Ethereum переходит к масштабированию L1 и конфиденциальности, а движок фондового рынка США DTCC с $100 триллионами начинает миграцию в ончейн, кажется, что новая волна крипто-инноваций вот-вот наступит.

Но логика прибыли институтов и розничных инвесторов совершенно различна.

Институты обладают чрезвычайно высокой толерантностью во времени и пространстве: десятилетний инвестиционный цикл и арбитраж с крошечными спредами гораздо надежнее, чем мечты розничных инвесторов о тысячекратном росте за год. В предстоящем цикле很可能 одновременно появятся ончейн-процветание, приток институтов и давление на розничных инвесторов.

Пожалуйста, не удивляйтесь: спотовый BTC ETF и DAT, четырехлетний цикл BTC и полное исчезновение «альткойн-сезона», а также переход корейцев «от монет к акциям» неоднократно подтверждают эту логику.

После 10.11 CEX, как последний барьер для проектов, VC и маркет-мейкеров, также официально вступили в «мусорное время»: чем больше влияние на рынок, тем более консервативной становится стратегия, что в дальнейшем разъедает эффективность капитала.

Бесполезность альткойнов и мемы от редакторов — все это лишь эпизоды на пути, обрушенном собственным весом. Миграция в ончейн — вынужденный шаг, но он будет несколько отличаться от того свободного и процветающего мира, который мы себе представляли.

Мы надеялись компенсировать эффектом богатства онемение, последовавшее за потерей веры в децентрализацию. Надеемся, мы не потеряем ни свободу, ни процветание.

Сегодня я в последний раз коснусь концепций децентрализации, киберпанка и т.д. Старые истории о свободе и предательстве уже не поспевают за неумолимым колесом времени.

Децентрализация: рождение карманного компьютера

DeFi не построена на идеях и сущности Биткойна, никогда не была.

Ник Сабо (Nick Szabo), создатель «смарт-контрактов» (1994) и Bit Gold (впервые предложен в 1998, доработан в 2005), а также вдохновитель ключевых концепций Bitcoin, таких как PoW (доказательство работы) и запись временных меток.

Он ласково называл Биткойн карманным компьютером, а Ethereum — универсальным компьютером. Однако после инцидента с The DAO в 2016 году, когда Ethereum решил откатить транзакции, Ник Сабо стал критиком Ethereum.

В бычьем цикле ETH 2017-2021 годов Ника Сабо считали старомодным упрямцем.

С одной стороны, Ник Сабо искренне считал, что Ethereum превзошел Биткойн, реализовав лучшую дезинтермедиацию (устранение посредников), поскольку в то время Ethereum полностью реализовал PoW и смарт-контракты.

С другой стороны, Ник Сабо считал, что Ethereum реформировал систему управления с точки зрения децентрализации доверия (distrust), механизм DAO впервые позволил эффективное взаимодействие и collaboration между незнакомцами по всему миру.

