Полная версия отчета доступна в формате PDF бесплатно.

Добро пожаловать в Strategy Watch #3

Strategy Watch был создан для удовлетворения явного спроса на высококачественный, беспристрастный анализ показателей фондового уровня и тенденций распределения активов в цифровых активах.

Наша цель проста — сделать Strategy Watch обязательным к прочтению ежемесячным изданием для сообщества инвесторов в цифровые активы.

Фонды и аллокаторы, которые предоставляют данные и аналитику, помогают сформировать более полное и ценное представление о ландшафте. Если у вас есть аналитика, данные или обновления по распределению, которыми стоит поделиться, мы приветствуем ваш вклад.

Представьте свои последние инициативы и обновления подготовленной аудитории институциональных аллокаторов.

Внутри последнего Strategy Watch

Отчет структурирован по шести основным разделам, каждый из которых посвящен отдельному измерению институциональной активности в цифровых активах:

01 Монитор институциональных потоков | Ранняя стабилизация, поскольку отток BTC/ETH улучшается, а спрос на ETF восстанавливается, но уверенность на спотовых рынках остается под давлением.

02 Эффективность фондов и SMA | Рыночно-нейтральные стратегии показали стабильный рост; директионная эффективность остается сильно дисперсной.

03 Глубокое погружение в стратегию: Квантовое тренд-следование | Что движет эффективностью квантового тренд-следования в сложной среде для директионных стратегий? Услышьте напрямую от управляющего фондом.

04 Эффективность ончейн-хранилищ | Отстают ли кураторы ETH от доходности стейкинга ETH?

05 Монитор менеджеров | Узнайте, как более 300 менеджеров ожидают performance крипторынка в следующие три месяца.

06 Обновления по распределению | Пенсионный фонд на $6B увеличивает экспозицию в крипто, поскольку продолжают запускаться новые фонды и институциональные стратегии.

Ведущая платформа для аллокаторов цифровых активов. Узнать больше

Монитор институциональных потоков

- Потоки капитала BTC и ETH оставались отрицательными в течение марта, но продолжали восстанавливаться от февральских минимумов, в то время как приток стейблкоинов стабилизировался на фоне общей стабилизации.

Биткоин и Эфириум продолжали регистрировать чистый отток в течение марта, с потоками капитала, закрывающими месяц на уровне -$7,0 млрд и -$1,6 млрд соответственно, что является значительным улучшением по сравнению с показателями -$9,6 млрд и -$3,2 млрд, наблюдавшимися в середине февраля. Приток стейблкоинов также стабилизировался до +$2,6 млрд к концу месяца, снизившись с пика +$6,2 млрд ранее в марте. Общая картина — это постепенная стабилизация, а не восстановление, при этом острая фаза институционального снижения рисков теряет импульс, но уверенность в спотовых активах остается под давлением.

