Author: Nancy, PANews

While crypto enthusiasts were happily posting their SpaceX subscription slips on social media, sharing the joy of participating in this super IPO feast, Trade.xyz on Hyperliquid found itself in the eye of a storm. Its SPCX pre-IPO perpetual contract pricing rules triggered a wave of controversy, making it the focal point of market debate.

After SPCX Pricing Turmoil, Trade.xyz Faces Trust Test

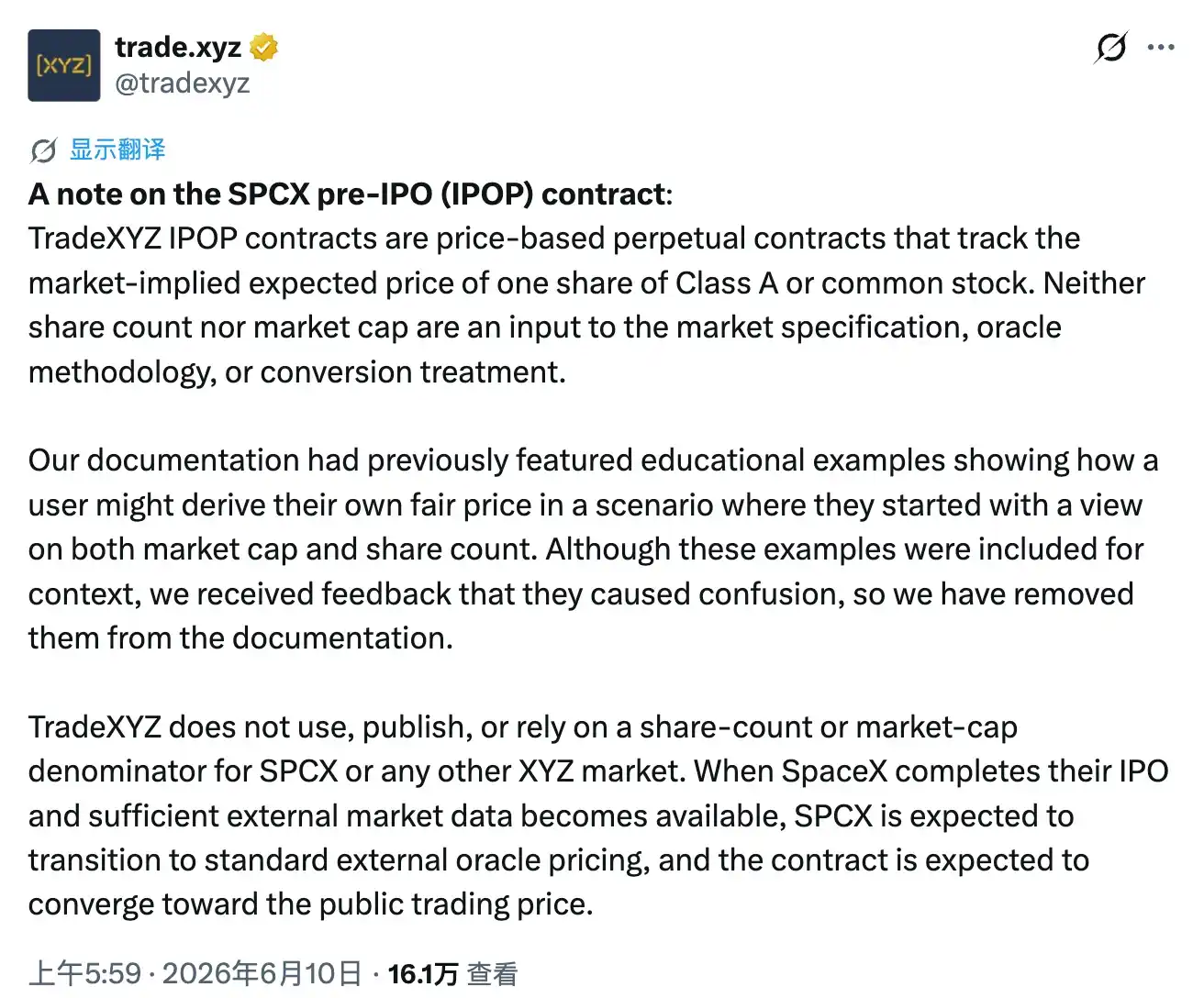

On June 10, Trade.xyz issued a statement formally responding to the recent pricing controversy surrounding its SPCX pre-IPO perpetual contract.

