Автор: Eli5DeFi

Компиляция: AididiaoJP, Foresight News

Если смотреть из 2024 года, майнинг биткоинов напоминает борьбу выживальщиков, которым приходится справляться как с халвингом биткоина, так и с остаточными холодами «криптозимы».

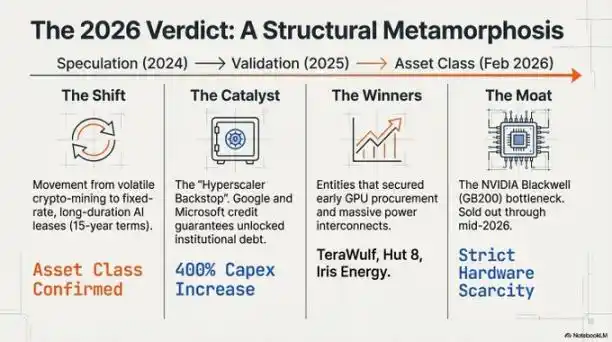

Но к началу 2026 года это представление полностью изменилось. Отрасль претерпела фундаментальную трансформацию, превратившись из спекулятивного аванпоста вычислительных мощностей в краеугольный камень новой эры — «фабрики искусственного интеллекта».

Движущей силой этого изменения стала жестокая борьба за ресурсы.

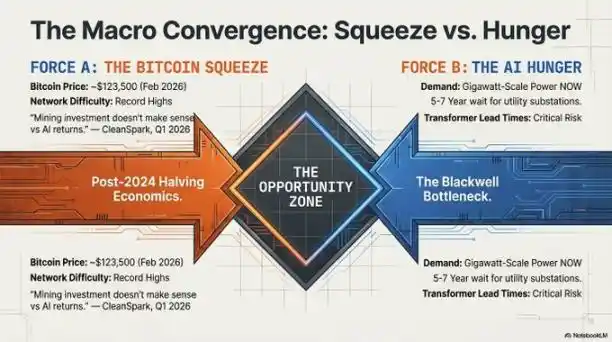

Поскольку глобальный спрос на вычислительные мощности ИИ достиг пика, узкое место сместилось с «нехватки чипов» на «нехватку электроэнергии». Высокопроизводительные вычисления требуют того, что нельзя скачать или быстро произвести: уже electrified землю.

Те майнеры биткоинов, которых когда-то высмеивали за волатильность и ненадежность, успешно превратили захваченные ими примерно в 2021 году земельные и энергетические ресурсы в инфраструктурный монопольный капитал 2026 года, превратившись в незаменимых «землевладельцев» в золотой лихорадке ИИ.

Великий вычислительный переворот

В реалиях 2026 года электроэнергия стала новым дефицитным ресурсом.

Главным «физическим рвом», защищающим победителей в отрасли, являются точки подключения к электросетям коммунальных предприятий. Теперь строительство новой подстанции занимает от 5 до 7 лет, и те electrified святые места — старые майнинговые фермы, уже подключенные к сети — стали единственными местами, способными удовлетворить немедленные потребности в обучении передовых моделей ИИ.

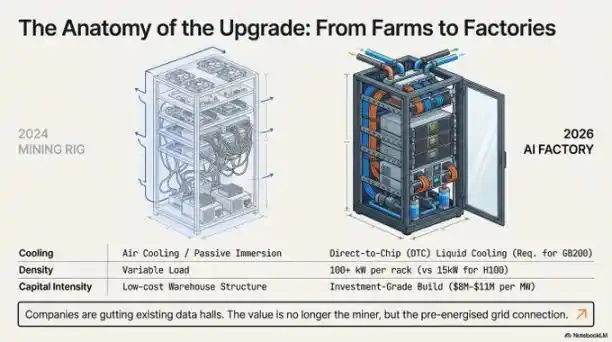

Однако входной барьер превратился из простого «захвата земли» в капиталоемкие крепости. Из-за требований к высокоплотному жидкостному охлаждению и глобального дефицита трансформаторов стоимость строительства объекта, готового к работе с ИИ, взлетела до примерно 8-11 миллионов долларов США за мегаватт. Этот высокий барьер капитальных затрат провел четкую разделительную линию между «лидерами исполнения» и другими игроками:

