На прошлой неделе ФРС снизила целевую ставку до диапазона 3,50%–3,75% — этот шаг был полностью учтен рынком и в целом ожидаем.

По-настоящему удивило рынок то, что ФРС объявила о ежемесячной покупке краткосрочных казначейских облигаций (T-bills) на сумму 40 миллиардов долларов, что быстро было названо некоторыми «облегченной версией количественного смягчения (QE-lite)».

В сегодняшнем отчете мы подробно разберем, что изменила эта политика, а что осталось прежним. Кроме того, мы объясним, почему это различие крайне важно для рисковых активов.

Давайте начнем.

1. Краткосрочная перспектива

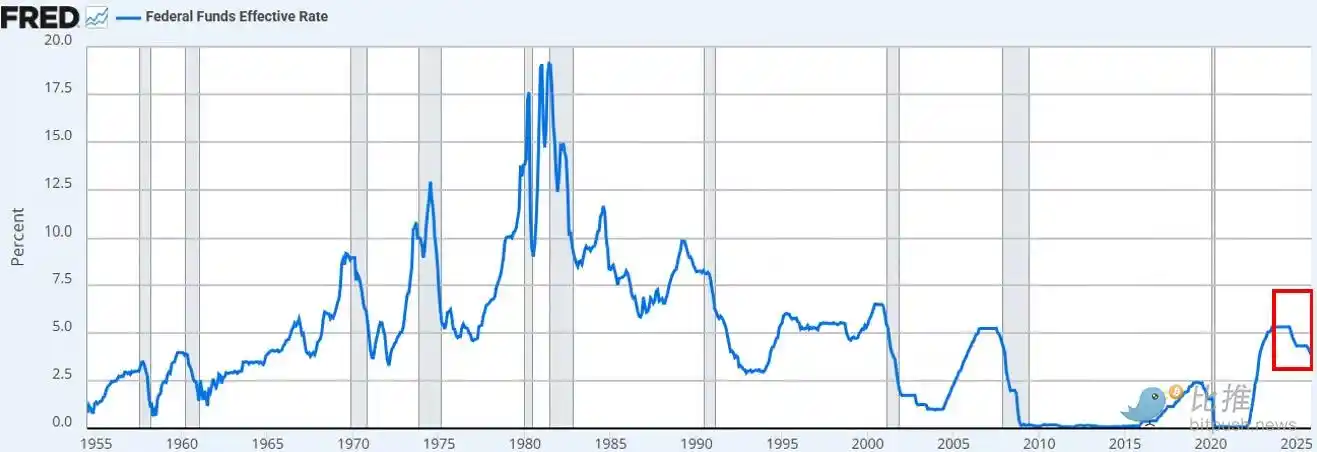

ФРС снизила ставки, как и ожидалось. Это уже третье снижение в этом году и шестое с сентября 2024 года. В общей сложности ставки были снижены на 175 базисных пунктов, что опустило ставку по федеральным фондам до самого низкого уровня примерно за три года.

Помимо снижения ставок, Джером Пауэлл объявил, что с декабря ФРС начнет «закупки для управления резервами» (Reserve Management Purchases) краткосрочных казначейских облигаций на сумму 40 миллиардов долларов в месяц. Учитывая сохраняющуюся напряженность на рынке репо и ликвидность банковского сектора, этот шаг был полностью ожидаем.

