SpaceX is preparing for an IPO that could rewrite the record books of the capital markets.

The company plans to issue approximately 556 million shares at $135 per share, raising about $75 billion, corresponding to an overall valuation of approximately $1.75 trillion. If the listing is completed successfully, this would become one of the largest IPOs in history, placing SpaceX directly among the highest-valued companies in the U.S. on its first day of trading.

Given SpaceX's achievements over the past two decades, such intense market attention is not difficult to understand.

The company has dramatically reduced the cost of commercial launches with its reusable rockets, built the world's largest satellite internet constellation, and turned Starlink from a technological experiment into a real source of revenue and profit. In the global commercial space sector, SpaceX has almost no comparable peers in the true sense.

However, as this IPO gets closer to realization, the voices of skepticism in the market have become more concentrated.

These doubts do not mean investors deny SpaceX's technical capabilities, nor do they imply the market thinks Starlink lacks value. What truly triggers the FUD (Fear, Uncertainty, Doubt) is the company's expectation that the public markets accept, all at once, an extremely aggressive pricing logic:

Today's investors not only need to pay for the rockets and satellite network, but also need to pay a premium upfront for AI infrastructure, orbital data centers, the next-generation Starship, and the longer-term space economy.

The market is not worried that SpaceX has no future, but that too much of that future has already been priced in.

