Геополитические события последних месяцев создали для инвесторов ситуацию постоянной неопределённости, что затрудняет открытие краткосрочных позиций с уверенностью. Макроэкономические факторы теперь преобладают над криптовалютными драйверами в формировании краткосрочной динамики цен.

Подготовленный в сотрудничестве с Coinbase Institutional, последний отчет Charting Crypto обобщает ключевые рыночные и ончейн-тенденции, влияющие на институциональную криптовалютную стратегию в этом квартале. От настроений инвесторов и ликвидности стейблкоинов до сигналов накопления биткойна и меняющейся рыночной структуры Ethereum — в отчете представлен основанный на данных взгляд на рынок, ожидающий более ясного направления.

Некоторые из многочисленных ключевых моментов этого выпуска:

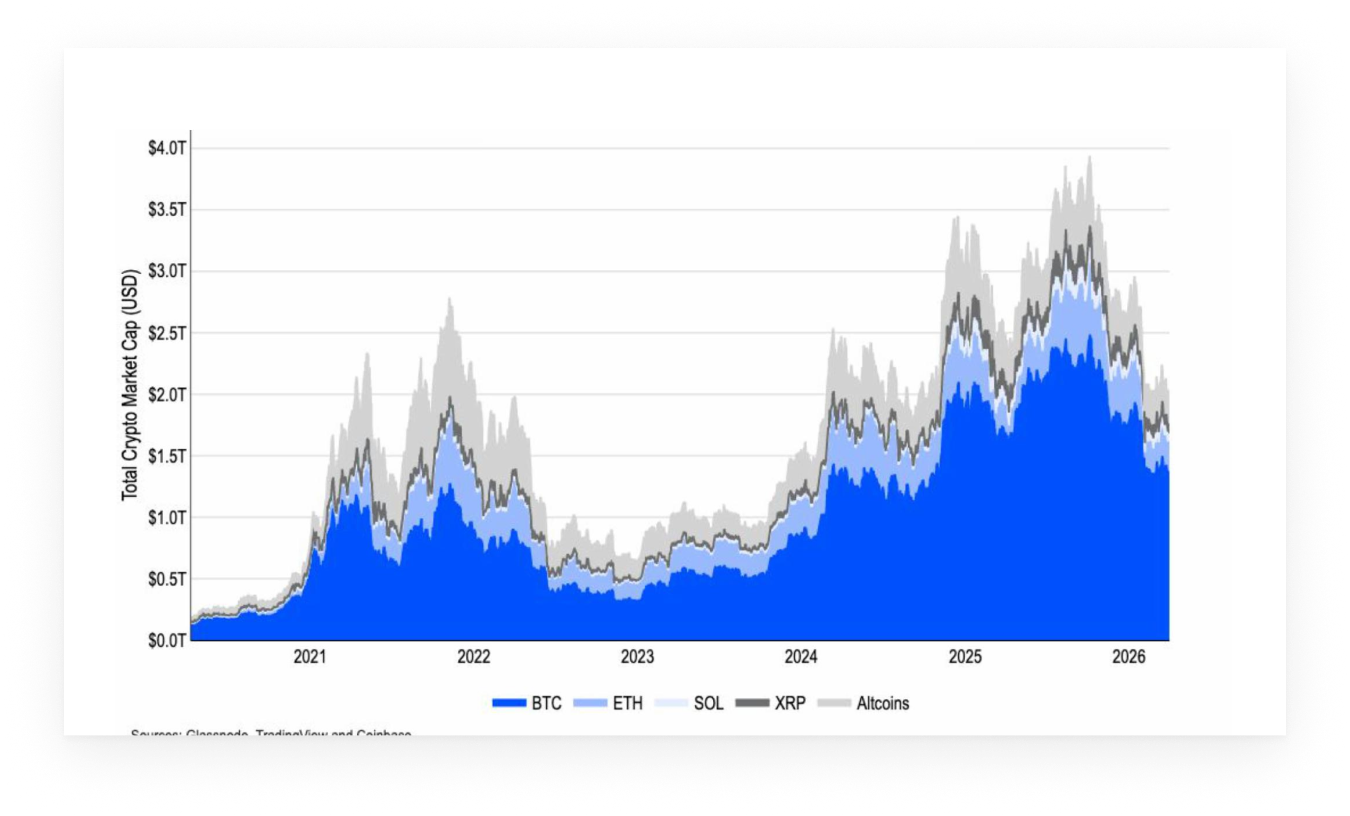

- Ликвидность перетекает в стейблкоины, а не покидает этот класс активов, так как общая рыночная капитализация криптовалют (без учета стейблкоинов) упала примерно на ~18% в I квартале, в то время как предложение стейблкоинов увеличилось с $308 млрд до $318 млрд.

- Аналогии с прошлыми циклами становятся менее полезными для определения моментов разворота рынка, поскольку циклы как биткойна, так и Ethereum продолжают отклоняться от исторических моделей.

