Recently, when I open my phone, the groups are mostly discussing these things:

Nvidia hits new highs again, and the overall US stock market reaches record highs; the memory sector soars, with SanDisk up more than 4 times this year, Micron achieving its strongest weekly gain since 2008, and even the A-share storage sector takes off.

Group friends simultaneously discuss 'What is the next target to get on board?' and 'Is this a replay of the peak of the dot-com bubble?'

It sounds contradictory, but it's actually the same sentiment: fear of missing out, and fear of a crash.

But in reality, the 'bubble' we are discussing now might not be the real bubble of this AI wave. Or, more accurately, the most dangerous part of this round of AI bubble isn't anywhere you can see when you open your trading account.

A few days ago, OpenAI was exposed as having arranged a stock sale and cash-out transaction for employees in October last year. 75 people cashed out at the maximum cap of $30 million, and the remaining 500+ employees cashed out an average of about $6 million each. The company originally planned to issue $6 billion, but due to too many external investors, it was temporarily increased to $10.3 billion. This round valued OpenAI at $500 billion, more than three times its valuation from six months prior.

This happened last October, but most people only found out in May this year. If it weren't for the Wall Street Journal report, many might still not know. And during these seven-plus months, OpenAI's valuation rose from $500 billion to $852 billion, an increase of 70%.

The memory surge, Nvidia's new highs—these are real, but they are not the most dangerous part of this AI bubble. The real bubble is increasingly happening in places you cannot see or buy.

This time, ordinary people didn't fail to see the bubble. It's that by the time they see the bubble, the most important trades have already been completed.

The valuation finishes rising, and you might not even see it

Yesterday, OpenAI issued a statement on its official website, saying that OpenAI equity cannot be traded privately, and transfers or pledges without written authorization are invalid. The announcement also specifically prohibited several products: packaging equity into shell companies to sell to investors, turning equity into crypto tokens to sell on-chain, and using 'forward contracts' to promise buyers a share of OpenAI's post-IPO gains.

If we compare this to the 2000 dot-com bubble, the biggest difference is that when that bubble burst, Google, Amazon, Yahoo, and various .com companies were already publicly listed. Retail investors could directly buy shares of these companies with P/E ratios of 100 or 200 times in their brokerage accounts. The bubble formed in the public market, and it collapsed in the public market.

