Автор: Deep Chao TechFlow

Оригинальное название: Индекс малых акций США обновил исторический максимум, незамеченный сигнал криптовалютного цикла?

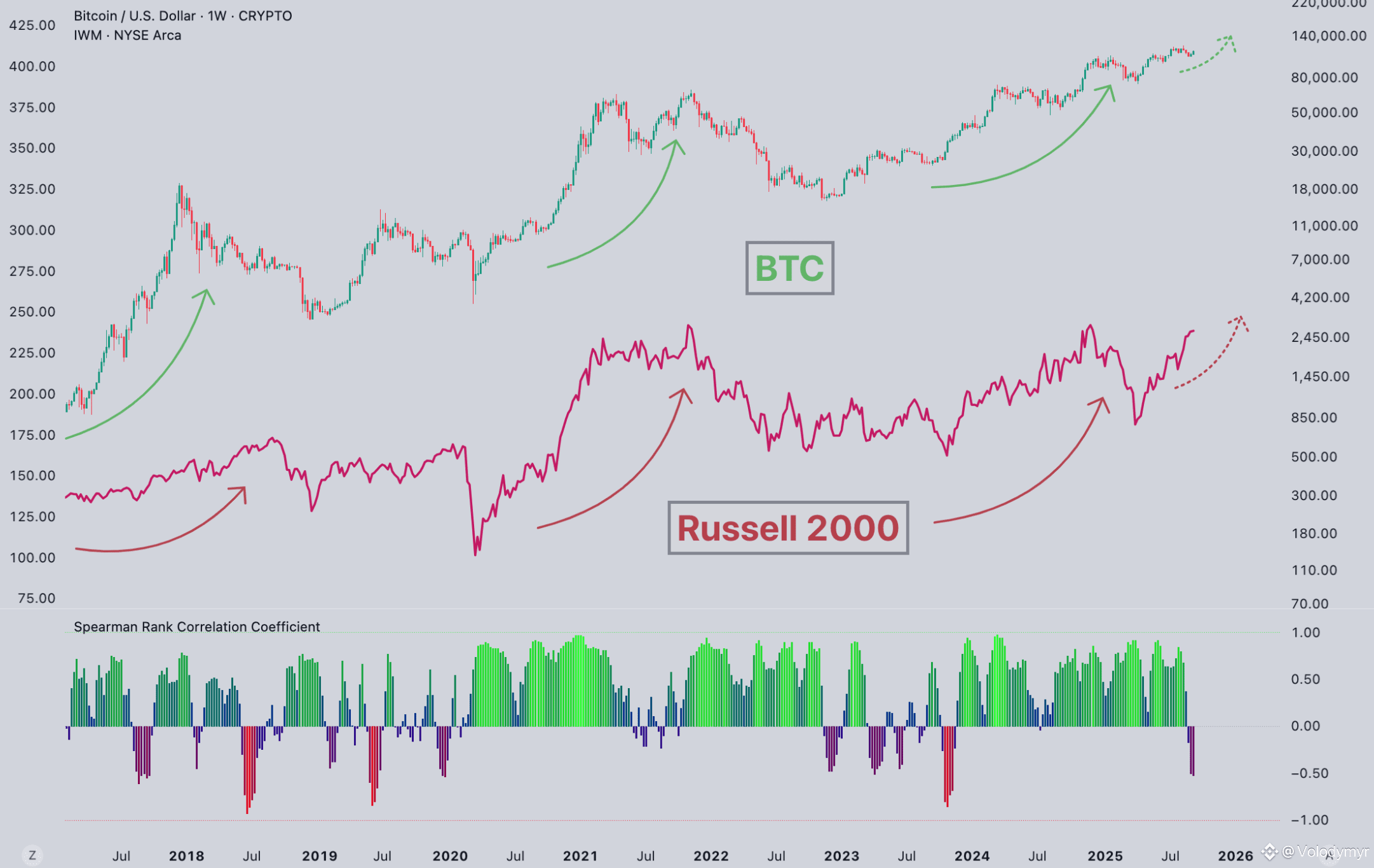

За первые три недели 2026 года Russell 2000 (индекс Russell 2000) вырос на 9%, превысив отметку в 2700 пунктов.

