Генеральный директор BlackRock, управляющий активами на 14 триллионов долларов, Ларри Финк опубликовал годовое письмо акционерам за 2026 год 23 марта. В письме он предупредил, что ИИ создает «K-образный исход», когда ведущие компании ускоряются и оставляют позади всех остальных. Он написал: «Когда рыночная капитализация растет, а владение остается узким, процветание может казаться все более недостижимым».

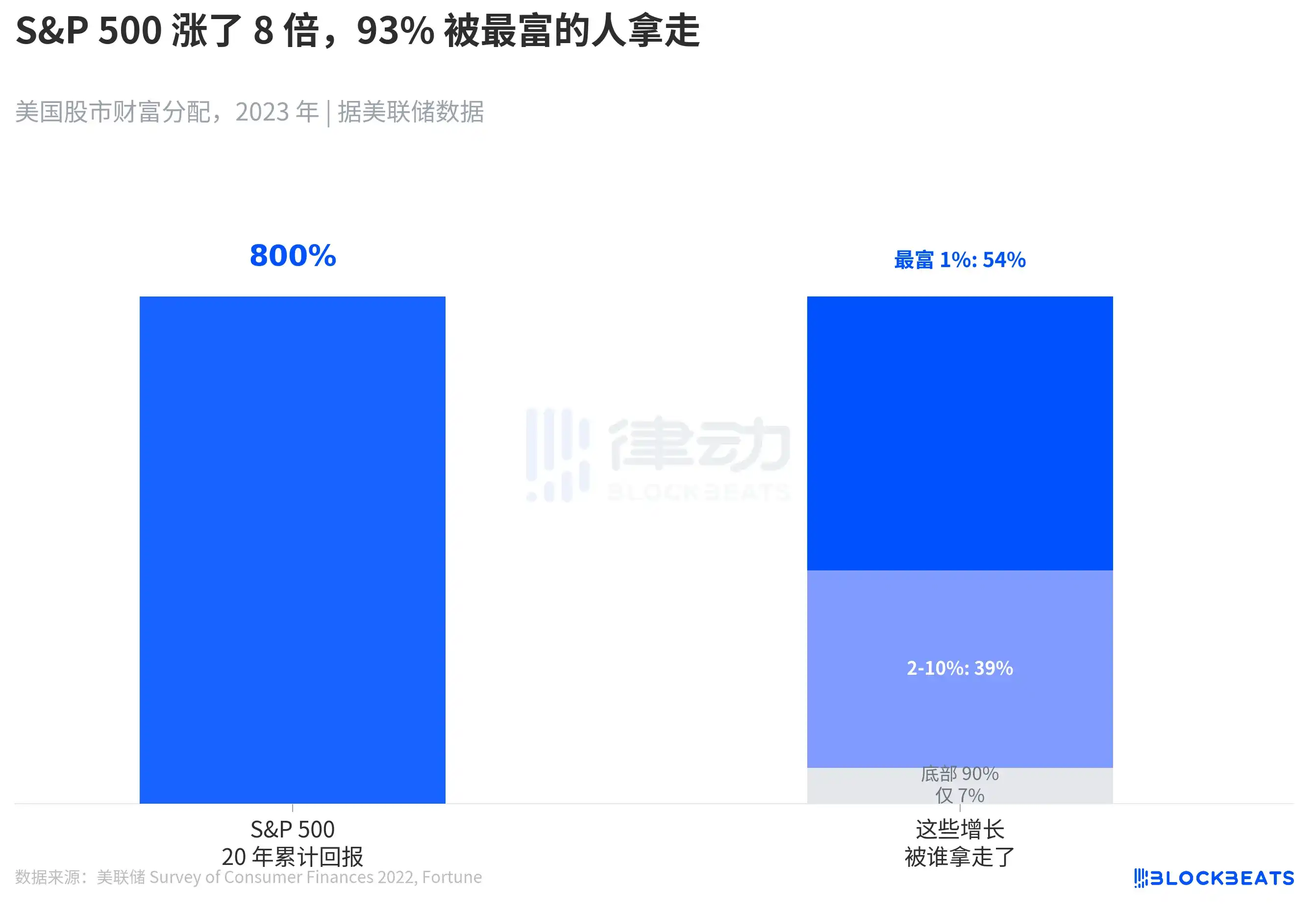

Это не пустые слова. За последние 20 лет индекс S&P 500 вырос в 8 раз. Но, по данным исследования финансов потребителей (SCF) ФРС за 2022 год, распределение этого восьмикратного роста крайне концентрировано.

