Автор: Odaily Planet Daily

Автор: Azuma

16 декабря в ранние часы гигант стейблкоинов Circle официально объявил о завершении подписания соглашения о приобретении ключевых специалистов и технологий команды разработчиков Interop Labs, стоявшей у истоков межсетевого протокола Axelar Network. Это шаг направлен на продвижение стратегии межсетевой инфраструктуры Circle и поможет обеспечить бесшовную и масштабируемую интероперабельность в ключевых продуктах компании, таких как Arc и CCTP.

Это казалось очередным классическим случаем поглощения крупной компанией перспективной команды, ситуацией, выгодной для всех. Однако ключевой момент заключается в томом, что Circle в своем объявлении четко указала: сделка касается только команды Interop Labs и ее интеллектуальной собственности, в то время как Axelar Network, фонд Axelar и токен AXL продолжат独立运作 под управлением сообщества. Другая команда, участвовавшая в проекте, Common Prefix, возьмет на себя деятельность, ранее осуществляемую Interop Labs.

Если подвести краткий итог: Circle забрала исходную команду разработчиков Axelar Network, но открыто отказалась от самого проекта Axelar Network и его токена AXL.

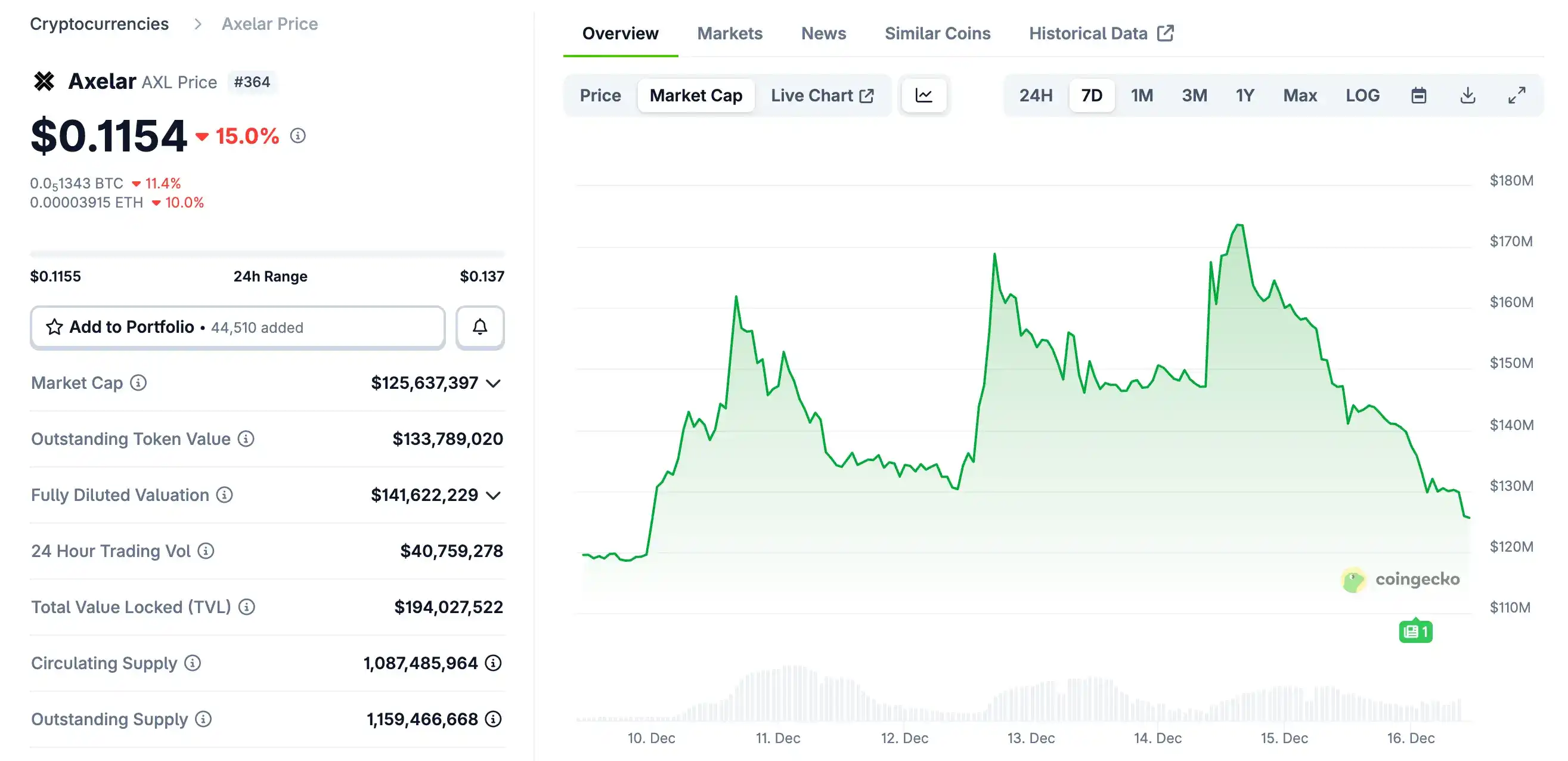

Под влиянием этой внезапной новости курс AXL резко упал. На момент около 10:00 утра он временно составлял $0,115, снизившись на 15% за 24 часа.

В то же время особая ситуация с приобретением по принципу «взять людей, но не токен» и вытекающая из нее проблема «акции против токена» вызвали множество дискуссий в сообществе, где сторонники и противники такой модели поглощения спорят без единого мнения.

Мнение противников: Скрытый RUG, Circle поступает безответственно, страдают только держатели токенов......

Основную силу оппозиции составляют некоторые венчурные капиталисты, что неудивительно — «Я вложил реальные деньги в токены проекта, у меня на руках куча токенов, а теперь ты забираешь тех, кто работал, какого черта мне тогда эти токены?»

