Written by: Gao fei

Compiled by: AididiaoJP, Foresight News

In 1987, the economist Robert Solow famously said, "You can see the computer age everywhere but in the productivity statistics." This statement puzzled economists for nearly a decade. It wasn't until the mid-1990s that the contribution of computers to productivity finally appeared in the data.

In 2026, the same perplexity is replaying with AI. Bubble theories come and go, scholars debate endlessly, enterprises hesitate, and macroeconomic signals remain ambiguous. But there is one place where the impact of AI on the economy is already beyond debate.

Now, let's look at Stripe.

Over the past few days, I attended Stripe Sessions in San Francisco. Stripe processes transaction volume equivalent to nearly 2% of global GDP, with annual payment volume reaching $1.9 trillion and over 5 million businesses on its platform. Eighty-six percent of companies on the Forbes AI 50 list use Stripe. If the AI economy is a newborn baby, then Stripe is the heart rate monitor in the delivery room. It records the baby's heartbeat earlier and more precisely than almost anyone else.

A study released by the St. Louis Fed in early 2026 shows that AI-related investments have contributed nearly 40% to marginal U.S. GDP growth, surpassing the peak contribution of the tech industry during the dot-com bubble. When these investments translate into revenue, most of the settlement happens on Stripe. More importantly, Stripe isn't just recording the heartbeat of the AI economy. At this year's conference, it announced its intention to drive a new economic form: Agentic Commerce, where agents become the subjects of transactions. In a collective media interview, co-founder and president John Collison stated that he expects agents acting as buyers in commercial transactions to become mainstream within 12 to 18 months.

Two days, 288 product and feature announcements, over 10,000 attendees, and one defining phrase ran through it all: Agentic Commerce. Here is what I saw at Stripe Sessions 2026, along with my personal reflections.

How Fast is the AI Economy Really Running?

Before discussing Agentic Commerce, let's look at the overall outline of the AI economy. When Solow said in 1987 that computers were invisible in statistics, nearly forty years later, AI is clearly visible in Stripe's data.

On the morning of the first day, CEO Patrick Collison presented a set of data. Since the pandemic, the number of new businesses formed monthly on Stripe has remained high but the curve has been relatively flat. Starting from early 2026, this curve has shot almost vertically upward. The direct reason is that AI coding tools have dramatically lowered the barrier to starting a business, with many developers now using "vibe coding" to create chargeable products in days. Patrick described it as a broader phenomenon—the entire economy is being replatformed around AI. Stripe's head of AI revenue, Maia Josebachvili, added an external comparison: until 2024, the number of app releases on the iOS App Store had been declining. After the emergence of AI coding tools, releases grew 24% month-over-month.

The change is not just quantitative but also qualitative. Stripe Atlas is one of the simplest ways for founders to register a U.S. company, having just celebrated its 100,000th incorporation last week. At the conference, I heard a staggering statistic: companies registered through Atlas in 2025 generated double the revenue at the same point in their lifecycle compared to companies from 2024. Companies from 2026, only a few months old, are already generating five times the revenue of companies from the same period last year.

In the AI Economic Report on the first afternoon, Maia Josebachvili listed several names driving the rise of the AI economy. Lovable reached $100 million in revenue in eight months, then surged to $400 million in the next eight months. Cursor achieved $1 billion in annualized revenue in less than two years, then doubled to $2 billion in three months. Leading AI-native companies on Stripe grew 120% in 2025 and have grown 575% so far in 2026.

Growth on the consumer side is equally steep. The highest-spending users spend $371 per month on AI products, exceeding what the average American spends monthly on internet access, streaming, and phone bills combined. I roughly calculated my own monthly token expenses, which have long surpassed my phone bill.

Patrick also drew a comparison: businesses on Stripe are growing 17 times faster than the global economy.

On the second day, John Collison directly referenced the Solow Paradox, explaining it with a historical analogy. In 1882, Edison lit the first customer electric lights in Manhattan. But during the subsequent thirty years of electrification, productivity hardly improved. The reason wasn't that electricity didn't work, but that factories were designed around steam engines. Productivity gains only appeared after entire factories were rebuilt. John's judgment is that AI is at a similar stage. Change is already happening, but the old models haven't fully absorbed it yet. "However," he said, "I suspect AI won't take thirty years."

Stripe's data seems to support his optimism. On its platform, the AI economy is already exploding. Almost every traditional company I've interacted with is pushing AI deployment with extreme urgency at the highest leadership levels.

Global from Day One

Besides speed, another impressive characteristic of these AI companies is that they are global from day one. Stripe has a term for this: global by default.

Since I became an AI blogger myself, I've often encountered this experience: AI content creation has no time zones. AI news from the other side of the Pacific carries the same weight as local news. The same goes for AI products. Large language models blur the interface languages and interaction habits traditional software relies on. A unified chat window allows global users to use products through natural language. In this sense, large language models make a unified global software market possible for the first time.

