Оригинал | Odaily Planet Daily (@OdailyChina)

Автор | Azuma (@azuma_eth)

С момента несанкционированного доступа к мостовому контракту rsETH Kelp DAO прошло более 30 часов. Хотя вовлеченные стороны (LayerZero, Kelp DAO, Aave) уже высказались (в основном, перекладывая вину и подчеркивая свою невиновность), окончательное решение пока не предложено.

Поэтому в этой статье мы обсудим текущие позиции и отношение вовлеченных сторон, рассмотрим причины задержки в принятии решения и попытаемся предположить, как в конечном итоге может быть разрешена эта ситуация.

Примечание Odaily: предысторию можно узнать в материале «Снова 292 миллиона долларов украдены в DeFi: теперь и Aave небезопасен?».

Кто же должен нести ответственность?

Сначала обсудим вопрос ответственности.

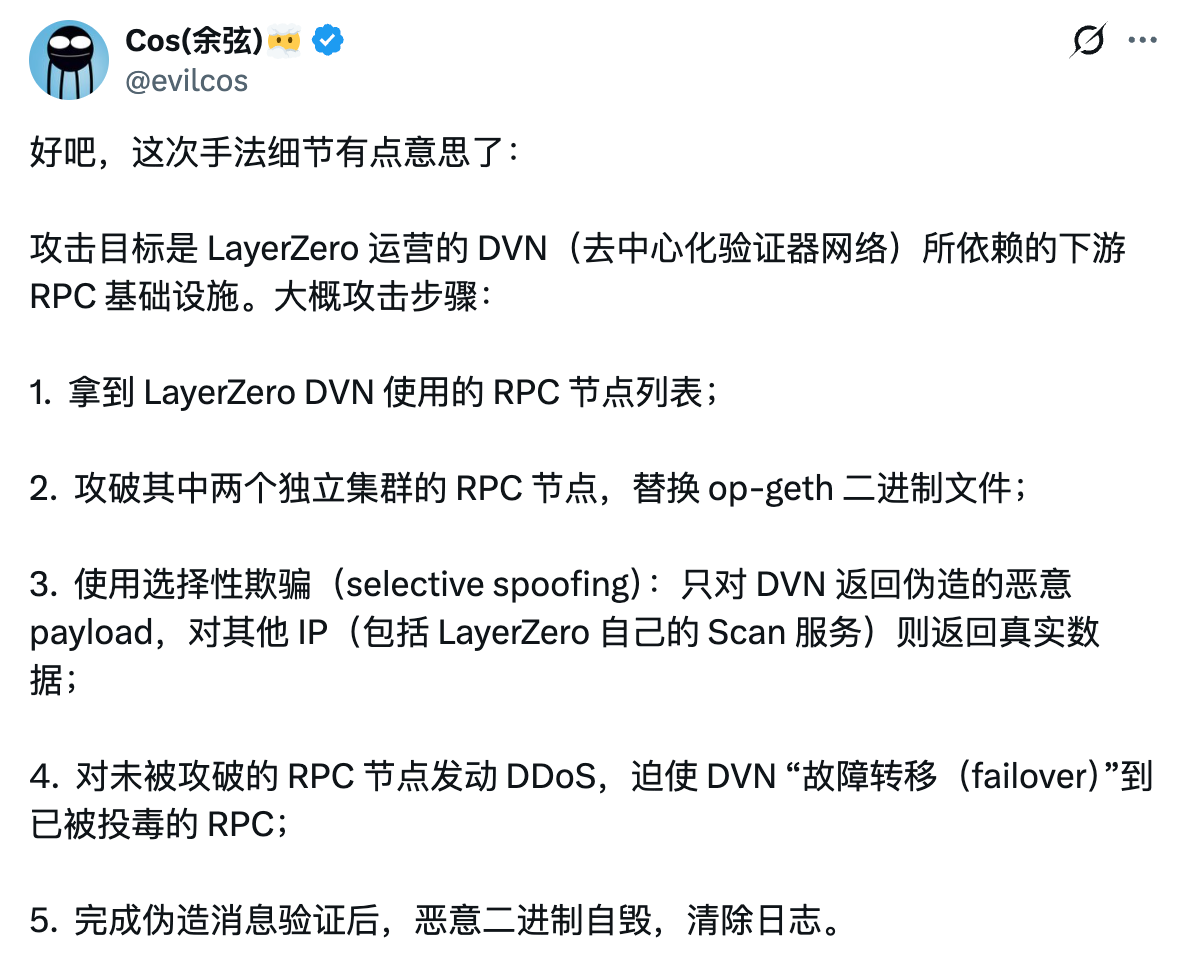

Согласно разъяснениям от LayerZero, непосредственная причина инцидента уже достаточно ясна: была скомпрометирована нижестоящая RPC-инфраструктура, от которой зависит децентрализованная сеть валидаторов (DVN), управляемая LayerZero (см. анализ основателя SlowMist, Юйсяня, на изображении ниже). И поскольку мостовой контракт Kelp DAO использовал конфигурацию 1/1 DVN, злоумышленнику достаточно было подделать одну проверку сообщения для успешной атаки.

LayerZero считает, что Kelp DAO, использовавший конфигурацию 1/1 DVN, является непосредственным виновником данного инцидента. Это очевидно, подобная «единая точка отказа» просто немыслима.

Однако базовый протокол межсетевого взаимодействия LayerZero также должен нести часть ответственности. LayerZero позволяет каждому вышестоящему приложению самостоятельно настраивать количество и порог DVN. Хотя выбор конфигурации 1/1 DVN был самостоятельным решением Kelp DAO, как разработчик базовой архитектуры, следовало бы исключить возможность такой очевидно flawed настройки.

