Автор | Odaily Planet Daily (@OdailyChina)

Автор | Ethan (@ethanzhang_web3)

Приближается конец года, и вопрос о том, кому достанется жезл председателя Федеральной резервной системы (ФРС) — «главного крана» глобальной ликвидности, стал самой ожидаемой интригой конца года.

Несколько месяцев назад, когда базовая процентная ставка впервые завершила длительную паузу и начала снижаться, рынок был уверен, что Кристофер Уоллер (Christopher Waller) — тот самый избранник (рекомендуемая статья: «Академик совершает прорыв: профессор из маленького городка Уоллер становится самым горячим кандидатом на пост председателя ФРС»). В октябре направление ветра изменилось, и Кевин Хассет (Kevin Hassett) вышел вперед, его шансы一度 приближались к 85%. Его рассматривают как «рупор Белого дома»; если он займет пост, политика может полностью следовать воле Трампа, и его даже в шутку называют «печатным станком в человеческом облике».

Однако сегодня мы будем обсуждать не фаворита, а «второго в очереди» с наибольшим потенциалом перемен — Кевина Уорша (Kevin Warsh).

Если Хассет представляет «ожидания жадности» рынка (более низкие ставки, больше денег), то Уорш представляет «страх и трепет» рынка (более жесткие деньги, более строгие правила). Почему рынок сейчас заново оценивает этого аутсайдера, которого когда-то называли «золотым мальчиком Уолл-стрит»? Если он действительно возглавит ФРС, какие фундаментальные изменения произойдут в крипторынке? (Прим. Odaily: основные идеи данной статьи основаны на недавних выступлениях и интервью Уорша.)

Эволюция Уорша: от золотого мальчика Уолл-стрит до аутсайдера ФРС

У Кевина Уорша нет докторской степени по макроэкономике, и начало его карьеры также не связано с академическими кругами — он начал в отделе слияний и поглощений Morgan Stanley. Этот опыт наложил на него отпечаток, совершенно отличный от мышления Бернанке или Йеллен: в глазах академиков кризис — это просто аномалия данных в модели; но для Уорша кризис — это секунда, когда контрагент по сделке объявляет дефолт, момент жизни и смерти, когда ликвидность мгновенно исчезает.

В 2006 году, когда 35-летний Уорш был назначен членом Совета управляющих ФРС, многие сомневались в его недостаточном опыте. Но история иронична: именно этот практический опыт «инсайдера Уолл-стрит» сделал его незаменимой фигурой в последовавшем финансовом кризисе. В самые темные моменты 2008 года роль Уорша вышла далеко за рамки регулятора — он стал единственным «переводчиком» между ФРС и Уолл-стрит.

Фрагмент интервью Уорша в Гуверовском институте Стэнфордского университета

С одной стороны, ему приходилось переводить токсичные активы Bear Stearns, которые за ночь стали бесполезными, на язык, понятный академическим чиновникам; с другой стороны, он должен был объяснять паникующему рынку намерения ФРС по спасению ситуации, выраженные сложным языком. Он лично участвовал в переговорах в безумные выходные перед крахом Lehman Brothers, и этот близкий контакт дал ему почти инстинктивную чувствительность к «ликвидности». Он понял суть количественного смягчения (QE): центральный банк действительно должен выступать в роли «кредитора последней инстанции» во время кризиса, но по сути это сделка, в которой будущий кредит обменивается на время выживания в настоящем. Он даже остро указал, что длительное «кровопускание» после кризиса на самом деле является «обратным Робин Гудом», искусственно завышая цены активов, чтобы грабить бедных и отдавать богатым, что не только искажает рыночные сигналы, но и закладывает более серьезную бомбу.

