Автор | Сян Сяньчжи

Позавчера вечером MoonDark выпустила Kimi K2.6 и подняла цену на API-ввод с 0,60 доллара до 0,95 доллара за миллион токенов.

Рост на 58%. Это первое повышение цен с момента запуска серии K2.

Но, кажется, никто не обращает на это внимания.

Четыре месяца назад, во внутреннем письме в последний день 2025 года, Ян Чжилинь написал, что MoonDark «не спешит с IPO в краткосрочной перспективе». В то время проспекты Zhipu и MiniMax уже были поданы в Гонконгскую фондовую биржу, что явно было намеренным позиционированием.

В том же письме он написал, что денежные резервы компании превышают 1,4 миллиарда долларов, а раунд C в 500 миллионов долларов был переподписан — подтекст в том, что потенциал рынка private equity еще не раскрыт полностью, с public market можно не спешить.

Три месяца спустя Bloomberg сообщил, что он начал переговоры с CICC и Goldman Sachs. Еще через три недели был запущен K2.6.

Человек, который не любит «спешить», за четыре месяца сделал то, о чем ранее говорил, что не будет делать.

K2.6 — определенно не последний релиз продукта от MoonDark перед IPO. Но этот релиз — первая презентация для инвесторов от Ян Чжилиня после того, как MoonDark запланировала выход на биржу.

Kimi никогда раньше не выпускала модель таким образом

У Kimi был устоявшийся порядок выпуска моделей.

Публикация технического отчета, открытие весов, подъем в рейтинге HuggingFace, а затем — оценка технического сообщества. K1.5 противопоставлялся o1 с методологией логического вывода, технических деталей было больше, чем цифр benchmark; K2 Thinking просто выложил веса на HuggingFace, позволив разработчикам самим проводить тесты. Эти действия были адресованы разработчикам и исследователям.

Риторика также была из технического сообщества: какие проблемы мы решили, почему наш метод лучше, добро пожаловать к воспроизведению.

С K2.6 все иначе.

Сначала о повышении цен. В юанях цена ввода K2.6 составляет 6,5 юаня за миллион токенов (при промахе кэша), а K2.5 — 4 юаня. Цена вывода выросла с 21 юаня до 27 юаней. Цена при попадании в кэш составляет 1,1 юаня.

Это структурированное повышение цен. На поверхности все уровни дорожают, но уровень с попаданием в кэш подорожал меньше всего — с 0,7 юаня до 1,1 юаня, в долларах это 0,16 доллара за миллион токенов.

Эти 0,16 доллара — ключ к пониманию этого повышения цен.

Для корпоративных пользователей, долгое время использующих один и тот же system prompt: помощники по коду, фреймворки для оркестрации агентов, умные客服, у которых префикс сильно переиспользуется, уровень попадания в кэш может достигать 75-83%. MoonDark оставила для этих клиентов цену, близкую к прежней.

Для разрозненных клиентов, которые используют сервис время от времени, с каждый раз новым промптом, повышение цен легло на них в полной мере.

Это дружественное изменение цены для «предприятий, уже привязанных к Kimi», и недружественное — для «разрозненных клиентов, которые все еще сравнивают цены». Первые — это «закрепленные корпоративные клиенты» в истории для биржи, вторые — «длиннохвостные пользователи», которые не появятся в презентации для инвесторов. MoonDark хорошо понимает, кто является ее активом для оценки.

Структура вычислительных мощностей в эпоху агентов отличается от эпохи чатов. Модели для диалога — это десятки токенов в запросе-ответе, агенты — это тысячи вызовов инструментов и потребление сотен тысяч токенов. В официальных примерах K2.6 — локальное развертывание на Mac модели Qwen3.5, вызывающей инструменты более 4000 раз,持续 12 часов, рефакторинг движка для открытых торговых систем exchange-core за 13 часов и 1000+ вызовов инструментов, и экстремальный пример — 5 дней автономной работы мониторинга, оповещений и реагирования на сбои — потребление токенов для этих единичных задач в сотни и даже тысячи раз выше, чем в сценариях диалогов времен K2.5.

Конечно, эти примеры приведены для демонстрации способностей к длинным рассуждениям, но с добавлением кластера из 300 агентов в K2.6, потребление токенов должно быть ошеломляющим.

По старой цене 0,60 доллара такой вызов агента, возможно, был убыточным. По цене 0,95 доллара — едва покрывает стоимость логического вывода.

