Автор оригинала: Sanqing, Foresight News

13 апреля генеральный директор StarkWare, компании-разработчика инфраструктуры ZK-Rollup для Starknet, Эли Бен-Сассон на общем собрании объявил о сокращении штата и реструктуризации компании в два независимых бизнес-подразделения, сфокусированных на выручке и разработке Starknet. Компания ранее выпустила движок масштабирования StarkEx, а в конце 2021 года запустила Starknet в мейннет как Validity Rollup второго уровня (Layer 2) для Ethereum, самостоятельно разработав язык программирования Cairo, промежуточный слой представления Sierra и постквантовую систему доказательств, став технологическим эталоном в области ZK Rollup. В 2022 году компания привлекла несколько раундов финансирования на общую сумму около 260 миллионов долларов, а её оценка достигала 8 миллиардов долларов, что делало её одним из проектов с самой высокой оценкой в области ZK в то время.

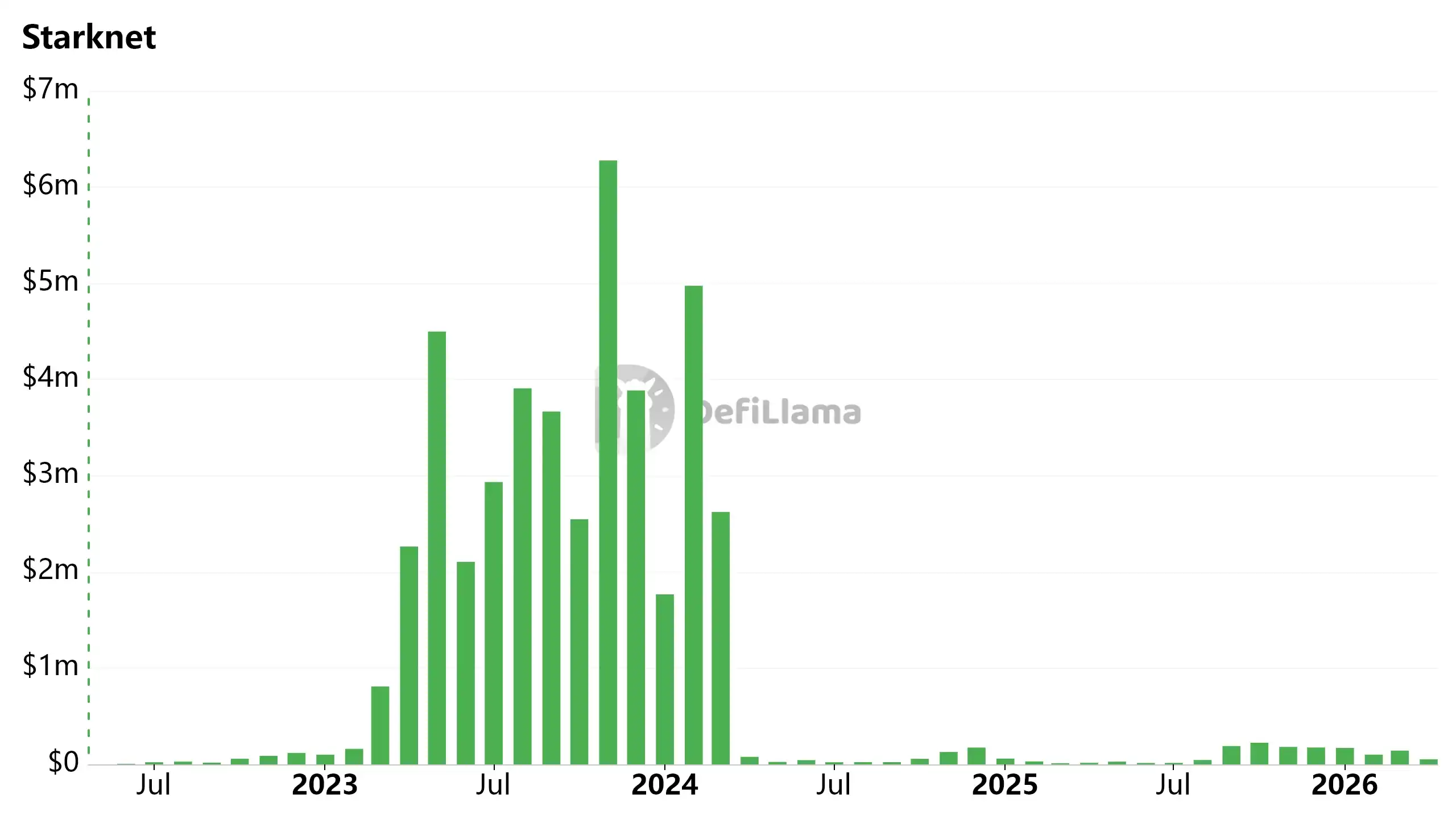

Согласно данным DefiLlama, ежемесячный доход сети Starknet достиг пика в почти 6,3 миллиона долларов в ноябре 2023 года, тогда как с апреля 2024 года её ежемесячный доход составляет лишь от десятков до сотен тысяч долларов, снизившись более чем на 95%.