According to the statement, Trade.xyz's IPOP contract is a price-type perpetual contract. Its core goal is to track the market's expectation for the price per share of Class A common stock, rather than reflecting the company's overall valuation. Therefore, information such as the company's total share count or market capitalization is not part of the contract rules, oracle pricing logic, or future contract conversion mechanisms. In other words, the SPCX price on Trade.xyz is more akin to an indicator reflecting market sentiment and trading expectations, not a theoretical share price calculated based on company fundamentals.

Trade.xyz also mentioned that early product documentation included some tutorial examples demonstrating how users could derive a reasonable per-share price based on their own judgment of the company's valuation and total share count. Although these examples were solely for understanding the product mechanism, some users mistakenly believed the platform itself would price based on market cap or share count data. Consequently, these examples have now been removed from the official documentation.

The statement emphasized: Trade.xyz will not use, publish, or rely on share quantities or market capitalization as a pricing benchmark for SPCX or any other XYZ market.

The catalyst for this controversy was the recently disclosed SpaceX prospectus. The document revealed SpaceX's actual total share count to be 13.08 billion shares, approximately 10% higher than the previously long-held market assumption of 11.87 billion shares. This means that, with the company's overall valuation unchanged, the corresponding theoretical per-share price for SpaceX would need to be adjusted downward by about 10%.

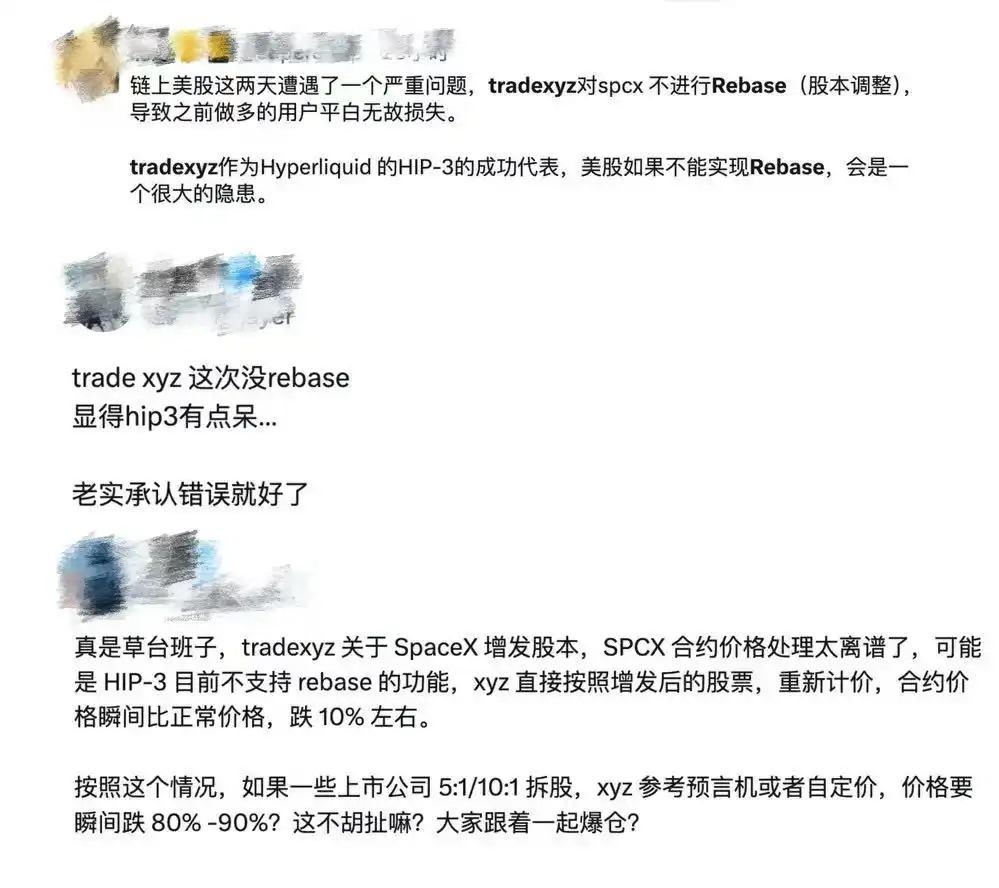

Following the announcement, several centralized exchanges (CEXs) suspended trading of relevant contracts, repriced them based on the new share count data, and then resumed trading. However, Trade.xyz adhered to its product logic of not relying on share count data and therefore did not adjust its pricing framework. These two different pricing systems triggered a wave of cross-platform arbitrage, swiftly pushing Trade.xyz into the center of public criticism.