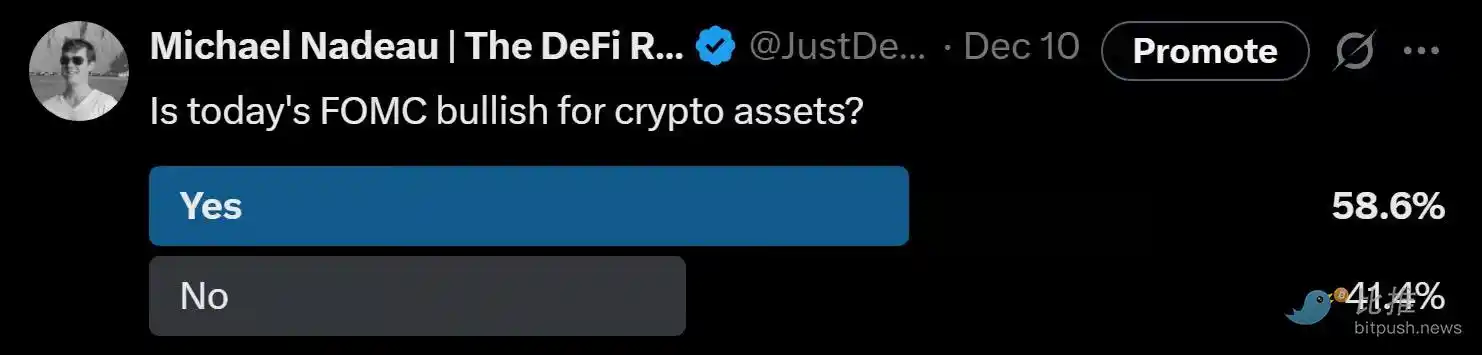

Общее мнение рынка (как на платформе X, так и на CNBC) состоит в том, что это «голубиный» поворот в политике.

Обсуждение того, эквивалентно ли объявление ФРС «печатанию денег», «QE» или «QE-lite», мгновенно заполонило ленты социальных сетей.

Наше наблюдение:

Как «наблюдатели за рынком», мы видим, что рыночный менталитет по-прежнему склоняется к «риск-он» (Risk-on). В таком состоянии мы ожидаем, что инвесторы будут «переобучаться» на заголовках, пытаясь сложить бычью логику, упуская из виду конкретные механизмы, с помощью которых политика трансформируется в реальные финансовые условия.

Наша точка зрения такова: новая политика ФРС благоприятна для «финансовой инфраструктуры», но не для рисковых активов.

В чем наше отличие от общего рыночного восприятия?

Наша позиция следующая:

· Покупка краткосрочных казначейских облигаций ≠ поглощение дюрации рынка

ФРС покупает краткосрочные казначейские векселя (T-bills), а не долгосрочные купонные облигации (coupons). Это не удаляет процентную чувствительность (дюрацию) с рынка.

· Долгосрочная доходность не подавляется

Хотя краткосрочные покупки могут незначительно сократить будущий выпуск долгосрочных облигаций, это не помогает сжать премию за срок. На данный момент около 84% выпуска казначейских облигаций уже составляют краткосрочные векселя, поэтому эта политика не меняет существенно структуру дюрации, с которой сталкиваются инвесторы.

· Финансовые условия не стали повсеместно более мягкими

Эти закупки для управления резервами, направленные на стабилизацию рынка репо и банковской ликвидности, не приведут к системному снижению реальных ставок, стоимости корпоративных заимствований, ипотечных ставок или ставок дисконтирования для акций. Их влияние является локальным и функциональным, а не широкой денежной экспансией.

Следовательно, нет, это не QE. Это не финансовое подавление. Важно прояснить: аббревиатуры не важны, вы можете называть это как угодно — печатанием денег, но оно не предназначено для подавления долгосрочной доходности путем удаления дюрации — а именно это подавление заставляет инвесторов двигаться вверх по кривой риска.

Сейчас этого не происходит. Динамика цен BTC и индекса Nasdaq с прошлой среды подтверждает это.

Что может изменить нашу точку зрения?

Мы верим, что у BTC (и у рисковых активов в целом) будет свой звездный час. Но это произойдет после QE (или как бы ФРС ни назвала следующую фазу финансового подавления).

Этот момент наступит, когда:

· ФРС искусственно подавит длинный конец кривой доходности (или подаст рынку сигнал).

· Реальные процентные ставки снизятся (из-за роста инфляционных ожиданий).

· Стоимость корпоративных заимствований снизится (что подстегнет технологические акции/Nasdaq).

· Премия за срок сожмется (долгосрочные ставки снизятся).

· Ставка дисконтирования для акций снизится (заставляя инвесторов переходить в более долгосрочные рисковые активы).

· Ипотечные ставки снизятся (под влиянием подавления длинных ставок).

Тогда инвесторы учуют запах «финансового подавления» и скорректируют свои портфели. Сейчас мы еще не в такой среде, но мы верим, что она приближается. Хотя время всегда трудно определить, наше базовое предположение таково: волатильность значительно возрастет в первом квартале следующего года.

Вот как мы видим краткосрочную перспективу.

2. Более широкая картина

Более глубокая проблема заключается не в краткосрочной политике ФРС, а в глобальной торговой войне (валютной войне) и напряженности, которую она создает в самой основе долларовой системы.

Почему?

