Author: David, Tide Research

Tide Research Guide:

J.P. Morgan's wealth management division issued a mid-year 2026 outlook report on June 1st, essentially advising its high-net-worth clients on how to invest for the second half of the year.

Against the backdrop of the Strait of Hormuz blockade pushing up oil prices, resurgent inflation, and the AI narrative shifting from fervor to skepticism, the overall tone of this report is cautiously optimistic, albeit with a change in specific investment allocations.

J.P. Morgan believes the market is overly pessimistically pricing the world's three major risks (fragmentation, inflation, AI's disruptive potential), and the current market volatility is precisely a window of opportunity to enter.

The overall judgment is:

Continue betting on the AI supercycle and US stocks, hedge inflation with real assets and alternative strategies, reduce cash holdings, and pay attention to emerging markets.

If you hold US tech stocks or are considering whether to add to or reduce your positions in the second half of the year, the framework and data in this report are worth a look; we have condensed and interpreted the original report, rearranging the priorities according to investment relevance.

Six Key Conclusions:

1. The AI supercycle is not over; the market is overly pessimistic.

The five Hyperscalers (Microsoft, Meta, Oracle, Google, Amazon) are expected to have 2026 capital expenditures exceeding $650 billion, revised up by $130 billion from the last earnings season. AI-related investment contributed 25 basis points to US real GDP growth in 2025. Taiwan's GDP growth exceeded 7%, the fastest since 2010, driven primarily by semiconductor exports. JPM believes the market is pricing in an "AI peak," but the data does not support this narrative.

