Оригинальный автор: Todd Wenning

Оригинальная компиляция: Deep Tide TechFlow

Введение: Академическая финансовая теория разделяет риск на системный и специфический. Аналогично, отказы акций также делятся на два типа: вызванные рынком системные отказы (как финансовый кризис 2008 года) и специфические для компании отказы (как обвал акций программного обеспечения из-за текущих опасений по поводу ИИ).

Todd Wenning на примере FactSet указывает: при системном отказе вы можете использовать поведенческое преимущество (терпеливо дожидаясь восстановления рынка); но при специфическом отказе вам нужно аналитическое преимущество — ваше видение компании через десять лет должно быть точнее, чем у рынка.

В условиях текущего воздействия ИИ на акции софта инвесторы должны различать: это временная паника на рынке или рвется по-настоящему?

Не используйте грубые поведенческие решения для проблем, требующих тонкого анализа.

Полный текст如下:

Академическая финансовая теория считает, что существует два типа риска: системный и специфический.

- Системный риск — это неизбежный рыночный риск. Его нельзя устранить диверсификацией, и это единственный тип риска, за который вы получаете вознаграждение.

- С другой стороны, Специфический риск — это риск, специфичный для компании. Поскольку вы можете дешево купить диверсифицированный портфель из несвязанных businesses, вы не получите вознаграждение за принятие этого риска.

Мы можем как-нибудь обсудить современную теорию портфеля, но системно-специфическая структура полезна для понимания различных типов отказов (процентное падение от пика до минимума инвестиций) и того, как мы, как инвесторы, должны оценивать возможности.

С того момента, как мы взяли в руки первую книгу о стоимостном инвестировании, нас учили использовать расстроенного Мистера Рынка при продаже акций. Если мы сохраним хладнокровие, когда он теряет рассудок, мы докажем, что являемся стойкими стоимостными инвесторами.

Но не все отказы одинаковы. Некоторые вызваны рынком (системные), а другие специфичны для компании (специфические). Прежде чем действовать, вам нужно знать, на какой тип вы смотрите.

