примеры, демонстрирующие, как пользователи, исходя из собственной оценки компании и общего количества акций, могут вывести разумную цену за акцию. Хотя этот контент был предназначен только для понимания механизма продукта, некоторые пользователи ошибочно предположили, что сама платформа будет основывать цены на данных о рыночной капитализации или количестве акций. Поэтому эти примеры были удалены из официальной документации.

В заявлении подчеркивается, что Trade.xyz не будет использовать, публиковать или полагаться на количество акций или рыночную капитализацию в качестве эталона ценообразования для SPCX или любых других рынков XYZ.

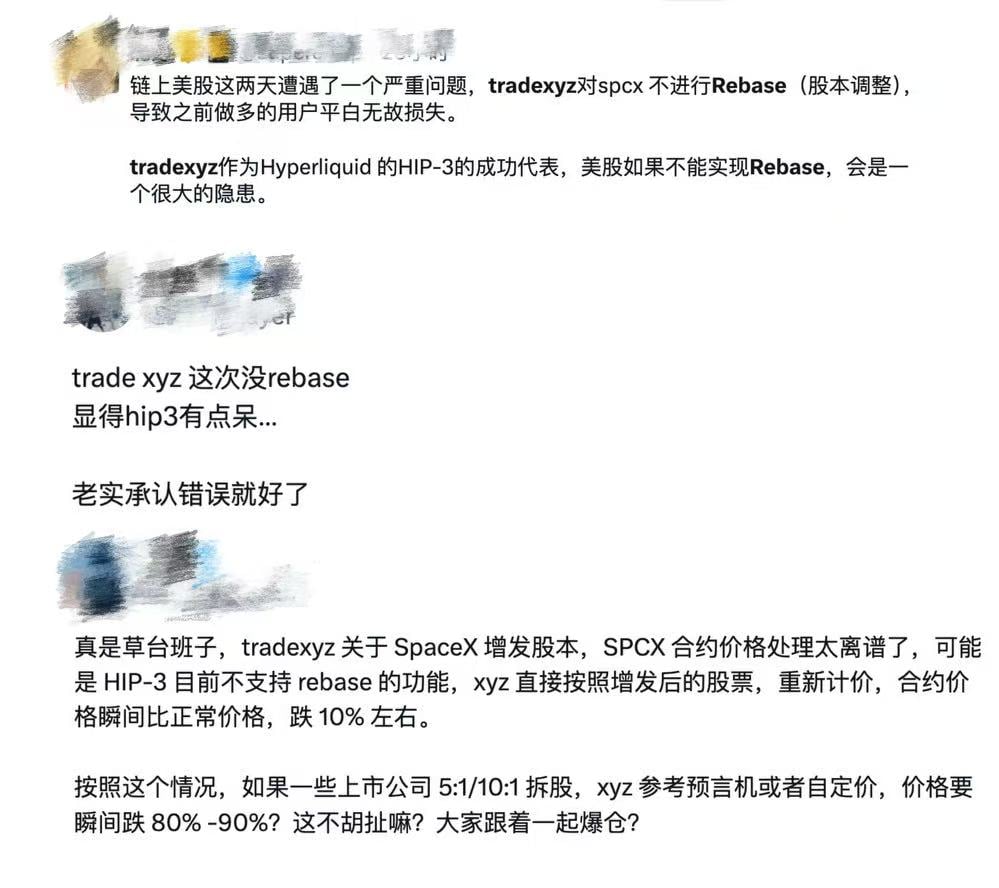

Непосредственной причиной скандала стал проспект акций SpaceX, опубликованный несколько дней назад. Согласно документу, реальное общее количество акций SpaceX составляет 13,08 миллиарда, что примерно на 10% больше, чем ранее использовавшаяся на рынке цифра в 11,87 миллиарда акций. Это означает, что при неизменной общей оценке компании теоретическая цена одной акции SpaceX должна быть скорректирована вниз примерно на 10%.

После объявления несколько централизованных бирж (CEX) приостановили торговлю соответствующими контрактами и возобновили её после пересмотра цен на основе новых данных об акционерном капитале. В то же время Trade.xyz, придерживаясь своей продуктовой логики, не полагающейся на данные о количестве акций, не синхронизировал свою структуру ценообразования. Две разные системы ценообразования вызвали волну межбиржевого арбитража и быстро вывели Trade.xyz в эпицентр общественного внимания.

Что касается решения этого расхождения в будущем, Trade.xyz заявил, что как только SpaceX официально проведет IPO и на открытом рынке сформируется достаточно внешних торговых данных, SPCX переключится на стандартный механизм ценообразования через внешний оракул, и ожидается, что цена контракта постепенно сойдется к фактической рыночной цене акций SpaceX.