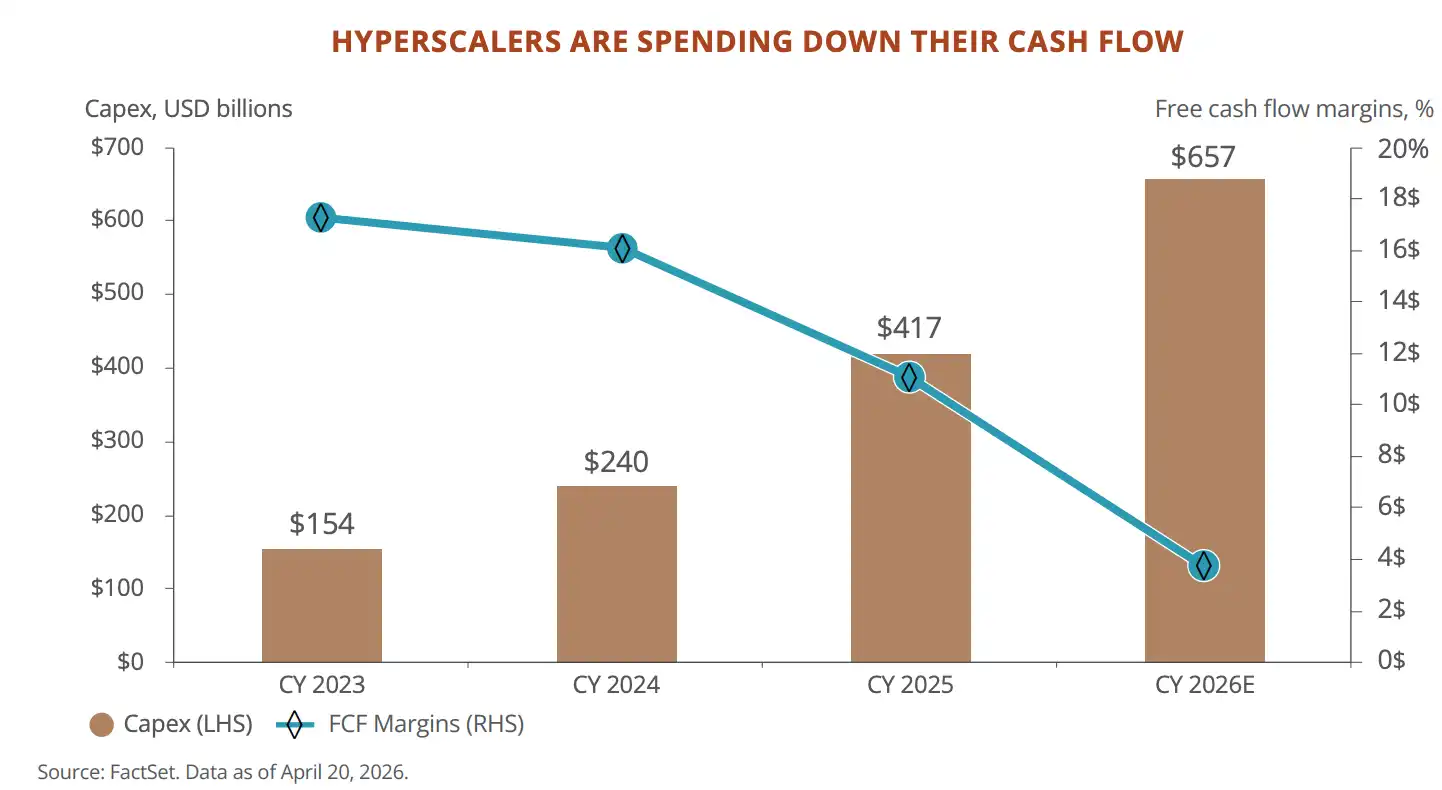

2. However, the financial characteristics of Hyperscalers are changing.

Free cash flow is projected to drop from $240 billion in 2024 to $73 billion by the end of 2026. Microsoft's Forward P/E has fallen from an AI-era high of 35x to 22.5x. These companies are transitioning from "light-asset, high-return" to "heavy-asset, high-investment," and the market is still digesting this shift.