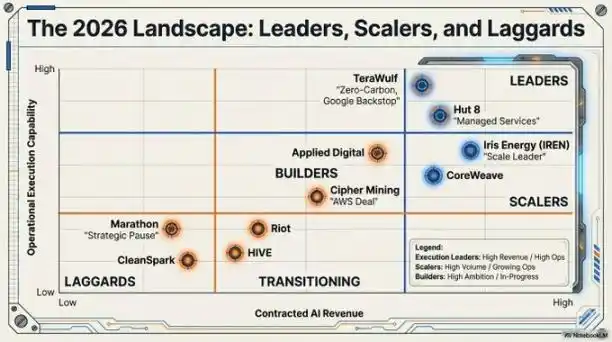

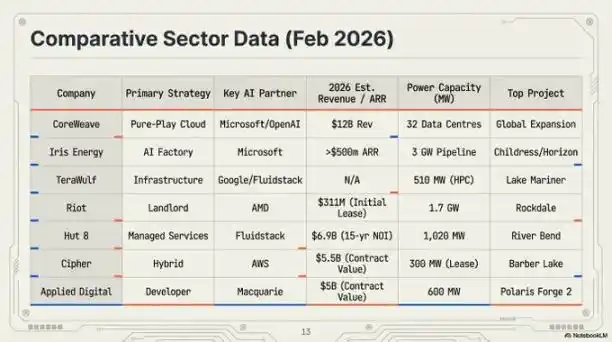

- Iris Energy (IREN): Отраслевой лидер по масштабу, оценка в 14 миллиардов долларов. Владеет портфелем энергии и земли мощностью 2910 МВт, поддерживающим его расширяющуюся «AI-фабрику».

- Riot Platforms: Имеет одобренную электрическую мощность в 1,7 ГВт. Riot превратила свои активы в «Техасском треугольнике» в стратегические центры размещения, недавно заключив знаковый договор аренды с AMD.

- TeraWulf и Hut 8: Признанные лидеры исполнения. Эти компании заключили контракты на 6,7 и 7 миллиардов долларов соответственно, успешно преобразовав майнинговые фермы в высокоценные активы для ИИ, соответствующие инвестиционному уровню.

«Гарантия гиперскейлеров» — конец волатильности криптовалют?

Возможно, самым глубоким изменением стала структурная переоценка бизнес-модели, ставшая возможной благодаря «кредитному усилению».

Раньше ведущие финансовые институты не хотели давать майнерам кредиты из-за высокой волатильности цены биткоина. Это изменилось с появлением «гарантий гиперскейлеров».

Через «соглашения о признании» такие гиганты, как Google и Microsoft, теперь предоставляют финансовые гарантии по арендной плате, которую платят эти бывшие майнеры.

Таким образом, некогда рискованные арендные контракты майнеров превратились в низкорисковые контракты с кредитным рейтингом tech-гигантов. В результате отрасль получила доступ к рынку облигаций с льготной ставкой около 7,125%. Такие компании, как Cipher Mining и Hut 8, смогли получить от J.P. Morgan и Goldman Sachs финансирование проектов без разводнения акций, покрывающее до 85% стоимости проекта. Эта модель «арендодателя» с условиями «бери или плати» привлекла значительный приток капитала от таких институциональных инвесторов, как Vanguard, Oaktree и Citadel.

Реальность Blackwell и подводные дата-центры

Технические требования ИИ в 2026 году сделали старые конструкции майнеров с воздушным охлаждением не только устаревшими, но и совершенно непригодными для развертывания высокоплотных кластеров ИИ.

Платформа NVIDIA Blackwell GB200 NVL72 с потреблением 120 кВт на стойку заставила отрасль перейти на жидкостное охлаждение непосредственно до чипа.