Этот индекс малых акций США находился в боковом тренде с конца 2021 года в течение трех лет и впервые пробил его только в ноябре прошлого года, а сейчас вошел в стадию «ценового открытия». Исторических уровней сопротивления для参考 больше нет.

Недавно появилось мнение: когда Russell 2000 пробивал уровни в 2016 и 2020 годах, BTC также запускал бычий рынок, оба раза совпадали. Сейчас снова пробил, последует ли за ним крипторынок?

Проверив данные, это действительно похоже на опережающий сигнал, по крайней мере, в истории он срабатывал.

Russell 2000 отслеживает 2000 компаний с наименьшей рыночной капитализацией в США, медианная капитализация составляет чуть более 1 миллиарда долларов. По сравнению с такими звездными акциями, как Apple и Microsoft, входящими в S&P 500, у этих небольших компаний есть общая черта: они в основном занимают деньги в банках, а не выпускают облигации.

Когда процентные ставки растут, их затраты на финансирование первыми не выдерживают; когда падают — они первыми получают выгоду.

Поэтому трейдеры любят использовать Russell 2000 как «термометр аппетита к риску». Его обновление рекорда означает, что рынок готов вкладывать деньги в рисковые активы.

Есть и другая логика. Малые акции сфокусированы на внутреннем рынке США, в отличие от глобализированных Apple и Microsoft. Рост Russell 2000 в некоторой степени отражает внутренние экономические ощущения в США.

2016 и 2020: два прорыва индекса малых акций, два взлета BTC

Сначала данные.

В 2016 году цикл повышения ставок ФРС почти завершился, избрание Трампа принесло ожидания снижения налогов, аппетит к риску вырос. BTC только что пережил халвинг, сокращение предложения столкнулось с восстановлением спроса, что позже привело к безумному бычьему рынку 2017 года.

В 2020 году было еще круче. Пандемия создала огромную яму, ФРС включила печатный станок на полную, прижав ставки к полу. Институционалы впервые массово вышли на рынок, MicroStrategy и Tesla начали скупать, BTC вырос с 10 000 с лишним до 69 000.

Временные окна двух прорывов Russell 2000 и бычьих рынков BTC действительно совпадают.

Но на самом деле исторических выборок всего две.

Оглядываясь на ноябрь 2024 года, Russell 2000 впервые пробил предыдущий максимум 2021 года. В то же время BTC уже находился near $100,000.

Если считать с халвинга в апреле 2024 года, BTC вырос с 63 000 до нынешних 90 000, примерно на 50%. Звучит неплохо, но по сравнению с 5-кратным и 27-кратным ростом в аналогичные периоды двух предыдущих циклов разница очевидна.

Несколько возможных причин.

Первая: выход институционалов снизил волатильность. После одобрения ETF в январе 2024 года такие гиганты, как BlackRock и Fidelity, вышли на рынок, только ETF привлекли сотни миллиардов долларов. Деньги институционалов не гоняются за ростом и не продают при падении, как розница, волатильность сгладилась. Плюс в том, что падения не такие сильные, но цена — невозможность резких взлетов, как в 2017 году.

Вторая: предельный эффект халвинга ослабевает. После четвертого халвинга годовая инфляция BTC упала с 1,7% до 0,85%. Звучит как сокращение вдвое, но 94% BTC уже добыто. Новое предложение все меньше разбавляет существующее, «шок предложения» от халвинга с каждым разом слабее.

Третья: BTC обновил исторический максимум еще в марте 2024 года. Впервые в истории это произошло до халвинга. Ожидания ETF提前 высвободили часть спроса, и когда халвинг действительно наступил, новость уже была大半 priced in.

Совпадение или одна и та же логика ликвидности?

Russell 2000 и BTC: один — малые акции США, другой — крипто-лидер, почему они должны двигаться синхронно?

Мое понимание: они чувствительны к одним и тем же макросигналам.

Когда ФРС подает сигналы о смягчении, деньги движутся по кривой риска. Сначала гособлигации, потом голубые фишки, затем малые акции, и, наконец, активы с высоким бета-коэффициентом, такие как крипто.