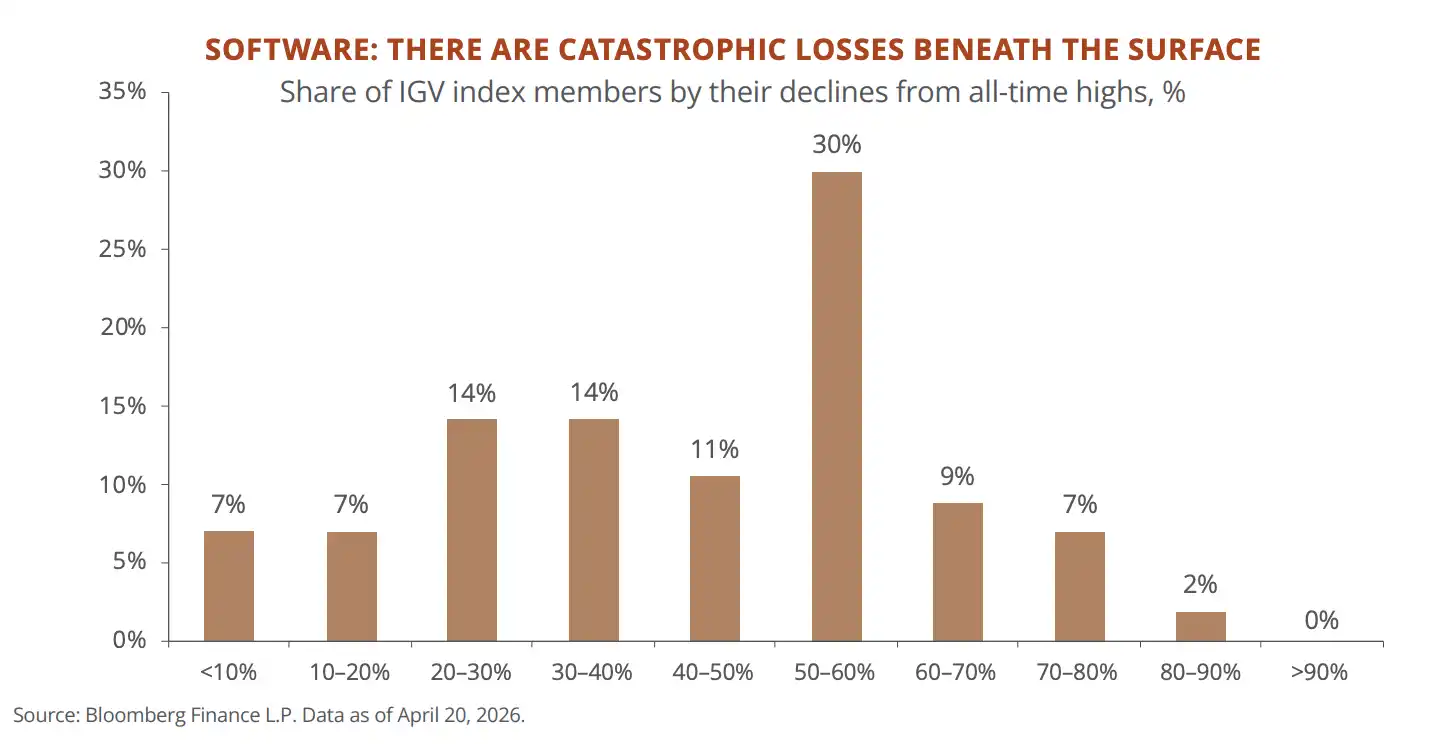

3. SaaS is undergoing an underwater massacre.

Approximately half of the constituents in the S&P Software Index (IGV) have fallen more than 50% from their all-time highs. JPM's tracked "AI Vulnerable Basket" is down nearly 20% this year. In the private credit market, 21% of exposure is to software companies, rising to 40% when combined with tech and business services. The impact of AI on the subscription-based software business model is already happening.