Комиссии Starknet (ежемесячно)

От «инфраструктуры» к отступлению в «независимые приложения»

Столкнувшись с переходом от «инфраструктурной компании платформенного типа» к «технологической компании продуктового типа», Бен-Сассон признал, что прежняя StarkWare была «слишком большой и неэффективной», и теперь необходимо вернуться к стартап-модели, используя небольшие команды для быстрых итераций в поисках PMF (Product-Market Fit).

Источник: Твит Эли Бен-Сассона

В этой волне отраслевого сокращения StarkWare не одинока. OP Labs (основная команда разработчиков Optimism) в марте сократила около 20 человек (около 20% штата), стремясь сфокусироваться на ключевых приоритетах, ускорить принятие решений и снизить координационные издержки; Polygon Labs в январе после приобретения провела интеграцию, сократив около 60 человек в нескольких командах, хотя компания заявила, что чистая численность персонала осталась неизменной.

Кроме того, биржа Crypto.com сократила штат на 12%, фонд Algorand (L1) — на 25%, а криптоисследовательская организация Messari и многие другие компании или проекты также провели новую корректировку кадров.

После реструктуризации главный финансовый директор Ран Гринштейн будет курировать后台-функции, такие как финансы и кадры, в то время как фронтенд-бизнес будет разделен на два подразделения, каждое со своими независимыми командами BD, разработки и GTM.

- Подразделение разработки Starknet: Руководимое главой по продукту Томом Брандом, продолжает основную работу над базовым протоколом.

- Подразделение приложений: Возглавляемое главным директором по продукту Авиху Леви, несет ответственность за прямую генерацию дохода и专注于 создание продуктов, которые «могут быть реализованы только с помощью технологического стека StarkWare и минимально зависят от внешних компонентов».

Хотя официально конкретные продуктовые линейки не объявлены, но в сочетании с недавней публикацией Леви статьи о реализации квантово-безопасных транзакций (QSB) без изменения протокола Bitcoin, а также с запуском в Starknet функции конфиденциальности, аналогичной Zcash, квантовая безопасность и продукты, связанные с Bitcoin, скорее всего, станут их первыми направлениями для проб.

Удар EIP-4844 и поляризация L2

Затруднительное положение Starknet, по сути, отражает коллективные трудности всего сегмента L2 после обновления протокола.

В марте 2024 года Ethereum внедрил EIP-4844, который значительно снизил стоимость данных Blob, напрямую уничтожив бизнес-модель L2, основанную на «зарабатывании на разнице в комиссиях Gas L1 и L2».

После этого Ethereum продолжил увеличивать предложение Blob через多次 обновлений, в мае 2025 года обновление Pectra увеличило цель с 3 на блок до 6 на блок (максимум 9); после обновления Fusaka в конце 2025 года оно further увеличилось до целевых 14 на блок, максимум 21 на блок.

В будущем Ethereum планирует продолжить постепенное увеличение емкости Blob с помощью更多 механизмов BPO и таких технологий, как PeerDAS, что позволит сохранить стоимость доступности данных для L2 на крайне низком уровне в долгосрочной перспективе.

Когда стоимость доступности данных大幅 снижается, защитным рвом сетевой стоимости становится уже не дешевизна, а собственная плотность пользователей и способность привлекать капитал.

Несмотря на同样遭受 удар EIP-4844,表现 рынка L2 крайне неоднородно.

