Author: Zen, PANews

In February 2026, when Coinbase's advertisement flickered once again on the giant LED screens of the Super Bowl, flashing the slogan "Crypto. For everybody." to the tune of a Backstreet Boys classic, the audience reacted with a mix of sighs and criticism, a stark contrast to the frenzy of the night four years prior, which was dubbed the "Crypto Bowl."

Back then, the FTX logo was still prominently displayed above the Miami Heat's arena. Crypto companies were waving massive checks, attempting to buy decades of mainstream trust in just a few days. However, the subsequent collapse, lawsuits, and the farce of the arena's name change turned this "attention experiment" into one of the most expensive jokes in sports history.

On the surface, it was a branding business, but in essence, it was more like a stress test: when sponsorships embed financial narratives into the daily lives of fans and viewers, trust is amplified. This was fundamentally a long-term experiment in "how high-risk financial products leverage high-trust public institutions to gain attention and legitimacy."

Crypto Company Sponsorships: Setting Sail from the Era of 'Big Money Splashing'

In 2021, with the emergence of a phenomenal bull market, rapidly profit-absorbing cryptocurrency companies began to aggressively penetrate the sports and cultural spheres. Cryptocurrency exchanges and blockchain projects started plastering their brands onto the most expensive, most visible public attention gateways: top leagues, major venues, and global sports broadcasts.

In March of that year, Miami-Dade County reached a 19-year naming rights agreement with FTX, renaming the Miami Heat home court to FTX Arena. This deal, which wrote a crypto company into the narrative of an urban landmark, marked the first large-scale entry of crypto advertising into mainstream urban public space narratives.

In the summer of the same year, Crypto.com reached a fight kit-level partnership with UFC, reportedly valued at around $175 million over 10 years, as disclosed by CNBC. In traditional sports, this level of sponsorship is one of the core commercial assets. Then, in October, Coinbase reached a multi-year official partnership with the NBA/WNBA, with its logo prominently displayed on the base of the basketball hoop.

In November, the news of Staples Center being renamed Crypto.com Arena further amplified this breakout. This arena is not only the home of the prestigious Los Angeles Lakers but also a super landmark for performances, music, and the entertainment industry in Los Angeles. This naming rights deal directly tied the crypto brand to the center stage of sports and pop culture.

During the same period, European football also began to quickly integrate, with Binance becoming the main shirt sponsor for Lazio, promoting fan token narratives and interactive benefits, merging exchange sponsorship with Web3 product conversion into a single commercial chain.

Entering 2022, this curve continued to rise and peaked at the global event level. Crypto.com not only became the global partner of the F1 Sprint series but also secured the title of official sponsor of the 2022 Qatar World Cup, marking the first time a crypto company officially entered the传播体系 (communication system) of the world's largest single sporting event with near-universal coverage.

The crypto industry's massive marketing offensive soon reached an inflection point at the end of 2022. The collapse of FTX quietly turned naming rights into a liability. In January 2023, a bankruptcy judge officially terminated the naming rights deal between Miami-Dade County and FTX, and the venue subsequently entered a process of de-FTX-ification and re-solicitation for sponsorship. This event also became a negative典型案例 (typical case) in the history of sports and cultural sponsorship.

After 2023, the industry as a whole entered a phase of contraction and re-evaluation. Many collaborations scaled back from venue naming rights and top-tier event sponsorships to more easily quantifiable ROI forms like sleeve patches, training kit sponsorships, digital content rights, and fan engagement activities. Sponsors also placed greater emphasis on compliance and sustainable exposure.

In football, OKX's partnership with Manchester City is an example of this more controlled version: starting as an official training kit partner in 2022 and later upgrading to the higher-exposure sleeve patch sponsorship. Its path resembles the gradual升级 (upgrade) of traditional sponsorship rather than an all-in gamble. From a macro-narrative perspective, the main theme of this stage was no longer ubiquitous crypto ads but rather how sports and cultural institutions re-priced the balance between新增收入 (new revenue) and reputational and compliance risks.

In the past two years, a more subtle change has emerged in this trend. Crypto sponsorships haven't disappeared but are increasingly repackaging their relationship with the mainstream using stablecoins, compliant products, and brand credibility.

For example, the 2025 partnership between the Aston Martin F1 team and Coinbase was described as the first publicly announced case of a sponsorship fee being settled entirely in stablecoins. Coinbase's appearance in the 2026 Super Bowl, with its closing slogan "Crypto. For everybody.," demonstrated its attempt to pull cryptocurrency from its early niche circles back into the mainstream narrative of "participation for all."

