Согласно совместному исследованию, на которое ссылаются новостные отчеты, около $110 миллиардов — примерно ₩160 триллионов — покинули южнокорейские криптоплатформы в течение 2025 года. Торговая активность не остановилась. Вместо этого большая часть средств перешла на зарубежные биржи, где обычным инвесторам доступно больше продуктов и инструментов.

Ограничения рынка стимулируют отток

В отчетах сообщается, что внутренние правила в основном ограничивают местные биржи спотовой торговлей. Многие сложные продукты остаются недоступными для розничных трейдеров в Корее, поэтому трейдеры обратились к зарубежным платформам, таким как Binance и Bybit. Совместное исследование CoinGecko и Tiger Research указывается как основная основа для цифры в $110 миллиардов.

Банковские услуги и правила формируют выбор

Согласно совместному отчету CoinGecko и Tiger Research, южнокорейские инвесторы перевели более KRW 160 триллионов (~$110 миллиардов) в криптоактивах с внутренних бирж на зарубежные платформы в 2025 году из-за местных регуляторных ограничений, которые разрешают CEX в основном только спотовую торговлю. Корейские... pic.twitter.com/KrYgFurdsm

— Wu Blockchain (@WuBlockchain) 2 января 2026 г.

В последние годы Южная Корея ужесточила соответствие требованиям и защиту пользователей. Были приняты законы, предназначенные для защиты клиентов, такие как Закон о защите пользователей виртуальных активов в 2024 году, но компании и пользователи заявляют, что эти законы не создали полной основы для более широких рыночных услуг.

Законодатели обсуждали Базовый закон о цифровых активах, но задержки оставили пробелы, которые некоторые трейдеры сочли ограничивающими. В результате растущая доля корейской криптовалюты мигрировала в кошельки и платформы за рубежом.

Влияние комиссий и поведение пользователей

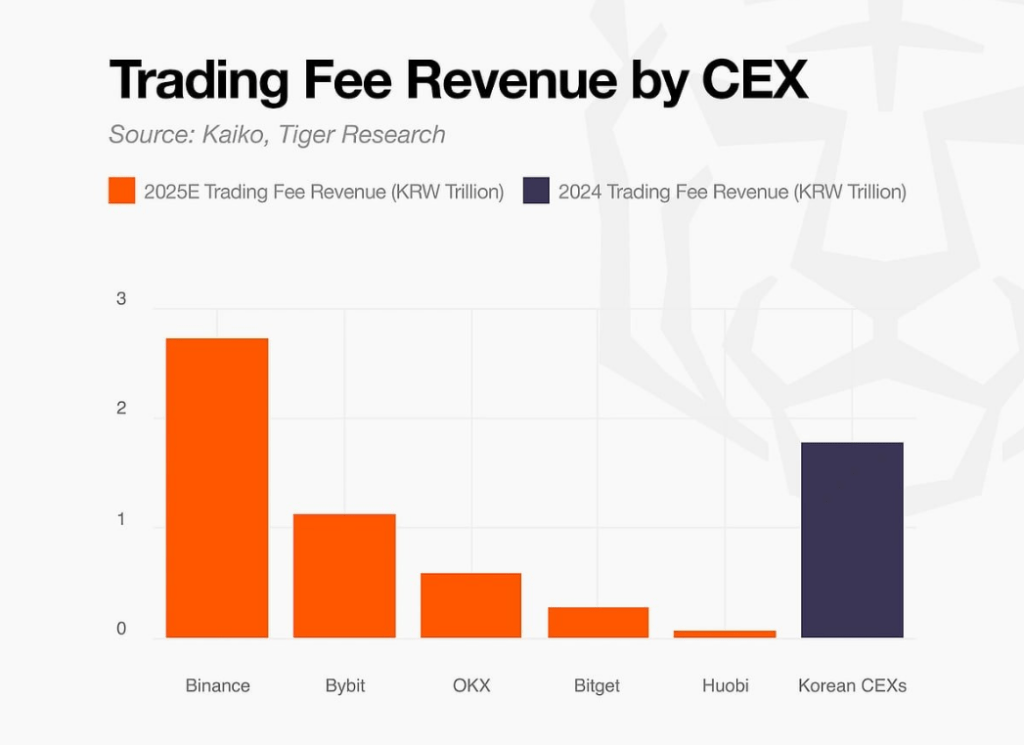

На основе анализа платформ, доходы от комиссий с корейских пользователей на зарубежных биржах стали значительными. Отраслевые оценки оценивают комиссии на основе пользователей примерно в ₩2,73 триллиона для Binance и примерно ₩1,12 триллиона для Bybit в 2025 году.

В отчетах также указывалось, что количество корейских счетов с крупными зарубежными балансами выросло более чем в два раза в годовом исчислении. Некоторая часть капитала также была переведена в кошельки для самостоятельного хранения (self-custody), что показывает, что пользователи распределяют средства между биржами и приватными кошельками.

Власти указывают на риски, когда деньги пересекают границы. Регуляторы сосредоточились на проверках по противодействию отмыванию денег и банковском партнерстве для криптокомпаний. Трейдеры, с другой стороны, подчеркивают доступ. Они хотят маржинальную торговлю, деривативы и другие услуги, которые они не могут получить дома. Это противоречие между доступом и надзором является центральным в движении средств.

Спрос на торговлю остается высоким

Тенденции объемов позволяют предположить, что интерес корейцев не ослаб, а сменил локацию. Внутренние платформы обрабатывали значительный объем спотовой торговли, но общий спрос, по-видимому, перетек на зарубежные площадки, а не исчез. Цифра в $110 миллиардов отслеживает переводы и размещения, а не потери активов. Другими словами, стоимость была перемещена, а не стерта.

Сообщается, что законодатели в Сеуле работают над более широкими правилами, включая положения о стейблкоинах, за которые многие участники индустрии выступали. Если появятся новые законы и рынки вновь откроются для более широкого спектра услуг, некоторые средства могут вернуться. Но пока многие пользователи продолжают торговать за пределами Кореи, чтобы получить доступ к более широкому выбору инструментов и возможностей.

Featured image from Unsplash, chart from TradingView