Статья переведена: Block unicorn

Компания заработала миллиарды долларов процентного дохода, держа казначейские резервы в качестве обеспечения для своего стейблкоина, и платила другим платформам за распространение и расчеты USDC по всей платежной экосистеме. Circle зарабатывает примерно 40 центов на каждый 1 доллар, который платит партнерам USDC. Пока маржа прибыли была достаточной, она могла себе это позволить. Но с наступлением эпохи низких процентных ставок этот эмитент USDC потерял слишком большую часть прибыли. В течение большей части своей истории у Circle был только один продукт: USDC.

В недавно опубликованном отчете за первый квартал 2026 года эмитент USDC объявил о нескольких инициативах, направленных на захват большей ценности в рамках своей операционной деятельности. Среди них: предпродажа собственного токена Layer-1 ARC на 222 миллиона долларов с полностью разводненной оценкой в 3 миллиарда долларов; запуск инфраструктуры для AI-агентов; и расширение своей платежной сети Circle, позволяющее банкам осуществлять платежи в стейблкоинах, обходя волатильность цифровых активов. Достижения Circle за последние несколько кварталов изменят эту ситуацию.

В совокупности эти шаги знаменуют попытку Circle трансформироваться из компании, работающей на одном уровне, в полноценную финансовую платформу, способную работать и извлекать ценность на нескольких уровнях платежного стека.

Сегодня я оценю, сможет ли Circle использовать вертикальную интеграцию для компенсации сокращения доходов от процентного бизнеса, которое продолжается с каждым снижением ставки ФРС.

Исчезающий поплавок

В первом квартале 2026 года общий доход Circle составил 694 миллиона долларов, что на 20% больше, чем годом ранее. Этот рост полностью объясняется увеличением объема стейблкоинов в обращении, сам по себе USDC не претерпел изменений. Объем стейблкоинов в обращении вырос с 235 миллиардов долларов в марте 2025 года до 315 миллиардов долларов в марте 2026 года, что более чем на 30%. За тот же период доля рынка USDC снизилась на 62 базисных пункта.

Но Circle сталкивается с более серьезной проблемой. Наступила эпоха низких процентных ставок, ставка ФРС снизилась с 4,5% год назад до нынешних 3,75%.

Несмотря на то, что средний объем обращения USDC в первом квартале 2026 года вырос на 39% в годовом исчислении, доход Circle от резервов вырос всего на 17% в годовом исчислении, до 653 миллионов долларов. Это произошло потому, что средняя ставка по резервам упала на 66 базисных пунктов в годовом исчислении — с 4,16% в первом квартале 2025 года до 3,50% в первом квартале 2026 года, что в значительной степени нивелировало указанный рост.

Это не разовое явление. В течение последних четырех кварталов разрыв между темпом роста дохода от резервов Circle и темпом роста предложения USDC продолжал сокращаться.

Основной источник дохода Circle не рос пропорционально объему стейблкоинов в обращении.

Компания также сталкивается с утечкой ценности.

Пробуждение за 60 центов

Это означает, что стоимость удержания и распространения USDC на платформах составляет более 60 центов за каждый доллар. Из 405 миллионов долларов USDC Circle выплатила Coinbase 330 миллионов долларов (около 80%) в качестве затрат на распространение только в первом квартале 2026 года. Из дохода от резервов в 653 миллиона долларов в этом квартале Circle выплатила партнерам 405 миллионов долларов в качестве затрат на распространение и транзакции.

В отрасли, где постоянно появляются новые игроки, расширяющиеся и интегрирующиеся на всех уровнях технологического стека, это просто огромная потеря денег.

В данный момент все указывает на то, что Circle должна посмотреть правде в глаза. Падение процентных ставок продолжает снижать ее доходы от резервов; высокие затраты на дистрибуцию продолжают вызывать утечку ценности; а основной бизнес Circle по-прежнему является прокси для доходности, стоимость которого сокращается с каждым снижением ставки ФРС. При президенте США Дональде Трампе ожидания мягкой позиции ФРС только усиливаются.

Что Circle делает в ответ? Ответ: захватить больше ценности по всей своей бизнес-цепочке за счет вертикальной интеграции и снизить зависимость от процентного дохода.

Чтобы понять, что строит Circle, подумайте о том, что у нее есть сейчас.