Самые богатые 1% семей в США получили 54% всего богатства фондового рынка, 20 лет назад этот показатель составлял 40%. Следующие 2-10% получили 39%. Нижние 90% американцев в совокупности владеют лишь 7% акций, а нижние 50% — только 1%. По данным Gallup, уровень владения акциями в семьях с доходом более 100 тысяч долларов составляет 87%, а в семьях с доходом менее 50 тысяч — лишь 28%.

Финк в письме использовал точную метафору. «С 1989 года доллар, вложенный в американский фондовый рынок, вырос более чем в 15 раз по сравнению с долларом, привязанным к медианной заработной плате». Другими словами, разрыв между теми, у кого есть деньги для инвестиций, и теми, кто живет только на зарплату, за 35 лет увеличился в 15 раз. Он опасается, что ИИ «повторит эту модель в еще большем масштабе, концентрируя богатство в руках компаний и инвесторов, которые способны его захватить».

С этим диагнозом проблем нет. А вот следующее предложенное лечение — это та часть письма, которая действительно заслуживает анализа.

Финк ссылается на двухпартийное предложение сенаторов Билла Кэссиди и Тима Кейна. Его содержание заключается в том, чтобы федеральное правительство заняло 1,5 триллиона долларов в течение 5 лет и влило их в инвестиционный фонд, независимый от существующей системы социального обеспечения, для покупки акций, частных активов и других инвестиций, заблокировав их на 75 лет, и использовало долгосрочную доходность для填补нения пробелов в соцобеспечении. Ожидается, что трастовый фонд социального обеспечения США иссякнет к 2033 году, и в этом случае бенефициары получат только 83% от обещанных benefits.

