Регулирование DeFi снова в центре внимания, поскольку криптоиндустрия и Уолл-стрит не согласны с предлагаемым «инновационным исключением» для токенизированных активов.

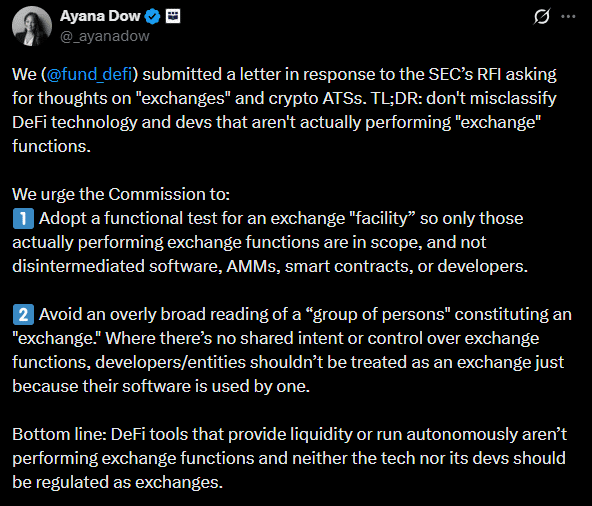

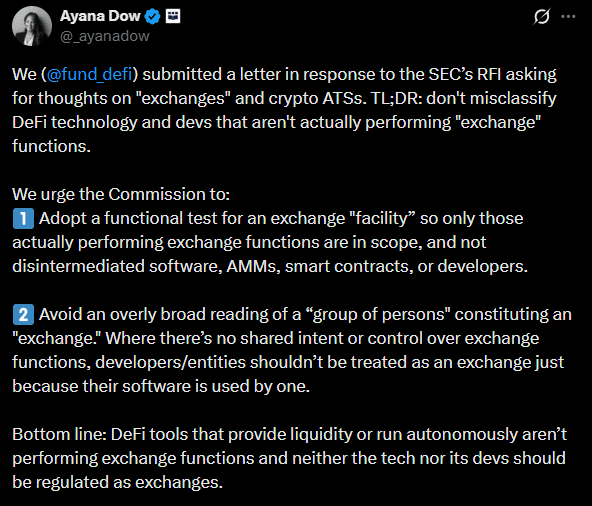

1 апреля группа защиты интересов DeFi, Фонд образования DeFi (DEF), написала в SEC, утверждая, что децентрализованные протоколы не следует «неправильно классифицировать как посредников», как централизованные традиционные биржи.

Аян Доу, юрист DEF, добавил:

Инструменты DeFi, которые обеспечивают ликвидность или работают автономно, не выполняют функций биржи, и ни технология, ни её разработчики не должны регулироваться как биржи.

По мнению группы защиты, любое некастодиальное приложение не подпадает под юридическое определение посредника или биржи. Кроме того, классификация разработчиков как посредников, хотя они не контролируют построенные ими «некастодиальные платформы», возложила бы на них непосильное регуляторное бремя.

Таким образом, группа настаивала, чтобы любая предлагаемая сфера регулирования DeFi исключала дезинтермедированное программное обеспечение, автоматические маркет-мейкеры (AMM), смарт-контракты и неконтролирующих разработчиков.