Regarding resolving this discrepancy in the future, Trade.xyz stated that once SpaceX officially completes its IPO and sufficient external trading data is formed in the public market, SPCX will switch to a standard external oracle pricing mechanism. At that point, the contract price is expected to gradually converge towards the actual trading price of SpaceX stock in the public market.

Feedback from some community members

However, this clarification further fueled market controversy. Many users believe that at the product's launch, Hyperliquid did not sufficiently or clearly disclose the contract rules. Descriptions in the UI interface and official documentation that were prone to misinterpretation existed for a long time. Only as the IPO approached and controversy erupted did the platform hastily issue clarification announcements and amend documentation. This post-facto correction approach was difficult to accept as credible.

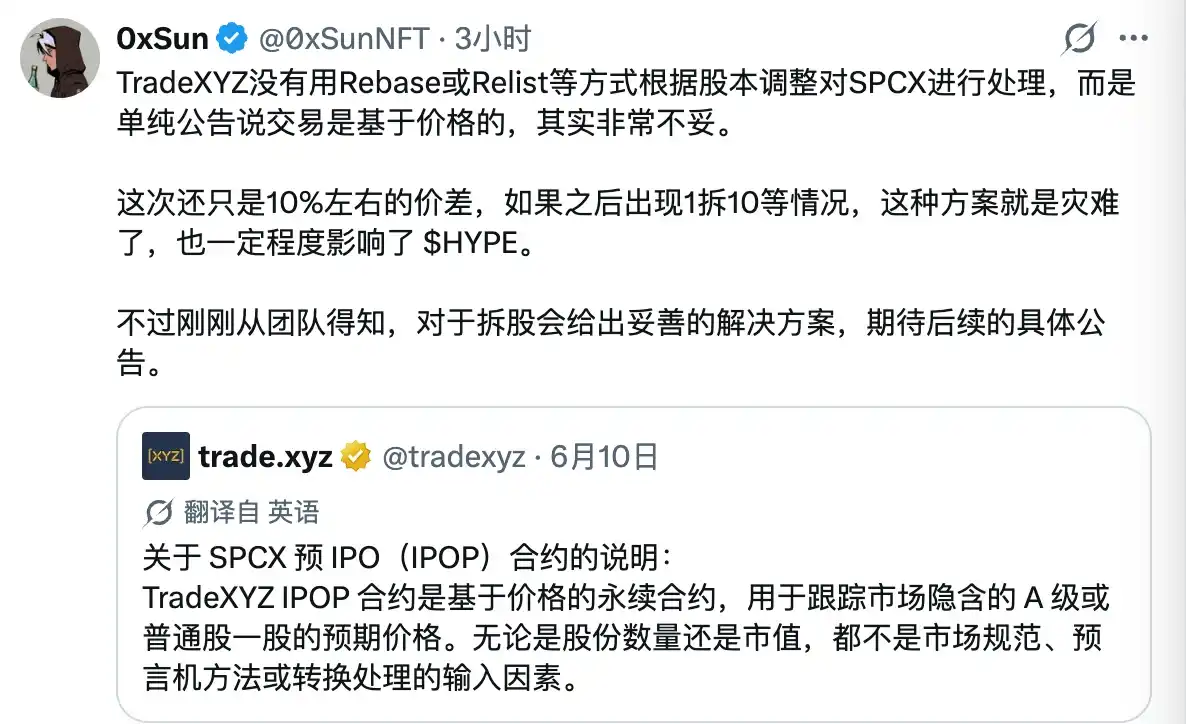

Greater dissatisfaction stemmed from users' real financial losses. Because the HIP-3 mechanism itself lacks the Rebase capability of traditional exchanges, when the market repriced according to SpaceX's latest share count, the SPCX contract price could only be passively adjusted downward in a gap. Consequently, long positions lost about 10% of their value almost instantly. Many users employing high leverage were forced to liquidate their positions or even faced immediate liquidation. These losses directly translated into profits for short sellers and arbitrageurs.

