Провайдер стейкинга Ethereum Lido сообщил о снижении годовой выручки, ссылаясь на сложную макросреду и конкуренцию.

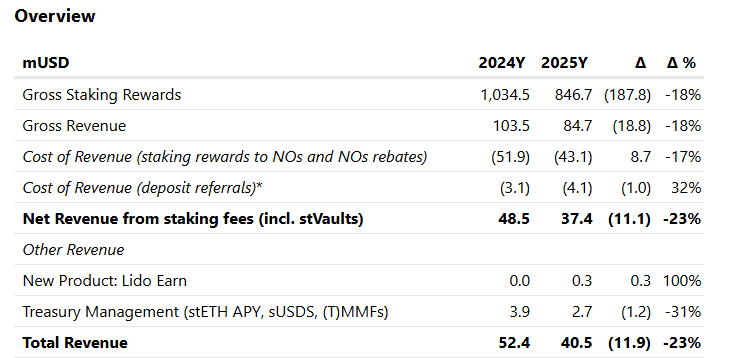

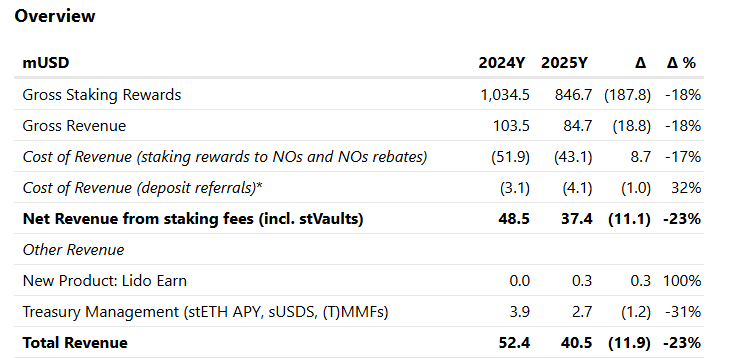

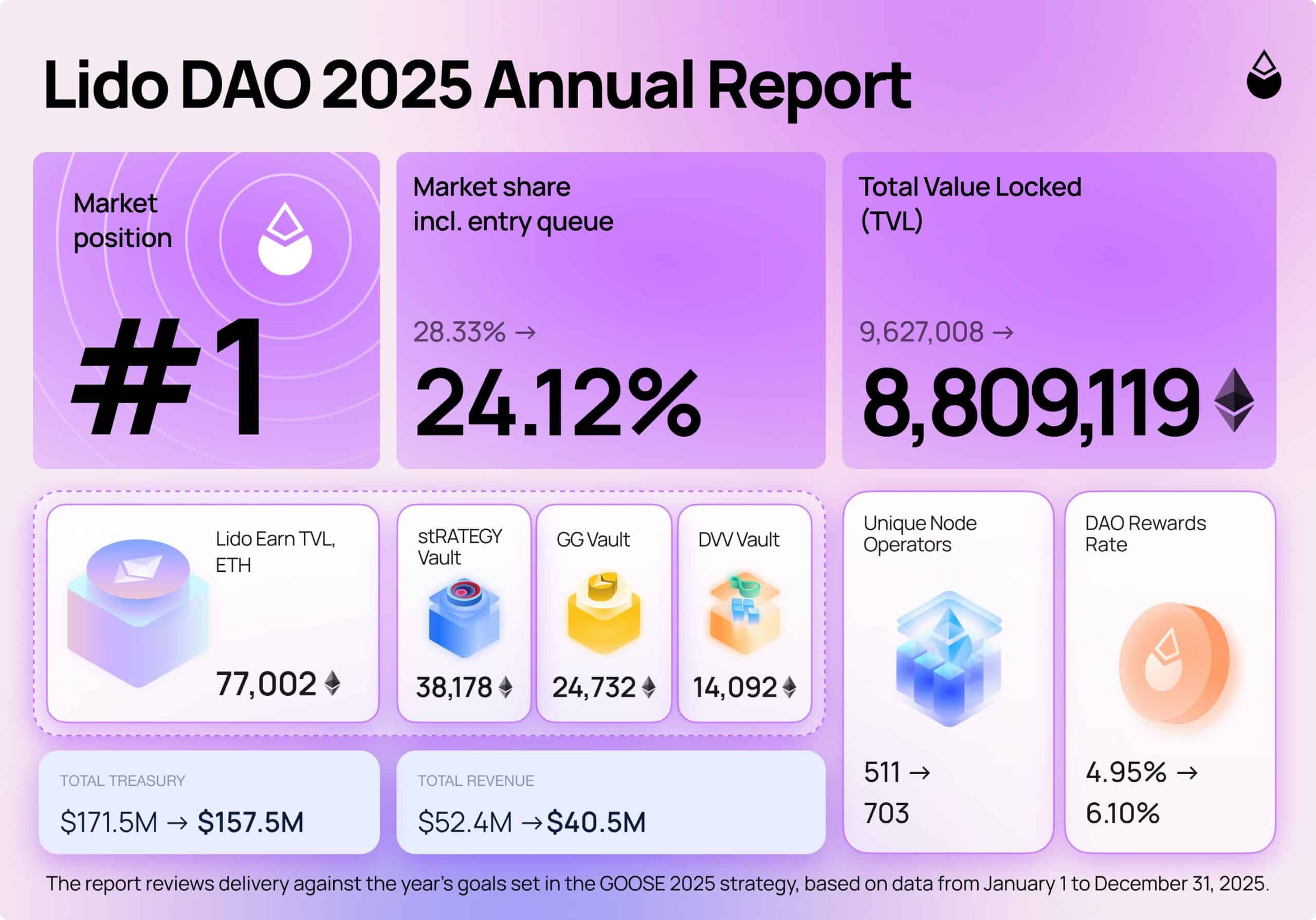

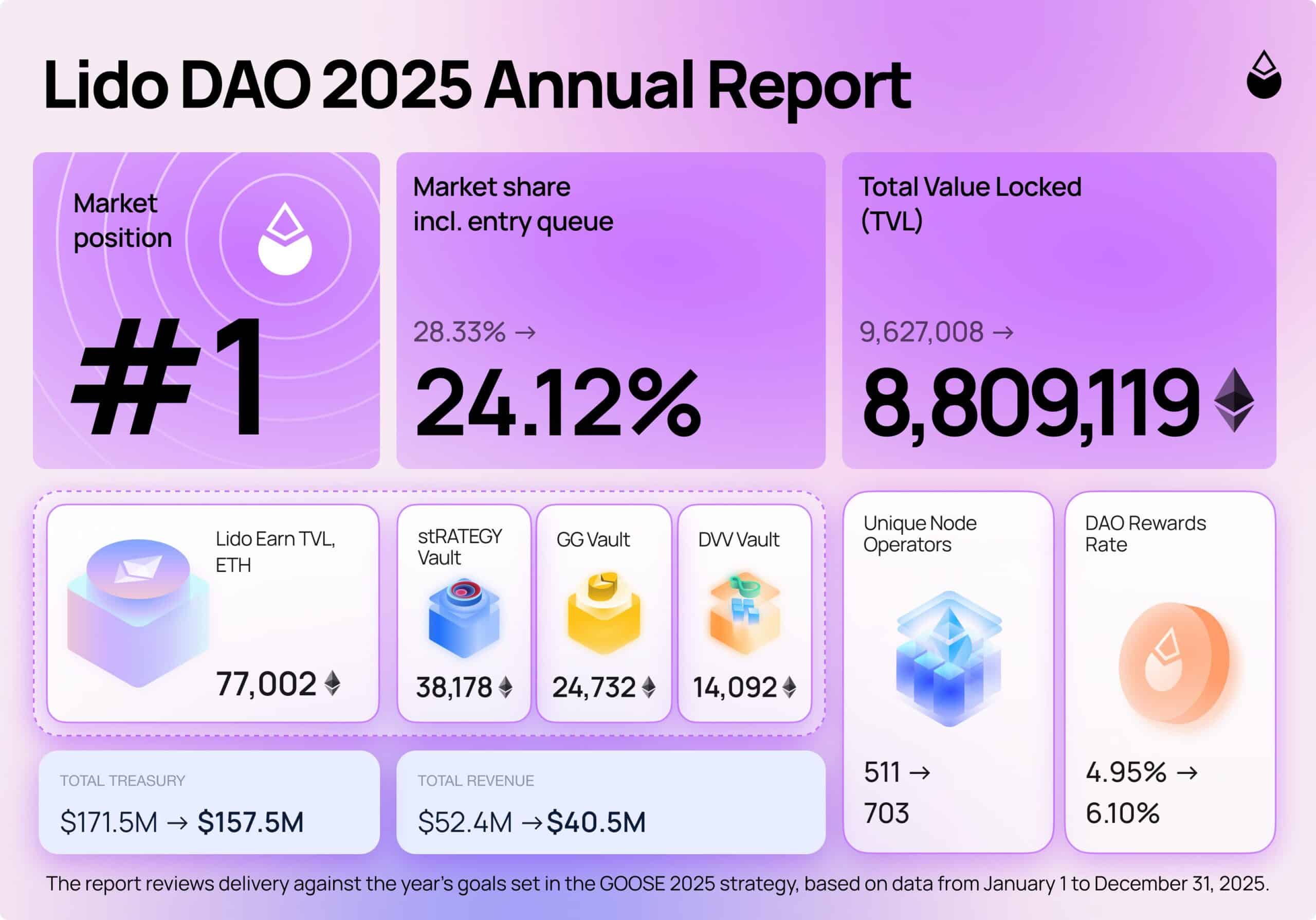

В своем годовом отчете за 2025 год Фонд Lido сообщил, что общая выручка протокола составила 40,5 миллиона долларов, что ниже 52,4 миллиона долларов, достигнутых в 2024 году — снижение выручки на 23% в годовом исчислении (YoY).

Лидерство Lido на рынке сталкивается с препятствиями

Комментируя падение выручки, Lido отметил:

2025 год прошел под знаком сжатия вознаграждений, вызванного оттоками стейкинга и общесетевым снижением годовой процентной доходности (APR) стейкинга.

Что касается оттоков стейкинга, протокол отметил, что это было дополнительно подогрето структурным сдвигом в сторону биржевого и институционального стейкинга.