Уолл-стрит выступает против юридического исключения для DeFi

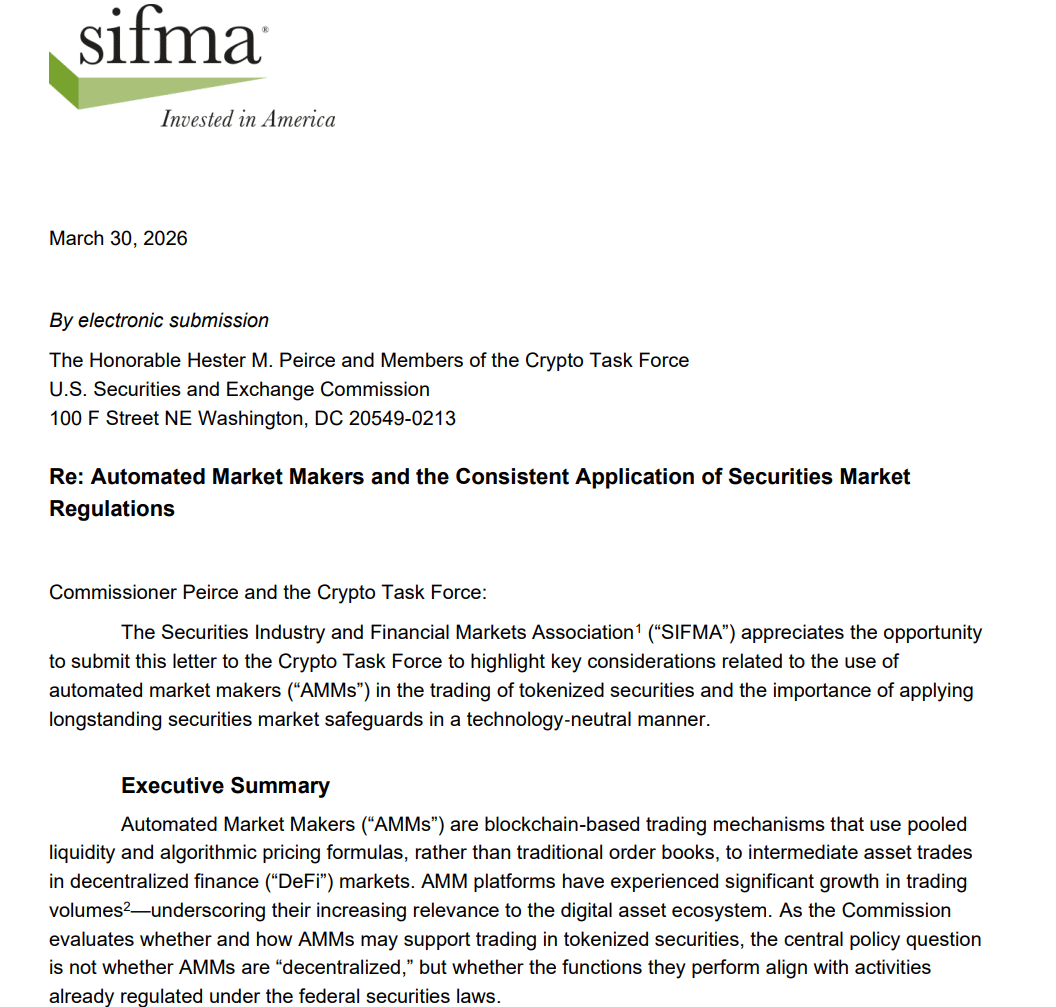

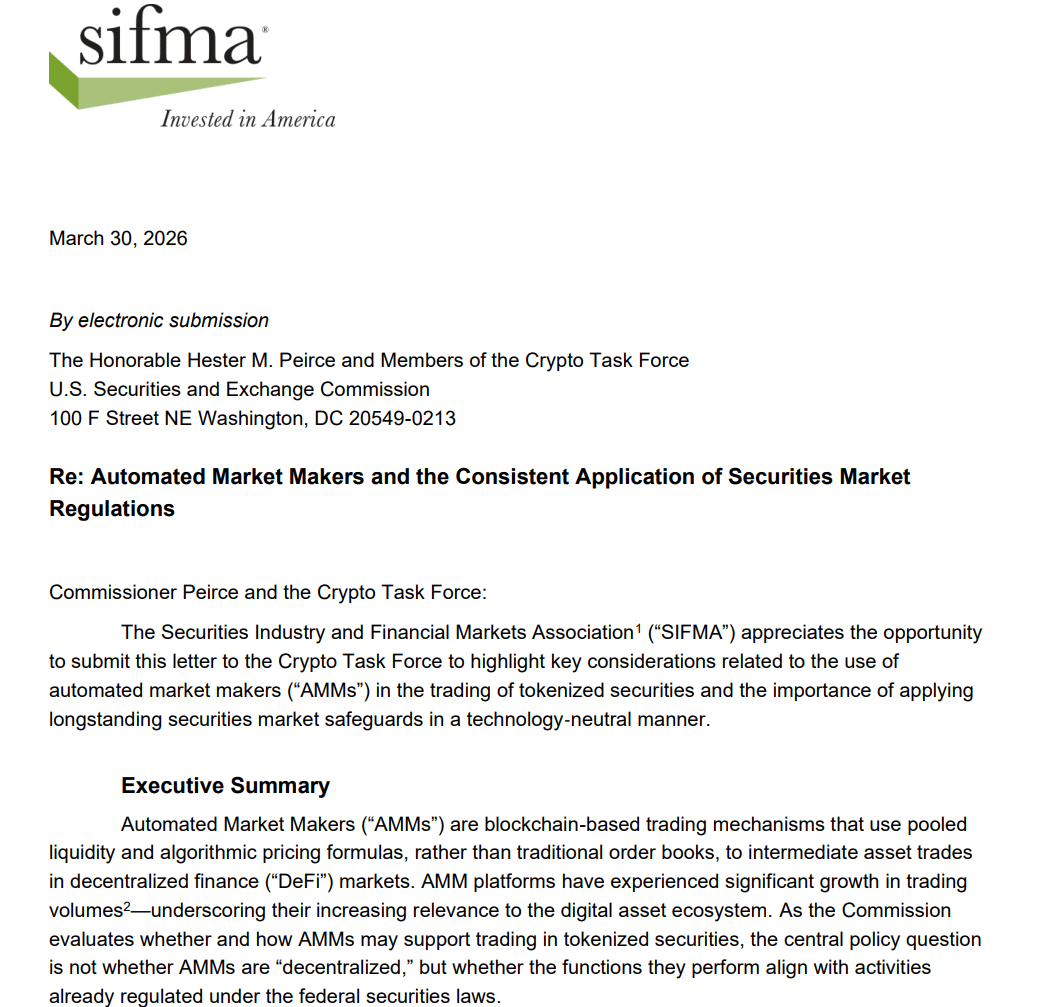

Письмо DEF также было ответом SIFMA (Ассоциации индустрии ценных бумаг и финансовых рынков). Эта группа TradFi недавно заявила, что SEC должна регулировать AMM, ссылаясь на риски для защиты инвесторов.

По мнению SIFMA, SEC должна регулировать AMM и платформы DeFi на основе их функций в поддержке торговли токенизированными ценными бумагами, а не на основе их децентрализованности, как предлагают сторонники DeFi.

SIFMA считает, что Комиссия должна сохранять технологическую нейтральность, регулируя AMM на основе их рыночной функции, а не архитектуры протокола.

Позиция SIFMA перекликается с позицией Citadel Securities. В прошлом году Citadel призвала к строгому регулированию платформ DeFi, которые работают с токенизированными ценными бумагами.

Оппозиция SIFMA и Citadel нерегулируемому DeFi может быть вызвана искренними опасениями, учитывая мошенничества и крахи, наблюдавшиеся в прошлом в этом секторе. Для Уолл-стрит соблюдение правил должно применяться ко всем, кто работает с токенизированными ценными бумагами.

Однако Citadel получает большую часть своего дохода от роли централизованного посредника, особенно для розничных платформ, таких как Robinhood. В результате DEF рассматривает оппозицию Уолл-стрит как мотивированную потенциальным разрушительным воздействием технологии DeFi (устранение посредников) на её деловые интересы.

Остаётся увидеть, как SEC будет решать эти конкурирующие интересы, продолжая поддерживать инновации в предстоящей системе «исключений» для токенизированных ценных бумаг.

Итоговое резюме

- Группа защиты DeFi Education Fund (DEF) выступила против усилий SIFMA по регулированию AMM и других некастодиальных платформ DeFi

- Однако SIFMA утверждает, что большинство «децентрализованных» платформ представляют риски для защиты инвесторов.