Основатель Moonrock Capital Саймон Дедик прокомментировал это так: «Еще одно поглощение, еще один RUG. То, что Circle приобрела Axelar, но четко исключила фонд и токен AXL, — это просто преступление. Даже если это не нарушает закон, это противоречит морали. Если вы основатель, желающий выпустить токен: либо относитесь к нему как к акции, либо убирайтесь прочь».

Сооснователь The Block и основатель 6MV Майк Дудас прокомментировал: «Всем, кто считает это проблемой «токен против акций», я могу четко сказать, что это полностью вина Circle. Ходят слухи, что вице-президент по развитию бизнеса Circle сказал одному из соучредителей Axelar: «Меня не волнуют твои инвесторы», и «купил» CEO и интеллектуальную собственность прямо из-под носа инвесторов, не заплатив им никакой компенсации, при том что эта IP и команда были crucial для запуска Arc».

Основатель Lombard Finance, разместив график AXL, предсказал: «Ключевая команда Axelar куплена Circle, теперь AXL, возможно, ничего не стоит. С момента выпуска токена прошло более трех лет, права команды уже полностью реализованы. Но такой результат вызывает дискомфорт: команда и/или инвесторы продают токены с прибылью, а держатели токенов могут only надеяться на далекую мечту».

Знаковый представитель сообщества ChainLink Зак Райнс заявил: «Это вновь exposes проблему конфликта интересов «токен против акций», которая преследует криптоиндустрию. Команда разработчиков, стоящая за протоколом, успешно приобретена, а держатели токенов, которые финансировали эту команду, не получают ничего. Так называемая independent работа под управлением сообщества无异于 то, что开发团队抛弃了 пользователей ради лучших перспектив. Если мы хотим привлечь настоящий капитал, это именно та первоочередная проблема, которую необходимо решить отрасли».