Отзывы некоторых участников сообщества

Однако это разъяснение только усилило рыночные споры. Многие пользователи считают, что на начальном этапе запуска продукта Hyperliquid не раскрывал правила контракта достаточно полно и четко, а описания в интерфейсе и официальной документации в течение долгого времени вводили в заблуждение. Только ближе к IPO и после всплеска споров платформа поспешно опубликовала разъясняющее заявление и внесла изменения в документацию. Такой подход «постфактум» трудно назвать убедительным.

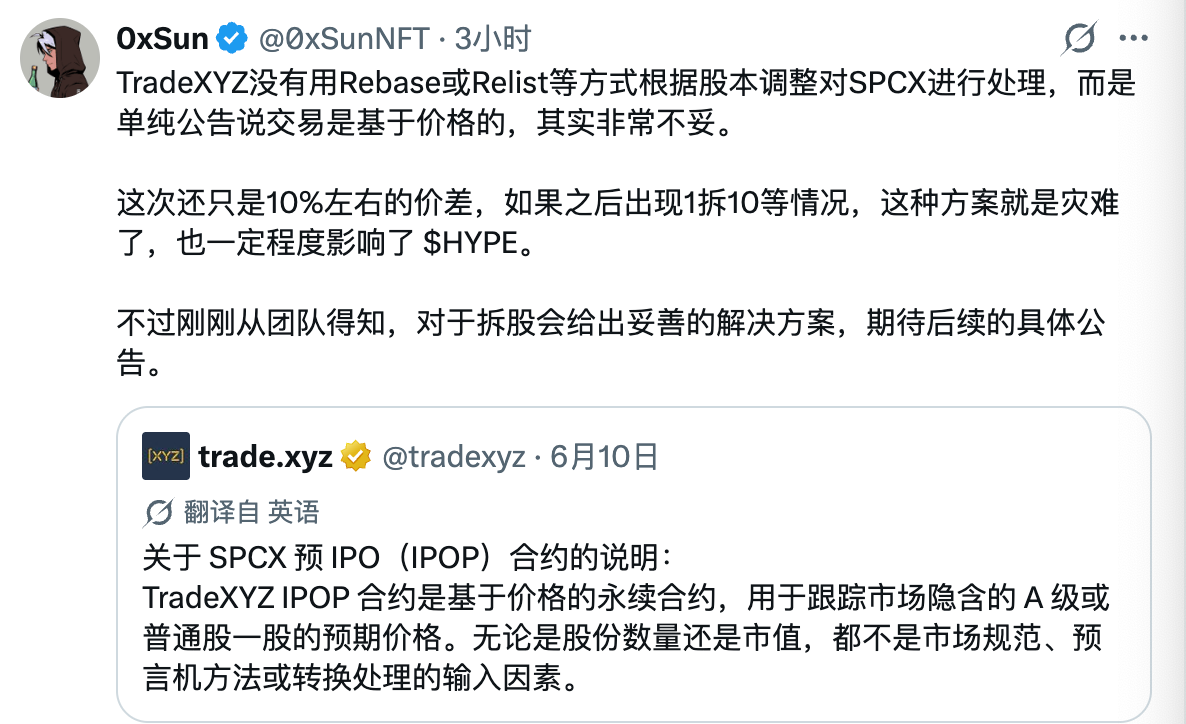

Еще большее недовольство вызвали реальные потери пользователей. Поскольку механизм HIP-3 сам по себе не обладает возможностью Rebase (сброса базовой цены), как у традиционных бирж, когда рынок переоценивает цены на основе нового акционерного капитала SpaceX, цена контракта SPCX может только пассивно скорректироваться гэпом вниз. В результате стоимость длинных позиций сократилась примерно на 10% за короткое время, и многие пользователи, использовавшие высокое кредитное плечо, были вынуждены закрыть позиции или даже понести убытки, которые напрямую превратились в прибыль для «медведей» и арбитражеров.

С точки зрения этих пользователей, платформа не только не проявила достаточной заботы о пострадавших пользователях и не предложила никакой компенсации или плана смягчения последствий, но и ответила «таков механизм продукта», что выглядит очень равнодушно и безответственно.

В некотором смысле дискуссия вокруг права на ценообразование SPCX послужит ориентиром для разработки и раскрытия правил для большего количества активов Pre-IPO в ончейне.

Проблема Rebase ждет решения: Pre-IPO в ончейне сталкивается с серьезным испытанием

Для Perp DEX отсутствие возможности Rebase означает, что любой актив Pre-IPO в будущем, столкнувшись с такими обычными событиями на традиционном фондовом рынке, как сплит акций, дополнительная эмиссия, выплата дивидендов и т. д., может привести к мгновенной переоценке цены контракта, вызвать массовые цепные ликвидации и несправедливые убытки, а также подорвать доверие пользователей к платформе.