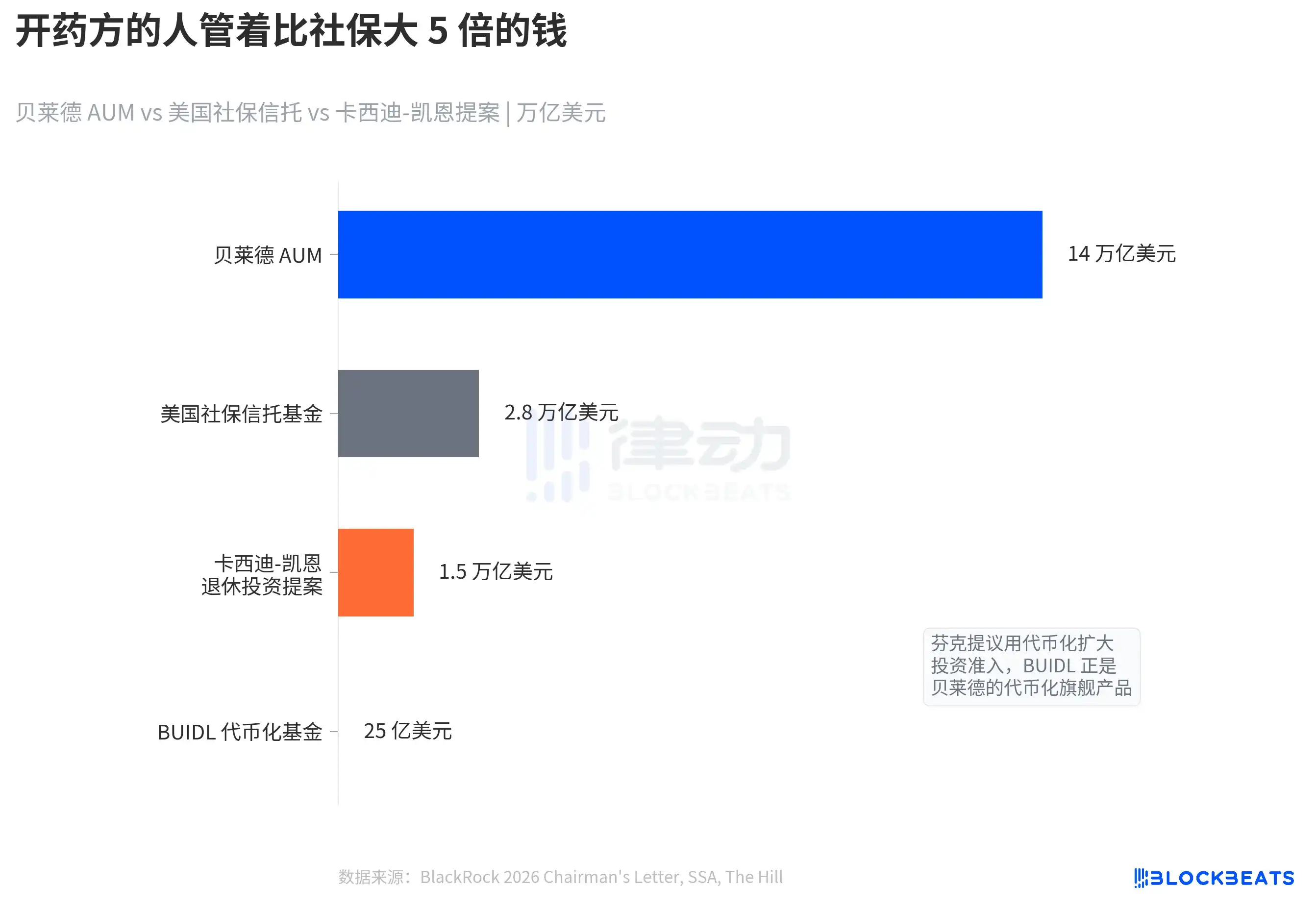

Сравните цифры. Трастовый фонд социального обеспечения США составляет около 2,8 триллиона долларов, предложение Кэссиди-Кейна предполагает вливание 1,5 триллиона. А объем активов под управлением BlackRock составляет 14 триллионов долларов, что в 5 раз больше фонда соцобеспечения. Если правительство действительно создаст инвестиционный фонд в 1,5 триллиона, кто будет им управлять? Финк не говорит прямо, но BlackRock является крупнейшей в мире управляющей компанией.

Еще более показательно второе предложение Финка. Он позиционирует токенизацию как «примерный эквивалент интернета в 1996 году» и предлагает создать «регулируемый цифровой кошелек», чтобы обычные инвесторы могли использовать его для хранения ETF, облигаций, стейблкоинов и долей инфраструктуры. Это снизит порог входа для инвестиций и позволит большему числу людей участвовать на рынке.

Это видение идеально соответствует крупнейшей бизнес-ставке BlackRock за последние два года. Фонд BUIDL от BlackRock (ончейн-фонд токенизированных казначейских облигаций США) в марте 2025 года превысил 1 миллиард долларов AUM, а к середине года пиковая стоимость приблизилась к 2,9 миллиарда, что составляет более 40% рынка токенизированных казначейских обязательств. В феврале 2026 года BUIDL вышел на Uniswap, позволив инвесторам из белого списка торговать стейблкоинами круглосуточно. По сообщениям CCN, BUIDL стал одним из крупнейших в мире токенизированных cash-продуктов.

Заявления Финка о интересах и политические предложения идеально совпадают. Он призывает к тому, чтобы больше людей выходили на инвестиционный рынок через токенизацию, а флагманский токенизированный продукт BlackRock уже ждет клиентов. Он предлагает правительству создать крупный инвестиционный фонд, а BlackRock является наиболее квалифицированным учреждением для управления этими деньгами. Это не обвинение его во лжи, а указание на структурный факт. Когда генеральный директор крупнейшей в мире управляющей компании призывает расширить доступ к инвестициям, он одновременно призывает расширить свою собственную клиентскую базу.

В тот же день с Уолл-стрит поступил еще один сигнал.