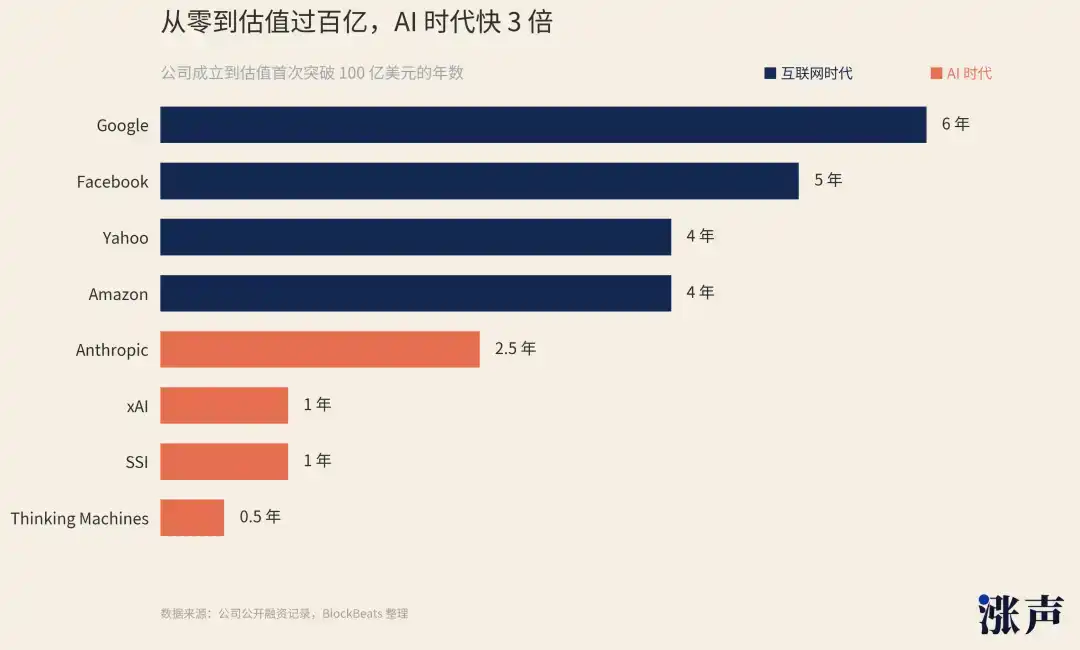

OpenAI's current valuation is $852 billion, compared to $157 billion a year and a half ago. Anthropic's valuation is nearing $900 billion, compared to $61.5 billion a year ago, an increase of more than 10 times. xAI reached a valuation of $250 billion in just three years since its founding. Databricks saw its valuation rise from $62 billion to $134 billion in a year. But none of these numbers, growing faster than a rocket, emerged from the public market.

The process of inflating this round of the AI bubble is happening where the public cannot participate.

Anxiety, unable to find an entry point, seeks substitutes. A while ago, a bunch of media reported that Anthropic's valuation broke through $1.2 trillion, surpassing OpenAI. This number came from an on-chain decentralized pre-IPO platform that packaged Anthropic's equity into crypto synthetic assets for trading (exactly the type of transaction OpenAI prohibited). But this platform's actual 24-hour trading volume is less than $1.4 million, with only a little over three hundred people participating.

What users buy is not actual Anthropic common stock, but an 'anxiety exposure.' This $1.2 trillion is not Anthropic's real valuation; it's more like an outburst of AI anxiety at a liquidity breaking point. Silicon Valley elites understand this anxiety all too well. They even hope for more and larger anxiety so they can sell more anxiety products.

Last month, the well-known Silicon Valley investor Naval launched a fund called USVC, a 'civilian fund' with the concept of allowing ordinary people to invest in AI companies. The fund's portfolio contains shares of the hottest AI companies like OpenAI, Anthropic, and xAI. Non-accredited investors can also buy in, starting at $500.

But it's a closed-end registered fund. The shares are not listed on an exchange. The quarterly buyback limit is 5%, and the board can decide not to buy back. If you dig into the prospectus, you'll also find it expects investors to 'treat the shares as illiquid assets.' Many people on social media directly called it a 'dump fund.'

The surge in the memory sector also follows this logic. The Mag 7, especially Nvidia, are already too expensive. OpenAI and Anthropic are out of reach, but you can still buy into targets along the AI industry chain: chips, memory, power, even helium, copper, silver.

The bubble you see and talk about in the public market is actually more like capital anxiety spilling over from the private market.