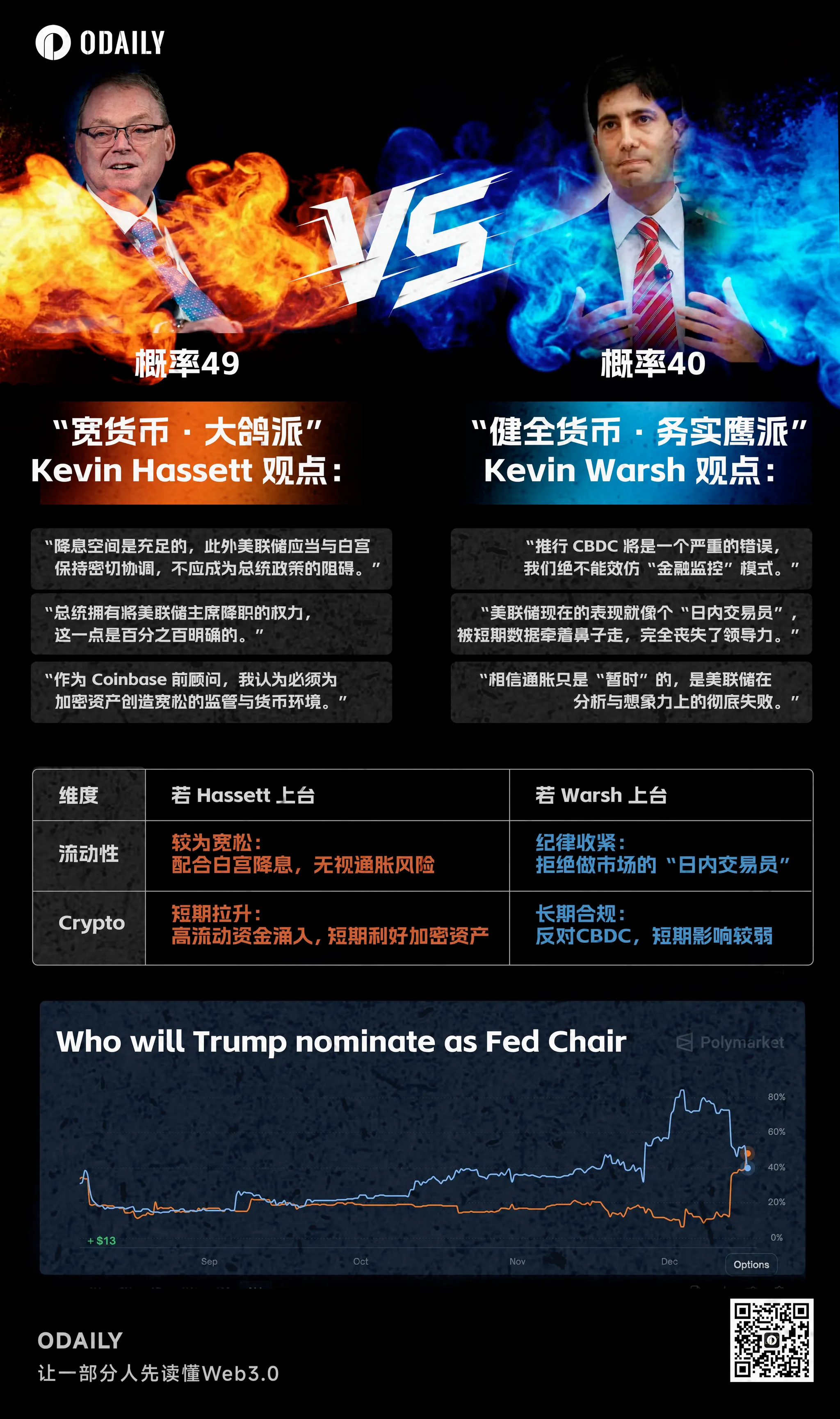

Именно это острое обоняние к уязвимости системы стало его главным козырем, когда Трамп выбирал кандидатов на пост нового председателя ФРС. В этом списке Трампа Уорш и другой горячий кандидат, Кевин Хассет, составили разительный контраст, и эту игру СМИ в шутку назвали «битвой двух Кевинов».

Кандидаты на пост председателя ФРС: Хассет против Уорша, источник: Odaily

Хассет — типичный сторонник «приоритета роста», его логика проста и прямолинейна: пока экономика растет, низкие ставки оправданы. Рынок普遍认为, что если Хассет придет к власти, он, вероятно, будет потакать желанию Трампа иметь низкие ставки и даже начнет снижать их до того, как инфляция будет полностью обуздана. Это также объясняет, почему всякий раз, когда шансы Хассета растут, доходность долгосрочных облигаций резко взлетает, потому что рынок боится выхода инфляции из-под контроля.