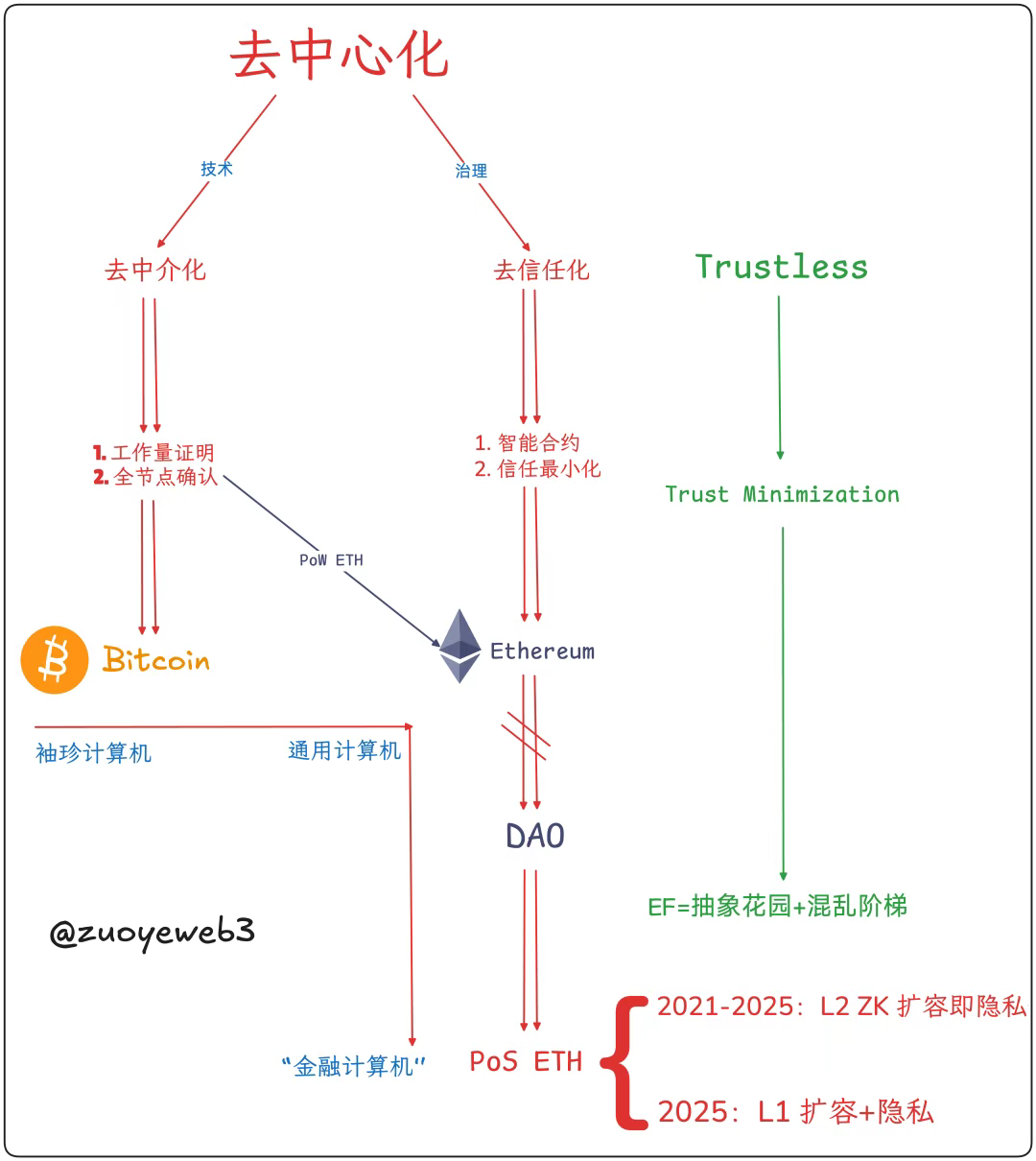

Так мы очертили, что на самом деле подразумевается под децентрализацией: дезинтермедиация на техническом уровне -> стоимость определения цены + консенсус транзакций, децентрализация доверия на уровне управления -> минимизация доверия.

Описание изображения: Составляющие децентрализации

Источник изображения: @zuoyeweb3

-

Дезинтермедиация: не нужно полагаться на золото или правительство, вместо этого использовать вычислительную работу как подтверждение участия в производстве Биткойна;

-

Децентрализация доверия: не нужно полагаться на социальные отношения людей, вместо этого открываться вовне при минимизации доверия, создавая сетевые эффекты.

Хотя Сатоши Накамото находился под влиянием Bit Gold, он не высказывался определенно о смарт-контрактах. В духе простоты, хотя он сохранил возможность комбинирования опкодов для сложных операций, в целом он практиковал одноранговые платежи.

Это также причина, по которой Ник Сабо увидел надежду в PoW ETH: полные смарт-контракты и «самоограничение». Конечно, Ethereum столкнулся с препятствием масштабирования L1, подобным биткойновскому, и Виталик в итоге выбрал масштабирование L2, чтобы уменьшить вред для本体 L1.