Так что повышение цен — не уверенность, а необходимость. MoonDark привлекла в общей сложности 2,5 миллиарда долларов, с раунда C до C+ есть денежный резерв в 1,4 миллиарда долларов, но если следующее поколение K3 действительно будет иметь масштаб в 3-4 триллиона параметров, один цикл предобучения может съесть половину этой суммы.

Без повышения цен данные о валовой прибыли за последние несколько кварталов перед IPO будут выглядеть плохо. Проспект эмиссии требует раскрытия валовой маржи.

Это можно было бы объяснить открыто — эпоха агентов требует новой модели ценообразования. Но MoonDark этого не сделала. Потому что пользователи из C-сегмента только недавно перешли с бесплатного периода K2 Thinking, и сейчас рассказывать им «я подорожал» — не лучшая продуктовая история.

Это история для другой аудитории — у Kimi уже есть пул корпоративных клиентов, которые от него зависят, и они будут использовать его, даже если он станет дороже. (Например, я сам)

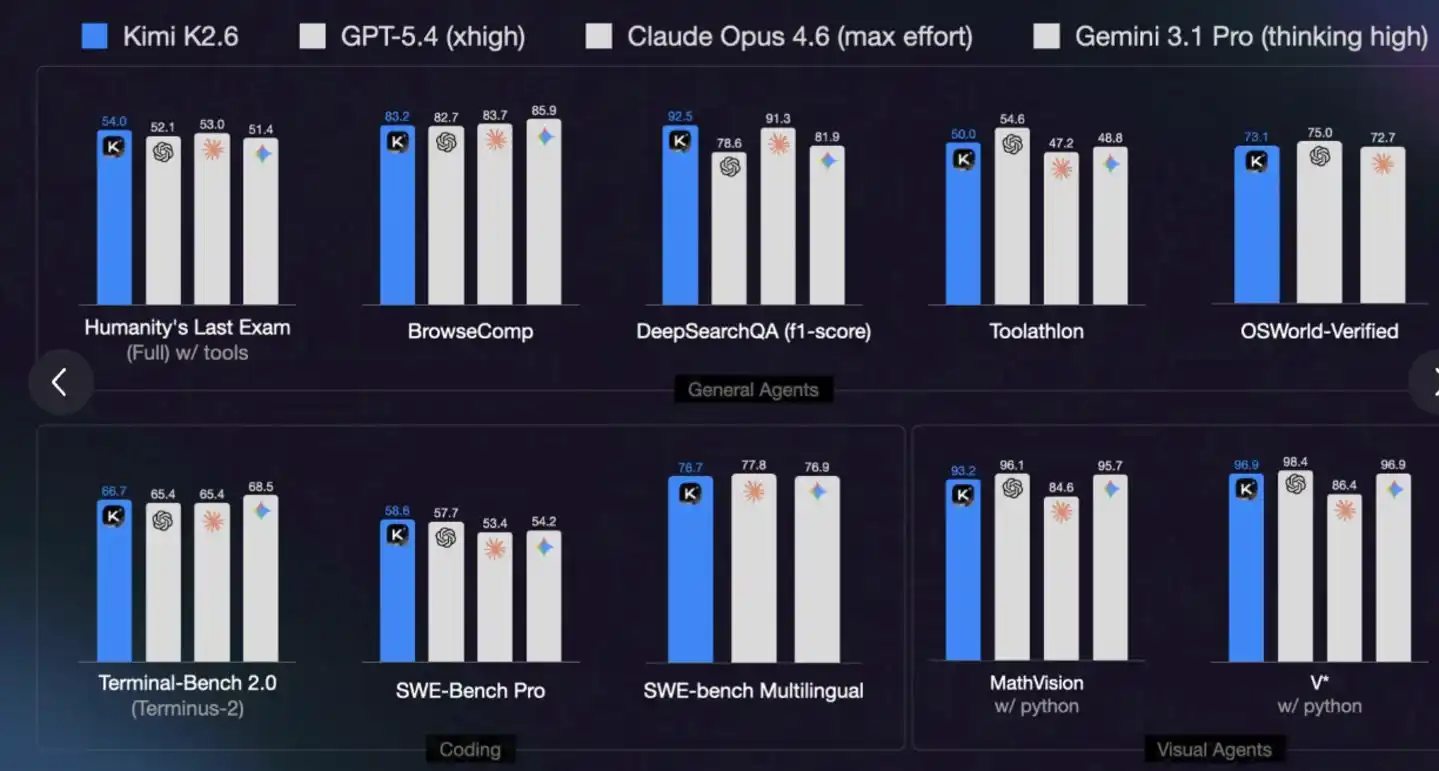

Вторая вещь — эталонное сравнение (бенчмаркинг). Официально выбранные K2.6 ориентиры — это GPT-5.4, Claude Opus 4.6, Gemini 3.1 Pro. Все три — флагманы предыдущего поколения.