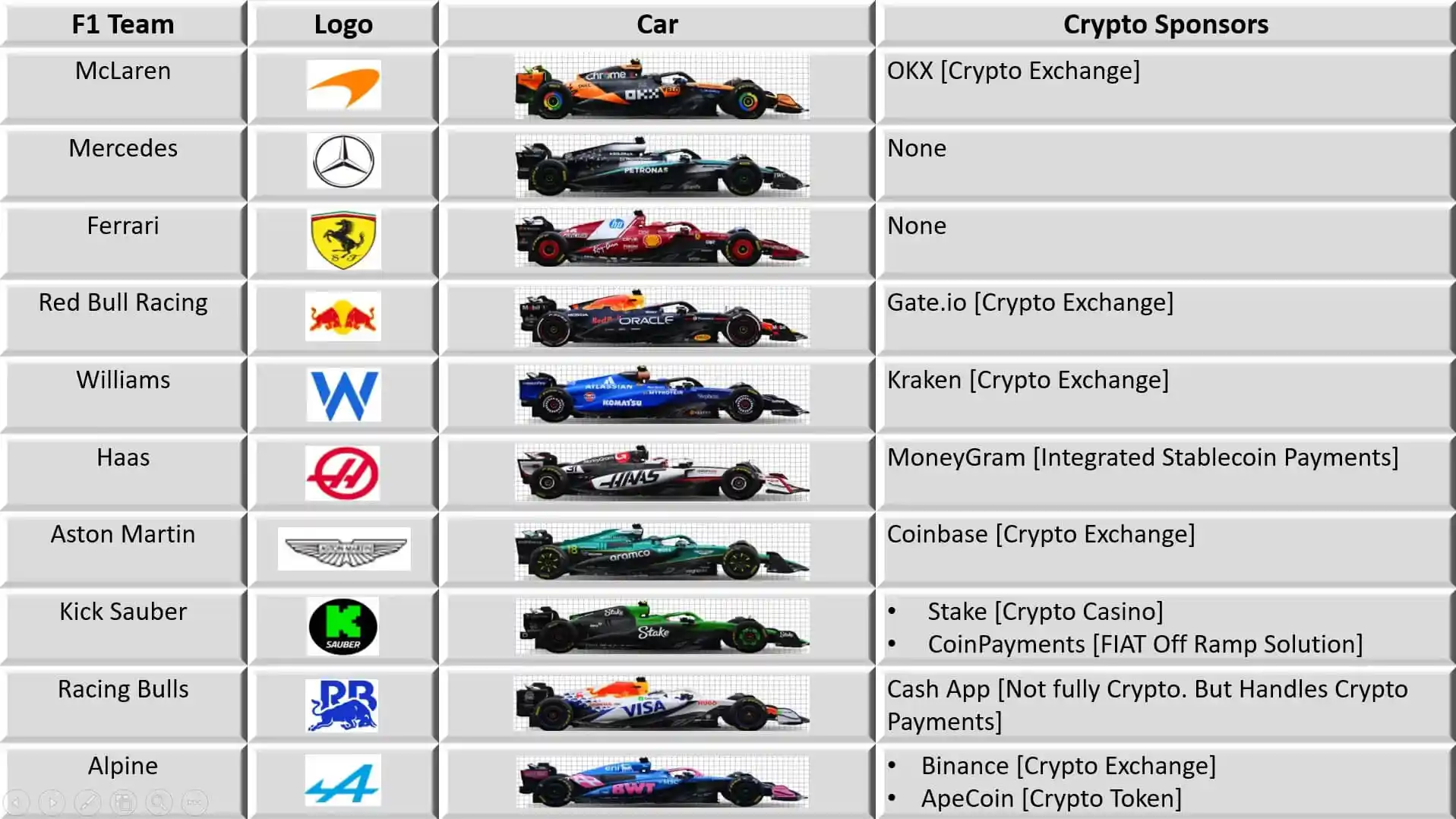

And this year's F1 season is about to start in March. Last year, the cryptocurrency industry spent $174 million on F1 sponsorship projects alone. This year, cryptocurrency sponsorship has reached a new high: 9 companies sponsor a total of 11 teams.

Exposure, Traffic Acquisition, and Criticism

Among the various advertisements and sponsorships of crypto companies, the exposure and conversion effectiveness of medium to long-term cooperation are difficult to estimate. However, in one-off investments like the Super Bowl, the early results were very significant.

In 2022, on Super Bowl Sunday, Coinbase's installs increased by 309% week-over-week, and by another 286% the next day; eToro saw increases of 132% and 82% respectively; FTX saw increases of 130% and 81% respectively. Coinbase's QR code advertisement caused the app to crash or experience access anomalies due to the massive influx of users scanning it. This indicates that the short-term conversion power of Super Bowl ads确实存在 (does indeed exist), at least in terms of generating peaks in downloads and activations.

However, this kind of explosive growth does not automatically translate into long-term retention, asset沉淀 (accumulation), or compliant operational capabilities. On the medium to long-term level, the hidden costs of sponsorship often materialize集中 (concentratedly) during periods of tightening regulation and enforcement cycles.