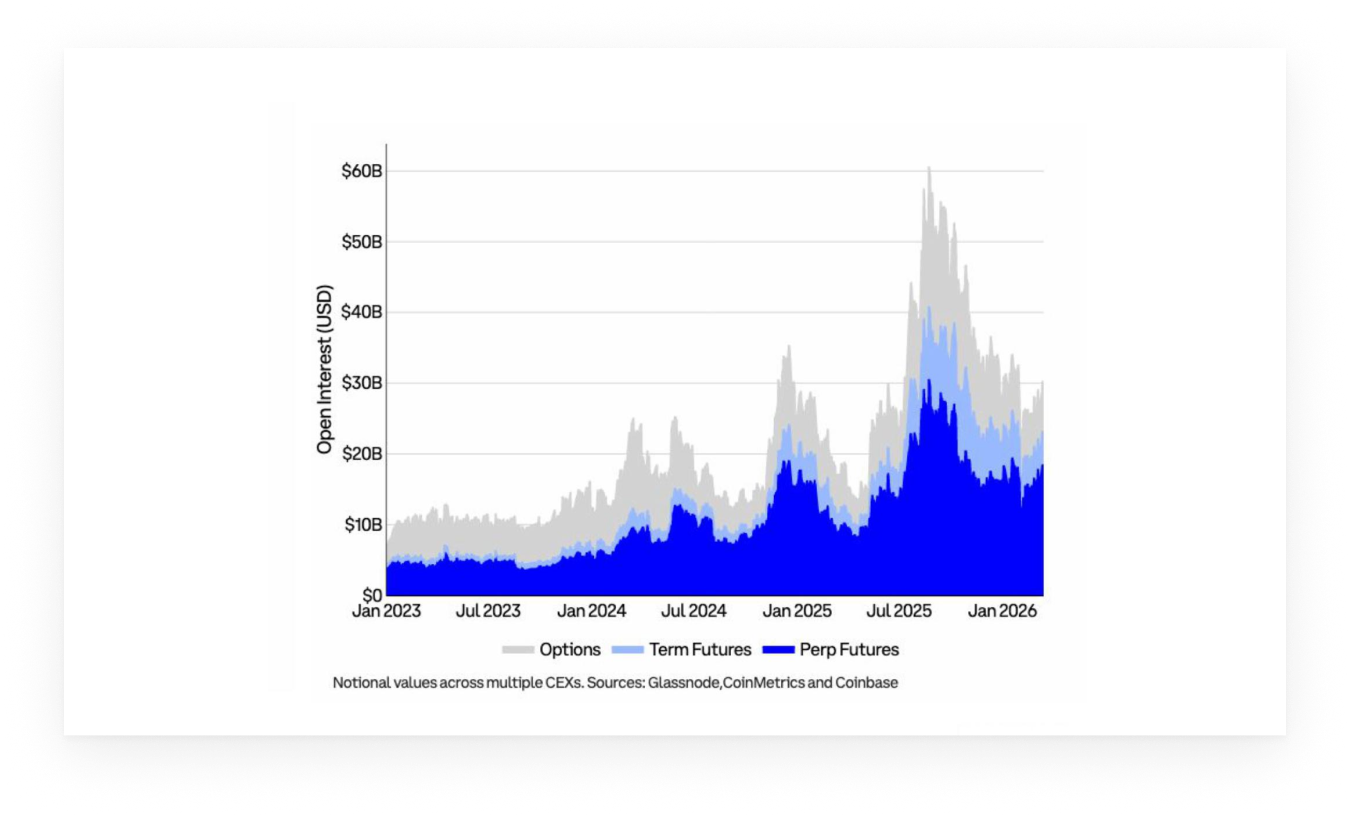

- Рыночная структура показывает признаки нормализации: открытый интерес по деривативам BTC восстанавливается (особенно по перпетуальным свопам), что указывает на восстановление аппетита к риску на рынках с левериджем.

- 82% опрошенных институциональных инвесторов сейчас относят рынок к медвежьей фазе или к поздней медвежьей фазе (по сравнению с 31% в декабре).

- Экосистема Ethereum становится более дифференцированной: капитал концентрируется в кейсах использования базового уровня по мере ослабления общей активности, что подчеркивает смещение в сторону утилитарного спроса по сравнению со спекулятивными потоками.

Ликвидность остается в системе

Несмотря на общее движение в сторону снижения риска (risk-off) в I квартале, динамика ликвидности раскрывает более тонкую картину. Общая рыночная капитализация криптовалют (без учета стейблкоинов) снизилась примерно на 18%, однако предложение стейблкоинов за тот же период увеличилось.

Это расхождение говорит о том, что капитал не полностью покидает криптовалютные рынки, а скорее перераспределяется в инструменты, подобные кэшу, в ожидании более четких сигналов. По сути, инвесторы снижают риски, не отказываясь от участия, сохраняя возможность вернуться на рынок.

