Стейблкоины контролируют 60% выручки, но сталкиваются с «ликвидацией» из-за снижения процентных ставок

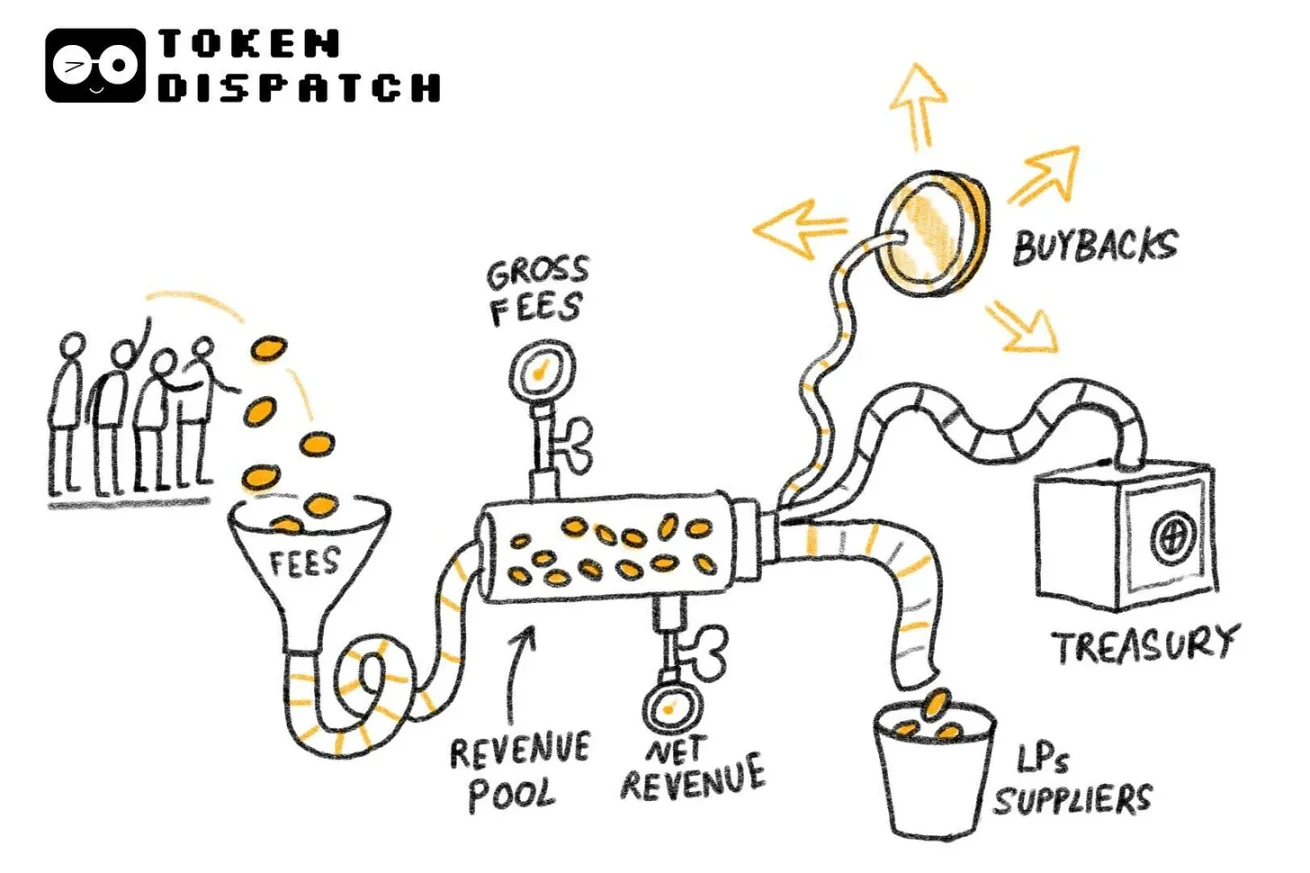

Анализ доходов криптоиндустрии за 2025 год показывает, что стейблкоины доминируют, генерируя 60% выручки, однако их модель доходности уязвима к снижению процентных ставок ФРС. Децентрализованные биржи перпетуальных контрактов (perp DEX), такие как Hyperliquid, стали ключевым новым игроком, заняв 7-8% рынка благодаря низкому трению и высокой ликвидности. Три основных драйвера доходов: спреды (стейблкоины), исполнение сделок (perp DEX) и дистрибуция (платформы выпуска токенов). В 2025 году общая выручка протоколов составила $176 млрд, при этом 58% комиссий были удержаны как доход, а $33,6 млрд распределены среди держателей токенов через стейкинг, шаринг комиссий и выкупы. Тренд перехода ценности к держателям токенов усиливается, что меняет инвестиционные подходы от нарративов к фундаментальным показателям. В 2026 году ожидается дальнейшее смещение от стейблкоинов к perp DEX и более широкое внедрение механизмов распределения доходов среди инвесторов.

比推01/14 14:23