Этот «вред» в основном относится к кризису размера полных узлов. Биткойн, потеряв оптимизацию Сатоши, помчался по пути безвозвратной гонки майнеров + вычислительной мощности, фактически исключив individuals из производственного процесса.

Описание изображения: Размер узла блокчейна

Источник изображения: @zuoyeweb3

Виталик, по крайней мере, сопротивлялся. До капитуляции перед моделью «цепочки дата-центров» в 2025 году, хотя и перешел на модель PoS, но также по возможности гарантировал существование персональных узлов.

Хотя PoW часто приравнивают к вычислительной мощности + потреблению электроэнергии для определения его базовой производственной стоимости, в раннем движении киберпанка доказательство работы и временные метки сочетались для подтверждения времени транзакции, формирования общего консенсуса и, на этой основе, взаимного признания.

Следовательно, переход Ethereum на PoS фундаментально исключает персональные узлы из производственной системы. В сочетании с «бесплатными» ETH, накопленными во время ICO, и почти $100 млрд, инвестированными VC в экосистему EVM+ZK/OP L2, невидимо накопилась колоссальная институциональная стоимость. DAT ETH можно полностью рассматривать как форму институционального OTC-выхода.

После провала дезинтермедиации на техническом уровне, хотя и удалось сдержать взрыв узлов, но движение пошло towards пулов майнеров и гонки вычислительной мощности. Ethereum прошел через несколько циклов L1 (шардинг, сайдчейны) -> L2 (OP/ZK) -> L1 и в конечном итоге фактически полностью embraced крупные узлы.

Необходимо объективно отметить: Биткойн потерял смарт-контракты и «персонализацию» вычислительной мощности, Ethereum потерял «персонализацию» узлов, но сохранил смарт-контракты и способность ETH захватывать стоимость.

Также субъективно оценим: Биткойн достиг минимизации управления, но сильно зависит от «совести»少数开发者的维护 консенсуса. Ethereum в конечном итоге отказался от модели DAO и перешел к централизованной модели управления (теоретически нет, но фактически Виталик может контролировать Ethereum Foundation, а EF может направлять развитие экосистемы Ethereum).

Здесь нет скрытого желания принизить ETH и возвысить BTC. С точки зрения эффекта богатства и цены, early инвесторы обоих были успешны. Но с точки зрения практики децентрализации, возможность их коренного изменения уже не видна.

Биткойн почти наверняка не будет поддерживать смарт-контракты, Lightning Network и BTCFi все еще занимаются платежами. Ethereum сохранил смарт-контракты, но отказался от ценового бенчмарка PoW и, помимо децентрализации доверия/минимизации доверия, выбрал исторический шаг назад — построение централизованной системы управления.

Историческую оценку оставим потомкам.

Экономика посредников: падение мирового компьютера

Где есть организация, там必然 есть внутренняя борьба; где говорят о единстве, там必然需要 центр, а затем рождается бюрократия.

В механизме ценообразования токенов есть два подхода: нарративный и основанный на спросе. Например, нарратив Биткойна — ориентированный на применение — одноранговая электронная наличность, но спрос на Биткойн — это цифровое золото. Нарратив Ethereum — «мировой компьютер», но спрос на ETH — ориентированный на применение — Gas Fee.

Эффект богатства более дружелюбен к механизму PoS. Для участия в стейкинге Ethereum сначала нужен ETH, использование DeFi Ethereum также требует ETH. Способность ETH захватывать стоимость, в свою очередь, усиливает обоснованность PoS. Ethereum был прав, отказавшись от PoW под牵引ом реального спроса.

Но на нарративном уровне модель Объем транзакций ✖️ Gas Fee очень близка к SaaS и Fintech и не соответствует грандиозному нарративу «вычислять всё». Когда пользователи, не использующие DeFi, уйдут, стоимость ETH не сможет постоянно поддерживаться.

В итоге, никто не использует Биткойн для транзакций, но всегда найдутся желающие вычислять всё на Ethereum.