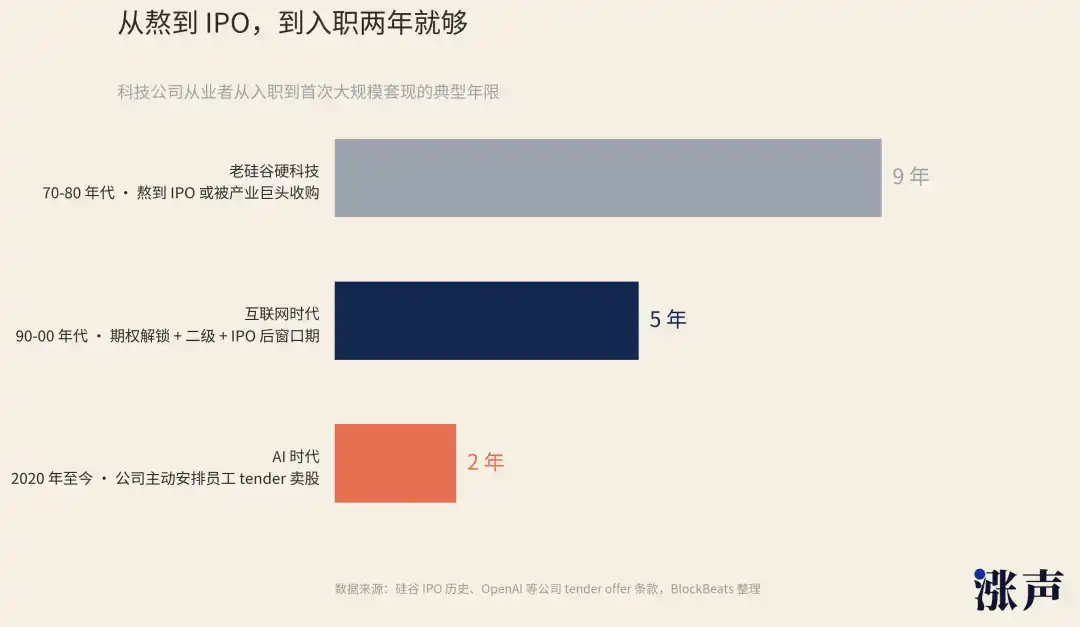

Cashing out is like breathing; exiting doesn't require waiting for an IPO

In the old Silicon Valley hard tech companies, employees had to endure 7 to 10 years to get cash, either waiting for an IPO or to be acquired by an industry giant. After the internet era, this cycle was compressed to about 5 years. Option vesting, secondary market transfers, post-IPO lockup periods—wealth distribution began to have multiple nodes, but IPO was still the biggest one.

In the AI era, cashing out has been thoroughly moved forward to the pre-IPO stage.

OpenAI's recent stock sale threshold for employees is only two years. ChatGPT was released in November 2022. Employees who joined after that started unlocking their stock sale eligibility in the second half of 2024, just in time for that $6.6 billion cash-out in October last year.

It's not just internal at OpenAI. Founders and core teams of AI companies are using new ways to exit early, without needing acquisition or an IPO.

Google's acquisition of Character.AI in 2024, by old Silicon Valley standards, wouldn't even be considered a real acquisition. Google didn't buy the whole company but spent $3 billion to obtain the technology usage rights of Character.AI, with $2.5 billion used to pay out existing Character.AI shareholders and the remaining $500 million as a technology licensing fee.

Simply put, it's technology licensing plus team migration. The company itself remains, but the most valuable people and the most critical technology have already exited through a non-public transaction. The two co-founders of Character.AI hold over 30% of the company's shares. This single deal could net them nearly $1 billion.

Similar cases include Microsoft acquiring Inflection AI, spending $650 million to license the technology and directly hiring the founders and core team. Amazon also used this method to acquire Adept AI.

The US Federal Trade Commission (FTC) launched an investigation into such deals in early 2025, focusing on whether big companies were using this structure to avoid merger review. But all the 'acquisitions' mentioned above happened in 2024, without regulatory review and without needing to put valuations on a prospectus.

From a primary market perspective, today's AI doesn't even need comparison with the internet bubble back then because the heat has already exceeded it by several orders of magnitude.

AI startups casually raise funding rounds starting in the tens of billions of dollars. Most crucially, teams and founders don't need to wait for an IPO to exit. The money in the private market alone is already more than enough, and the ways this money enters the pockets of employees and founders are increasing and becoming more concealed.

Before last October's employee stock sale, OpenAI had conducted two similar internal transactions. Large unicorns like Anthropic and Databricks have also done this. AI companies no longer need to wait for an IPO; they can have 'exit windows' periodically.

Founders have their own channels too. 'Founder-led secondary' transactions are popular in Silicon Valley now, where entrepreneurs sell part of their equity without leaving the company. They can enjoy the continued rise in the company's valuation while also getting cash early.

Or they can take out loans secured by their equity. A company called Pluto specializes in this, helping AI founders and early investors use their private equity holdings as collateral to get cash, with loan-to-value ratios of 20% to 35%. No need to sell shares; just get the cash directly.

Early investors don't need to wait for the company's IPO to deliver returns to LPs. They can have the original VC firm set up a new fund, sell the star assets from the old fund to the new fund, and old LPs can choose to cash out or continue holding through the new fund. This method is called a 'GP-led continuation fund.' In the first half of 2025, the scale of such deals was nearly $50 billion, double that of 2024.