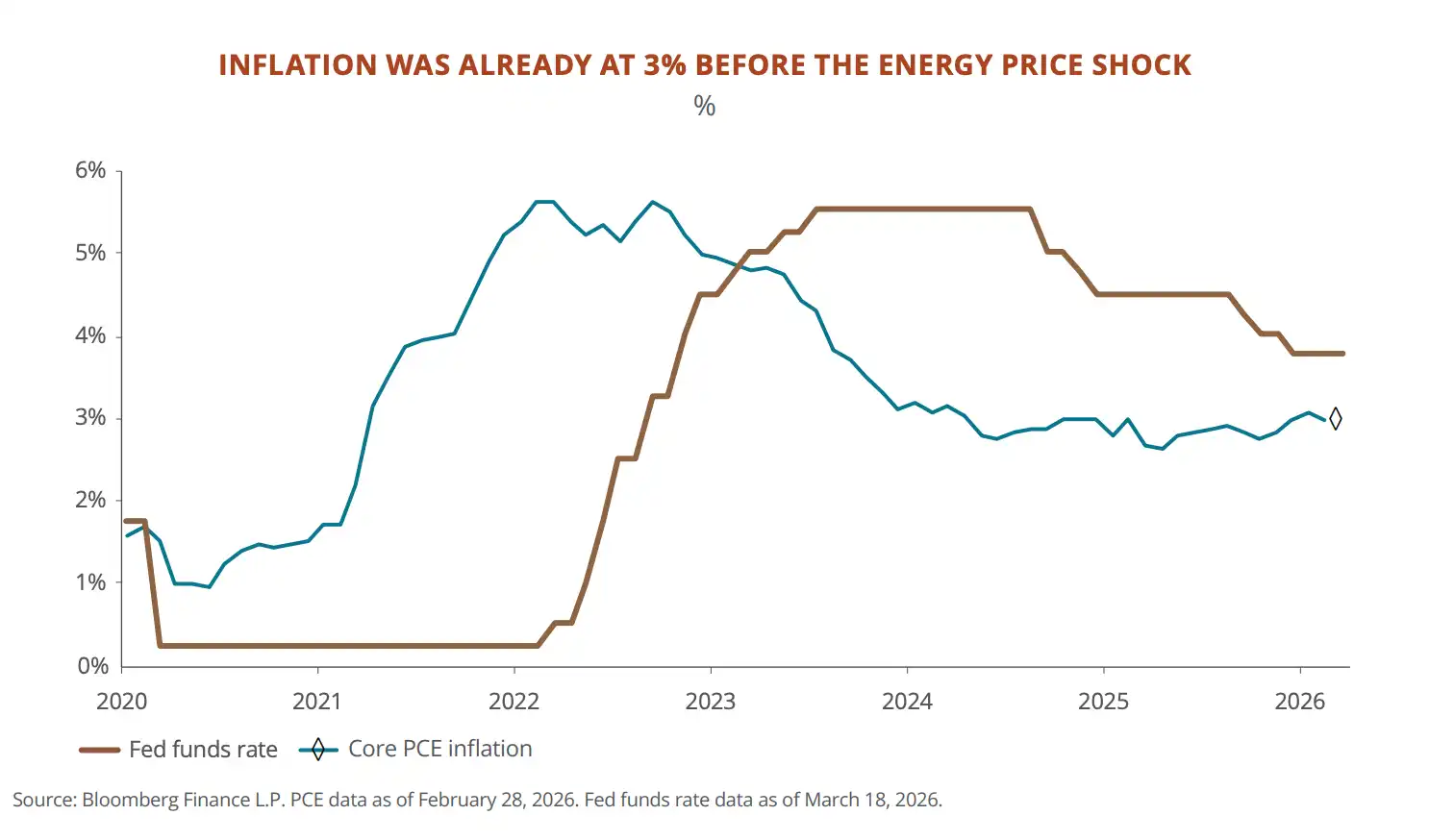

4. The inflation floor is higher than pre-pandemic; cash is slowly bleeding value.

US core PCE was already sticky at around 3% before the energy shock. Consumer prices have cumulatively risen 25% since 2020, while core fixed income has only returned 6%. Nearly 20% of JPM's clients' assets are in cash and short-term bonds. The report's message is clear: you think you're taking shelter, but you're actually losing money.

5. The Strait of Hormuz blockade is the largest oil supply shock since WWII, but JPM believes you should buy the dip.

Oil prices have nearly doubled, US stocks experienced a roughly 10% correction, and the S&P 500's P/E briefly fell below 20x. JPM's historical data shows that buying after the VIX breaks above 30 yields a 70% to 83% probability of positive returns within 6 months, with an average return of 12.4%.

6. Emerging markets could be an opportunity in the second half.

EM corporate earnings are expected to grow 46%, with a P/E of only 11.8x. Taiwan and South Korea are core nodes in the AI hardware supply chain. Latin America holds over 40% of the world's copper and nearly 60% of its lithium reserves. The discount of Chinese stocks relative to other Asian markets is at its deepest in 20 years, and JP's stance is "cautiously warming."

On AI: The Market is Pricing a "Peak," JP Morgan Thinks It's Too Early

JPM opens by stating that Wall Street's narrative on the AI supercycle has "already become too pessimistic."

Core data supporting this judgment:

- Microsoft, Meta, Oracle, Google, and Amazon, the five cloud giants, have a combined 2026 capital expenditure expectation exceeding $650 billion. GPU (core chips for training AI models) cloud rental prices have risen 40% since last October, indicating supply still lags demand. Nvidia's stock trades at a 40% discount to its average P/E over the past decade. The market is pricing in "chip sales peaking," but cloud business revenue is still accelerating.