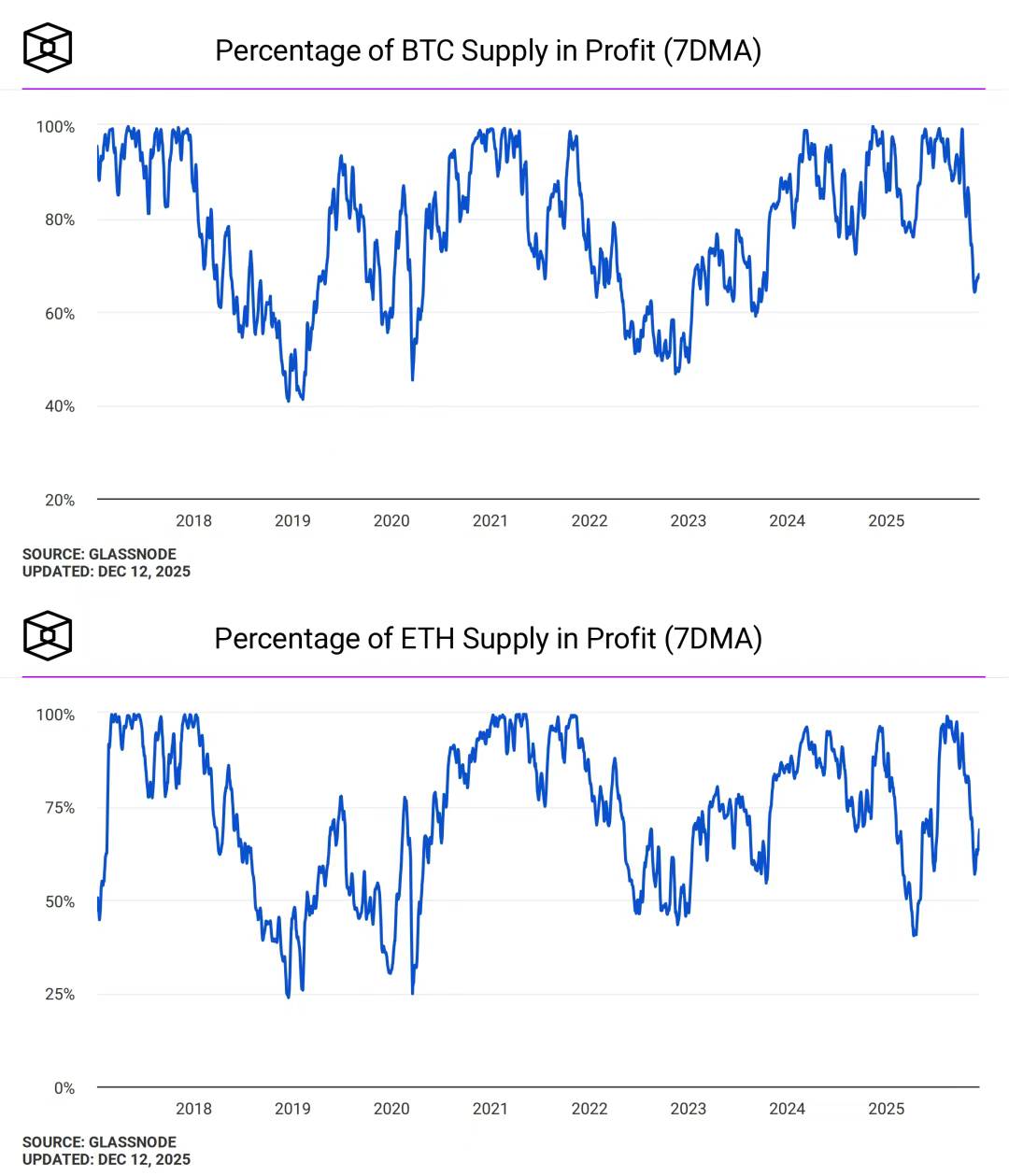

Описание изображения: Прибыльность адресов BTC и ETH

Источник изображения: @TheBlock__

Децентрализация ≠ эффект богатства. Но после перехода Ethereum на PoS, он по умолчанию признал, что капитальная стоимость ETH — его единственная цель. Колебания цены будут постоянно привлекать чрезмерное внимание рынка, further подвергая拷问 разрыв между его видением и реальностью.

