Гонконг отложил выдачу первой партии лицензий на стейблкоины из-за опасений отмывания денег, что может потребовать ужесточения правил KYC.

Гонконг отложил выдачу первой партии лицензий на стейблкоины

Как сообщает Wu Blockchain со ссылкой на Caixin, Гонконг отложил выдачу первых разрешений на стейблкоины, что означает, что заявителям придется ждать дольше, прежде чем они получат лицензию.

Гонконг впервые принял закон о стейблкоинах в августе 2025 года, установив, что организации, желающие выпускать стейблкоины в юрисдикции китайского города, должны получить одобрение Валютного управления Гонконга (HKMA).

После введения новых правил HKMA начала принимать заявки от таких крупных имен, как Standard Chartered в своем совместном предприятии (СП) и HSBC. Ожидалось, что первая партия одобрений будет выдана к концу марта, но сейчас уже начался апрель, а лицензии так и не были выданы.

«Гонконг обеспокоен тем, что стейблкоины могут использоваться для отмывания денег, и поэтому может ввести более строгие правила KYC», — отметил Wu Blockchain. Задержка нарушила планы 36 заявителей. Ранее регуляторы материкового Китая обрушились на этот сектор, заявив, что привязанные к фиату криптовалюты не являются законным платежным средством, поскольку они не соответствуют регуляторным требованиям и несут риск использования в незаконной деятельности.

Несмотря на позицию материка, Гонконг все же продвинулся вперед со своими планами по стейблкоинам, объявив в феврале, что «очень небольшое количество» лицензий эмитентов будет выдано в марте. Поскольку этот план не осуществился, теперь остается ждать, когда HKMA сможет продвинуть амбиции города в отношении стейблкоинов.

В других частях Азии планы Южной Кореи по стейблкоинам также забуксовали: Банк Кореи (BoK) выступает за стейблкоины с преобладанием банков, а Комиссия по финансовым услугам (FCS) ратует за более мягкие правила.

Тем временем Япония опередила своих соседей, запустив в прошлом году свою первую иеновую монету. В этом году страна также может увидеть свой первый банковский стейблкоин: Shinsei Trust and Banking планирует запуск во втором квартале 2026 года.

В Соединенных Штатах президент Дональд Трамп подписал в прошлом году закон GENIUS Act, предусматривающий формальные рамки для стейблкоинов. В целом, эта часть сектора криптовалют продемонстрировала значительный глобальный регуляторный импульс за последний год, поэтому неудивительно, что ее рыночная капитализация сохранилась относительно хорошо, несмотря на недавний спад на рынке.

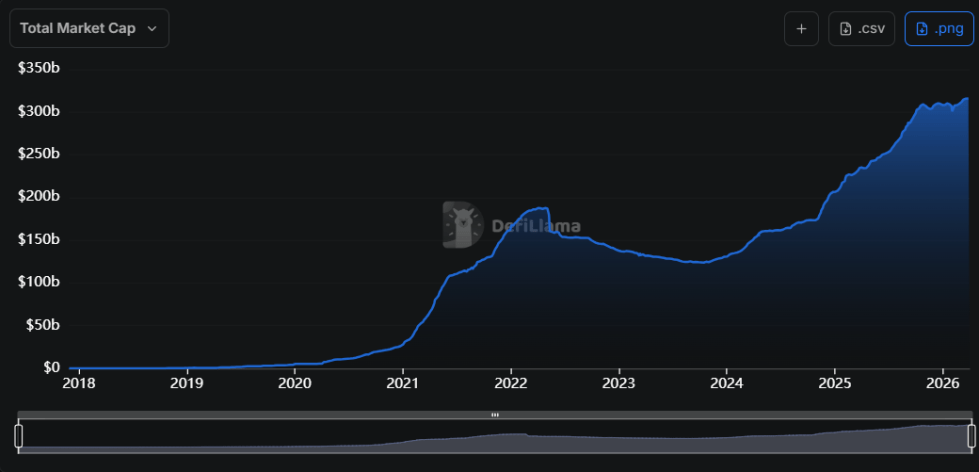

Динамика рыночной капитализации стейблкоинов за последние несколько лет | Источник: DefiLlama

Как показывает график от DefiLlama, рыночная капитализация токенов, привязанных к фиату, в последние месяцы в основном двигалась в боковом тренде, а ее текущее значение составляет 316 миллиардов долларов, что является новым историческим максимумом (ATH).

Цена Биткоина

На момент написания Биткоин торгуется около 68 700 долларов, потеряв более 4% за последнюю неделю.

Похоже, цена монеты немного выросла за последние сутки | Источник: BTCUSDT на TradingView