Напротив, логика Уорша гораздо сложнее, его трудно просто определить как «ястреба» или «голубя». Хотя он также выступает за снижение ставок, его理由完全不同. Уорш считает, что нынешнее инфляционное давление вызвано не тем, что люди покупают слишком много, а ограничениями предложения и слишком агрессивным выпуском денег за последнее десятилетие. Раздутый баланс ФРС фактически «вытесняет» частный кредит и искажает распределение капитала.

Поэтому Уорш предлагает экспериментальный набор мер: агрессивное сокращение баланса (QT) в сочетании с умеренным снижением ставок. Его намерение ясно: контролировать инфляционные ожидания за счет сокращения денежной массы, восстановить доверие к покупательной способности доллара, то есть немного осушить liquidity; и одновременно снизить номинальные ставки, чтобы ослабить финансовые затраты для предприятий. Это жесткая попытка заставить экономику снова работать без накачки liquidity.

Эффект бабочки для крипторынка: ликвидность, регулирование и ястребиная сущность

Если Пауэлл похож на «мягкого отчима» крипторынка, который осторожничает и не хочет будить детей, то Уорш больше похож на «строгого директора школы-интерната» с указкой в руках. Буря, вызванная взмахом крыльев этой бабочки, может быть более сильной, чем мы ожидали.

Эта «строгость»首先 проявляется в его щепетильности к ликвидности. Крипторынок, особенно биткоин, в каком-то смысле является производным от глобального изобилия долларов за последнее десятилетие. А ядро политики Уорша — «стратегическая перезагрузка», возврат к稳健货币原则 эпохи Волкера. Его упомянутое «агрессивное сокращение баланса» для биткоина является как краткосрочным кошмаром, так и долгосрочным испытанием.

Уорш четко заявил: «Если вы хотите снизить ставки, вы должны сначала остановить печатный станок». Для рискованных активов, привыкших к «опциону пут ФРС», это означает исчезновение зонтика. Если он, придя к власти, будет твердо проводить свою «стратегическую перезагрузку», ведя денежно-кредитную политику к более稳健原则, сжатие глобальной ликвидности станет первой падающей костяшкой домино. Как «передовой рискованный актив»,高度 чувствительный к ликвидности, криптовалютный рынок в краткосрочной перспективе, несомненно, столкнется с давлением переоценки.

Кевин Уорш обсуждает стратегию процентных ставок председателя ФРС Джерома Пауэлла в программе «Кудлоу», источник: Fox Business

Что более важно, если ему действительно удастся добиться «роста без инфляции» за счет реформ供给侧, чтобы реальная доходность长期 оставалась положительной, то владение фиатными деньгами и гособлигациями станет прибыльным. Это разительно отличается от эпохи отрицательных ставок 2020 года, когда «все росло, и только наличные были мусором». Привлекательность биткоина как «актива с нулевой доходностью» может подвергнуться серьезному испытанию.

Но у медали две стороны. Уорш — человек,极其迷信于 «рыночной дисциплиной», он绝不会, как Пауэлл, спешить спасать рынок при падении акций на 10%. Такая среда рынка «без дна» может反而 дать биткоину шанс доказать свою состоятельность: когда традиционная финансовая система столкнется с信用трещинами из-за делевериджа (как во время кризиса Silicon Valley Bank), сможет ли биткоин脱离 гравитационного притяжения фондового рынка США и真正 стать Ноевым ковчегом для避险 средств? Это и есть终极экзамен, который Уорш приготовил для крипторынка.