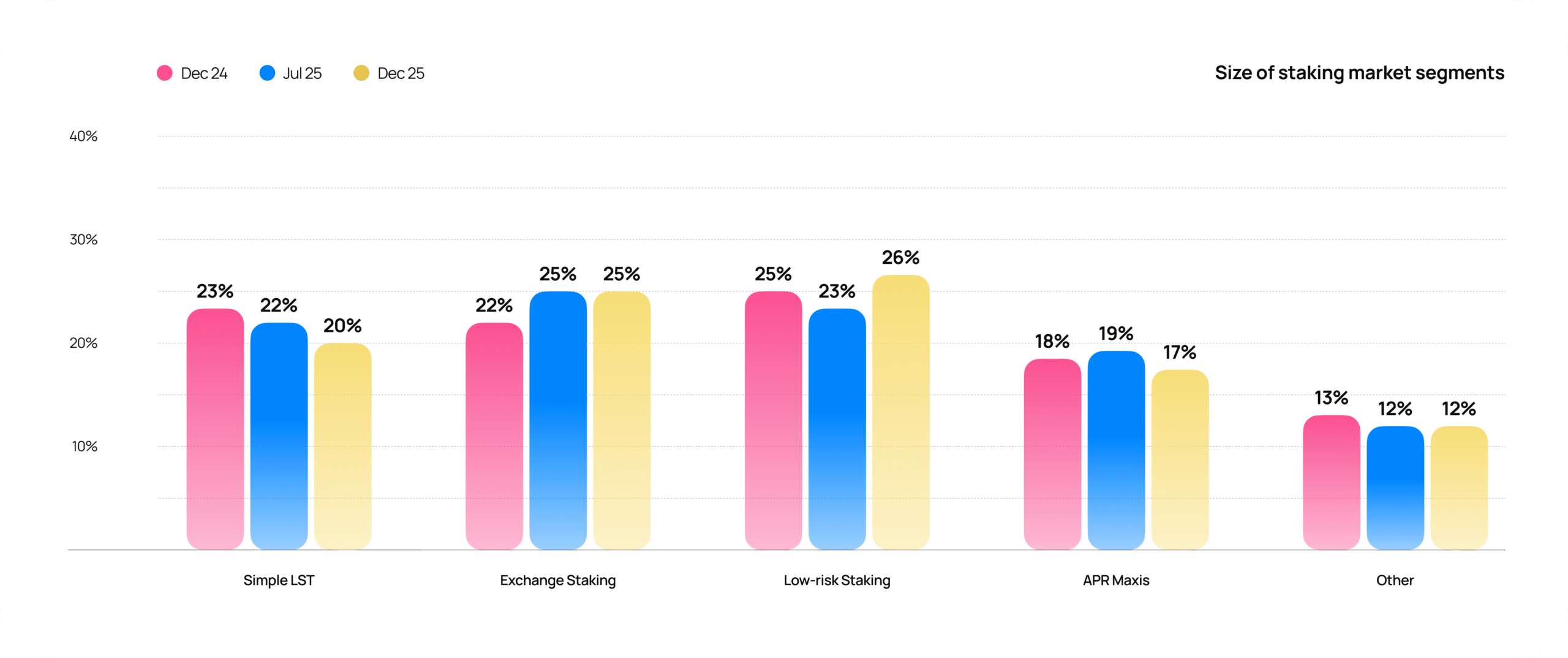

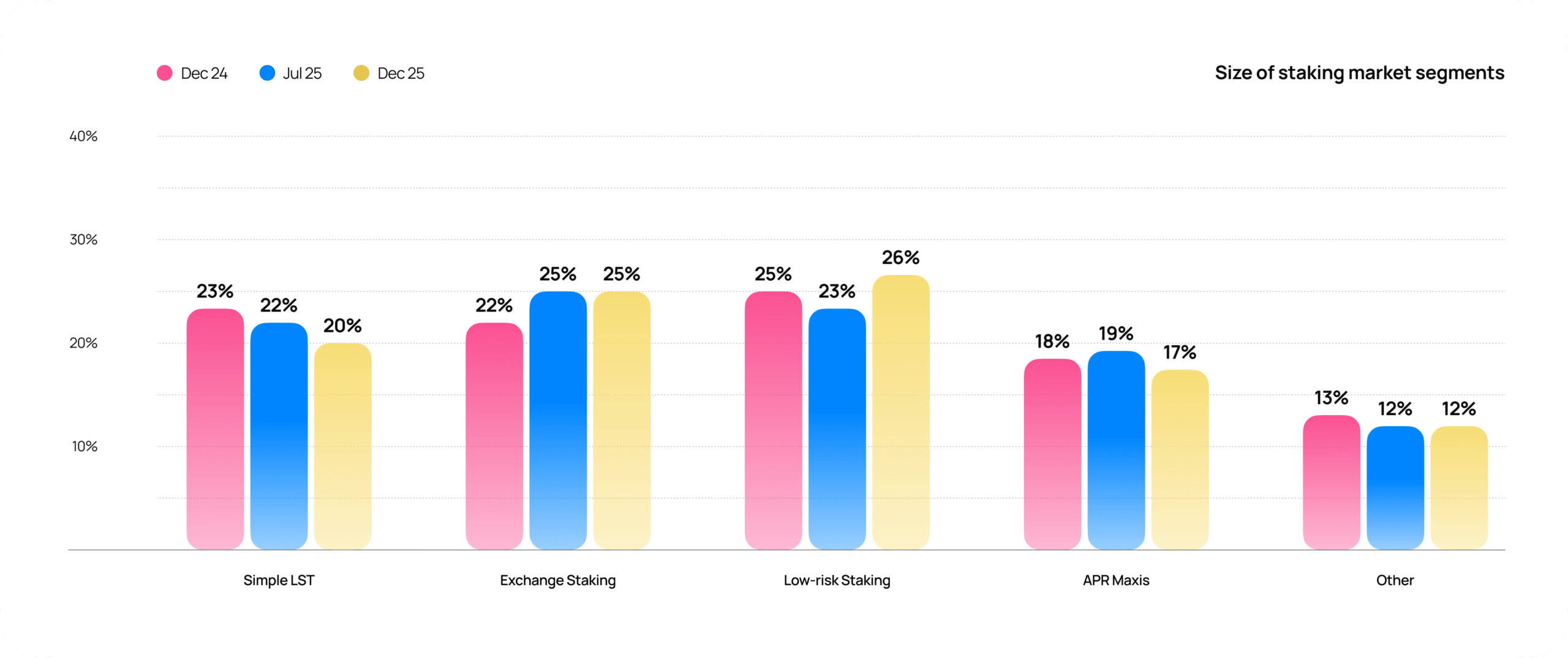

Переток капитала от простых LST к биржевому и институциональному стейкингу, а также усиление конкуренции сократили размер сегмента, в котором Lido удерживает лидерство в категории.