Simultaneously, the financial characteristics of these five companies are changing. Free cash flow is projected to drop from $240 billion in 2024 to $73 billion by end-2026, Microsoft's P/E has fallen from an AI-era high of 35x to 22.5x. The light-asset model that attracted investors over the past decade is being rewritten by heavy capital investment. JPM believes the focus at this stage should be on revenue growth rather than cash flow, but this also means that once demand slows, these investments could become a drag.

A few other judgments on AI serve as localized risk warnings within the larger trend:

Traditional software companies are the first real victims of AI. About half of the constituents in the US software sector index have fallen more than 50% from their highs, with a median operating profit margin of only 4%. The logic of the impact is simple: SaaS (subscription software) charges per head, AI reduces heads. This has already transmitted to the lending market, with about 21% of money in the US direct lending market lent to software companies, and publicly traded tech-focused loan fund prices falling close to the lows of the last cycle. JPM's stress tests show potential leveraged losses could reach 4% in extreme scenarios, but it does not yet constitute a systemic risk.

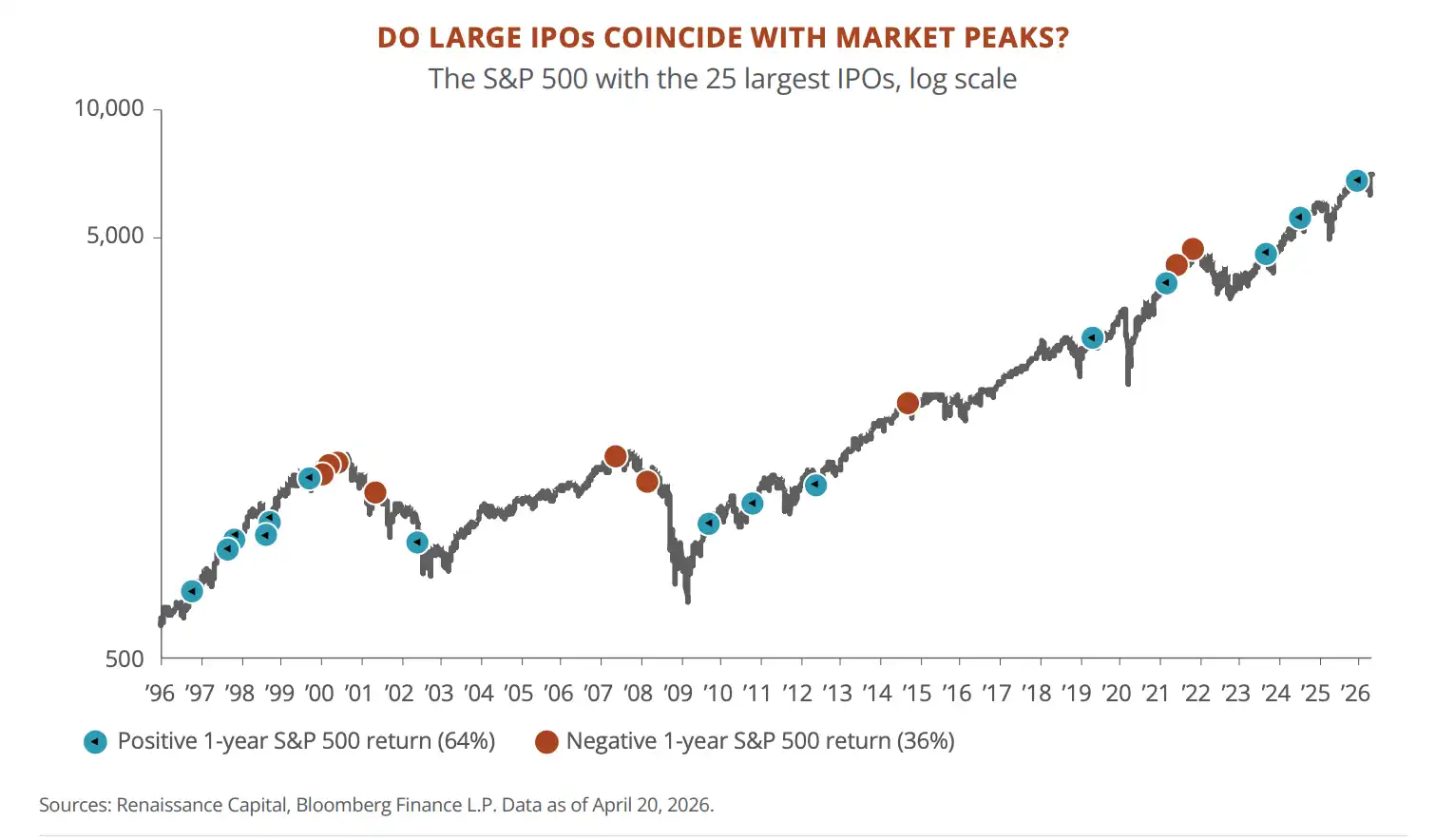

