Author: @bonnazhu, Bonna | U酪乳

This round of rapid decline driven by STRC, in my opinion, might be the best financial teaching case.

Long post warning, again, with strong personal views.

TL;DR

- If MSTR were to truly die, it would still be due to reflexivity, but not this time.

- The return of STRC to its par value anchor is a matter of time; this is the nature of floating-rate bonds.

- Selling Bitcoin to raise cash is merely drinking poison to quench thirst, solving short-term problems while sowing endless future troubles.

The detailed analysis is as follows:

First, How to Understand This BTC Decline?

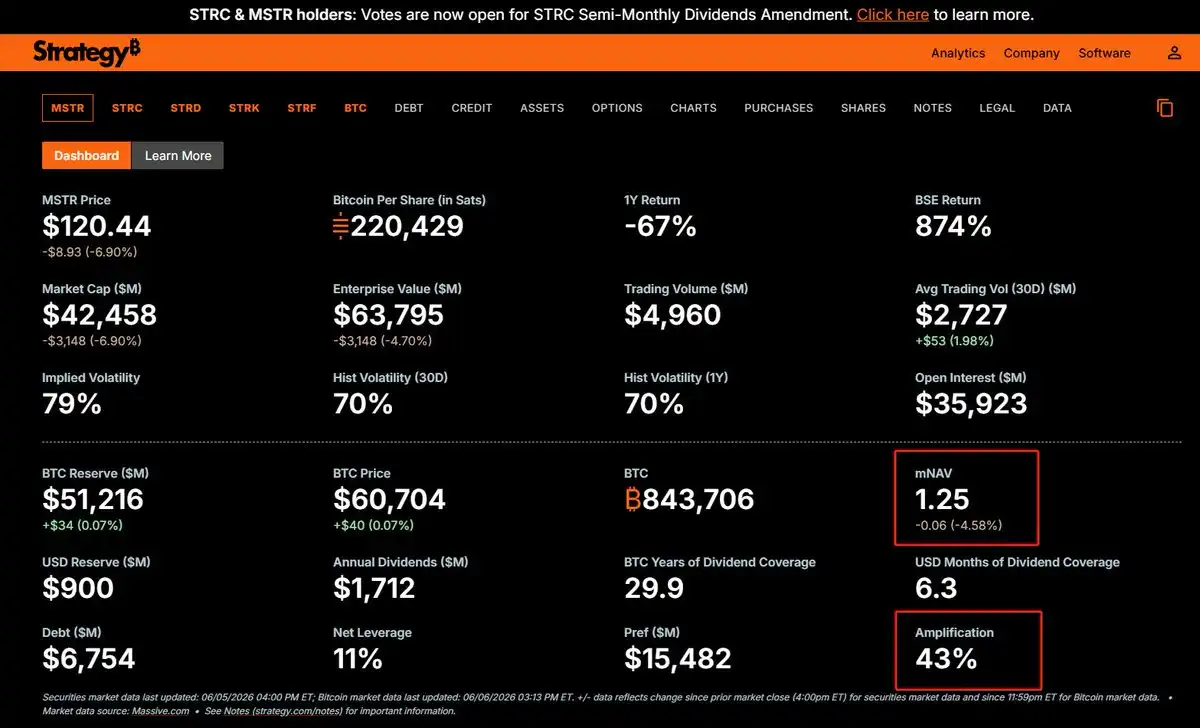

Personally, I tend to believe this rapid decline in BTC was a targeted attack by capital around MSTR. The trigger was MSTR using its already insufficient cash reserves (widely believed by the market to be a safety cushion set aside for preferred stock dividends) to repurchase part of its convertible bonds, causing the cash reserve coverage for preferred dividends to plummet from over two years to about six months, immediately followed by the sale of 32 BTC.

The market instantly picked up the scent of a "cash flow crisis" and launched a swift attack. Pre-existing sentiment worries, such as massive IPOs draining liquidity, the World Cup diverting attention, resurgent inflation and dampened rate cut expectations, further facilitated the attackers in solidifying this expectation in the market, allowing them to quickly force information-asymmetric funds to capitulate or hesitate to step in and buy the dip.

This is essentially a classic case of reflexivity in traditional financial markets:

Market prices do not passively reflect reality; they actively change it.

In other words:

Expectations are contagious, and this contagion can alter reality.

Soros' attack on the British Pound followed the same script. The Bank of England's forex reserves might have been sufficient initially, but market participants are information-asymmetric. Once everyone believes the reserves are insufficient and collectively shorts, the reserves can indeed become insufficient. Bank runs are the same: if everyone simultaneously believes the bank will fail and withdraws their money, the expectation of failure can become a reality!