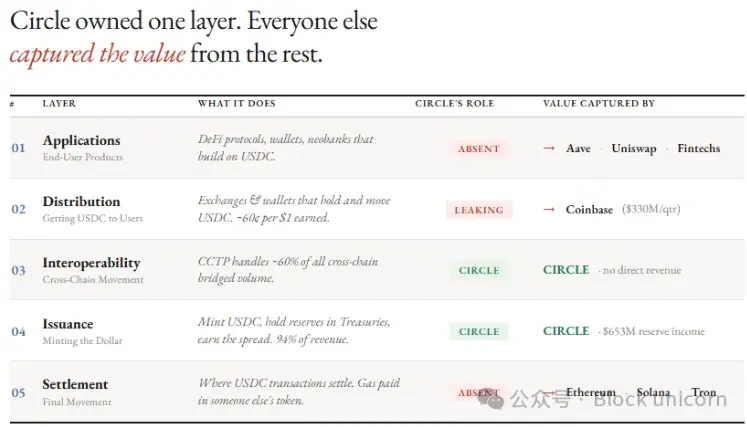

Эмитент USDC начинал с самого нижнего уровня стека стейблкоинов — уровня эмиссии — и годами наблюдал, как другие захватывают ценность на каждом уровне над ним.

На уровне эмиссии Circle выпускает USDC и EURC, держит резервы в казначейских облигациях США через резервный фонд Circl от BlackRock, управляет паритетом 1:1 и обрабатывает выпуск и погашение через Circle Mint. 94% ее общего дохода приходится на доход от резервов в государственных облигациях.

Затем Circle расширила свою деятельность до уровня взаимодействия через свой Протокол межсетевой передачи (CCTP), который перемещает USDC между блокчейнами и обрабатывает около 60% объема мостовых транзакций. Хотя этот механизм отвечает за маршрутизацию USDC между цепочками, сам CCTP работает на цепочках, принадлежащих другим. Следовательно, Circle не может получать от этого существенный прямой доход.

Все остальные уровни стека принадлежат другим.

Система расчетов работает на Ethereum, Solana и Tron. Каждая транзакция USDC оплачивает комиссию за газ в других токенах (ETH, SOL, TRX), и Circle не имеет никакого контроля над перегрузкой, комиссиями или управлением в этих сетях.

Каналы распространения в значительной степени зависят от Coinbase, бирж и кошельков. Circle должна платить долю от дохода, программу стимулирования и затраты на интеграцию, чтобы доставить USDC конечным пользователям.

Сторонние организации, такие как децентрализованные финансовые (DeFi) протоколы, финтех-компании, необанки и прогнозные рынки, создают приложения и продукты, использующие USDC. Это означает, что конечным клиентам, будь то розничные или институциональные, не нужно напрямую взаимодействовать с Circle.

Такая структура приводит к тому, что Circle зарабатывает всего 40 центов на каждый доллар дохода.

Захват контроля над стеком

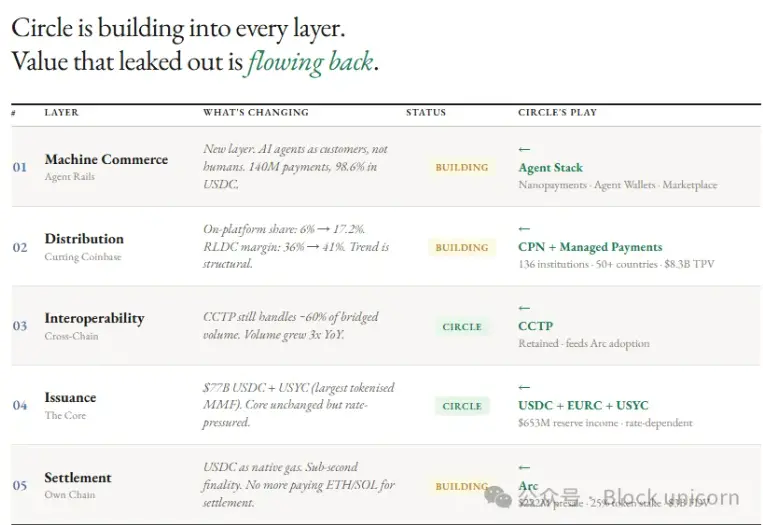

11 мая Circle объявила о трех планах инвестиций, направленных на вертикальную интеграцию различных уровней бизнеса, которыми она ранее не владела.

Во-первых, расчеты. Circle владеет собственным блокчейном Layer-1 Arc, предназначенным для захвата комиссий, которые в настоящее время генерируются переводом USDC в блокчейнах, таких как Ethereum, Solana и Tron.

Совместимый с EVM Arc обеспечивает финализацию в течение долей секунды и использует USDC в качестве собственного токена для оплаты комиссии за газ, при этом плата за транзакцию составляет около 0,001 доллара США. Чтобы сделать свою цепочку более привлекательной для институциональных пользователей, Circle предлагает настраиваемые параметры конфиденциальности и архитектуру, устойчивую к квантовым атакам. В то время как публичные блокчейны общего назначения, такие как Ethereum и Solana, полностью прозрачны и не могут обеспечить конфиденциальность для деликатных транзакций, таких как институциональные платежи.

Circle привлекла 222 миллиона долларов в ходе предпродажи токена ARC с оценкой в 3 миллиарда долларов. Этот раунд возглавили лидеры раунда финансирования на 75 миллионов долларов от a16z, другие инвесторы включают BlackRock, Apollo Global Management, Intercontinental Exchange (материнская компания NYSE), Standard Chartered, ARK Invest, SBI Group, IDG Capital, Bullish и Haun Ventures.