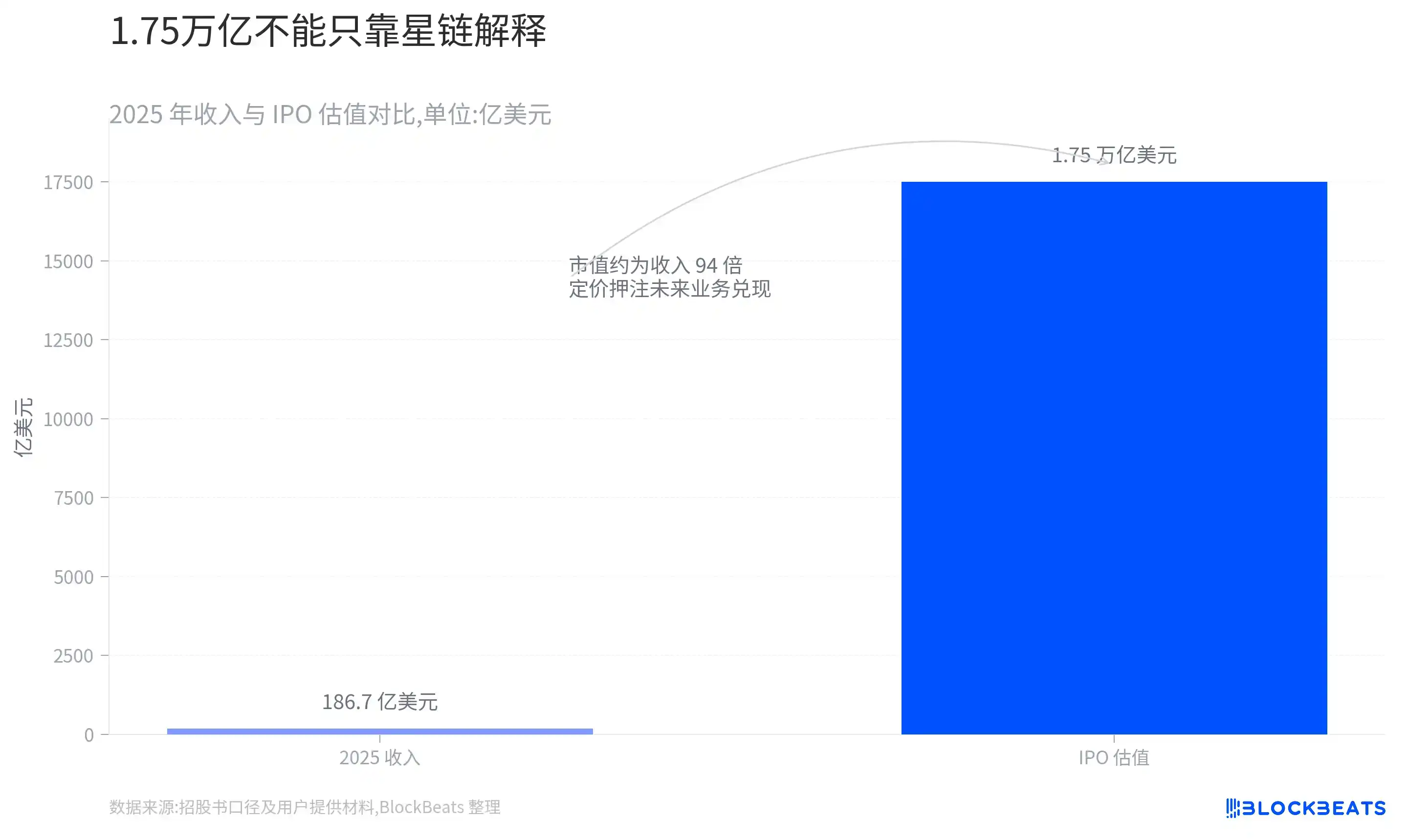

A $1.75 Trillion Valuation Can No Longer Be Explained by Starlink Alone

The most direct controversy surrounding this SpaceX IPO stems from its valuation.

In 2025, the company's revenue was approximately $18.67 billion, a year-over-year increase of 33%, but it still reported a net loss of about $4.94 billion. Based on the $1.75 trillion valuation, SpaceX's market capitalization is nearly 94 times its previous year's revenue.

This multiple does not necessarily mean the company is overvalued. SpaceX possesses infrastructure with exceptionally strong scarcity, and its business structure is also difficult to simply compare with traditional aerospace, telecommunications, or technology companies.

The problem is that when the valuation reaches $1.75 trillion, it's already hard to fully explain the market price based solely on existing businesses.

If investors view SpaceX solely as a rocket launch and satellite internet company, the current valuation appears very aggressive; the pricing logic only holds water if the market simultaneously believes that AI, orbital data centers, next-generation satellite networks, and longer-term space infrastructure can become real revenue sources.

This is also why the grand vision outlined in SpaceX's prospectus has become the starting point for market debate.

When a company's valuation needs to be explained by businesses that have not yet matured into commercial models, the market naturally applies a higher risk discount.