SpaceX, Anthropic, and OpenAI might crowd into IPOs this year, which historically is not a good sign. Following the 25 largest IPOs in the past, the median new stock underperformed the market by 30 percentage points in the first year, with 12 out of 18 falling in their first year. In years with mega IPOs, the median annual market return was only 3%, far below the long-term average of 10%. JPM doesn't say it's definitely a peak, but it is clearly watching the market reaction to SpaceX's IPO as a cycle thermometer.

On Inflation: Inflation Won't Return to 2%, Your Cash and Bonds Are Losing Money

The key point in the inflation section is not that the Strait of Hormuz has pushed up oil prices, but that US inflation hadn't returned to normal even before oil prices were pushed up.

In January 2026, core PCE was at 3.1% year-on-year, with particularly solid increases in local service categories like dining and personal care. Then oil prices doubled. The Fed's model shows that for every $10 increase in oil prices per barrel, inflation rises by about 0.3 percentage points; this time it's a $40 increase.

JPM believes a full 1970s-style replay is unlikely. The labor market isn't showing a wage-price spiral, the quit rate is declining, housing inflation has dropped from over 5% at the end of 2024 to just over 3%, and China's overcapacity is also suppressing global goods prices. However, the inflation floor is a notch higher than pre-pandemic, likely oscillating around 3%.