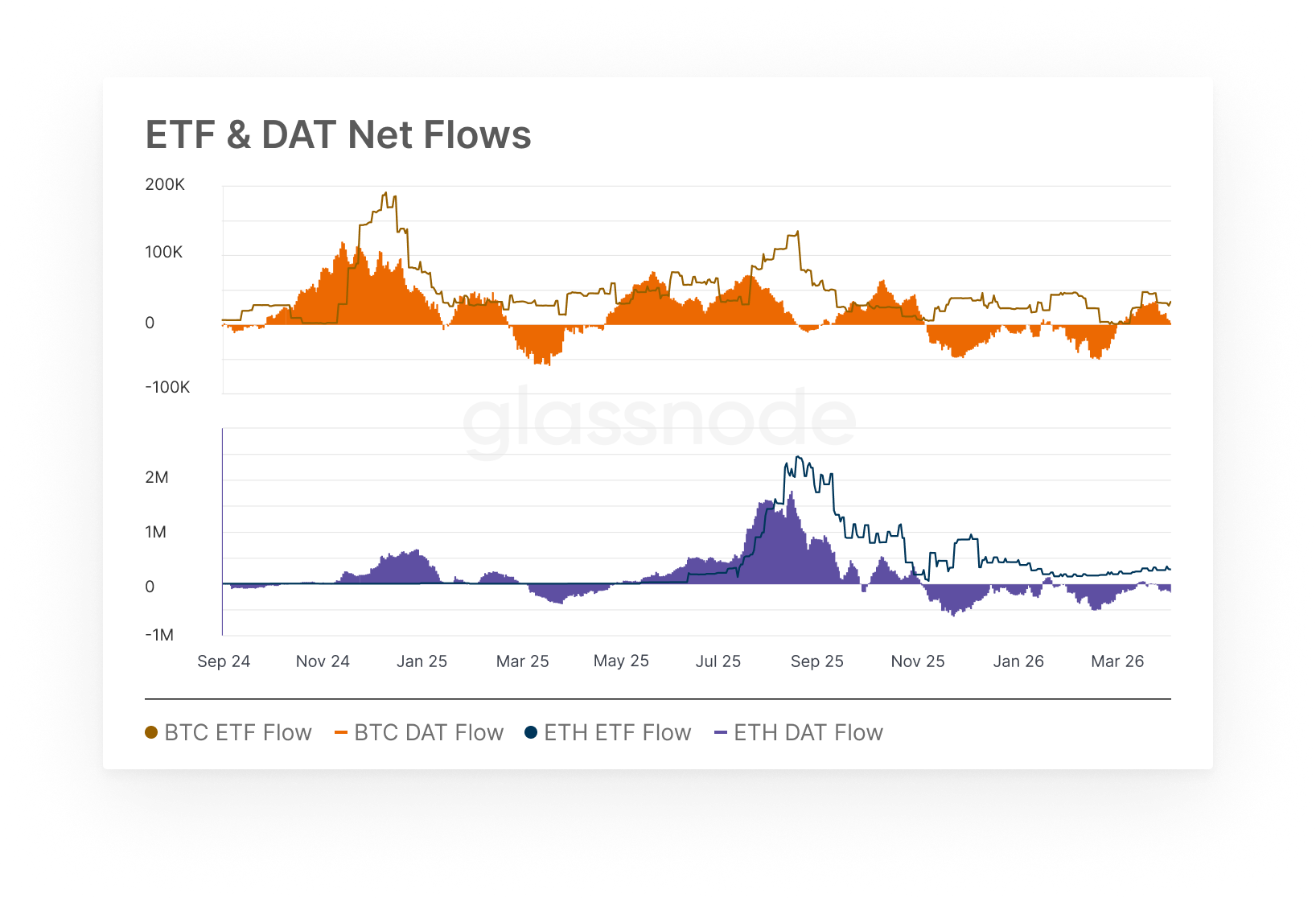

Чистые потоки ETF & DAT

- Потоки BTC ETF и DAT решительно развернулись в положительную сторону в течение марта, в то время как каналы ETH следовали более умеренными темпами, прежде чем оба ослабли к концу месяца.

Потоки BTC ETF и DAT наконец стали положительными в течение марта, достигнув внутримесячных максимумов в +30,6 тыс. BTC и +46,8 тыс. BTC соответственно в середине месяца, прежде чем стабилизироваться на уровне +17,6 тыс. BTC и +30,9 тыс. BTC к концу месяца. Потоки ETH повторили смену направления с меньшей интенсивностью: потоки ETF достигли +46,6 тыс. ETH, а потоки DAT достигли пика в +295,9 тыс. ETH, прежде чем снизиться до +261,9 тыс. ETH на закрытии. Всплеск в середине месяца, за которым последовало незначительное отступление, позволяет предположить, что спрос остается чувствительным к более широким рыночным условиям, а не является истинным устойчивым структурным сдвигом в институциональном позиционировании.