Another indirect exit method is starting a new company. Among the companies founded by people who left OpenAI, at least 7 have become unicorns, with Anthropic, Thinking Machines Lab, and SSI being representatives of this wave. The original team leaves, reassembles, raises funds again—a single departure triggers a new round of wealth distribution.

Every exit method mentioned above doesn't require regulatory review or putting valuations on a prospectus. AI is the biggest beneficiary because many quality AI assets cannot IPO for now.

AI Infrastructure is More Like the Real Estate Bubble

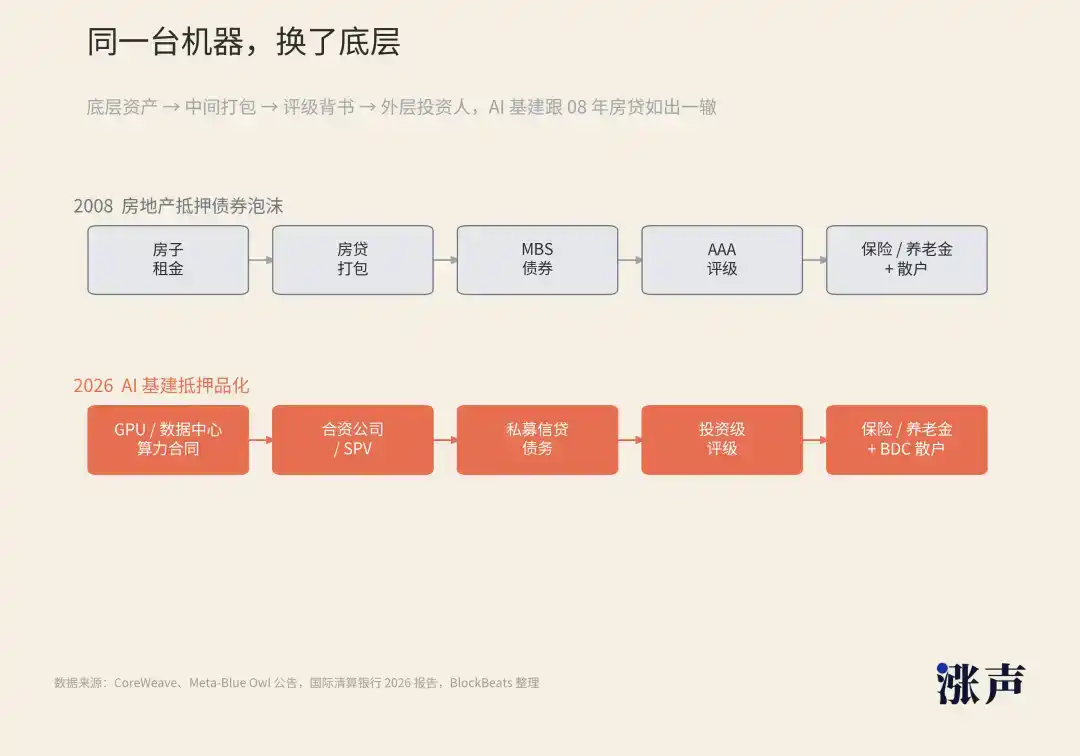

Many people compare today to the 2000 internet bubble, but that comparison is off. The current AI bubble is actually more like the 2008 real estate bubble.

In the 2008 subprime mortgage crisis, the houses were real, the rents were real, but housing prices, loans, ratings, and securitization were all built on the same overly optimistic expectations. The result was Lehman Brothers collapsed, and mortgage-backed bonds became worthless.

Now, similar financialization is happening with AI data centers, GPUs, and compute contracts, and on an even larger scale.

AI training and inference require data centers. Data centers require land, electricity, water, cooling, networks, and long-term clients. So data centers are no longer just the backend server rooms of tech companies; they are assets competed for by real estate funds, private credit, and insurance funds.

Meta announced a partnership with Blue Owl last year to develop the Hyperion data center in Louisiana, with a total development cost of $27 billion, enough to build about 30 Shanghai Towers. Funds managed by Blue Owl hold 80%, a large portion raised through private debt issuance. Meta holds 20%, contributes land and construction in progress, and then signs a 4-year operating lease with the joint venture, plus a 16-year residual value guarantee. If the lease is not renewed at expiry, Meta compensates based on the data center's value at that time.