Во-вторых, распространение. Платежная сеть Circle (CPN) помогает эмитенту USDC снизить зависимость от Coinbase.

CPN подключает финансовые учреждения непосредственно к сети Circle, позволяя выпускать, погашать и маршрутизировать USDC без необходимости проходить через биржи. Сеть насчитывает 136 зарегистрированных учреждений (рост на 36% кв/кв), годовой объем транзакций составляет 8,3 миллиарда долларов (рост на 17% кв/кв) и обеспечивает платежи в фиате в более чем 50 странах.

В результате доля USDC, основанная на собственной инфраструктуре Circle, выросла почти втрое — с примерно 6% год назад до 17,2%. Даже несмотря на снижение доходности резервов, маржа RLDC (доходы за вычетом затрат на дистрибуцию и транзакции в процентах от доходов) стабилизировалась и выросла с 38% во втором квартале 2025 года до 41% в первом квартале 2026 года.

Circle еще не монетизировала CPN, отдавая приоритет росту пользователей, а не сбору платы. Но как только она будет монетизирована, каждый дополнительный доллар использования CPN принесет Circle доход, основанный на использовании, не зависящий от процентных ставок.

Circle создала полноценную экономику агентов с помощью таких продуктов, как Agent Wallets, Nanopayments (поддержка переводов USDC без газа на сумму до 0,000001 доллара США [одна миллионная]), Agent Marketplace (где агенты могут находить и оплачивать услуги) и Circle CLI (ускоряет регистрацию агентов и настройку кошельков).

Третий уровень — это уровень приложений. Через этот третий уровень Circle взимает небольшую плату за крупные транзакции, выполняемые ИИ-агентами, тем самым постоянно захватывая ценность по всей экономике агентов.

Насколько велика рыночная возможность для платежей агентами? В прошлом месяце глава отдела маркетинга Circle Питер Шредер сообщил, что USDC составил 98,6% из 140 миллионов транзакций, выполненных ИИ-агентами за девять месяцев.

Гонка за стеком

Расширение Circle в платежный стек — непростая задача. Платежный гигант Stripe начал с вершины, а затем углубился благодаря серии сделок и запусков продуктов. Приобретение Bridge позволило Stripe контролировать уровни авторизации, кастодиального обслуживания, иностранной валюты и выпуска карт. Запуск Tempo позволил Stripe выйти на уровень расчетов. Сегодня Stripe контролирует все семь платежных уровней, обслуживая 5 миллионов торговцев.

Tether использует Plasma, инкубированную эмитентом USDT, в качестве своей расчетной цепочки. Однако регулирование Tether все еще менее строгое, чем у USDC.

Stripe доминирует в области транзакций между людьми, а Tether лидирует в сделках с долларами США на развивающихся рынках и в криптовалютных транзакциях. Таким образом, Circle позиционирует себя в области институциональных расчетов и транзакций между машинами, где репутация в области регулирования и программируемая инфраструктура могут быть важнее интеграции оформления заказа, доминируемой Stripe.

Ответный удар CRCL

Хотя Circle привлекла 222 миллиона долларов за счет предпродажи токена ARC институциональным инвесторам, начальное финансирование разработки ARC фактически поступило от акционеров CRCL. Ирония заключается в том, что самое большое сопротивление, с которым может столкнуться Circle, возможно, заключается в том, как справиться с внутренним сопротивлением.

Что значит рост стоимости токена Arc для публичной компании? Я указывал на эту проблему еще в ноябре прошлого года.

«Природа собственного токена вызовет некоторые разногласия на публичных рынках. Почему рынок будет признавать или ценить собственный токен, который захватывает ценность, создаваемую Arc и CPN, а не позволит этой ценности вернуться в отчет о прибылях и убытках Circle? Почему излишки Circle должны использоваться для финансирования центра затрат, который, как ожидается, не будет возвращать прибыль акционерам? Существующие акционеры этого никогда не потерпят. Инвесторы публичного рынка покупают CRCL из-за его доходов от резервов. Маловероятно, что они будут сидеть сложа руки и наблюдать, как новый актив поглощает прирост стоимости инфраструктуры, в которую они инвестировали».

Как Circle решит эту проблему? Имеет ли смысл отдельный листинг Arc? Ответ мы узнаем только в первом квартале после запуска основной сети Arc.

На данный момент долгосрочная цель Circle — захватить как можно больше ценности, постоянно расширяя свое присутствие на этих уровнях. Каждый раз, когда USDC рассчитывается на Arc, Circle получает комиссию за расчеты. Когда учреждения совершают транзакции через CPN, Circle будет сохранять прибыль от дистрибуции. И, наконец, когда агенты совершают транзакции через Nanopayments на Arc, Circle также надеется взимать плату на этом уровне.