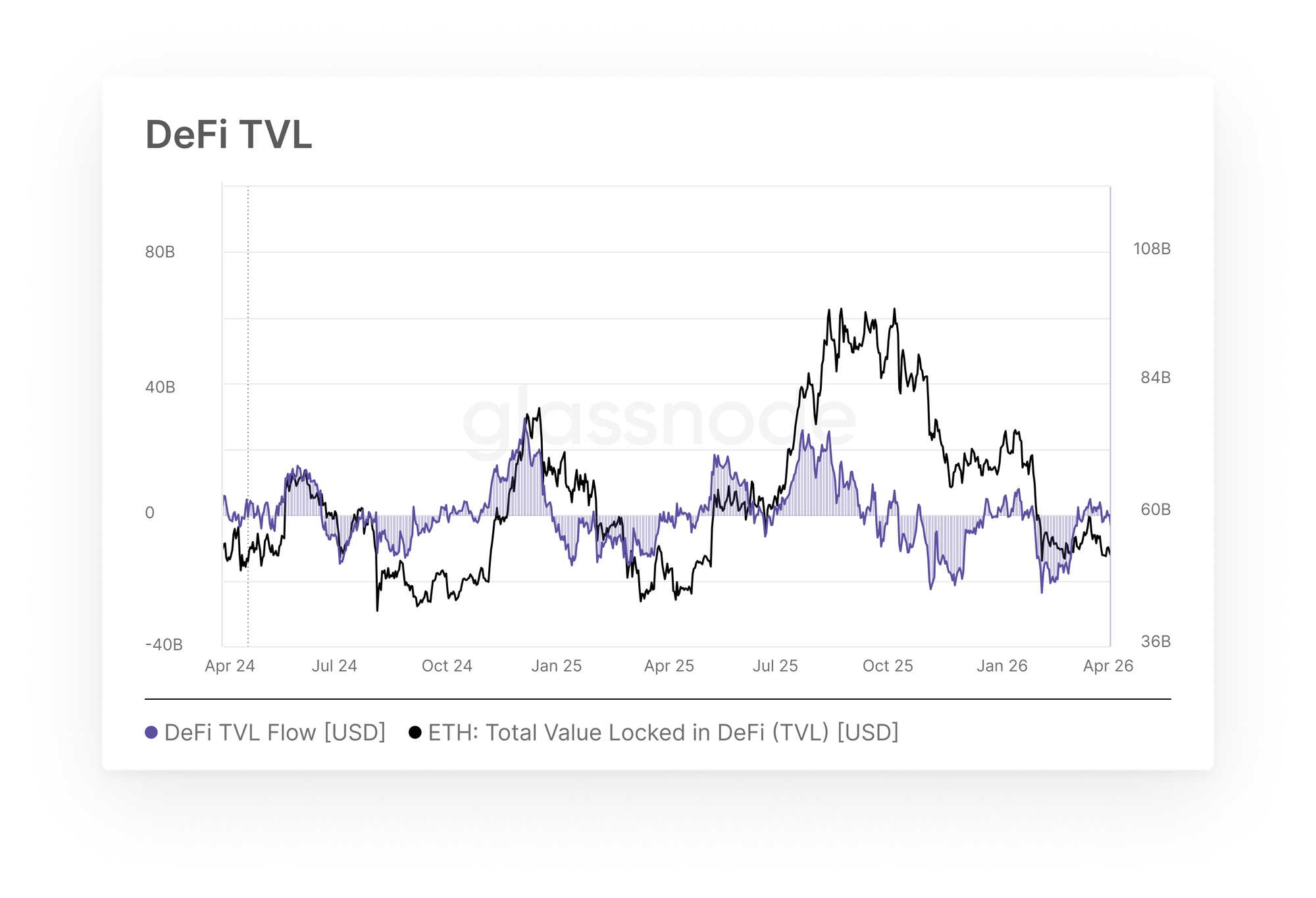

TVL DeFi и капитализация стейблкоинов

- Потоки TVL DeFi на Ethereum значительно восстановились в течение марта, развернувшись от пиковых оттоков февраля к почти нейтральной территории к концу месяца.

После регистрации пиковых месячных оттоков в $17,8 млрд в конце февраля, потоки TVL Ethereum DeFi резко восстановились в течение марта, став положительными в середине месяца и закрыв период почти на нейтральном уровне в -$0,75 млрд. Темпы восстановления были заметными: потоки переместились от двузначных оттоков в начале марта до кратковременных положительных значений около $4,9 млрд к середине месяца, прежде чем стабилизироваться. Хотя сдвиг тренда значим, одного месяца стабилизации недостаточно, чтобы объявить о развороте более широкого сокращения, которое сохраняется с августа 2025 года, и для подтверждения подлинного возвращения уверенности аллокаторов в ончейн-доходных стратегиях потребуются устойчивые притоки.