Биткойн: сброс настроений, предложение сокращается

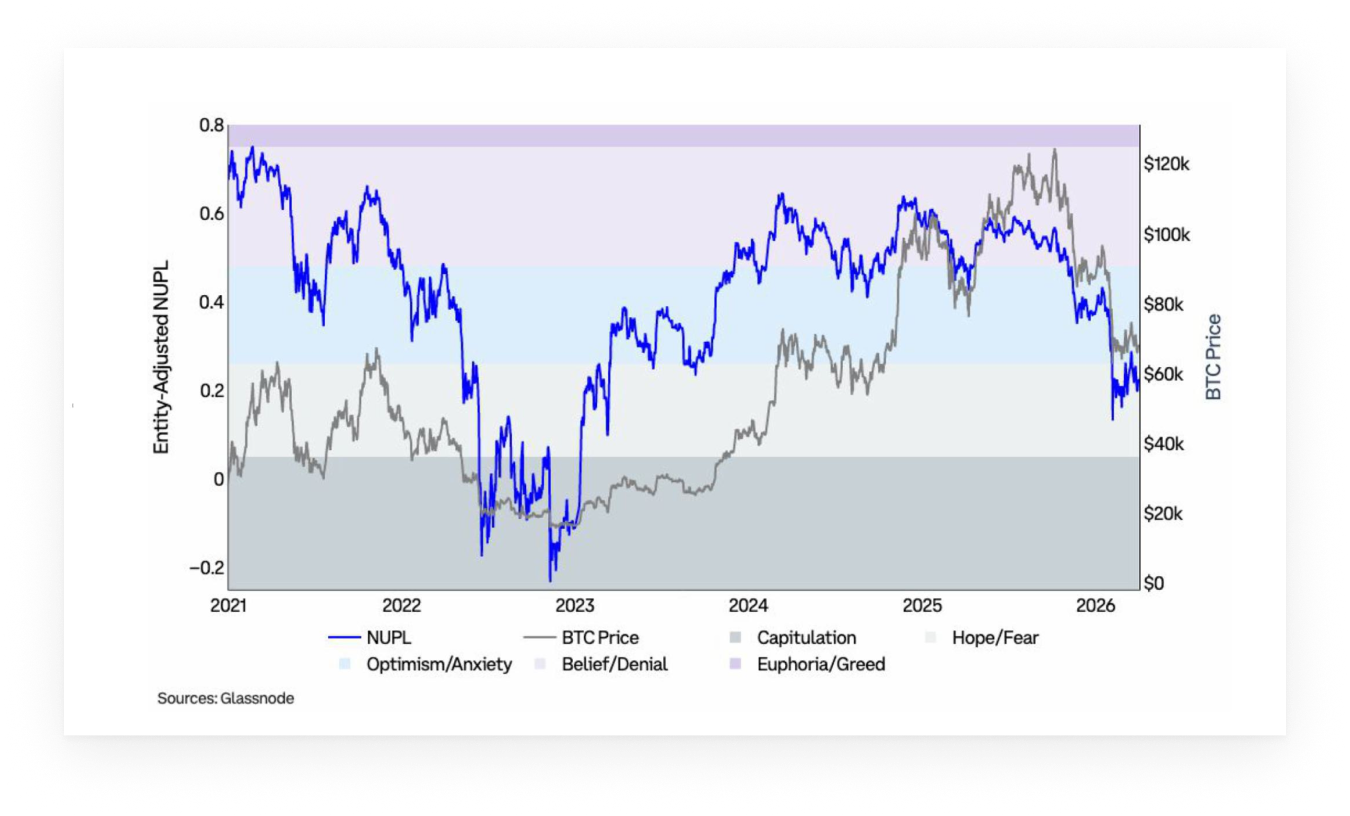

Просадка биткойна в феврале отразилась в ухудшении настроений инвесторов: показатель Net Unrealized Profit/Loss (NUPL) переместился из зоны Тревоги в зону Страха до конца I квартала. Хотя в апреле настроения начали показывать ранние признаки улучшения, они по-прежнему тесно связаны с внешними событиями, что говорит о хрупкости уверенности.

В то же время ончейн-динамика предложения указывает на переход монет от более реактивных участников. Сокращение недавно активного предложения наряду с умеренным увеличением долгосрочно удерживаемых монет подразумевает, что краткосрочный, спекулятивный капитал сократился.

Ethereum: концентрация капитала на базовом уровне

Данные по Ethereum указывают на расхождение между активностью и распределением капитала. Краткосрочное участие снижалось на протяжении всего первого квартала, о чём свидетельствует резкое падение недавно активного предложения и продолжительный период подавленных настроений. Однако потоки капитала оставались сконцентрированными на базовом уровне.

Предложение стейблкоинов в сети Ethereum продолжает расти с положительной динамикой, а токенизированные реальные активы достигли новых максимумов, что указывает на устойчивый спрос на случаи использования для расчетов и залога. В то же время ETH с конца 2025 года опережает по доходности основные токены L2, что говорит о том, что капитал консолидируется на базовом уровне, а не перетекает дальше по кривой риска.

Чтобы помочь вам ориентироваться в нынешней сложной криптовалютной среде, ознакомьтесь с полным анализом и данными в отчете Glassnode x Coinbase: скачайте отчет здесь.