Наконец, кредитные протоколы, такие как Aave (здесь основное внимание уделяется Aave), хотя и являются косвенными пострадавшими, объективно говоря, именно предоставление Aave чрезмерных кредитных полномочий таким активам, как rsETH, в целях экспансии, стало прямой причиной их нынешнего затруднительного положения. Также стоит отметить, что бывшая команда управления рисками Aave, BGD Labs (ныне отделившаяся от Aave), еще в январе прошлого года четко указывала на проблему DVN у Kelp DAO. Kelp тогда принял рекомендацию, но очевидно не внес изменения... То, что Aave не продолжил контроль и не принял соответствующих мер, также аукнулось им самим.

Таким образом, распределение ответственности вполне ясно: основная ответственность лежит на Kelp DAO, LayerZero несет второстепенную ответственность, а у Aave также есть частичная косвенная ответственность.

Неудобная реальность

Реальность всегда сложнее теоретических ожиданий. Ключевая проблема заключается в том, что команда Kelp DAO, несущая основную ответственность, не может найти столько денег, чтобы заполнить дыру... Прямое списание убытков со всех rsETH или удар по держателям токенов в Layer2 — по сути, тупиковый путь.

Тогда у кого есть деньги? Первым является LayerZero, который из-за этого инцидента столкнулся с репутационным кризисом, был временно отключен несколькими учреждениями и протоколами, включая Bitgo, Tron, Ethena, Curve, ether.fi, и рискует потерять значительную долю рынка межсетевого взаимодействия. Вторым — Aave, который столкнулся с потенциальными огромными безнадежными долгами и наблюдает отток TVL на сотни миллиардов долларов.

Так что теперь «скрытые мотивы»各方 очевидны. Основной виновник, Kelp DAO, практически парализован и не способен主导 последующие выплаты, что делать — нужно советоваться с двумя старшими братьями; в то же время LayerZero и Aave, обладающие средствами для выплат и несущие второстепенную и косвенную ответственность, уже заявили, что в их протоколах не было уязвимостей, давая понять, что не собираются просто так брать на себя такую огромную ответственность... Поэтому сейчас ситуация, кажется, зашла в тупик.

Но я не думаю, что это продлится долго, потому что оба протокола заинтересованы в скорейшем решении проблемы — LayerZero не может отказаться от своей экосистемы межсетевого взаимодействия OFT; Aave не может игнорировать продолжающийся отток存量资金.