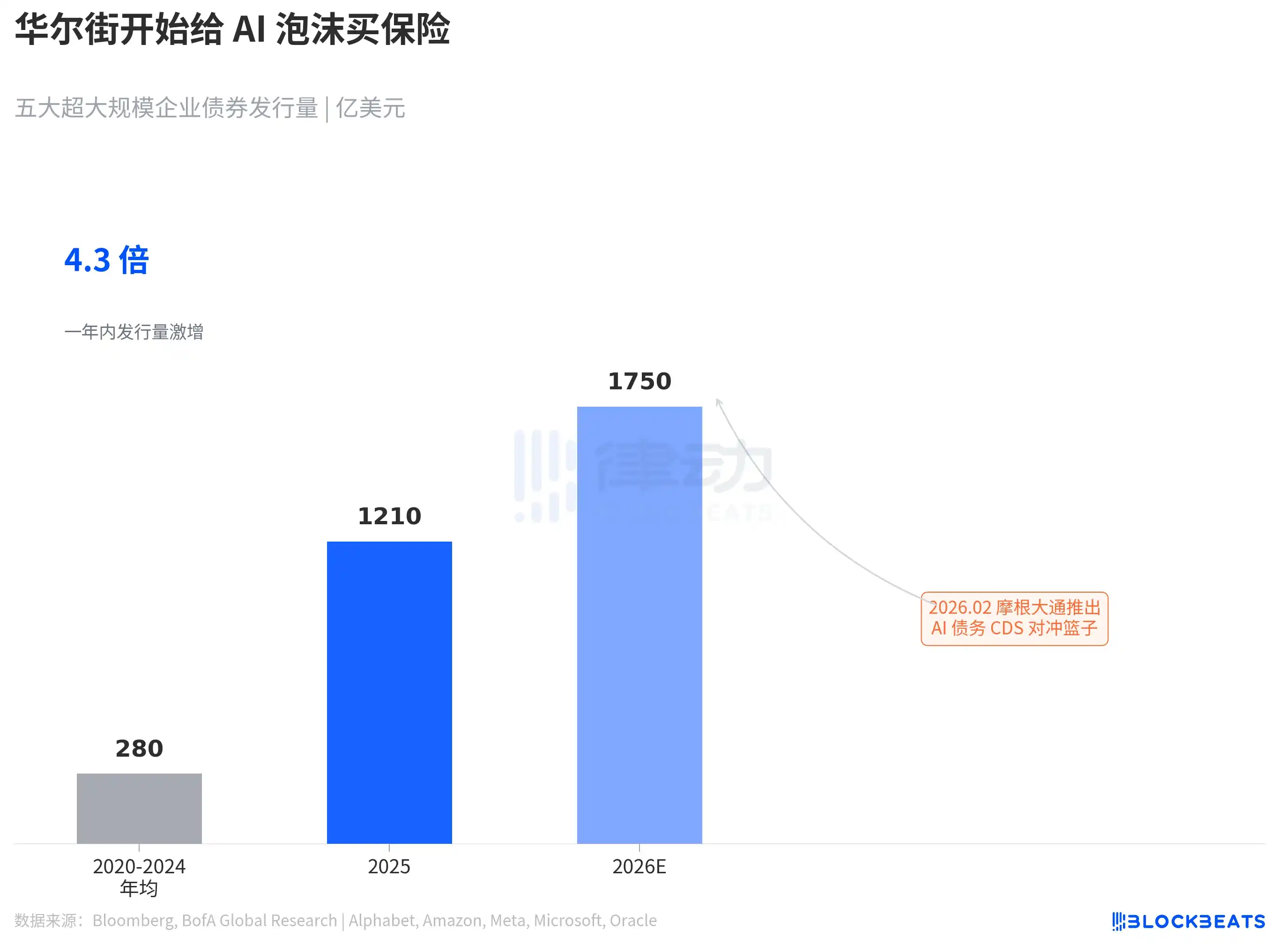

По данным Bloomberg, JPMorgan Chase в феврале 2026 года推出了 (запустила) корзину CDS (кредитных дефолтных свопов) на пять компаний-гиперскейлеров (Alphabet, Amazon, Meta, Microsoft, Oracle) с торговым лотом в 25 миллионов долларов. Эти пять компаний выпустили в 2025 году облигаций на сумму около 121 миллиарда долларов, что в 4,3 раза больше среднегодового объема выпуска в 280 миллиардов в 2020-2024 годах. По прогнозам Bank of America, объем выпуска в 2026 году进一步攀升 ( further climb ) до 175 миллиардов долларов.

Когда Уолл-стрит начинает разрабатывать инструменты хеджирования для долговой нагрузки инфраструктуры ИИ, это означает, что институциональные инвесторы уже готовятся к краху пузыря. Финк говорит, что ИИ усугубит неравенство, а JPMorgan говорит, что долговые риски ИИ уже достаточно велики, чтобы продавать страховку. Оба сигнала указывают на один и тот же факт. Бум ИИ создает огромное богатство, но способ распределения этого богатства и риски повторяют модель предыдущего цикла.

Финк управляет 14 триллионами долларов. Его диагноз неравенства точен. Но предлагаемое им лечение — это恰好 (как раз) его собственный продукт.