Meta didn't simply say 'I'm going to spend $27 billion to build a data center.' It turned the data center into a joint venture, turned capital expenditure into a lease, turned residual value into a guarantee, and then sold part of the project as debt to private bond investors. This logic is identical to mortgages being packaged into financial derivatives in 2008.

CoreWeave is another typical case. In 2023, it completed $2.3 billion in debt financing, using Nvidia chips as collateral. In 2024, it signed $7.5 billion in debt financing, led by Blackstone. In 2026, it completed $8.5 billion in GPU-backed financing, receiving an A3 investment-grade rating from Moody's—the first-ever investment-grade-rated GPU-backed financing.

And it's not just CoreWeave. Lambda completed $1 billion in senior secured credit this year; Crusoe secured $750 million in credit from Brookfield, plus $11.6 billion for building OpenAI's Stargate compute factory. Broadcom is reportedly also negotiating a $35 billion AI chip financing deal with Apollo and Blackstone.

Each one is turning AI compute assets into financeable, pledgeable credit products.

Regulators have already named this. The Bank for International Settlements, in its 2026 report, called this structure 'shadow borrowing.' Tech giants hold data center assets through joint ventures and SPVs, assume debt in the form of long-term leases and guarantees, but this debt doesn't appear on their balance sheets. They borrow money to buy GPUs and build data centers while waiting for the GPUs to depreciate. And the borrowed money has long terms, while GPU depreciation is fast.

The bubble risk on this path doesn't actually need this wave of AI to validate; the recent private equity fund turmoil was a preview.

In 2020, private equity firm Vista Equity bought an online technical training SaaS company called Pluralsight for $3.5 billion. Its creditors were all top players in private credit: Blue Owl, Ares, Goldman Sachs, BlackRock. By 2024, Pluralsight couldn't sustain itself, and Vista had to 'hand over' the entire company to the creditors, with Vista and co-investors losing $4 billion.

The reason it couldn't sustain wasn't 'how much money the company is making now,' but 'how stable the company's future subscription renewal revenue will be.' When AI changed the renewal logic of the software market, all 'seemingly stable cash flows' needed reinterpretation. The moat of SaaS private credit suddenly turned from water to sand.

Blue Owl, which lent to Pluralsight, is one of the top players in private credit. Earlier this year, its OCIC private credit fund faced 40% redemptions from retail investors due to AI's impact on SaaS. But even so, Blue Owl continues lending for AI data centers. Besides the Meta data center mentioned earlier, it's also a major financier behind OpenAI's Stargate compute project.

The most dangerous aspect of private credit is that its opacity can cause widespread valuation distortions. External investors have no way to verify the fund's underlying assets.

In August last year, BlackRock's private credit division HPS was defrauded of over $400 million by an Indian-born telecom entrepreneur using fake invoices. HPS lent to several telecom companies under this entrepreneur, with the collateral being these companies' customer accounts receivable. It was only when an HPS employee noticed issues with the customer email addresses that the entire collateral was discovered to be non-existent.

If a top player like BlackRock can't even clearly see if the money it lent out has real collateral, how much can the investors buying its fund shares possibly know?

All these AI data center financings, GPU-backed loans, new SPV structures are built on one assumption: the underlying assets are valuable.

But how fast do GPUs depreciate? Will data center client contracts renew? Will AI inference demand materialize enough to support this compute? Even the agencies rating these assets and the banks underwriting the funds can only give judgments 'based on available information.' Ordinary investors see only a prospectus, a rating report, and a name.

The Real Bubble Doesn't Necessarily Quote You First

Back to the opening question, 'What is the next target to get on board?'

What most people can get on board with now is essentially the shadow cast by the core assets. The 2000 internet bubble peaked in the public market and crashed in the public market. You could see it, feel it, read about that day in the news.

This time, the most bubbly, most dangerous part is happening where you can't see it. By the time you see these, the most important trades have already been completed.