Ключевой момент博弈各方

Сегодня утром Aave выпустил обновленное заявление по этому инциденту, в котором最重要的的一个信息点在于 — Aave подчеркивает, что «rsETH в основной сети Ethereum имеет полное обеспечение».

Как это понять? Нужно начать с дизайна rsETH.

rsETH по сути является токеном凭证 ликвидности рестекинга, выпускаемым Kelp DAO. Каждый 1 rsETH обеспечен 1 ETH в системе стейкинга и рестекинга по пути «ETH - Lido - EigenLayer - Kelp DAO - rsETH».

rsETH в основной сети — это оригинальный токен凭证, выпущенный Kelp DAO в Ethereum. Затем для экспансии в экосистеме Layer2 Kelp DAO использует мостовой контракт LayerZero (тот самый, с которым произошел инцидент) для отображения основного rsETH в различных Layer2. При выпуске каждого 1 rsETH в Layer2, соответствующий rsETH в основной сети также помещается на хранение в custody контракт Kelp DAO и высвобождается только при возврате rsETH из Layer2 обратно в основную сеть.

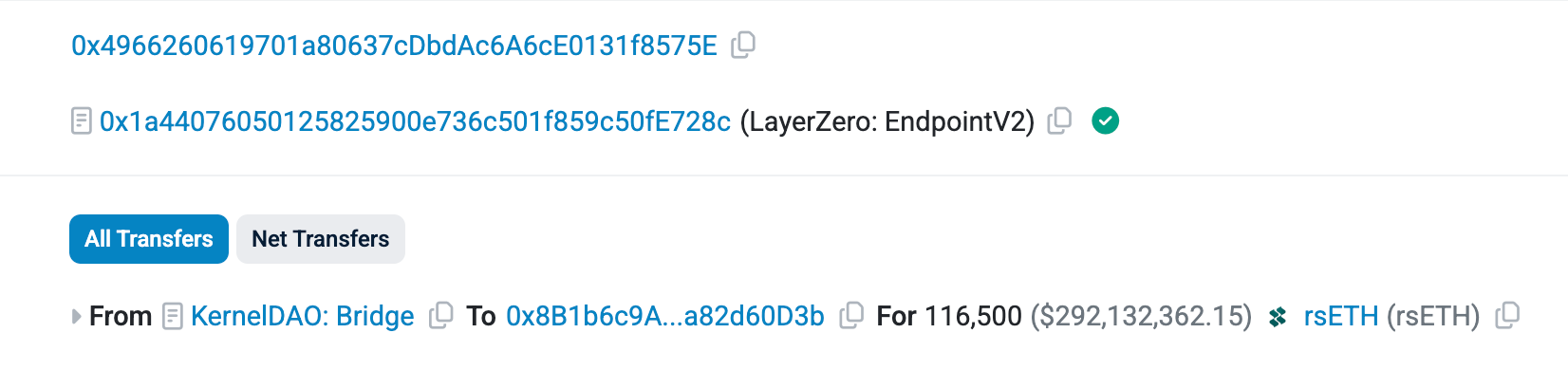

Теперь вернемся к самой атаке. Как упоминалось ранее, причина кражи заключается в том, что хакер обманул DVN, подделав межсетевое сообщение, в результате чего мостовой контракт «ошибочно释放» 116 500 rsETH — обратите внимание, это не создание новых монет из воздуха, а получение из основной сети оригинальных токенов凭证, которые не должны были быть释放.

Проблема именно в этом. Эти токены уже находились в обращении в Layer2 через механизм отображения, в то время как токены в основной сети были заблокированы. Однако после успеха хакера они были внесены в кредитные протоколы, такие как Aave, и использованы для займа более ликвидного WETH, что позволило осуществить кражу — еще раз подчеркиваем, внесенные хакером rsETH были подлинными, поэтому Aave和支持вал их использование в качестве залога.