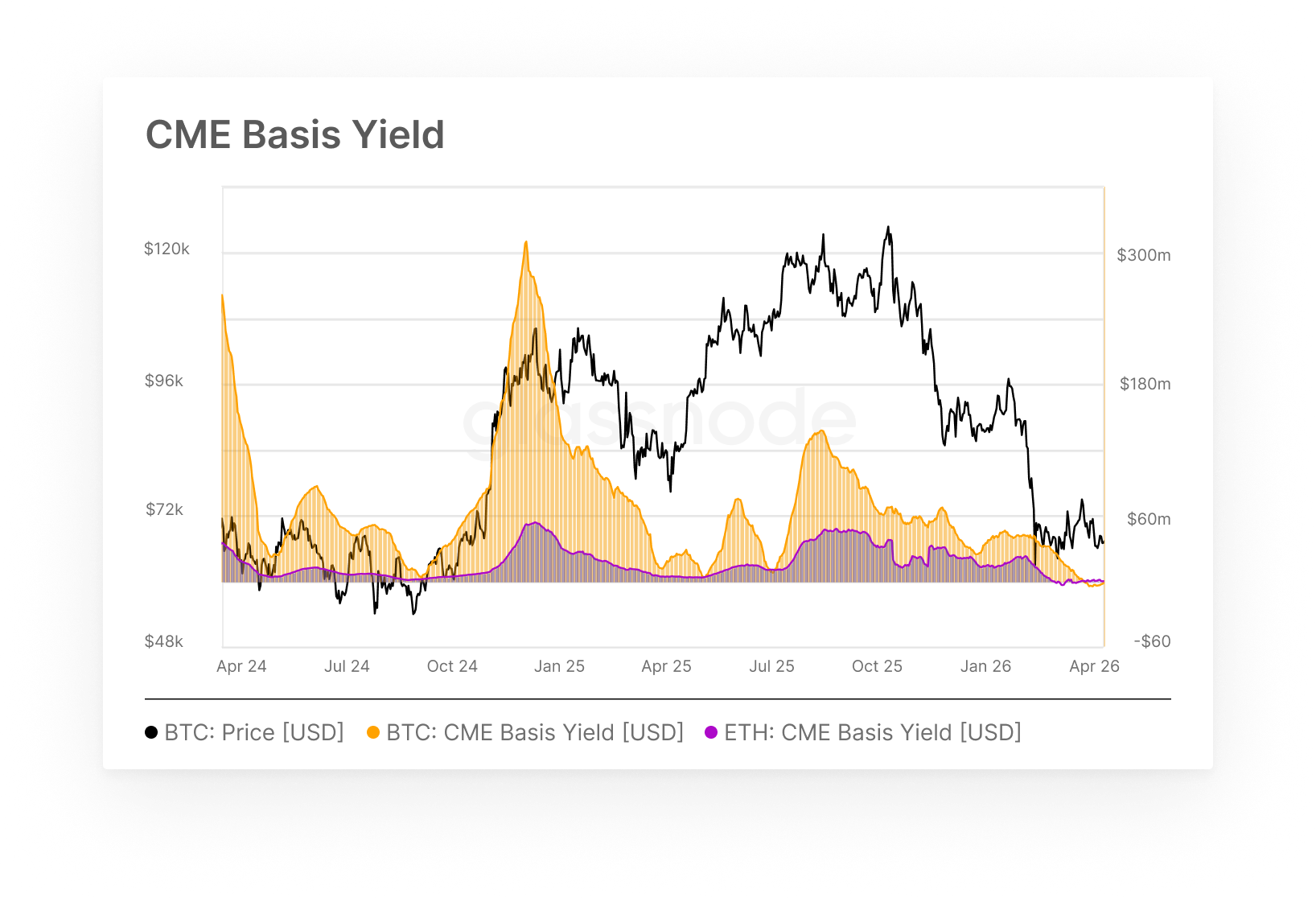

Доходность базиса CME

- Доходность базиса BTC CME стала отрицательной в течение марта, полностью уничтожив керри-трейд, в то время как доходность базиса ETH оставалась subdued, но показала tentative признаки восстановления к концу месяца.

Здесь мы измеряем доходность, доступную институциональным инвесторам, осуществляющим керри-трейды. После сжатия в течение февраля до $17,3 млн/месяц, доходность базиса BTC перешла в отрицательную территорию в середине марта и закрыла месяц на уровне -$3,9 млн, что отражает полную инверсию керри-премии. Это сигнализирует о том, что фьючерсы торгуются с дисконтом к споту, полностью устраняя экономическую целесообразность рыночно-нейтральных стратегий. Доходность базиса ETH, уже отрицательная в конце февраля, колебалась в узком диапазоне, прежде чем modestly восстановиться до +0,9 млн к концу месяца. В совокупности, среда керри для обоих активов остается структурно сложной, и значительное восстановление зависит от устойчивого восстановления премии фьючерсов над спотом.

Отказ от ответственности: Этот отчет не предоставляет каких-либо инвестиционных рекомендаций. Все данные предоставляются исключительно в информационных и образовательных целях. Ни одно инвестиционное решение не должно основываться на информации, предоставленной здесь, и вы несете единоличную ответственность за свои собственные инвестиционные решения. Представленные балансы на биржах получены из комплексной базы данных меток адресов Glassnode, которые собираются как из официально опубликованной информации бирж, так и с помощью проприетарных алгоритмов кластеризации. Хотя мы стремимся обеспечить максимальную точность в представлении балансов бирж, важно отметить, что эти цифры могут не всегда охватывать всю полноту резервов биржи, особенно когда биржи воздерживаются от раскрытия своих официальных адресов. Мы призываем пользователей проявлять осторожность и осмотрительность при использовании этих метрик. Glassnode не несет ответственности за любые несоответствия или потенциальные неточности. Пожалуйста, прочтите наше Уведомление о прозрачности при использовании данных бирж.