Руководитель экосистемы SOAR Николас Венцель заявил: «Токен Axelar движется к нулю, спасибо всем за участие. Это еще один случай поглощения, когда держатели токенов не получают ничего, а держатели акций получают substantial прибыль».

Мнение сторонников: Нормальное рыночное поведение, токены изначально находятся на самом дне структуры капитала

Если оппозиция больше focuses на несправедливом отношении к держателям токенов, то сторона поддержки больше focuses на правилах финансирования и слияний и поглощений.

Главный инвестиционный директор Arca Джефф Дорман считает, что действия Circle не являются проблемой, и подробно объяснил структуру капитала корпоративного финансирования и天然所处的劣势位置 токенов.

Компании привлекают financing через различные уровни структуры капитала, и эти уровни本身就有清晰的优先级顺序 —有些层级天然比其他层级更靠前 — Обеспеченный долг > Необеспеченный приоритетный долг > Субординированный долг > Привилегированные акции > Обыкновенные акции > Токены.

В истории было бесчисленное количество случаев, когда выгода одного типа инвесторов достигалась за счет ущерба для другого типа инвесторов.

- При банкротстве и ликвидации кредиторы выигрывают за счет инвесторов в акции;

- При leveraged buyout (LBO) держатели акций often получают выгоду за счет кредиторов;

- При невыгодном поглощении (take-under) кредиторы usually имеют приоритет над держателями акций;

- При стратегическом приобретении usually выигрывают и кредиторы, и держатели акций (но не всегда);

- А токены often находятся на самом дне структуры капитала......

Это не означает, что токены не имеют ценности, и не означает, что токены обязательно need某种«защитный механизм»,但 рынок должен осознавать реальность: когда кто-то приобретает компанию, стоимость которой и так невысока, а выпущенные ею токены也几乎一文不值, держатели токенов не получат凭空「магического дивиденда». В such ситуации выгода от акций often реализуется за счет потерь по токенам.

Соучредитель Electric Capital Авичал Гарг также прокомментировал: «Это нормально. Если вся будущая стоимость создается командой, то ни одна компания не захочет платить returns инвесторам».

Ключевое противоречие: Что такое токен на самом деле?

Вокруг скандала с поглощением Axelar компанией Circle по принципу «взять людей, но не токен» обе стороны спора, кажется, по-своему правы.

Гнев оппозиции реален: держатели токенов взяли на себя风险 в самое трудное для проекта время, когда更需要 ликвидность и narrative поддержка, но были полностью исключены в ключевой момент реализации стоимости. По результатам, ключевая команда и интеллектуальная собственность实现了变现 стоимости, а токены были оставлены в вакуумном narrative «управления сообществом». Рынок проголосовал самым прямым образом — ценой, что действительно deeply разочарует всех, кто верил в стоимость токенов.

Суждение стороны поддержки также разумно в практическом смысле: с точки зрения строгой структуры капитала, токены не являются ни долгом, ни акциями и天然 не обладают приоритетом в контексте слияний и поглощений и ликвидации. Circle не нарушила существующие商业规则, она просто冷静地 выбрала самые ценные для себя активы.

Истинное ядро противоречия заключается не в том,道德 ли поступила Circle, а в проблеме, long время намеренно замалчиваемой отраслью: чем является токен в юридической и экономической структуре?

Когда перспективы радужны, токены默认为「квази-акции», им赋予воображение требования на будущий успех; но в реальных сценариях, таких как поглощения, банкротства, ликвидации, они быстро возвращаются к своей原始форме「сертификата без прав». Именно это — narrative акционирование при структурном нахождении на самом дне — является корнем反复出现的 конфликтов.

Случай с поглощением Axelar, возможно, не станет последним подобным спора, но хотелось бы надеяться, что он станет поводом для дальнейшего размышления индустрии о позиционировании и смысле токенов —Токены не обладают правами по天然, только институционализированные, структурированные права будут признаны в关键时刻, а конкретные формы реализации still требуют совместных исследований и практики всех участников отрасли.