Taking the partnership between Premier League club Arsenal and Socios for fan tokens as an example, the UK Advertising Standards Authority (ASA) ruled in 2021 against the related promotional content, stating that the advertisement downplayed high-risk decision-making in the context of crypto assets and did not sufficiently highlight key risk information such as taxes. It ultimately required that the ads not appear again in the complained-about form and that the club adjust the presentation of pages and risk warnings.

As the world's number one sport, football has always been a favored traffic入口 (entry point) for crypto companies. Compared to the crypto industry giants willing to invest heavily, the companies flooding into football leagues and clubs are also more complex, generating more controversy and negative impacts.

In 2024, a book titled "No Questions Asked: How football joined the crypto con" was published, describing football's embrace of crypto sponsorship as a collective dereliction of duty driven by greed and侥幸 (wishful thinking) with almost no due diligence, resulting in fans being treated as an outlet for high-risk, low-regulation financial products, while clubs often offered no apology, explanation, or commitment to improvement after blow-ups.

At the level of sports and the arts, the core矛盾 (contradiction) is that organizations, under financial pressure, introduce high-risk sponsorships, potentially binding their own reputation to the counterparty's credit. Sports sponsorship research categorizes this damage into operational risk and reputational risk: once the sponsor blows up or faces major controversy, the sponsorship asset turns from a "credit enhancement tool" into a "liability."

Expanding to a sociological perspective, the controversy centers on crypto companies leveraging the emotional communities of sports and culture (fans, music lovers, movie buffs) to lower the participation threshold, packaging highly volatile assets as identity, interest, and trends, thereby amplifying FOMO and herd diffusion.

In the case of the Floki Inu London Underground advertisement, the UK ASA clearly stated that it "took advantage of consumers' fear of missing out and trivialized the risk," making it a typical expression of regulatory language. Collaborations with film festivals, art fairs, and awards also serve similar functions, but this "cultural legitimization" is not equivalent to financial suitability. It更像 (is more like) a conversion of symbolic capital: replacing risk explanation with cultural authority, and product understanding with brand association.

Regulation and Enforcement Gradually Catching Up

Faced with the expansion and controversy of crypto sponsorships in the cultural and sports fields, regulatory agencies are gradually补全 (completing) the rules.

In the UK, financial regulators announced in 2023 that starting October 8th, stricter requirements would be imposed on crypto asset marketing targeting UK consumers, including a首次 (first-time) investor cooling-off period, strengthened risk warnings, and a clear ban on inappropriate incentives like referral rewards.

The ASA, through密集 (dense) rulings, applied standards such as "whether risk display is sufficient," "whether it exploits inexperience," and "whether it encourages buying on credit" to specific copy and placement scenarios, and in 2026 expanded the scope of review to "whether crypto is packaged as a solution to real financial problems."

In the US, consumer protection agencies updated guidelines on "disclosure obligations for influencers and advertisers" from an advertising and anti-fraud perspective, releasing an updated version of the endorsement guidelines in 2023 to address platform-based distribution and influencer marketing;同时 (simultaneously), they used data bulletins to reveal the high incidence of crypto scams, strengthening public education and platform governance pressure. Futures and derivatives regulators continued to publish digital asset risk education materials to prevent the public from falling into related fraud entry points.

In the EU, the MiCA framework explicitly requires in its official summary that relevant service providers communicate with potential holders in a fair, clear, and non-misleading manner,配合 (coupled with) consumer risk warnings and reminders of authorization/regulatory boundaries. EU regulators have also issued risk warnings for consumers. With the rising influence of financial content on social media, EU securities regulators have also issued fact sheets for "finfluencers," emphasizing the必须 (must)显著 (prominently) disclose compensation and利益关系 (interest relationships), and that hidden labels cannot be used to弱化 (weaken) the advertising attribute.

The effectiveness of the above regulatory frameworks is reflected in three points: First, the minimum standards for risk disclosure in advertising text are being raised, especially in UK adjudication practice; Second, the disclosure obligations for celebrity endorsements are shifting from "moral expectations" to enforceable rules; Third, cross-border platform distribution is being纳入 (brought into) the regulatory narrative (even if an ad is produced overseas, it may be subject to regulation if targeted at domestic consumers).

But the regulatory空白点 (gaps) remain equally clear. The legal ambiguity of many tokens or experiential rights means regulation can only address surface-level issues based on whether there is misleading information or inadequate disclosure.

Sponsorship contracts are contractual transactions between companies and clubs, relying核心 (corely) on the parties to约定 (stipulate) terms themselves. Regulation typically finds it difficult to directly impose unified "naming rights" risk control standards for such commercial transactions; intervention更多 (more often) comes from angles like advertising compliance and consumer protection.