США движутся к следующему этапу своей стратегии: возврат производства, перебалансировка глобальной торговли и конкуренция в стратегически необходимых отраслях, таких как ИИ. Эта цель находится в прямом конфликте с ролью доллара как мировой резервной валюты.

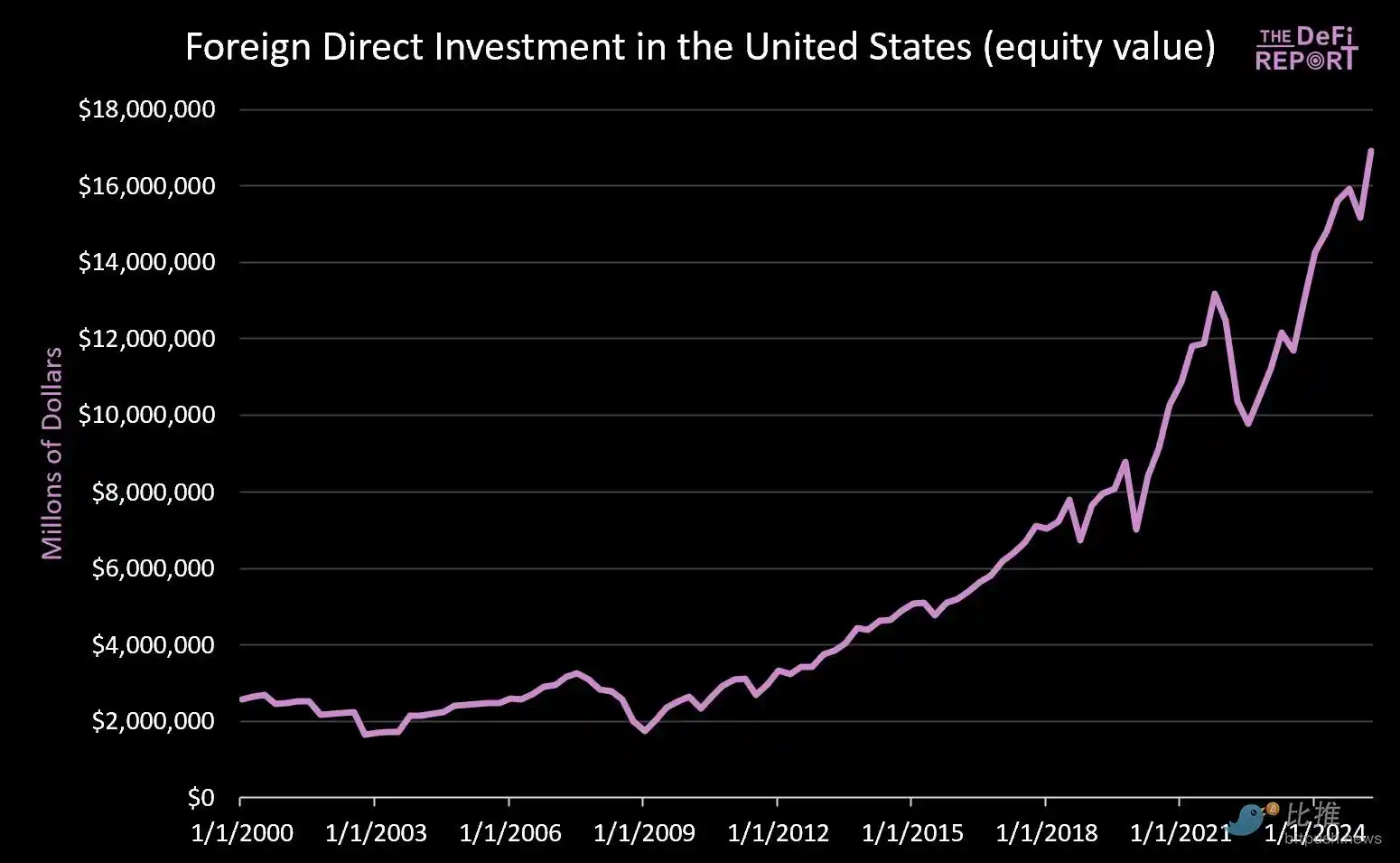

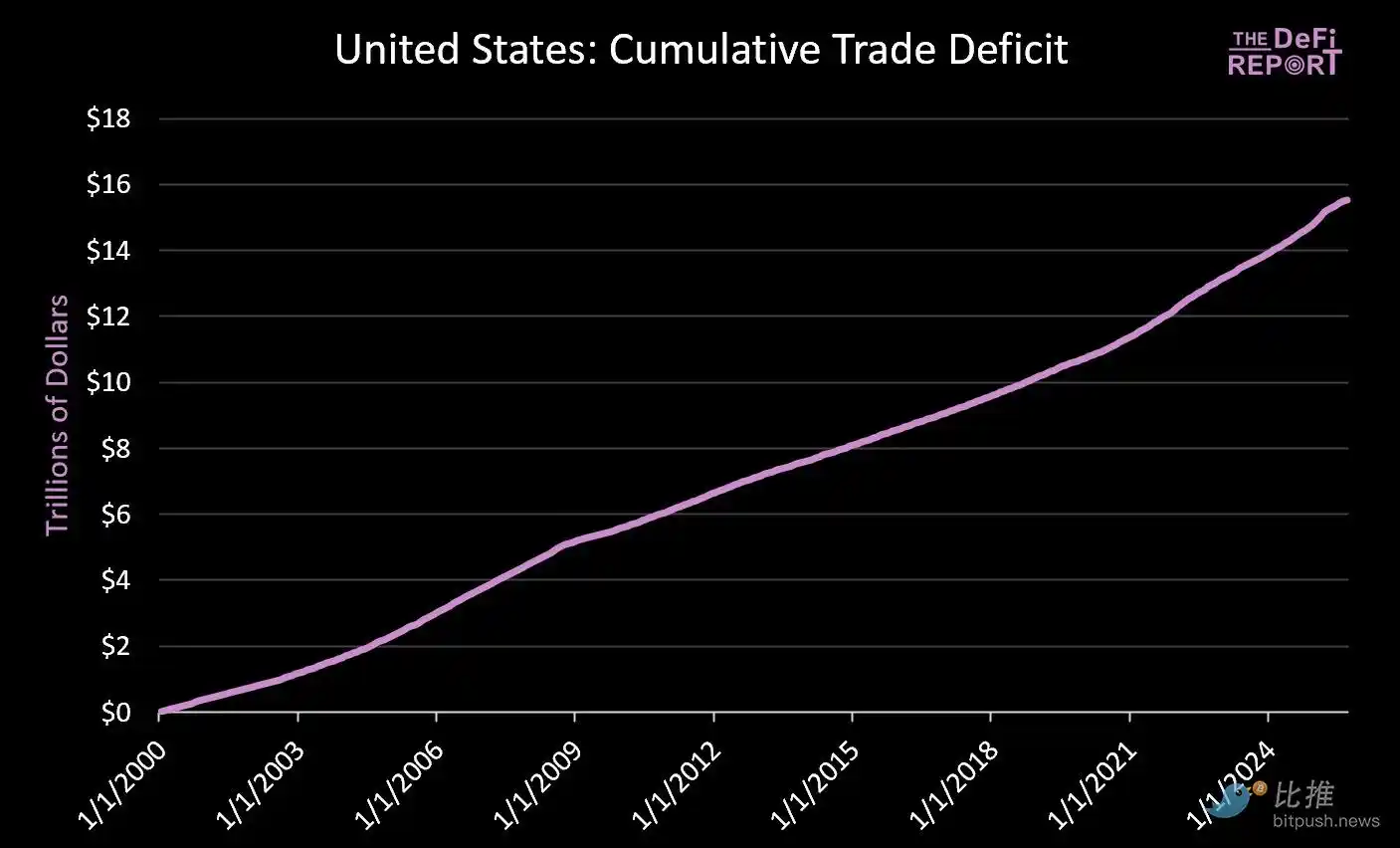

Резервный статус валюты может поддерживаться только при условии, что США持续运行贸易逆差的情况下才能维持运行 торгового дефицита. В текущей системе доллары отправляются за границу для покупки товаров, а затем возвращаются на рынки капитала США через казначейские облигации и рисковые активы. В этом суть «Дилеммы Триффина» (Triffin's Dilemma).

· С 1 января 2000 года: на рынки капитала США поступило более 14 триллионов долларов (и это не считая 9 триллионов долларов в облигациях, которыми currently владеют иностранцы).

· В то же время, для оплаты товаров, за границу ушло около 16 триллионов долларов.

Усилия по сокращению торгового дефицита неизбежно уменьшат объем капитала, циркулирующего обратно на американские рынки. Хотя Трамп宣扬 Япония和其他国家承诺 «инвестировать 550 миллиардов долларов в американскую промышленность», он не уточнил, что капитал Японии (и других стран) не может одновременно находиться и в производстве, и на рынках капитала.