Для сравнения, рост и падение цен на золото и Биткойн уже в значительной степени приравниваются к базовым изменениям рыночных настроений. Люди беспокоятся о мировой ситуации, когда золото резко растет, но никто не сомневается в базовой стоимости Биткойна, когда он падает.

Сложно сказать, что именно Виталик и EF привели к «де»-децентрализации Ethereum, но必须 признать, что система Ethereum становится все более посреднической.

В 2023/24 годах стало модным, чтобы члены Ethereum Foundation становились советниками проектов, например, Dankrad Feist в EigenLayer. Но мало кто помнит, что The DAO было неясно связано с несколькими核心成员 Ethereum.

Это продолжалось до тех пор, пока Виталик официально не объявил, что больше не будет инвестировать в проекты L2. Но системная «бюрократизация» всего Ethereum уже стала不可避免ной.

В некотором смысле, посредник не обязательно несет негативный оттенок, like маклер, а означает эффективное сопоставление и удовлетворение взаимных потребностей. Например, Фонд Solana,一度 считавшийся отраслевым эталоном, в целом продвигает развитие проектов исходя из потребностей рынка и собственной экосистемы.

Но для ETH и Ethereum, ETH должен стать «посредническим» активом, а Ethereum должен оставаться полностью открытым и автономным,维持 техническую архитектуру публичного блокчейна без разрешений.

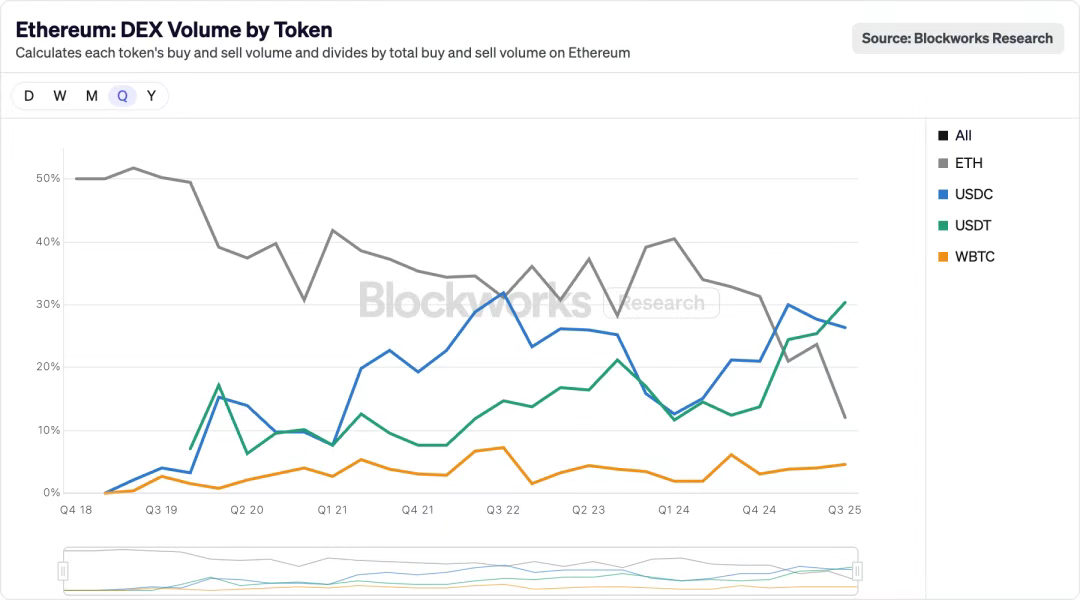

Описание изображения: Ethereum DEX Volume by Token

Источник изображения: @blockworksres

В экосистеме Ethereum наблюдается тенденция, когда стейблкоины постепенно вытесняют ETH. Ликвидность мигрирует в ончейн с Perp DEX, а USDT/USDC также profoundly меняют старую格局. История замены ETH/BTC стейблкоинами в качестве базового актива на CEX повторится в ончейне.