Чтобы понять важность Rebase, сначала нужно понять, что это такое и почему оно стало ключевым звеном в дизайне Pre-IPO перпетуальных контрактов.

Проще говоря, Rebase — это механизм нейтральной корректировки стоимости. Платформа пропорционально синхронно корректирует цену контракта и количество позиций пользователей, так что общая стоимость позиций трейдера до и после корректировки остается практически неизменной. Этот механизм необходим, потому что на этапе Pre-IPO фактическое общее количество акций компании обычно не раскрывается публично, и биржа может разработать начальную цену и множитель контракта только на основе прогнозируемого рынком акционерного капитала. Когда компания официально подает документы S-1/S-1A и раскрывает реальный акционерный капитал, если фактическая цифра отличается от прогнозируемой, требуется Rebase для калибровки параметров контракта. В противном случае цена контракта будет постепенно отклоняться от реальной стоимости акции, что может создать возможности для межбиржевого арбитража и заставить владельцев односторонних позиций нести убытки.

Однако по сравнению с CEX, реализация Rebase для Perp DEX является более сложной задачей.

Конкретно, CEX опираются на централизованные базы данных и профессиональные команды управления рисками, что позволяет им быстро приостанавливать торговлю после корпоративных действий (таких как дополнительная эмиссия акций или сплит) и единообразно корректировать позиции всех пользователей перед возобновлением торгов. Весь этот процесс выполняется на стороне биржи, и номинальная стоимость позиций пользователей остается плавной и непрерывной. Даже для крупных CEX со зрелыми торговыми системами и профессиональными техническими командами такие операции Rebase, связанные с синхронной корректировкой позиций по всему рынку, по-прежнему являются сложной инженерной задачей.

Более того, в Perp DEX все процессы сопоставления ордеров, ликвидации и состояния позиций выполняются в смарт-контрактах, и нельзя напрямую изменять данные, как в CEX. Для достижения эффекта, аналогичного Rebase, часто требуется дополнительная разработка логики мониторинга, специальных хуков или модернизация механизма контрактов, что не только увеличивает затраты на газ и сложность системы, но и расширяет потенциальную поверхность для атак, создавая новые угрозы безопасности.

Кроме того, Rebase может еще больше усугубить проблему фрагментации ликвидности, изначально присущую децентрализованным рынкам. Один и тот же актив Pre-IPO может одновременно существовать на нескольких DEX, где глубина каждого рынка ограничена, а LP (поставщики ликвидности) в условиях дополнительной неопределенности, вызванной Rebase, могут снизить готовность вкладывать средства, что в конечном итоге приведет к снижению ликвидности, увеличению проскальзывания и ухудшению торгового опыта.

Конечно, реализация Rebase в децентрализованной архитектуре не является полностью невозможной. Как отметили некоторые участники сообщества, например, Aster уже успешно провел корректировку Rebase для аналогичных активов, что означает, что реальная проблема заключается не в том, что DEX по своей природе не могут поддерживать это, а в том, готова ли платформа разработать для этого дополнительные механизмы и взять на себя связанные с этим затраты на разработку и эксплуатацию.

Для сравнения, Trade.xyz, помимо приверженности более рыночной философии ценообразования, основан на архитектуре HIP-3, которая позволяет разработчикам независимо развертывать свои собственные рынки перпетуальных контрактов. Хотя эта модель унаследовала высокопроизводительную систему ордербуков Hyperliquid, каждый рынок имеет полностью независимые спецификации контрактов, определения оракулов и настройки параметров, не имея встроенной поддержки Rebase на уровне платформы, поэтому невозможно легко реализовать пакетную корректировку всех позиций. Однако, как сообщили некоторые представители сообщества, Trade.xyz изучает соответствующие решения для возможных в будущем особых событий, таких как сплит акций.

С более долгосрочной точки зрения, вопрос ценообразования SPCX выявил не просто недостаток в дизайне продукта, а реальные проблемы, с которыми сталкиваются текущие Perp DEX в процессе исследования активов RWA. В будущем, по мере того, как все больше активов Pre-IPO будут переноситься в ончейн, смогут ли ончейн Pre-IPO перпетуальные контракты, как рынки-предшественники до формирования публичных рыночных цен, создать достаточно надежный механизм обнаружения цен, выдержат ли они проверку реальными корпоративными действиями и раскрытием информации или превратятся в игру на деньги, оторванную от фундаментальных показателей — все это еще предстоит проверить временем и рынком.