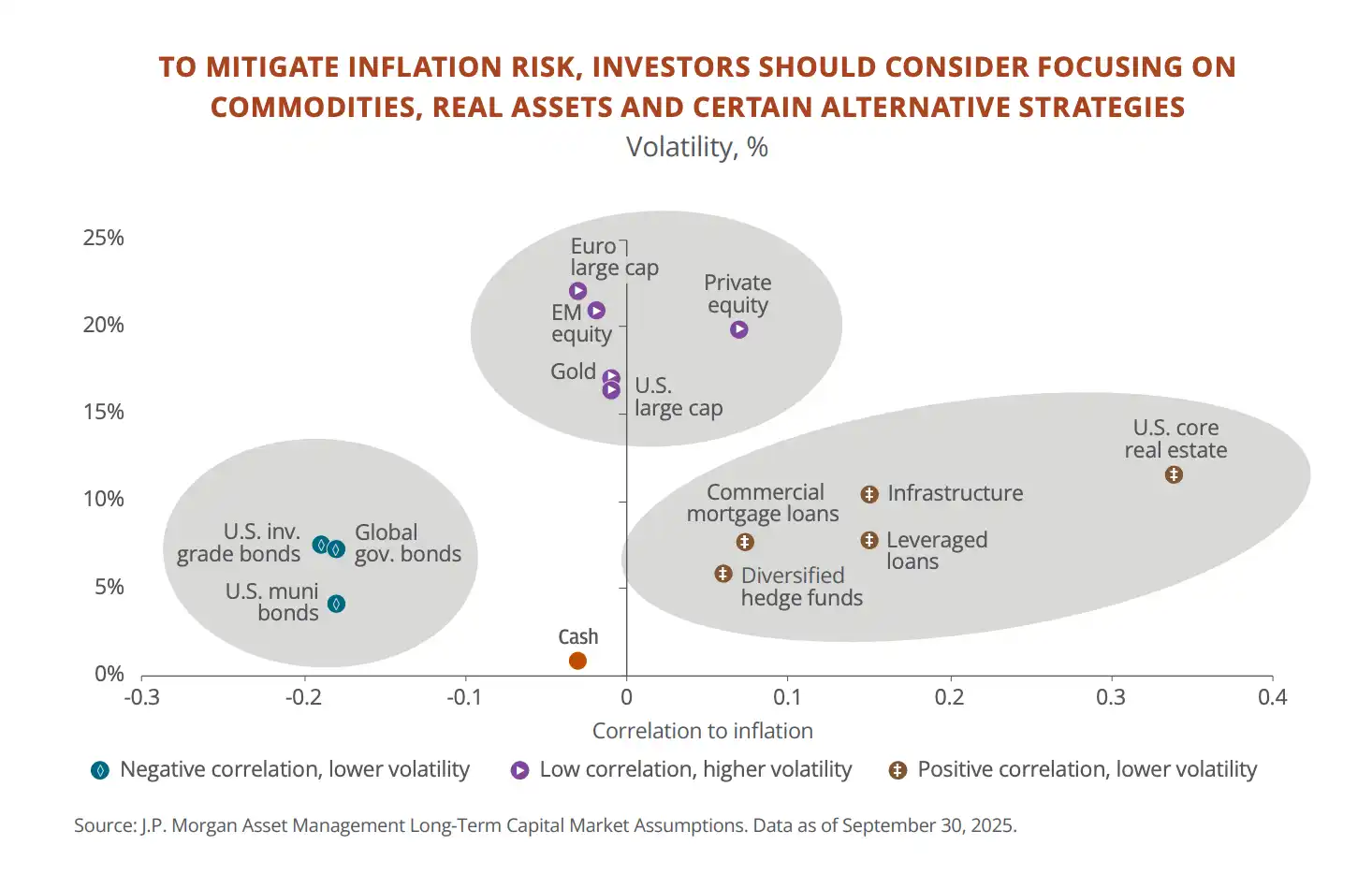

JPM's proposed countermeasure is to increase allocation to real assets.

Since 2020, US prices have cumulatively risen 25%, while bonds have only returned 6%, and cash even less. You think your money is sitting still, but it's actually shrinking every year. Among JPM's own clients, nearly 20% of assets are still in cash and short-term bonds.

Therefore, its suggestion is to move some money into assets that are linked to inflation:

- Commodities, infrastructure, real estate—things that rise with prices—are suggested to be allocated around 5% of the portfolio in total.

- Gold is separately suggested at 3% to 6%.

- Then there are hedge funds. In 2022, when stocks and bonds fell together, macro strategy hedge funds gained 9%. However, JPM also acknowledges that 94% of its private banking clients have never bought hedge funds, and 86% haven't bought infrastructure-like products.

To sum up this section in one sentence:

Inflation may not spiral out of control, but it won't return to 2%. If your portfolio is still the traditional 60/40 stock/bond mix with a pile of cash, JPM thinks you're preparing for a world that no longer exists.

On Geopolitics: Chinese Equities May Be Poised for Structural Revaluation

This section covers the most diverse content, from Middle East conflicts to US-China competition to Europe's troubles. We'll only focus on what directly relates to investment decisions.

1. The Strait of Hormuz blockade is the biggest market shock of the first half of this year. About 20 million barrels of oil pass through this chokepoint daily, accounting for one-fifth of global oil consumption. After the US-Israel joint strikes on Iran, oil prices nearly doubled within days, and European natural gas prices rose nearly 100% in two days. QatarEnergy's CEO said 15% of LNG (liquefied natural gas) capacity could be offline for up to five years. Qatar also supplies about 30% of the world's helium, essential for chip manufacturing, and South Korea has warned of potential chip factory shutdowns.