А USDT/USDC как раз и являются централизованными активами. Если ETH не сможет поддерживать обширные сценарии применения и будет использоваться только как «актив», то в условиях ускорения и снижения комиссий, объем потребления Gas Fee должен быть достаточно большим, чтобы维持 цену ETH.

Более того, если Ethereum хочет быть полностью открытым, он должен позволять любым активам выступать в качестве промежуточного актива. Но это серьезно навредит способности ETH захватывать стоимость. Поэтому L1 должна забрать власть у L2, L1 должна重新 масштабироваться. Конфиденциальность в этом контексте можно интерпретировать как необходимость для институтов, а也可以 как выбор, не забывающий первоначальные намерения.

Здесь много историй, каждая值得 послушать. Но你必须 выбрать направление для действий.

Полная децентрализация не может достичь минимизации организации, приводя к тому, что каждый действует в одиночку. В соответствии с принципом эффективности, можно only постоянно склоняться к минимизации доверия. Минимизация доверия, опирающаяся на порядок, производный от Виталика, ничем не отличается от крайней свободы, которую Санье [Sun Ge] дает черно-серным business.

Мы должны either доверять Виталику, либо доверять Санье [Sun Ge]. Проще говоря, децентрализация не может建立自在、自维持的秩序 (установить спонтанный, самоподдерживающийся порядок). Люди внутренне渴望极端的混乱 (жаждут крайнего хаоса), но телом крайне厌恶缺乏安全感的环境 (крайне厌恶 среду без чувства безопасности).

Виталик — посредник, ETH — посредник, Ethereum также будет посредником между традиционным миром и ончейном. Ethereum хочет продукта без продукта, но любой продукт неизбежно несет элементы маркетинга, фальши и обмана. «Just use Aave» и UST не имеют фундаментальных различий.

Только повторяя первое неудачное действие, финансовая революция может succeed. USDT сначала потерпел неудачу в сети Биткойн, UST потерпел неудачу, покупая BTC, затем успех TRC-20 USDT и USDe.

Или же, люди страдают от падения и застоя ETH и от раздувания системы Ethereum, из-за чего розничные инвесторы无力 отделиться от Уолл-стрит.应该是 Уолл-стрит покупала ETH у розничных инвесторов, но люди пожинают горькие плоды покупки ETF и DAT.

Ограничение Ethereum — это сам капитал ETH. Производство ради производства, производство ради ETH — это две стороны одной медали, самоочевидная истина. Восток и Запад не покупают активы друг у друга, капитал и проекты, предпочитающие certain экосистему, определенного предпринимателя, в конечном итоге производят не для токена инвестированного проекта, а для производства ETH.

Де—–>«централизация»: будущее финансового компьютера

От Второго Интернационала до LGBT, от Партии Черных пантер до Черной пантеры, от Биткойна до Ethereum.

После инцидента с The DAO Ник Сабо возненавидел все, связанное с Ethereum. В конце концов, Сатоши Накамото уже скрылся от мира, но performance Ethereum нельзя назвать плохой. У меня нет шизофрении, чтобы раскритиковать Ethereum, а затем восхвалять Виталика.

По сравнению с публичными блокчейнами следующего поколения, такими как Solana и HyperEVM, Ethereum по-прежнему остается лучшим игроком, балансирующим между децентрализацией и эффектом богатства. Даже Биткойн, его главный недостаток — врожденное отсутствие поддержки смарт-контрактов.

Как 10-летний старый блокчейн, ETH и Ethereum превратились из «оппозиции» в «официальную оппозицию», которым необходимо время от времени воскрешать дух децентрализации и киберпанка, а затем继续 двигаться к现实ному будущему финансового компьютера.

Сова Минервы может летать только ночью. Споры об эффекте богатства и децентрализации должны быть похоронены в Кенигсберге.真正残酷的历史实践 уже похоронил оба этих нарратива.