Сгенерировано Gemini

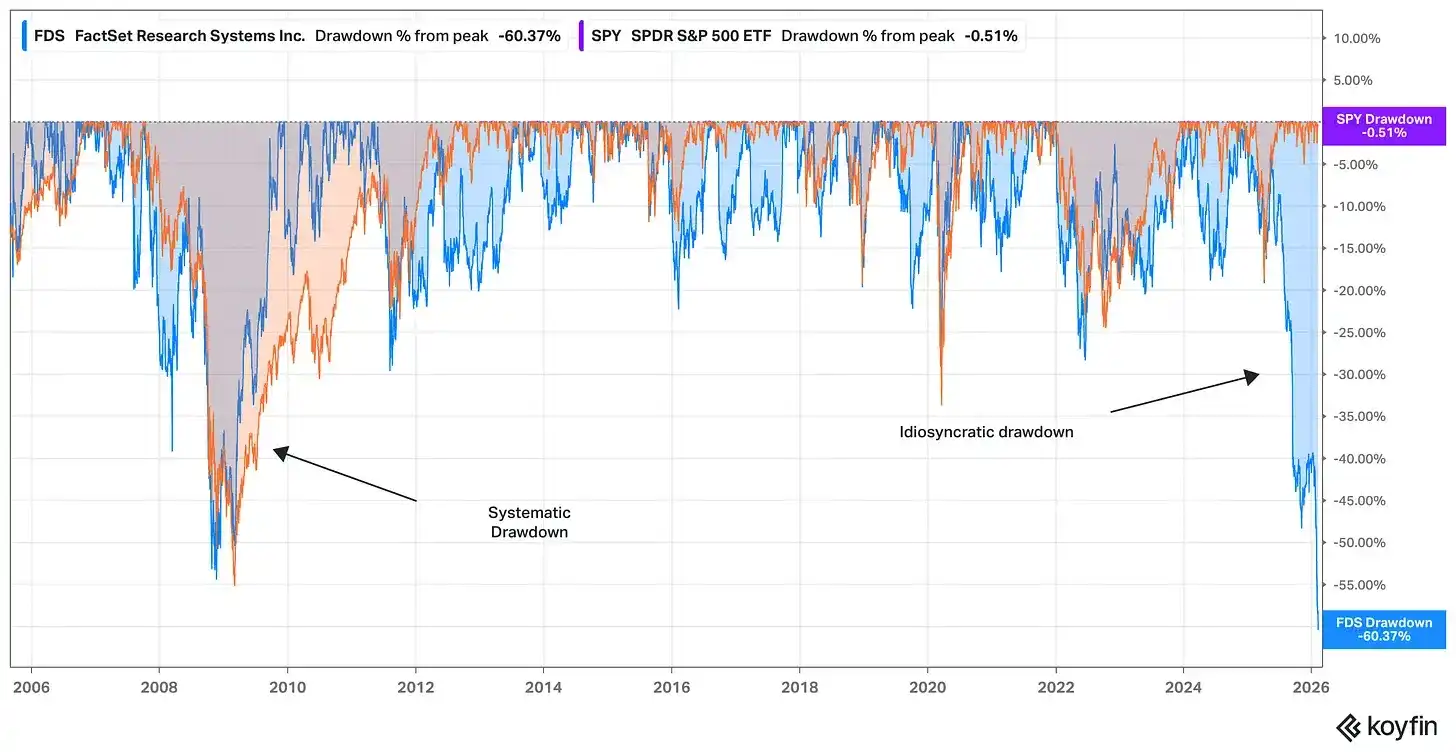

Недавние продажи акций программного обеспечения из-за опасений по поводу ИИ иллюстрируют это. Давайте посмотрим на 20-летнюю историю отказов между FactSet (FDS, синий) и S&P 500 (измеряемым через ETF SPY, оранжевый).

Источник: Koyfin, по состоянию на 12 февраля 2026 г.

Отказы FactSet во время финансового кризиса были в основном системными. В 2008/09 годах весь рынок беспокоился о долговечности финансовой системы, и FactSet также не мог избежать этих опасений, особенно потому, что он продает продукты финансовым профессионалам.

В то время отказы акций были меньше связаны с экономическим рвом FactSet и больше с тем, имеет ли значение ров FactSet, если финансовая система рухнет.

Отказы FactSet в 2025/26 годах — противоположная ситуация. Здесь опасения почти полностью сосредоточены на рве FactSet и пространстве для роста, а также на общих опасениях по поводу того, что ускоряющиеся возможности ИИ подрывают ценовую власть в индустрии программного обеспечения.

При системных отказов вы можете более обоснованно делать ставки на временной арбитраж. История показывает, что рынки tend to recover, и компании с полным рвом могут стать даже сильнее, чем раньше, поэтому, если вы готовы и способны сохранять терпение, пока другие паникуют, вы можете использовать сильный аппетит, чтобы использовать поведенческое преимущество.

Фото Walker Fenton на Unsplash

Однако при специфических отказов рынок говорит вам, что с самим бизнесом что-то не так. В частности, это暗示ет, что конечная стоимость бизнеса становится все более неопределенной.

Следовательно, если вы надеетесь воспользоваться специфическим отказом, вам нужно, помимо поведенческого преимущества, иметь аналитическое преимущество.

Чтобы преуспеть, вам нужно иметь более точное видение того, как компания будет выглядеть через десять лет, чем это в настоящее время подразумевает рыночная цена.

Даже если вы хорошо знаете компанию, это непросто сделать. Акции обычно не падают на 50% относительно рынка без причины. Многие once стабильные держатели — возможно, даже некоторые инвесторы, которых вы уважаете за их глубокие исследования — должны были капитулировать, чтобы это произошло.

Если вы собираетесь вмешаться как покупатель во время специфического отказа, вам нужно иметь ответ, почему эти в остальном информированные и вдумчивые инвесторы ошиблись, продавая, и почему ваше видение是正确的.

Между верой и высокомерием тонкая грань.

Независимо от того, держите ли вы акции, находящиеся в откате, или хотите начать новую позицию в них, важно, чтобы вы понимали, на какой тип ставок вы идете.

Специфические отказы могут соблазнить стоимостных инвесторов начать искать возможности. Прежде чем рискнуть, убедитесь, что вы не используете грубое поведенческое решение для проблемы, требующей тонкого анализа.

Оставайтесь терпеливыми, оставайтесь сосредоточенными.

Тодд