JPM believes the conflict is moving towards de-escalation, but physical damage and energy risk premiums won't disappear quickly.

Therefore, their advice to investors is: Use the pullback to add to US equity positions.

US stocks fell about 10% in the first half, with the S&P 500 P/E briefly falling below 20x. Historically, buying after the VIX (fear index) breaks above 30 yields a 70% to 83% probability of positive returns within 6 months, averaging a 12.4% gain.

2. The US and China are each building their own ecosystems, and markets may accelerate into two camps. The US is restricting chip exports to China, teaming up with the Netherlands and Japan to control semiconductor equipment. China is expanding exports to non-US markets, with Belt and Road investment hitting a record high in 2025, investing $53 billion in Brazil in one year, and its trade volume with Latin America already exceeds that with the US. JPM's judgment is that future investment returns may increasingly depend on which camp your assets belong to, not just the company's own growth.

But fragmentation is also creating opportunities, especially in emerging markets.

JPM lists several directions:

- Latin America holds over 40% of the world's copper and nearly 60% of its lithium, along with abundant nickel, rare earths, and agricultural resources. Foreign direct investment has doubled in the past two decades, central banks' ability to control inflation is stronger than in developed countries, and politics are shifting towards more pragmatic, business-friendly governments.

- Middle Eastern Gulf countries are using oil revenues to build AI data centers. Saudi Arabia partnered with Blackstone on a $3 billion data center project, with costs 30% lower than in the US.

- East Asia (Taiwan China, South Korea) controls key nodes in the AI hardware supply chain. If AI capital expenditures continue to accelerate, these economies' exports and pricing power will further strengthen.

- Chinese equities are at their deepest discount relative to other Asian markets in 20 years; 80% of Chinese consumers are excited about AI products (38% in the US), and electricity costs are about half of those in the US. JPM's stance is "cautiously warming." If policy signals become more clearly business-friendly, Chinese equities may be poised for structural revaluation.

In contrast, Europe is the market where JPM is most conservative. Electricity prices are two to four times those in the US, R&D spending as a share of GDP is only 2.2% (US 3.6%, South Korea 5.2%), and venture capital scale is one-tenth that of the US.

The energy shock is also forcing the ECB to potentially consider re-tightening. In Europe, JPM only recommends buying defense and infrastructure-related stocks, avoiding autos and consumer sectors.

What JPM is Betting On, and What It's Not

Condensing a 60-page report into one sentence: Volatility is an entry opportunity, but the entry stance must change.

What You Should Bet On:

- AI infrastructure chain (chips, optical modules, power), emerging market equities and bonds, real assets (commodities, infrastructure, gold), defense-related stocks, Chinese AI concepts (cautious addition).

What You Should Not Bet On:

- Cash, traditional subscription-based software companies, European autos and consumer sectors, and relying solely on a traditional 60/40 stock/bond portfolio model to navigate the second half of this year.

Link to the original research report:

https://www.jpmorgan.com/content/dam/jpmorgan/documents/wealth-management/mid-year-outlook-2026.pdf

This article is Tide Research's compilation and interpretation of J.P. Morgan Wealth Management's Mid-Year Outlook Report 2026. The judgments and recommendations cited in the article are the views of JPM and do not represent the stance of Tide Research, nor do they constitute any investment advice.

Sell-side reports are inherently bullish; JPM is also an investment banking services provider for many of the mentioned companies. The value of the report lies in its framework and data, not in any single conclusion. Look at the logic, not just the direction.

The market carries risks; decision-making should be independent.

Data sources: J.P. Morgan Wealth Management Mid-Year Outlook 2026 · Bloomberg · FactSet · U.S. Bureau of Labor Statistics · IEA · METR · Renaissance Capital

Tide Research · 2026 June 4