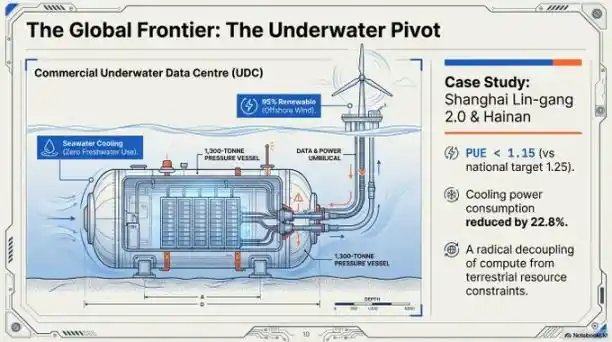

Чтобы одновременно решить проблемы охлаждения и нехватки земли, отрасль обратила взгляд на «голубую экономику». Шанхайский проект Lingang 2.0 стал образцом подводного дата-центра коммерческого масштаба.

- Технические показатели: PUE (эффективность использования энергии) объекта составил 1,15, что значительно превышает национальную цель в 1,25. Он использует морскую воду в качестве основного источника охлаждения, снижая общее энергопотребление на 40-60%.

- Точное развертывание: С помощью судна «Sanhang Fengfan» с GPS-наведением эти подводные модули весом 1300 тонн могут погружаться с нулевой погрешностью, питаясь от оффшорной ветровой энергии, полностью摆脱 (освобождаясь) от ограничений наземных ресурсов.

«Ров Blackwell» и держатели оборудования

К 2026 году «стена供应链» (цепочки поставок) укрепила отраслевую иерархию. Поскольку чипы архитектуры NVIDIA Blackwell были распроданы до середины 2026 года, заказы, размещенные компаниями в 2024 году, стали их конкурентным преимуществом.

Без чипов электричество бесполезно; без электричества чипы — просто кирпичи. Победителями стали те, кто рано заблокировал и энергию, и чипы.

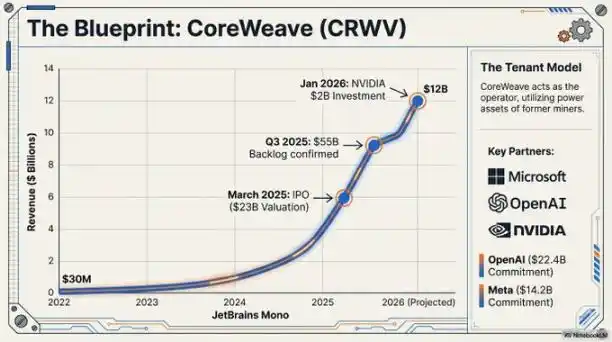

CoreWeave готовится к IPO с оценкой в 35 миллиардов долларов, опираясь на свои огромные заказы на оборудование, включая крупный заказ на 22,4 миллиарда долларов от OpenAI. Те, кто опоздал и не успел заказать чипы в период окна возможностей 2024 года,基本上 (в основном) оказались заблокированными вне核心 (ядерного) рынка инфраструктуры ИИ.

«Накопленные заказы на архитектуру Blackwell в 3,6 миллиона единиц фактически блокируют newcomers (новичков) вне первичного рынка инфраструктуры ИИ, и эта ситуация в обозримом будущем вряд ли изменится». — Джексон Хуанг, генеральный директор NVIDIA, 2026 г.

За пределами майнеров

Превращение из «фабрики биткоинов» в «узел цифровой инфраструктуры ИИ» знаменует собой созревание некогда маргинальной отрасли и ее интеграцию в глобальную промышленную политику.

Изолированная, чисто майнинговая модель подходит к концу. Ей на смену приходят промышленные энергетические компании. Они рассматривают вычисления — будь то алгоритм SHA-256 для биткоина или обучение больших языковых моделей — как взаимозаменяемый продукт своих основных энергетических активов, распределяемый по мере необходимости.

Поскольку эти гигаваттные «AI-фабрики» становятся постоянной частью энергосистемы, мы не можем не задаться вопросом:

Может ли чистая майнинговая модель без диверсификации в бизнес ИИ выжить при такой огромной разнице в доходах на мегаватт? Что более важно, как глобальные энергосистемы адаптируются, когда эти объекты превратятся из гибких потребителей энергии — «майнинговых ферм» — в требующие стабильного питания «базовые нагрузки» ИИ? В то время дата-центры перестанут быть просто потребителями энергии, а станут проектировщиками и архитекторами сетей.

Майнеры изменились, но эта высокорискованная игра энергетического арбитража только начинается.