Спрос на стейкинг в последние месяцы резко вырос, достигнув рекордных 30,7% от общего предложения ETH (38,2 миллиона ETH в стейкинге). Этот рост был обусловлен спотовыми ETH ETF и казначейскими фирмами, активирующими функцию получения дохода для своих инвесторов.

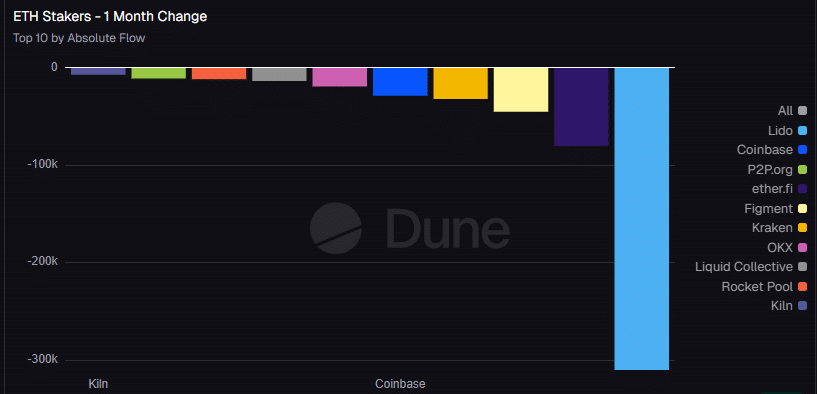

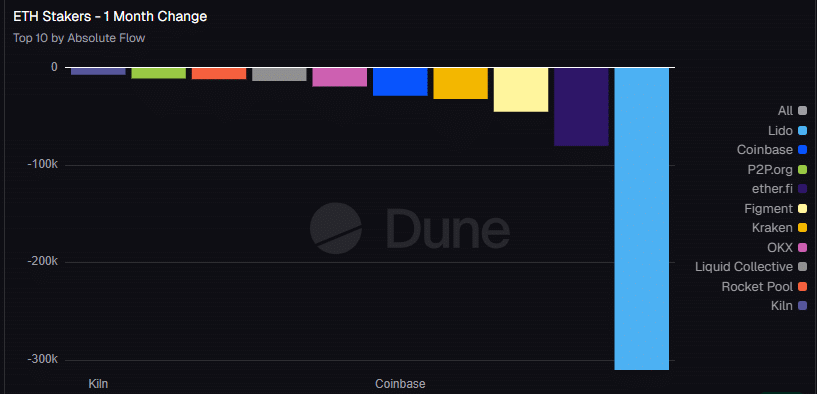

В отличие от этого, оттоки из Lido не прекращались даже в 2026 году. Только в марте Lido лидировал по оттокам стейкинга, с почти 310 тыс. ETH, покинувшими протокол.

Несмотря на это, Lido сохранил свою доминирующую долю рынка на уровне 24% (8,8 миллиона ETH в стейкинге). Однако в 2026 году он сосредоточится на диверсификации.

Это будет включать удвоение усилий по институциональным каналам дистрибуции для сегментов стейкинга с низким риском (например, через WisdomTree Physical Lido Staked Ether), расширение своего продукта Lido Earn и масштабирование своей валидаторской торговой площадки.

Планы по согласованию токена LDO

Lido также отметил, что будет продвигать «более сильное экономическое согласование» между производительностью протокола и LDO. Согласно текущим обсуждениям, часть плана накопления токенов будет включать автоматический выкуп токенов через «фонд избытка казначейства».

Это предложение было выдвинуто в ноябре прошлого года с годовым бюджетом в 10 миллионов долларов для программы выкупа. Официальный план по этому вопросу ожидается во втором квартале 2026 года, но еще предстоит увидеть, как на это обновление отреагирует LDO, собственный токен протокола.

На момент написания статьи LDO торговался по цене 0,299 доллара и упал на 80% с максимума второй половины 2025 года в 1,5 доллара.

Итоговый обзор

- Выручка Lido упала на 23% до 40,5 млн долларов на фоне растущей конкуренции в стейкинге со стороны спотовых ETH ETF, казначейских фирм и централизованных бирж.

- Согласование токена LDO и программа выкупа на 10 млн долларов, как ожидается, будут формализованы во втором квартале 2026 года.