На той же неделе Anthropic выпустила Claude Mythos, Opus 4.7 тоже только что запущен — оба на поколение сильнее, чем Opus 4.6. K2.6 не сравнивается с ними.

Это активный выбор. При сравнении с Mythos, K2.6 оказывается в позиции «догоняющего»; при сравнении с Opus 4.6, K2.6 оказывается в «первом эшелоне». Для оценки в 18 миллиардов долларов нужна последняя.

Kimi раньше такого не делала. При выпуске K2 Thinking официально запустили полный бенчмарк, были хорошие и плохие результаты, все выложили, чтобы разработчики сами оценили. Это была игра по правилам технического сообщества — сообщество понимает, где ты силен, где слаб, и готово принять модель с явными недостатками, но четкой roadmap.

Презентация для инвесторов — нет. Презентация для инвесторов требует заключения, которое управляющий фондом поймет за 30 секунд: «наравне или лучше ведущих международных проприетарных моделей». Это дословная цитата из официального блога K2.6.

Третья вещь — кластер агентов и двухколейность open source. K2.6 обновила штуку под названием Claw Groups — экосистема гетерогенных агентов, где агенты на разных устройствах, с разными моделями, с разными инструментальными цепочками работают в одном пространстве для collaboration, а K2.6 выступает orchestrator-ом. 300 дочерних агентов работают параллельно, 4000 шагов协同, 5 дней автономной работы.

Эти цифры адресованы корпоративным клиентам. Не разработчикам. Для разработчика «300 параллельных агентов» не имеет практического смысла — он не будет запускать 300 агентов в локальном проекте. Эта конфигурация имеет смысл только для одного типа клиентов: крупных предприятий, которым нужно автоматизировать сквозные бизнес-процессы с помощью матрицы агентов.

Ориентир — история Salesforce, а не история HuggingFace.

При этом K2.6 полностью открыта. Ян Чжилинь на форуме в Чжунгуаньцуне 26 марта сказал, что open source — это абсолютная победа.

Open source + корпоративные кластеры агентов — это позиция посередине между DeepSeek и Anthropic, половина от каждой модели. Звучит как хорошая история. Но занятие обеих позиций означает, что нужно доказывать обе.

Рынок капитала на самом деле не волнует, есть ли ответы на эти вопросы. Он только требует, чтобы у вас была история по каждому направлению.

Повышение цен, бенчмаркинг, кластер агентов — у этих трех вещей есть одно аномальное общее свойство. Ни одна из них не предназначена для технического сообщества.

Прежняя глубинная логика выпуска моделей Kimi была такой — если разработчики меня любят, корпоративные клиенты рано или поздно подтянутся, а рынок капитала — тем более. У этой тактики есть название — техническая искренность.

K2.6 не ждет. Повышение цен — прямое заявление о ценообразовании для B2B, сравнение с GPT-5.4 — заблаговременное занятие позиции для оценки, кластеры агентов и Claw Groups — образец истории корпоративного обслуживания.

Каждый пункт соответствует вопросу в презентации для инвесторов: какова ваша коммерциализация? Каково ваше позиционирование? Каковы ваши барьеры для B2B?

Сжатие срока с Preview до GA до 8 дней — тоже эта логика. Предыдущие версии серии K2 проходили 2-3-месячный preview-период, чтобы сообщество протестировало, дало обратную связь, итеративно улучшило. K2.6 не оставила себе этого пространства. Не потому что технологии созрели быстрее, а потому что временное окно не ждет.

IPO во второй половине 2026 года, по процедуре Гонконгской биржи требуется оставить 4-6 месяцев на подачу заявки, запросы, заслушивание, roadshow, ценообразование, период охлаждения. Запуск roadshow в сентябре означает, что продукт должен быть готов к апрелю.

Если не выпустить GA в апреле, потом окна не будет.

K3 — настоящая кульминация

Но K2.6 — тоже не самая сильная карта, которую может разыграть MoonDark.

В официальном блоге есть сдержанная фраза — K2.6 это «взлетно-посадочная полоса для K3».