Мы не считаем, что эта напряженность разрешится гладко. Вместо этого мы ожидаем более высокой волатильности, переоценки активов и, в конечном итоге, корректировки валютных курсов (то есть обесценивания доллара и сокращения реальной стоимости американских казначейских облигаций).

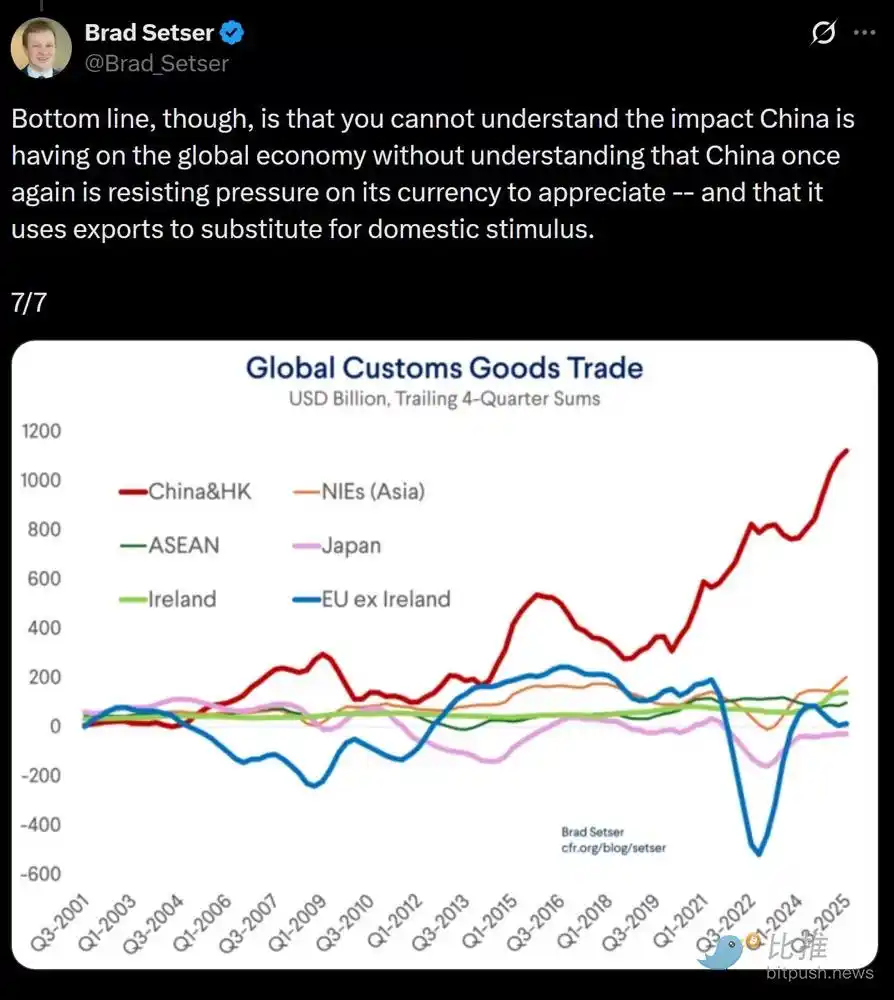

Ключевая мысль: Китай искусственно занижает курс юаня (придавая своим экспортным товарам искусственное ценовое преимущество), в то время как доллар искусственно завышен из-за иностранных капиталовложений (что делает импортные товары относительно дешевыми).

Мы считаем, что для решения этого структурного дисбаланса может即将到来可能即将来临 принудительное обесценивание доллара. На наш взгляд, это единственный可行ный путь решения проблемы глобального торгового дисбаланса.

В условиях нового раунда финансового подавления рынок в конечном итоге решит, какие активы или рынки заслуживают статуса «средства сбережения стоимости».

Ключевой вопрос在于, когда пыль уляжется, смогут ли казначейские облигации США продолжать扮演全球储备资产的角色扮演 роль глобального резервного актива.

Мы верим, что биткоин и другие глобальные, несуверенные средства сбережения стоимости (такие как золото) будут играть гораздо более важную роль, чем сейчас. Причина: они обладают scarcity, и не зависят от какого-либо политического кредита.

Вот какую «макроэкономическую картину» мы видим.