Applying this to MSTR, the attackers' playbook is:

Cash reserves decline → Market expects a liquidity crisis, forcing BTC sales → Panic selling drives down BTC → BTC decline further compresses mNAV, worsens the balance sheet → The "can't hold on" expectation becomes increasingly validated by the price, options dwindle → More join the short side → Expectation moves closer to reality.

And the inherent soft spot that BTC itself cannot create sustainable cash flow for MSTR to cover dividend payments, requiring continuous reliance on financing to keep the flywheel spinning, is also why attackers find easier opportunities.

Second, The Logic Behind STRC's Decline and Return to Par Anchor

The relationship between STRC and MSTR common stock is essentially that of senior and junior tranches:

Common stock, as the junior tranche, absorbs most of the risk from BTC price volatility.

STRC, as the senior tranche, remains relatively stable under most circumstances.

Based on MSTR's target overall leverage ratio discipline of roughly 33-35% (currently increased to about 43% due to BTC's drop to $61k), theoretically, only if BTC price falls below $26k, wiping out the common stock, would the preferred stock be truly impacted.

So why did STRC decline too?

This involves some basics of bond pricing.

STRC is nominally preferred stock but is debt in substance, with floating interest and no maturity date.

The price of a bond is essentially the present value sum of all future cash flows (each period's interest, calculated from the coupon rate + principal at maturity, equal to par value of 100), discounted back at a discount rate. This discount rate is the required rate of return demanded by the market at that moment.

If the coupon rate exactly equals the required rate of return, the discounted price equals the par value of 100. This often happens at issuance, where underwriters typically set the coupon rate based on prevailing market conditions and investor return requirements.

However, a bond's life is long. Throughout its duration, external interest rate environments and issuer creditworthiness can change, affecting that discount rate (the denominator) corresponding to the required return. Once the market's required return rises while the coupon interest (the numerator) remains fixed, the discounted present value falls below par, and the bond trades at a discount. Conversely, if the required return falls, the bond trades at a premium.

Therefore, a bond's price is never a static number. Instead, it reflects the return the market currently demands to hold it.

A price falling below par implies: "The market demands a higher return than the coupon rate." If you buy at this discount and hold to maturity, your ultimate yield will indeed be higher than the coupon rate, as the portion of principal you didn't pay when buying the $100 face value bond compensates for the return the coupon didn't provide. That is, the market uses the discount to extract the compensation it deems necessary for the risk, which the coupon rate fails to provide.

STRC is similar. Market concerns about MSTR's cash flow translate into a repricing of STRC's repayment capacity. As the "cash flow crisis" narrative develops, the required return demanded by the market to hold STRC jumps; bearing this risk, the 11.5% coupon is no longer enough.

Of course, from the attackers' perspective, this is also part of putting on a full show: only by having STRC decline alongside can they, under information asymmetry, solidify the "cash flow crisis" narrative, making you wonder:

Is there really some information I don't know?

For fixed-rate bonds, the story essentially ends here. The increase in the market's required return can only be matched by a price drop, so the discount can persist long-term without returning to the par anchor. But STRC is not a fixed-rate bond; it's floating-rate, allowing adjustment of the numerator.

For example, if the market demands a 12% required return to hold STRC, and MSTR management consequently raises the coupon dividend from 11.5%, the price cannot stay below par value 100 for long. In such a case, buying STRC at a discount would yield an actual return above 12%, naturally attracting buy-side pressure that pushes the price to a level where the implied return equals 12%, i.e., par value.

This is why medium-to-long-term floating-rate bonds must anchor to par value 100; it's an inherent property of such instruments.

For MSTR, STRC's price returning to its par anchor of 100 is a prerequisite for its ability to continuously use it for financing. Because if issued at a discount, the company nominally issues $100 face value, but the buyer only pays $90. This means the company incurs dividend obligations based on a $100 face value for only $90 of actual funds received, artificially raising its real financing cost—losing money on every financing round. Is that fucking possible?

Third, When mNAV > 1, Sell Stock, Never Sell Bitcoin

So, what's the key to breaking the deadlock?

As discussed earlier, this entire decline is a reflexive script of a self-fulfilling prophecy, built on information asymmetry and expectations of a cash flow crisis. To break it, one only needs to prove this liquidity crisis doesn't exist, refilling the reserves, and the attack loses its footing, breaking the reflexive spiral.

How to replenish reserves?

As many on X have shouted, should Saylor just come out and say, "In this decline, we sold more BTC, and now we have ample funds for several years"? This move would certainly work, and the panic would end.

But its cost is another layer of implied uncertainty.