Прорыв Russell 2000 эквивалентен зеленому свету в середине цепочки.

Исследование JPMorgan в прошлом году показало, что у BTC самая высокая корреляция с малыми технологическими акциями из Russell 2000. Причина в том, что криптопроекты зависят от финансирования VC, блокчейн-инновации сосредоточены в небольших компаниях, а не в технологических гигантах. Проще говоря, у людей, покупающих малые акции, и людей, покупающих монеты, аппетит к риску схож.

Но я не решаюсь считать это причинно-следственной связью. Две выборки статистически недостаточны.

К тому же, в 2016 и 2020 годах у самого BTC был цикл халвинга, Russell 2000 мог быть просто еще одним макросигналом, появившимся в тот же период, а не тем, кто лидирует.

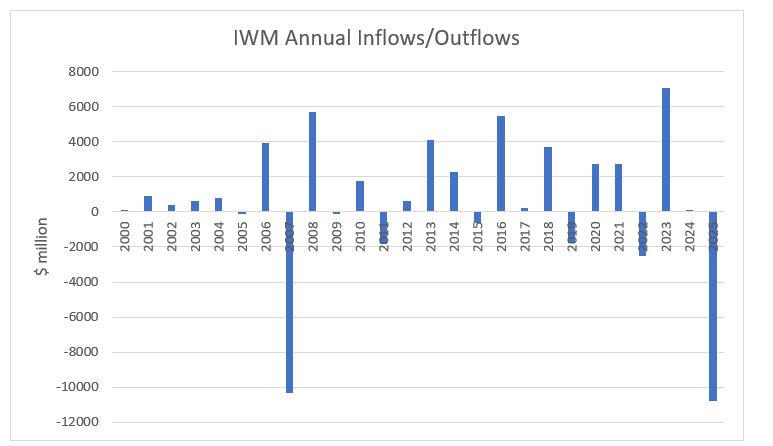

Кроме того, интересное явление: хотя индекс Russell растет, деньги уходят.

В 2025 году Russell 2000 вырос более чем на 40%, но ETF на малые акции США за год показали чистый отток почти в 200 миллиардов долларов. Это резко контрастирует с прошлыми бычьими рынками — раньше, когда индекс рос, деньги шли внутрь.

(Источник: etf.com)

Еще один набор данных. Около 40% компаний в Russell 2000 в третьем квартале 2025 года сообщили об отрицательной прибыли, что близко к историческому максимуму. Этот показатель более чем удвоился с 2007 года.

Индекс обновляет рекорды, фундаментальные показатели вызывают опасения, деньги все еще уходят.

Как это объяснить? Одна возможность — рост индекса обеспечивают少数 акций, другая — перебалансировка пассивных средств. Но независимо от объяснения, нарратив о «возвращении аппетита к риску» ставится под сомнение.

В последнее время, если вы следите за макроконтентом и泛金融ным контентом, вы увидите, что среди видео-блогеров об инвестициях и в крипто-твиттере все чаще звучат голоса о том, что «запуск Russell 2000 — это опережающий сигнал роста BTC».

Прорыв Russell 2000 действительно был сигналом, появлявшимся перед бычьими рынками криптовалют 2016 и 2020 годов, и сейчас он снова появился. Как окно для наблюдения он имеет ценность, но моя точка зрения: не используйте его как торговый сигнал.

Две выборки не устанавливают причинно-следственную связь, и в этом цикле есть несколько переменных, отличающихся от предыдущих: ETF изменили структуру капитала, волатильность подавлена институционалами, эффект халвинга ослабевает. Старый сценарий может не сработать.

«Резонанс» между Russell 2000 и BTC, возможно, ждет ответа только после завершения этого цикла.

Примечание:

Источники данных: Yahoo Finance, TradingEconomics, JPMorgan Research, BeInCrypto. По состоянию на январь 2026 года.

Twitter:https://twitter.com/BitpushNewsCN

Группа общения比推 TG:https://t.me/BitPushCommunity

Подписка比推 TG: https://t.me/bitpush