From the perspective of these affected users, the platform not only failed to show sufficient concern for the losses nor proposed any compensation or mitigation plan, but instead responded with "that's how the product mechanism works," appearing very indifferent and lacking in responsibility.

In a sense, this debate surrounding SPCX pricing authority also serves as a reference case for the design and rule disclosure of more on-chain Pre-IPO assets in the future.

Rebase Dilemma Remains, On-Chain Pre-IPO Faces Major Test

For Perp DEXs, lacking Rebase capability implies that any future Pre-IPO asset encountering common corporate actions in traditional stock markets, such as stock splits, secondary offerings, or dividends, could lead to instantaneous contract price revaluation. This could trigger large-scale chain liquidations, unfair losses, and ultimately weaken user trust in the platform.

To understand the importance of Rebase, one must first understand what Rebase is and why it becomes a critical component in the design of Pre-IPO perpetual contracts.

Simply put, Rebase is a value-neutral adjustment mechanism. The platform adjusts the contract price and user position quantity proportionally, ensuring the trader's overall position value remains largely unchanged before and after the adjustment. This mechanism is necessary because during the Pre-IPO phase, a company's actual total share count is often not publicly disclosed. Exchanges can only design the initial contract price and multiplier based on market-estimated share counts. When the company officially files S-1/S-1A documents and discloses the true share count, if there's a discrepancy with the estimate, Rebase is needed to calibrate contract parameters. Otherwise, the contract price gradually deviates from the true per-share value, creating arbitrage opportunities across platforms and forcing unilateral position holders to passively bear losses.

However, compared to CEXs, implementing Rebase on a Perp DEX is more challenging.

Specifically, CEXs rely on centralized databases and professional risk control teams. They can quickly suspend trading after a corporate action (like a share increase or stock split), uniformly adjust all user positions, and then resume market trading. This entire process is handled by the exchange's backend, ensuring user position notional values remain smooth and continuous. However, even for large CEXs with mature trading systems and technical teams, such Rebase operations involving synchronized adjustments across all market positions remain complex engineering tasks.

Moreover, Perp DEXs operate matching, liquidation, and position states entirely on smart contracts, preventing direct data modification like CEXs. Achieving a similar Rebase effect often requires designing additional monitoring logic, special hooks, or upgrading contract mechanisms. This not only increases gas costs and system complexity but also expands the potential attack surface, introducing new security risks.

Beyond this, Rebase could further exacerbate the inherent liquidity fragmentation problem in decentralized markets. The same Pre-IPO asset might exist simultaneously on multiple DEXs, each with limited market depth. Faced with the additional uncertainty brought by Rebase, Liquidity Providers (LPs) might reduce their willingness to deploy capital, ultimately leading to decreased liquidity, increased slippage, and a further deterioration of the trading experience.

Of course, Rebase is not entirely impossible in a decentralized architecture. Community users have pointed out that platforms like Aster have already completed Rebase adjustments for similar assets. This suggests the real challenge is not that DEXs are inherently incapable, but rather whether platforms are willing to design additional mechanisms for it and bear the associated development and operational costs.

In contrast, besides adhering to a more market-oriented pricing philosophy, Trade.xyz, built on the HIP-3 architecture, allows developers to independently deploy their own Perp markets. While this model inherits Hyperliquid's high-performance order book system, each market has completely independent contract specifications, oracle definitions, and parameter settings, lacking native, platform-level unified Rebase support. Therefore, easily implementing batch adjustments for all positions is not feasible. However, community sources have also revealed that Trade.xyz is researching corresponding solutions for potential future events like stock splits.

From a broader perspective, the issues exposed by the SPCX pricing are not merely a product design flaw but represent a practical challenge Perp DEXs must confront while exploring RWA (Real World Asset) assets. In the future, as more Pre-IPO assets are tokenized on-chain, serving as pre-trading markets before public market price formation, a key question remains: Can on-chain Pre-IPO perpetual contracts establish a sufficiently reliable price discovery mechanism? Can they withstand the test of real corporate actions and information disclosures, or will they devolve into capital games detached from fundamentals? Only time and the market will tell.