Основатель Cardano Чарльз Хоскинсон призывает криптоиндустрию более внимательно изучить законопроект H.R. 3633, утверждая, что этот закон о структуре рынка может заблокировать будущие американские токен-проекты в статусе ценных бумаг, вместо того чтобы обеспечить нормативную ясность, которую обещают его сторонники. Его критика выходит за рамки процесса: Хоскинсон заявляет, что данный законопроект, в его нынешнем виде, может защитить устоявшиеся сети, одновременно значительно усложнив запуск и рост новых криптопроектов внутри Соединенных Штатов.

Основатель Cardano выносит суровое предупреждение

В видео, опубликованном 2 марта, основатель Cardano частично представил спор как прямой ответ на точку зрения генерального директора Ripple Брэда Гарлингхауса о том, что неидеальный законопроект все же лучше, чем его полное отсутствие. Хоскинсон с этим категорически не согласился. «Плохой законопроект не лучше, чем его отсутствие», — заявил он. «Вы начинаете с принципиального подхода. Вы не делаете все ценной бумагой по умолчанию и модернизируете законы о ценных бумагах, чтобы это было не так плохо».

Его основное возражение заключается в том, что «Закон о ясности» будет рассматривать вновь выпущенные цифровые активы прежде всего как ценные бумаги, а затем потребует от них убедить SEC, что они имеют право «перейти» в статус товара после того, как их сети станут достаточно децентрализованными. По мнению Хоскинсона, эта framework-структура охватила бы XRP, Cardano и Ethereum на момент их запуска. Разница, по его словам, в том, что старые сети в конечном итоге могут быть «дедушкины» (оставлены в прежнем статусе), в то время как будущие проекты с первого дня столкнутся с нормативным лабиринтом.

Хоскинсон неоднократно возвращался к одному и тому же вопросу: что на практике мешает SEC indefinitely сохранять токен в качестве ценной бумаги? «Если он начинается как ценная бумага, что мешает им сохранять его в качестве ценной бумаги вечно? — спросил он. — И действительно ли мы уверены, что можем доверять этому нормотворчеству, которое еще не произошло, людям, которые еще не назначены агентствами, которые потратили последние четыре [бранное слово] года на то, чтобы судиться со всеми и сажать всех в тюрьму?»

Далее он изложил серию так называемых «векторов атаки», которые враждебно настроенная SEC могла бы использовать в нормотворчестве. Один из них касался процедурных задержек, связанных с полнотой подачи документов, когда агентство могло постоянно сбрасывать счетчик с помощью уведомлений о недостатках. Другой был сосредоточен на неопределенном толковании в законопроекте понятия «общий контроль», которое, по его словам, могло позволить регуляторам интерпретировать саму координацию в open-source как доказательство централизованного управления.

Он также утверждал, что доказать децентрализацию может стать невозможно, если от эмитентов потребуют идентифицировать бенефициарных владельцев в псевдонимных wallet-системах или полагаться на категории соответствия, которые SEC еще даже не создала.

Главная мысль заключалась в том, что законопроект может выглядеть работоспособным по букве закона, но стать карательным на практике. «Плохой законопроект закрепляет в законе все то, что Гэри Генслер пытался сделать с индустрией», — заявил Хоскинсон. «Плохой законопроект посредством нормотворчества позволяет SEC произвольно и своевольно убивать каждый новый проект в Соединенных Штатах. Плохой законопроект подвергает всех разработчиков DeFi персональной ответственности».

Он также заявил, что нынешняя политическая борьба в Вашингтоне на самом деле вообще не касается структуры законопроекта. По словам Хоскинсона, реальная загвоздка — это доходность стейблкоинов (stablecoin yield), а не защита разработчиков, охват DeFi или разделение полномочий между SEC и CFTC. По его словам, это ставит отрасль в странное положение: законопроект, рекламируемый как реформа структуры рынка, но тот, который «не затрагивает суть того, что происходит в отрасли прямо сейчас».

Предпочтительной альтернативой для Хоскинсона является переработка на основе принципов, которая модернизирует само законодательство о ценных бумагах, создает blockchain-native системы раскрытия информации, явно защищает разработчиков и DeFi и ограничивает объем дискреционных полномочий, которые регуляторы могут использовать в последующем нормотворчестве. В противном случае, предупредил он, практическим результатом может стать простое: устоявшиеся сети выживут, в то время как следующее поколение американских криптопроектов сначала будет строиться за рубежом и попытается выйти на американский рынок только спустя годы.

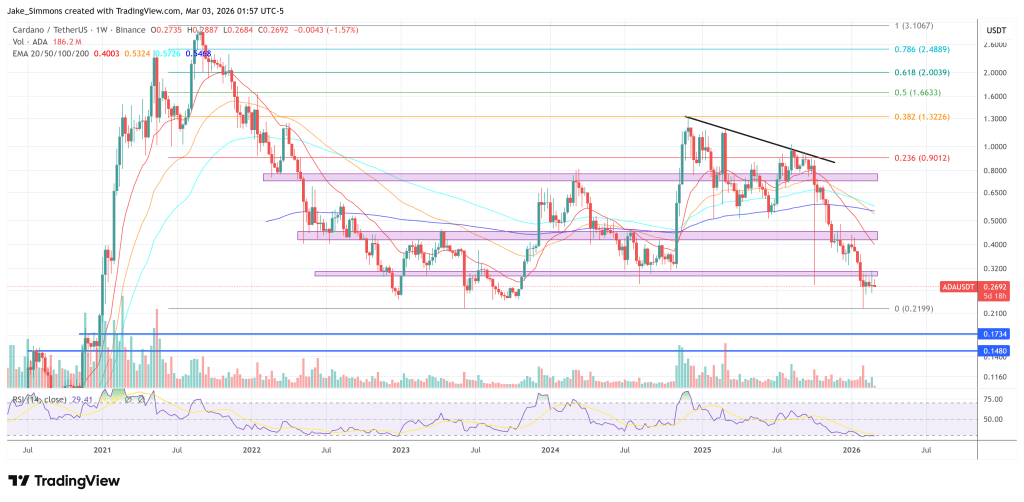

На момент публикации Cardano торговался на уровне $0.2692.