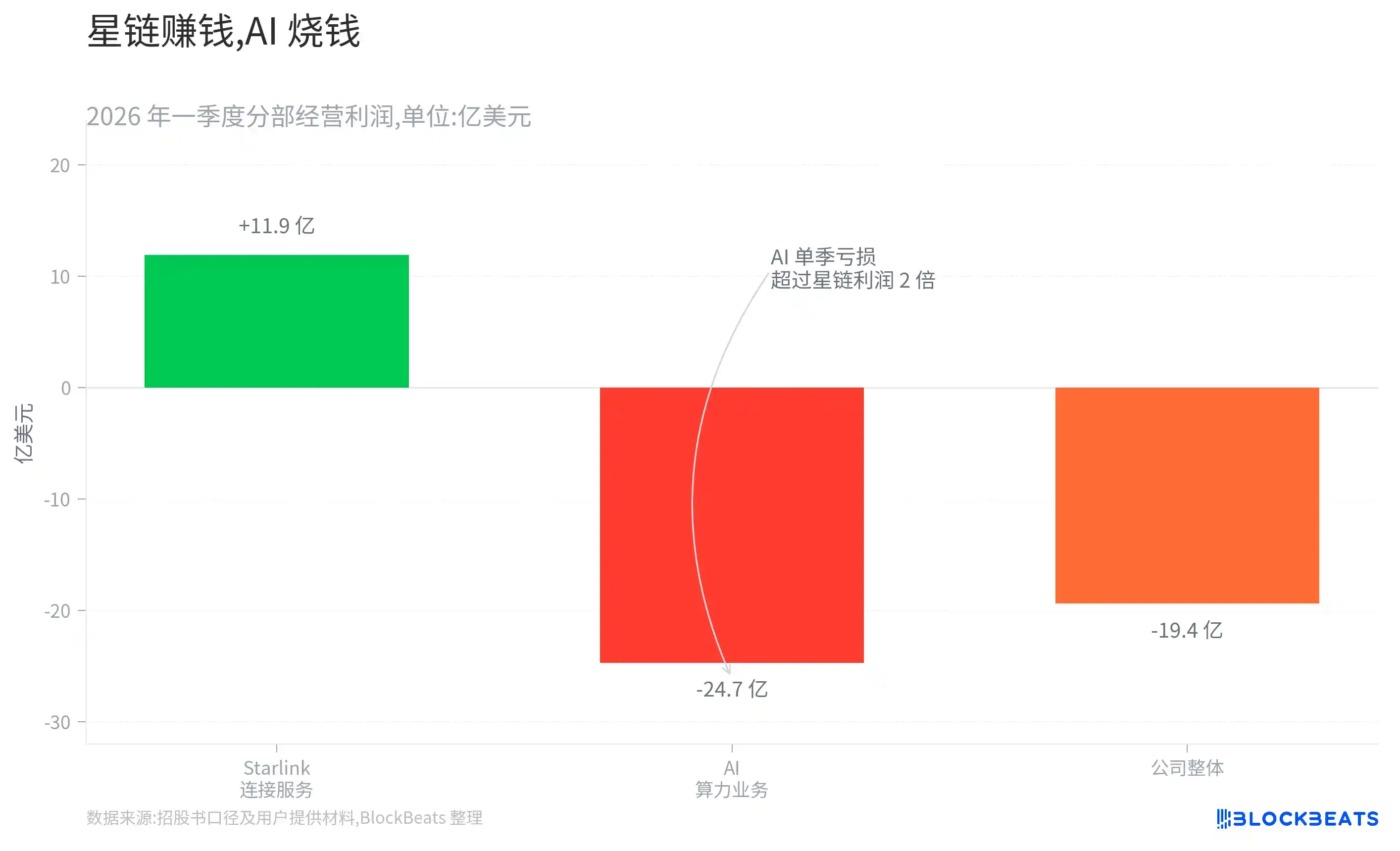

Starlink Makes the Money, AI Burns It

If we temporarily set aside Mars, orbital data centers, and deep-space transport, SpaceX's current financial structure is actually quite clear.

In the first quarter of 2026, the company generated revenue of approximately $4.69 billion but reported an operating loss of about $1.94 billion. Among its three major business segments, only the Connectivity Services segment, centered on Starlink, was profitable, with quarterly operating profit of about $1.19 billion. The AI segment's revenue was approximately $818 million, yet its operating loss reached about $2.47 billion.

Meanwhile, SpaceX's capital expenditures are accelerating noticeably. The company's capital expenditure in the first quarter was approximately $10.1 billion, with 76% flowing into AI-related businesses.

This means that SpaceX's most stable source of profit remains Starlink, while the company's most aggressive capital investment is currently flowing into AI.

This model is not without rationale. AI infrastructure itself is an industry that requires massive upfront capital investment; data centers, power, chips, and network equipment cannot be recouped in a short period.

But what the market is truly worried about is:

Is Starlink's profit being funneled into a new business that requires continuous cash burn, yet whose return cycle remains unclear?

If AI can gradually form stable revenue and profit streams, these investments will be viewed as forward-looking positioning.

Conversely, if the AI business remains stuck in the heavy-asset compute leasing stage for a long time, SpaceX's valuation logic will come under pressure. Because what the market ultimately needs to see is not just revenue growth, but whether profits can keep pace with the speed of capital investment.