12-часовое длинное кодирование, кластер из 300 агентов, компрессор контекста — это не конечная форма серии K2, это инфраструктура уровня исполнения, которую может нести更大的 базовая модель. MoonDark не стала бы тратить силы на доведение этой штуки до ума, если бы не была уверена, что есть更大的 модель, которой потребуются эти возможности.

Ранее на Reddit просочилась информация о K3, целевой масштаб параметров — 3-4 триллиона. По сравнению с триллионным масштабом серии K2, это скачок базовой модели.

Если K3 успеют выпустить в окно для roadshow — это будет настоящий ответ. Взлетно-посадочная полоса, подготовленная K2.6, взлет K3.

Вопрос в том, успеют ли. Сколько времени нужно для обучения модели на 3-4 триллиона параметров? У GPT-5 и Claude Opus 4.6 цикл предобучения составляет около 6-9 месяцев, пост-обучение и оценка безопасности добавляют еще несколько месяцев. Могут ли существующие вычислительные мощности MoonDark — судя по сотрудничеству с Alibaba Cloud и текущим денежным резервам — сжать этот цикл до 5-6 месяцев?

Эта ставка сделана на K2.6.

8 дней с Preview до GA, кластер агентов одним махом расширен со 100 до 300, длинное исполнение растянуто с нескольких сотен шагов до 4000 — каждое действие сжимает время, освобождая пространство для возможности K3.

Если K3 удастся выпустить к августу-сентябрю — это будет кульминационный номер на roadshow.

Если не успеют — K3 станет «моделью, которую можно выпустить только после IPO», и K2.6 придется одной тянуть всю нарративу оценки.

MoonDark ставит на то, что успеет.

На что ориентирована оценка в 18 миллиардов долларов

Вернемся к оценке.

Три месяца назад оценка MoonDark составляла 4,3 миллиарда долларов, два месяца назад — 5,5 миллиарда долларов, сейчас — 18 миллиардов долларов.

Не то чтобы MoonDark за эти три месяца стала в четыре раза сильнее. Просто Zhipu и MiniMax после выхода на биржу выросли в 4 раза, подняв потолок всей отрасли. Рыночная капитализация Zhipu в Гонконге составляет 305 миллиардов гонконгских долларов, MiniMax — 309,2 миллиарда гонконгских долларов — рыночная капитализация обеих компаний превысила исторический максимум SenseTime.

Логика рыночной капитализации этих двух компаний — не «что может сделать下一代 технология», а «насколько можно оценить активы ИИ в гонконгском пуле».

Оценка MoonDark в 18 миллиардов долларов ориентирована на то же самое. Она больше не доказывает, что она сильнейшая китайская AI-компания, она доказывает, что она — оцениваемая китайская AI-компания.

Все действия K2.6 — повышение цен, бенчмаркинг, кластер агентов, двухколейность open source — отвечают на этот тезис.

Но有一件事 K2.6 еще не доказала. Готовы ли пользователи C-сегмента Kimi платить за подорожавший K2.6? Перетекут ли платные подписчики в DeepSeek или MiniMax? Сколько среди корпоративных клиентов тех, кто реально запускает Claw Groups, а сколько просто подписали POC?

Эти цифры — то, что инвесторы обязательно спросят во время roadshow. K2.6 сейчас может только выставить продукт. Станет ли это цифрами — зависит от следующих трех месяцев.

Zhipu при выходе на биржу подала проспект, где прибыль еще не вышла в плюс, MiniMax тоже. Инвесторы приняли эту историю, потому что тогда большая нарратива «активы китайского ИИ» только открылась. MoonDark опоздала на полгода. На тот же вопрос Zhipu и MiniMax могли сказать «мы проверяем», а MoonDark должна сказать «мы монетизируем».

Все это давление ложится на три месяца между K2.6 и K3.

Так что вернемся к最初 тому вопросу — K2.6 — это последняя презентация для инвесторов перед IPO от MoonDark?

Нет.

Если K3 успеет в окно roadshow, то K3 — настоящая кульминация. K2.6 — лишь подготовленная для нее взлетная полоса. Если K3 не успеет в окно roadshow, то K2.6 придется тянуть всю историю IPO до конца. Тогда это будет первая презентация, которую Ян Чжилинь был вынужден начать раньше времени.

Ни того, ни другого результата Ян Чжилинь не хотел четыре месяца назад.

Но все, что произошли за эти четыре месяца — выход на биржу Zhipu и MiniMax, подъем потолка оценок, сжатие временного окна — заставили человека, который не любит «спешить», поспешить.

Когда выйдет K3, это будет вторая презентация.