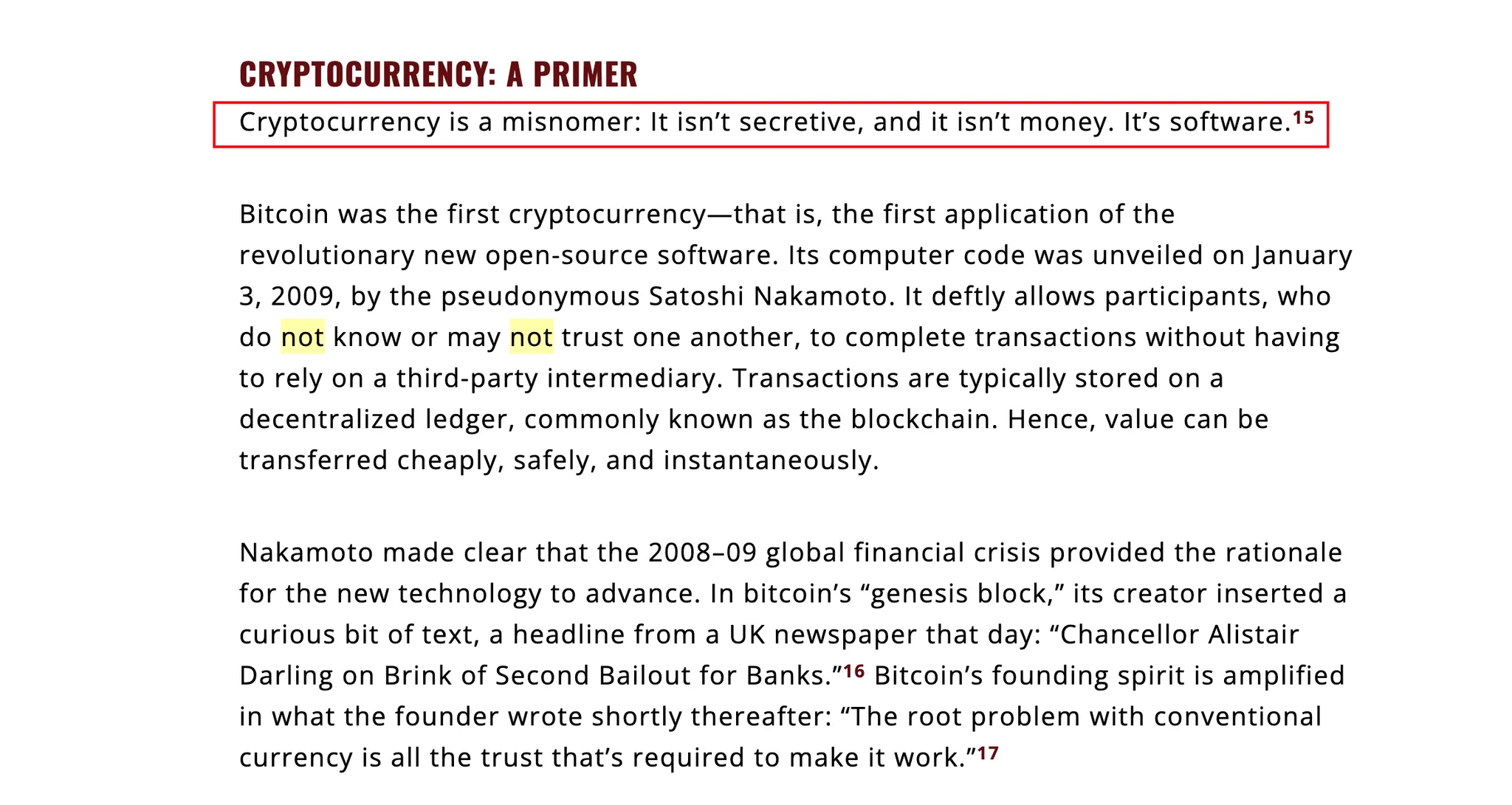

За этим экзаменом скрывается уникальное определение Уоршем криптовалют. В The Wall Street Journal он оставил известную фразу: «Криптовалюта — это неправильное название. В ней нет ничего таинственного, и это не деньги. Это программное обеспечение.»

Фрагмент колонки Кевина Уорша «Деньги превыше всего: доллар, криптовалюты и национальные интересы»

Эта фраза звучит резко, но если вы посмотрите его послужной список, то обнаружите, что он не слепой противник, а инсайдер, глубоко понимающий технические механизмы. Он является не только советником крипто-индексного фонда Bitwise, но и ранним бизнес-ангелом проекта алгоритмического стейблкоина Basis. Basis пытался использовать алгоритмы для имитации операций центрального банка на открытом рынке. Хотя проект в最终 умер из-за регулирования, этот опыт позволил Уоршу понять, как код генерирует «деньги», лучше любого бюрократа.

Именно потому, что понимает, он更жесток. Уорш —典型的 «институционалист», он признает криптоактивы как инвестиционный актив, подобный сырьевым товарам или tech-акциям, но он极低 терпим к «частному чеканению монет», которое бросает вызов суверенитету доллара.