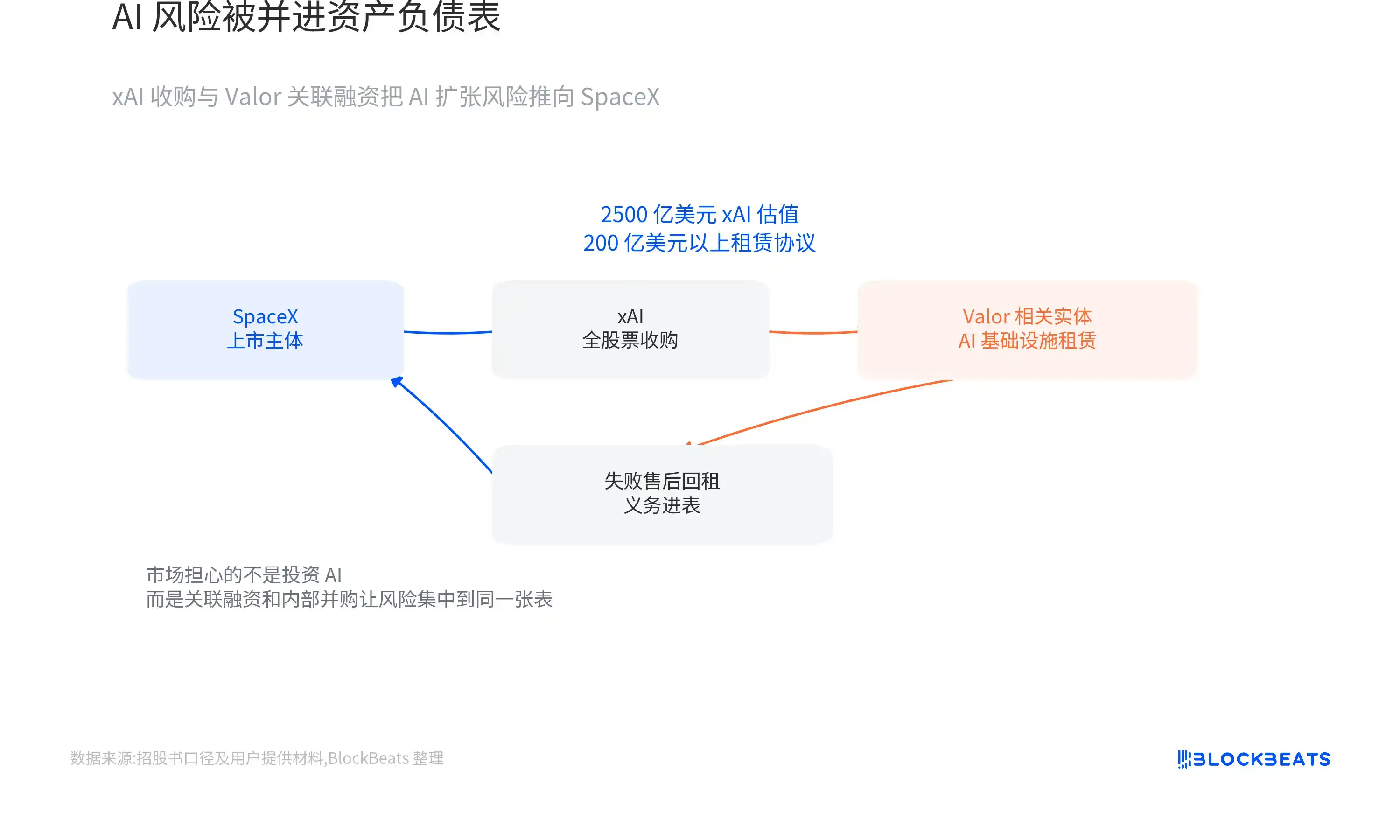

After Acquiring xAI, SpaceX Also Inherited the Risks of AI Expansion

SpaceX's AI investment is more complex than just increasing capital expenditures.

In February 2026, SpaceX acquired xAI in an all-stock transaction. The transaction valued SpaceX at approximately $1 trillion and xAI at approximately $250 billion, resulting in a combined valuation of approximately $1.25 trillion.

Strategically, this deal is not hard to understand. SpaceX possesses rockets, satellite networks, and potential orbital infrastructure, while xAI has Grok, large data centers, and an AI business. Combining the two provides a more complete framework for the narrative around orbital data centers and space-based computing.

But from a financial perspective, what SpaceX took on wasn't just the growth potential of AI, but also the capital pressures behind AI expansion.

The prospectus discloses that xAI-related subsidiaries have entered into AI infrastructure lease agreements exceeding $20 billion with entities related to Valor Equity Partners, involving GPUs and data center hardware. Valor founder Antonio Gracias is concurrently a SpaceX director and a long-time business partner of Elon Musk.