Теперь вновь посмотрим на заявление Aave, и оно становится весьма интересным. Фраза «rsETH в основной сети Ethereum имеет полное обеспечение» фактически означает: «Эти монеты настоящие, парень из Kelp DAO, ты должен支持нам использовать эти монеты для выкупа лежащего в основе ETH (контракт приостановлен, сейчас выкупить нельзя)... А на те отображенные версии rsETH в Layer2, которые потеряли обеспечение в основной сети, мне плевать!»

Вероятно, такова позиция Aave. Хотя акцент на стоимости основного rsETH подразумевает игнорирование стоимости отображенных версий rsETH в Layer2, и поскольку у самого Aave также есть определенные долговые позиции по rsETH в своих кредитных продуктах на Layer2 (текущий объем составляет 359 миллионов долларов), это также создаст некоторый безнадежный долг. Но из двух зол выбирают меньшее. Aave, вероятно, оценил потенциальное влияние двух вариантов и решил, что защита核心产品 основной сети больше соответствует его интересам.

Но это всего лишь заявление одной стороны, Aave. То, как в конечном итоге будет решена проблема, зависит от того, удастся ли достичь согласия с LayerZero и Kelp DAO.

Хотя последние пока не сделали further заявлений, я лично считаю, что LayerZero будет трудно принять этот план, поскольку отказ от отображенных токенов Layer2 напрямую угрожает репутации LayerZero в межсетевом взаимодействии.

Потенциальные решения

Проблему в конечном итоге нужно решать. Последние два дня различные大佬 в социальных сетях дают советы Aave, LayerZero и Kelp DAO.

Основатель DefiLlama 0xngmi проанализировал три возможных пути, но также отметил, что у всех трех есть очевидные недостатки. Первый путь — все держатели rsETH совместно несут списание стоимости на 18.5% (соотношение украденных токенов к выпущенным), Kelp DAO сам несет ответственность, а Aave также必须承担大约 2.16 миллиарда долларов безнадежных долгов в основной сети; второй путь — игнорировать стоимость всех отображенных версий rsETH в Layer2, что позволит сохранить продукт Aave в основной сети, но экосистема Layer2, вероятно, рухнет, а репутация Kelp DAO сведется к нулю; третий путь — произвести полное возмещение держателям rsETH на момент снимка состояния до атаки, а последующие покупатели или те, кто передал токены, несут убытки самостоятельно, но из-за значительного движения средств после атаки это практически невозможно осуществить.

Основатель OneKey Yishi сказал: «Сейчас лучший результат — это договориться с хакером, предложить 10–15% вознаграждения (bounty), вернуть основную часть, и все будут довольны. Если договориться не удастся, то фонд экосистемы LayerZero должен внести основную часть, у него больше всего денег и долгосрочных интересов, заплатив, он сможет сохранить экосистему OFT. Kelp DAO самый бедный, либо компенсирует токенами и будущими доходами, либо干脆整个项目打包卖给 LayerZero или Bitmine. Umbrella и stkAAVE от Aave покрывают последний слой, но вкладчики WETH绝对不能 понести списание стоимости, иначе Morpho, Spark, Fluid, Euler все будут переоценены, весь сектор LRT будет занесен в черный список, и вся индустрия DeFi откатится на три года назад.»

Так или иначе, сторонам肯定是要继续 спорить некоторое время, ведь речь идет о сотнях миллионов настоящих денег, и никто не хочет быть тем, кого больше всего надурили.

Что касается того, сколько еще времени потребуется для предложения решения, как упоминалось ранее, двум гигантам不敢拖太久. LayerZero сейчас принудительно поставлен на паузу крупными合作机构 и протоколами, и если затянуть, эти партнеры肯定 переключатся на другие межсетевые пути; ситуация с Aave также不容乐观, использование нескольких пулов достигло 100%, вкладчики оказались в «ловушке»... Если ETH突然 резко упадет, Aave,很可能 из-за невозможности эффективного清算 (сейчас это действительно так), столкнется с еще большим количеством безнадежных долгов, что в конечном итоге усугубит проблему, как снежный ком —如果真的到了这一步, могут пострадать основы отрасли, и очевидно, никто не захочет看到这种情况.