Это двоичное отношение напрямую определит судьбу стейблкоинов. Уорш, вероятно, будет продвигать включение эмитентов стейблкоинов в регуляторные рамки «узкого банка»: они должны持有 100% резервов в виде наличных или краткосрочных облигаций, им запрещено заниматься кредитованием с частичным резервированием, как это делают банки. Для Tether или Circle это палка о двух концах: они получат законный статус,类似银行, и их рвы станут极深; но одновременно они потеряют гибкость «теневого банкинга», и их бизнес-модель будет彻底 заперта на процентах по гособлигациям. Что касается тех небольших стейблкоинов, которые пытаются заниматься «кредитным创造нием», они, вероятно, выйдут из игры under such high pressure. (Рекомендуемая статья: «Прощай, эра «банков-корреспондентов»? Пять криптоорганизаций получили ключи к платежной системе ФРС»)

Та же логика распространяется и на CBDC. В отличие от многих республиканцев, которые категорически против, Уорш предлагает более тонкий «американский方案». Он坚决 против «розничного CBDC», выпускаемого ФРС напрямую для физических лиц, считая это вторжением в частную жизнь и выходом за пределы полномочий, что удивительно совпадает с ценностями криптосообщества. Но он является сторонником «оптового CBDC», выступая за использование технологии блокчейн для модернизации межбанковской расчетной системы, чтобы应对 геополитические вызовы.

В такой архитектуре в будущем, возможно, появится любопытное слияние: базовый结算овый уровень контролируется оптовым链 ФРС, а верхний уровень приложений остается регулируемым публичным链 и Web3-机构. Для DeFi это будет конец эпохи «Дикого Запада», но, возможно, и начало настоящей весны для RWA. В конце концов, в логике Уорша, пока вы не пытаетесь заменить доллар, повышение эффективности technology всегда будет приветствоваться.

Заключение

Кевин Уорш — не просто запасной вариант в списке Трампа, он воплощение попытки старого порядка Уолл-стрит спасти себя в цифровую эпоху. Возможно, под его руководством RWA и DeFi, построенные на реальной полезности и институциональном compliance, только вступят в свою真正的 золотую эру.

Однако, пока рынок过度 интерпретирует послужной список Уорша, основатель BitMEX Артур Хейес облил всех трезвой холодной водой. По мнению Хейеса, мы, возможно, все совершили ошибку в направлении,关键 заключается не в том, во что那个人 верил до того, как стать председателем, а в том, поймет ли он, «на кого он работает», заняв этот пост.

Оглядываясь на столетнюю историю ФРС,博弈 между президентом и председателем никогда не прекращалась. В свое время президент Линдон Джонсон, чтобы заставить ФРС снизить ставки,甚至 применил физическую силу к тогдашнему председателю Уильяму Мартину на ранчо в Техасе. По сравнению с этим твиттер-атаки Трампа — просто детская забава. Логика Хейеса жестока, но правдива: президент США в конечном итоге всегда получит желаемую денежно-кредитную политику. А Трамп всегда хочет более низкие ставки, более горячий рынок и более обильное денежное предложение, и независимо от того, кто сидит на этом посту, в конечном итоге ему придется拿出 инструменты для выполнения задачи.

Вот итоговая загадка, стоящая перед крипторынком:

Уорш действительно человек, который хочет положить руку на выключатель печатного станка и попытаться выключить его. Но когда наступит политическая гравитация, когда потребность в росте «Сделать Америку снова великой» столкнется с его идеалом «жестких денег», кто кого приручит: он ли инфляцию, или игра властей его?

В этой博弈 Уорш может быть достойным уважения «ястребиным» оппонентом. Но в глазах опытного трейдера like Хейес, неважно, кто будет председателем, потому что, как бы извилист ни был процесс, пока политическая машина还在 работать, кран ликвидности в конечном итоге всегда будет снова открыт.

Рекомендуемая литература:

«Инфляция — это выбор: Кевин Уолш о修复 ФРС | Необычные идеи»

«Прощай, эра «банков-корреспондентов»? Пять криптоорганизаций получили ключи к платежной системе ФРС»)

«Деньги превыше всего: доллар, криптовалюты и национальные интересы»