Among these, some transactions, due to failing to meet the accounting recognition criteria for normal sale-leasebacks, were classified as "failed sale-leasebacks." This means the corresponding obligations need to be recorded as debt on SpaceX's balance sheet, rather than simply treated as lease expenses.

Reducing the upfront cash pressure of data center construction through leasing and financing arrangements is not uncommon in itself. What genuinely triggers market concern is that the financing party is not a completely independent third party, and both the buyer and seller in the xAI acquisition are controlled by Musk.

This makes two questions hard to avoid:

Is xAI's $250 billion valuation reasonable?

Are the terms of the related-party financing transactions sufficiently transparent?

The market isn't worried that SpaceX is starting to invest in AI, but that the debt, financing arrangements, and execution risks of the AI business are entering the listed company's balance sheet through internal M&A and related-party transactions.

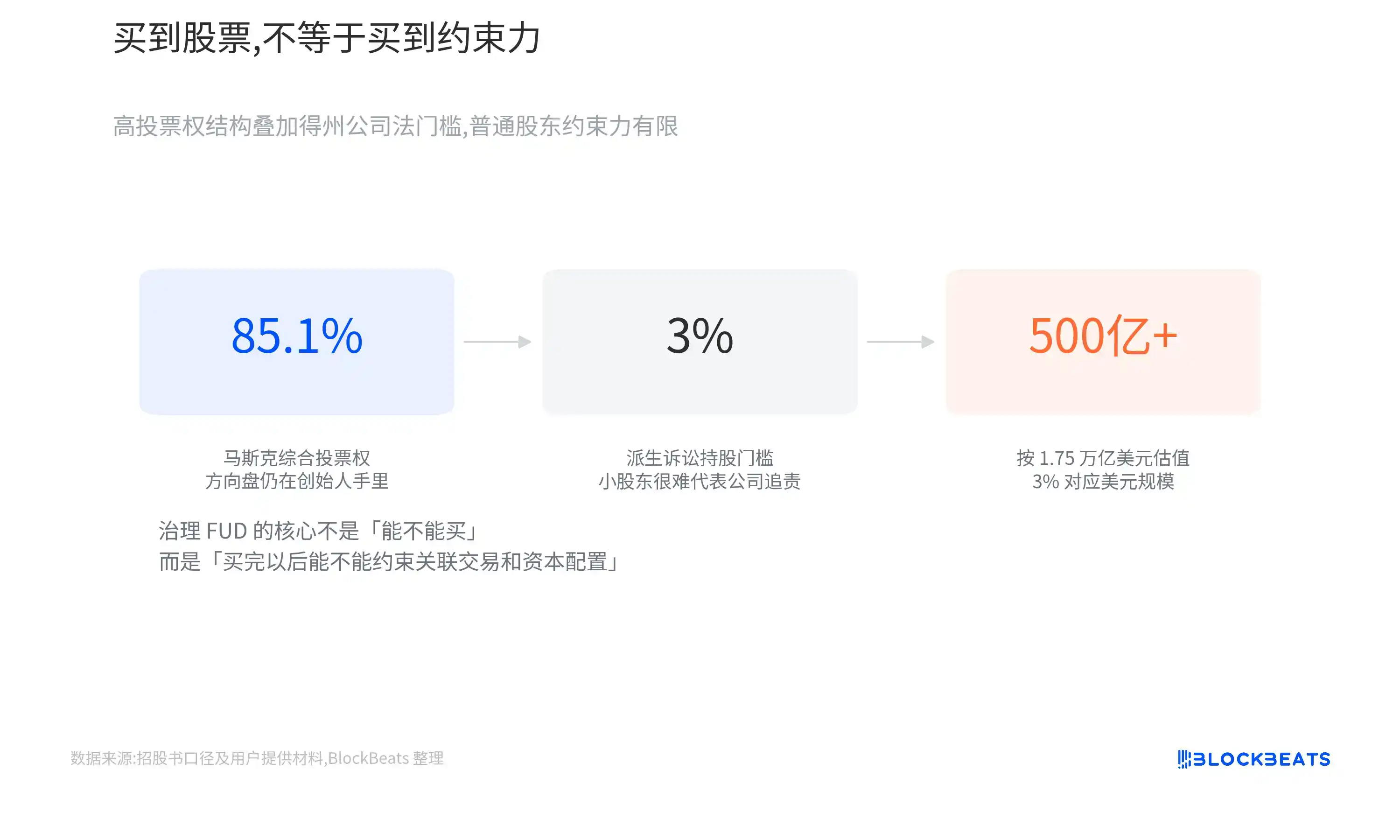

Texas corporate law further amplifies this concern. SpaceX is incorporated in Texas, and relevant laws allow public companies to raise the ownership threshold for shareholder derivative lawsuits and restrict shareholder access to certain emails, text messages, and electronic communication records. For a SpaceX valued at approximately $1.75 trillion, a 3% equity stake corresponds to a value exceeding $50 billion.

This does not mean ordinary shareholders cannot sue the company under any circumstances.

But it means that if investors believe related-party transactions have harmed the company and wish to challenge directors or executives on the company's behalf, the practical hurdle is very high.

As corporate boundaries become increasingly blurred, what the public market assumes is not just business risk, but also the capital allocation risk of Musk's entire business ecosystem.

Investors Can Buy Growth, But It's Hard to Influence Decisions

The governance issue is important because SpaceX is about to become a public company, yet the influence ordinary investors can exert is very limited.

SpaceX employs a dual-class share structure. Musk will maintain absolute control through high-voting-power shares. Even if future capital allocation disputes, related-party transaction controversies, or strategic direction disagreements arise, ordinary shareholders will find it very difficult to change the outcome through the voting mechanism.

This structure is not uncommon. Many tech companies use dual-class designs to prevent founders from losing control after going public.

But what makes SpaceX special is that the company will still need to make numerous high-risk, long-cycle, and capital-intensive decisions in the future. What investors need to accept is not just lower voting power, but a more extreme governance premise:

The company can continue to channel substantial resources into Starship, AI, and orbital infrastructure, even if these projects cannot generate profits in the short term, and ordinary shareholders will have little ability to alter the strategic direction.

For long-term investors bullish on Musk, this structure may not be a problem. SpaceX's past success was itself built upon the founder's极强的个人决策能力和风险偏好 (exceptionally strong personal decision-making ability and risk appetite).

But for investors who place greater emphasis on governance transparency, it means something else:

Investors need to bear the long-term execution risk, yet have little real ability to constrain management.

Starship is a Technical Project and a Valuation Variable

Market concerns about SpaceX are not solely concentrated on AI and governance structure.

Whether it's the next generation of Starlink satellites, orbital data centers, or Mars transport, all ultimately depend heavily on the same foundational infrastructure: Starship.

The significance of Starship is not just building a bigger rocket. It needs to significantly reduce per-launch costs, increase payload capacity per launch, and ultimately achieve high-frequency, reusable commercial launches.

Only when Starship truly enters the scaled operational phase will SpaceX have the potential to deploy the next-generation satellite network at lower cost, send larger-scale equipment into orbit, and create realistic conditions for orbital computing infrastructure.

This is also why every Starship test is not just space news; it also influences how the market interprets SpaceX's long-term valuation.

SpaceX's valuation doesn't just depend on whether Starship can fly, but on whether it can fly like an infrastructure tool—stably, at low cost, and with high frequency.

What Exactly Is the Market's FUD Worried About?

Putting several data points together yields a framework more complete than "Is SpaceX overvalued?": Starlink has already demonstrated commercial value, reusable rockets have established a clear competitive moat, and AI and orbital data centers provide the company with new growth avenues.

But at the same time, the company's valuation has reached $1.75 trillion, the AI segment is still posting heavy losses, capital expenditures continue to expand, related-party financing and internal M&A are blurring business boundaries, and the governance constraints ordinary shareholders can exert are very limited.

These facts can all be true simultaneously, and they are not mutually contradictory.

Because the FUD surrounding SpaceX is not a denial of the company's past achievements.

Rather, it's this:

When Musk places Starlink, rockets, AI, and future orbital infrastructure into the same valuation model, for which possibilities is the public market willing to pay a premium, and for which uncertainties should it retain a discount?