Because it tells the market: You need to reprice me.

The capital market premium flywheel narrative of "continuous accumulation, never selling Bitcoin, constantly increasing BTC per share for shareholders" would surely be gone. It would shift to, "May sell significant amounts of BTC to shrink the balance sheet if necessary, thereby diluting BTC per share," at least a discounted flywheel taking three steps forward, one step back.

The result is you don't know how common shareholders will react, and whether mNAV might completely disappear. Even if it doesn't disappear, narrowing is highly likely. After all, the premium for the part where mNAV > 1 corresponds to an implicit Call Option on "future increased BTC per share" for MSTR. If the acceleration of BTC per share growth slows, the Call naturally becomes less valuable.

The importance of mNAV premium to MSTR is self-evident. MSTR's expansion logic doesn't rely solely on common stock or leverage instruments like STRC (debt in substance), but on a cycle of adding water when there's more flour, and flour when there's more water, thereby keeping overall leverage from spiraling out of control, maintaining its ideal 33-35% range. A narrowing mNAV premium would directly impact the window for subsequent equity financing, constituting a poison-quenching-thirst action.

A better approach, in my view, would be to leverage the current situation where mNAV = 1.25x, and the premium remains significant, to raise cash reserves by issuing and selling stock. MSTR previously registered a Shelf Offering with the SEC with ample capacity. This is the only operation that clearly pleases both STRC holders (debt in substance) and common shareholders simultaneously, without the risk of repricing.

The specific mechanism is:

When mNAV is significantly greater than 1, choosing to issue and sell stock first means that for every $1 of stock you issue and use entirely to buy BTC, you create more than $1 of shareholder value in the capital market. This is precisely why shareholders are willing to give you money. And precisely because of this, in this state, you don't actually need to use all the raised funds to buy BTC: you can retain a portion as cash reserves for future debt servicing, without negatively impacting shareholder value. Meanwhile, increased cash reserves make STRC holders feel safer, the alarm dissipates, risk premiums decrease, and STRC gradually returns to its anchor, allowing subsequent STRC financing if desired. It doesn't hinder either.

Conversely, choosing to sell Bitcoin for cash is drinking poison to quench thirst. Once repricing causes mNAV to narrow or disappear, the path of issuing stock to buy BTC becomes impassable. At that point, your stock's fair value equals its underlying BTC—why wouldn't I just buy BTC directly? Moreover, if you then retain a portion of the financing for interest payments, that's outright negative shareholder value: taking my money, part to buy BTC (creating value just breaking even in the capital market), and another part directly used for interest payments, which is pure loss.

This is a net bleed structure.

By then, as equity issuance becomes unfeasible, STRC issuance would also gradually be affected. Not only would the overall expansion flywheel likely get stuck, but your financing window would also close, forcing reliance on cash reserves. Once those are exhausted, you're truly left with only selling Bitcoin, and that's the end.

Moreover, selling stock has the added benefit of directly improving the leverage ratio. Currently, with BTC at $61k, MSTR's overall leverage ratio has increased from the target 33-35% to about 43%. Issuing and selling stock brings in equity capital: cash (asset side) increases, equity increases. After deducting a small portion retained for interest payments, the overall leverage ratio would actually improve further.

And selling Bitcoin? Because the cash from selling BTC is immediately paid out as dividends, the asset side first sees BTC decrease, then cash outflow. The net effect is total assets shrink, liabilities remain unchanged, and the leverage ratio actually worsens slightly.

Sell stock: Improves leverage ratio ✓, Preserves BTC per share ✓, Doesn't harm premium ✓

Sell Bitcoin: Worsens leverage ratio, Reduces BTC per share, Severely harms premium

The superiority is clear.

Finally, if, I mean if,

MSTR truly sells large amounts of Bitcoin to replenish reserves?

Then, indeed, as many X influencers, including those from Delphi, have said, the short-term crisis would be resolved, BTC would rebound, and STRC would return to its anchor. This is precisely why I say, if MSTR were to truly die, it wouldn't be this time. Whether selling stock or Bitcoin can indeed solve the immediate crisis.

But personally speaking, for me, MSTR and Saylor would then be demystified.

And due to the repricing of common stock logic, that "BTC per share" Call Option would no longer be as valuable, causing the mNAV premium to gradually disappear. This could lead to a strange divergence: BTC rebounds, STRC returns to anchor, while MSTR common stock反而下跌.

And next time, when cash reserves dwindle again, and the market anticipates Bitcoin sales again, the reflexive script plays out once more. Then, who knows if it's the beginning of the end.

But honestly, I would accept such an outcome.

Perhaps "change" itself is part of this "game."