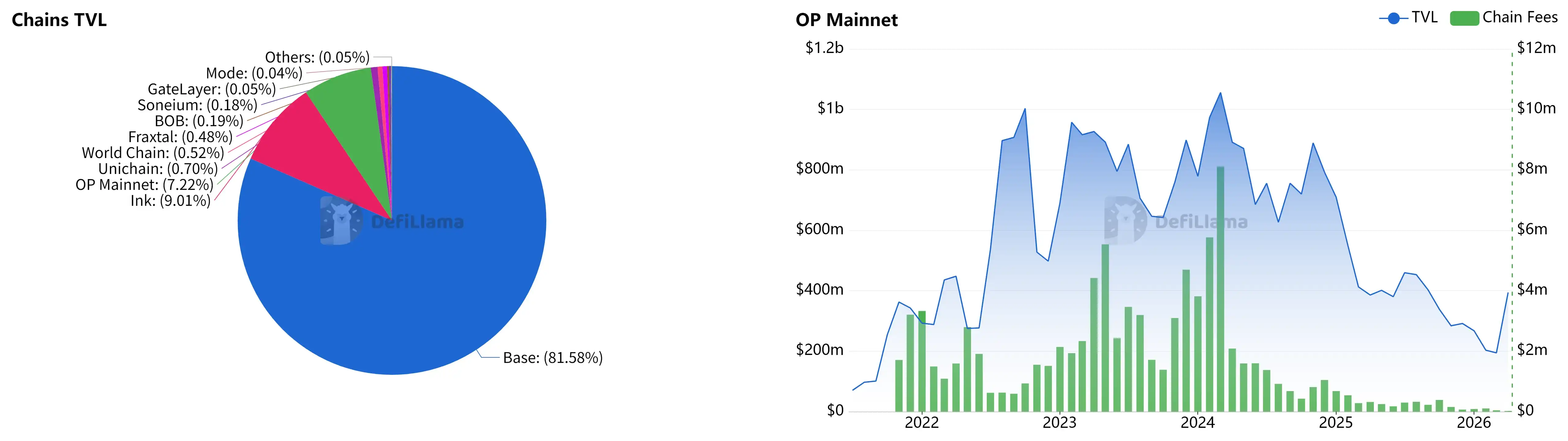

Согласно данным DefiLlama, Base, благодаря мощному потоку пользователей от Coinbase и каналам фиатного пополнения, в 2025 году получила доход в 75,4 миллиона долларов (62% от общего дохода L2), обработав более 60% всего объема транзакций; Arbitrum, опираясь на композитный финансовый стек из таких ведущих протоколов, как GMX и Pendle, поддерживает TVL на уровне около 2 миллиардов долларов.

Optimism ранее полагалась на экосистему OP Stack и Superchain, но в настоящее время TVL Superchain高度 зависит от Base (более 80%), при этом доля самого OP Mainnet составляет лишь однозначные проценты. Его TVL и доход от комиссий в сети также значительно снизились в 2025-2026 годах. Что еще более усугубляет ситуацию, Base в феврале 2026 года объявила о выходе из OP Stack и переходе на собственную унифицированную технологическую платформу, что further ослабит позиции Optimism как хаба в экосистеме L2.

Слева: круговая диаграмма TVL различных цепочек Superchain | Справа: TVL OP Mainnet и комиссии сети (ежемесячно)

Starknet находится в еще более тяжелом положении, её текущий TVL составляет лишь около 241 миллиона долларов, что менее одной двадцатой от TVL Base; её нативный токен STRK с момента airdrop в феврале 2024 года一路狂跌 до 0,033 доллара, с общей рыночной капитализацией около 187 миллионов долларов. Это даже ниже общего объема исторического финансирования компании в 260 миллионов долларов.

TVL Starknet, цена STRK и рыночная капитализация STRK

Способность к дистрибуции определяет, кто останется за игровым столом

«Инфраструктура сама по себе не выигрывает соревнование». Эта фраза Бен-Сассона является反思 стратегии StarkWare за последние восемь лет «построить сеть и ждать гостей».

Инвестиции StarkWare в инженерию криптографии намного превосходят同行. Построенные с нуля язык Cairo и抗квантовая система STARK невероятно сложны. Но на практике技术洁癖, отказ от совместимости с EVM, создал极高的 миграционный барьер для разработчиков, что является одним из факторов, ограничивающих процветание экосистемы.

Ключевым драйвером роста L2 уже давно является не технологическая дифференциация, а способность к дистрибуции и стратегические альянсы. В настоящее время Base и Arbitrum вместе контролируют近 75% общей стоимости L2.

21Shares прогнозирует, что сегмент L2 к концу года консолидируется в «более компактный и устойчивый набор сетей». В этой выживательной игре по принципу «победитель получает все», отступление к собственным приложениям — один из немногих оставшихся для StarkWare путей дифференциации.

Технологический задел — это лишь входной билет, а не финишная черта. Теперь StarkWare должна доказать рынку не то, что она может «изобрести» самые передовые технологии, а то, что она может реально «продать» какой-либо продукт.