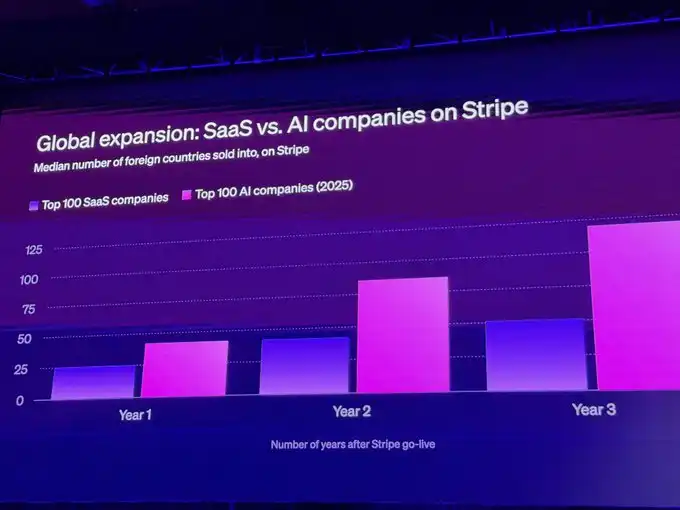

Conference data confirmed this observation. In the previous SaaS wave, the fastest-growing companies covered about 25 countries in their first year and 50 by their third year. AI companies have a completely different rhythm: 42 countries in the first year, 120 by the third. Maia said Kazakhstan now appears on the market lists of many AI companies. In the "Indexing the Economy" breakout session on the second day, Stripe gave a median: the top 100 AI startups are already selling to 55 countries in their first year.

Emergent Labs is a concrete example. The company was founded in the U.S. in 2024, but nearly 70% of its revenue already comes from overseas, with at least 16 countries each contributing at least 1% of revenue. Among leading AI companies, 48% of revenue comes from outside their home market. Three years ago, this figure was only 33%. Global revenue is no longer supplementary; it's the baseline.

Speed and globalization are two core characteristics of the AI economy, and both are directly relevant to Stripe. AI companies need to quickly establish payment capabilities; they need to be able to receive payments in 40 countries and regions within their first week. This is precisely what Stripe has been doing since its founding.

Here, a bit of Stripe's founding background is necessary.

Stripe's founders, Patrick Collison and his younger brother John Collison, are Irish; they themselves were cross-border entrepreneurs. At the conference, I met an Irish colleague who told me that in the eyes of Irish AI founders, these two brothers are heroes. After arriving in the U.S., they found online payment collection extremely difficult: connecting a payment system required signing contracts with banks, undergoing PCI compliance reviews, and integrating multiple intermediaries—a process that could take weeks or even months.

So in 2010, two men in their early twenties dropped out of college, moved to San Francisco, and wrote a solution allowing developers to collect payments with seven lines of code. These seven lines of code coincided with the rise of mobile internet and SaaS. Shopify needed to help millions of merchants collect payments, Uber needed frictionless payments for passengers, Salesforce needed to handle global subscriptions... they all chose Stripe. Growing alongside these global clients, Stripe built local capabilities in 46 countries, covering 195 markets and supporting 125 local payment methods.

To consumers, Stripe is not the company in the spotlight. It hides behind Shopify checkout pages, OpenAI subscription confirmation emails, and Uber fee notifications. But this invisibility hasn't stopped it from becoming the underlying financial pipeline of the internet economy. In the AI era, this global financial infrastructure gives Stripe a first-mover advantage in serving AI companies expanding internationally.

At this year's conference, I also met Stripe's global head of product, Abhi Tiwari. He took on this role just three months ago and moved to Singapore. Stripe has engineering hubs in San Francisco, Dublin, and Singapore, and has also set up a Latin America office in São Paulo. Abhi told me that when many AI companies approach Stripe, their first sentence is often: "We are global by default; where users are doesn't matter." The old model of developing products at headquarters and then pushing them globally is being replaced by a new model where local teams build in their markets.

Reaching global users is one thing; getting them to pay is another. The latter is much more complex because each market has its own currency and payment habits. In this regard, Stripe helps AI companies and other customers mainly in two ways: local currency pricing and connecting local payment methods. The former shows Brazilian users prices in Brazilian Reais rather than U.S. dollars, increasing cross-border revenue by 18%; the latter allows Indian users to pay with UPI and Brazilian users with Pix, boosting conversion rates by over 7%. The AI presentation tool Gamma saw Indian revenue surge 22% in the month it integrated UPI. At the booth, I also saw the presence of the Chinese company MiniMax. From what I understand, many Chinese companies expanding overseas use Stripe's financial services through overseas entities.

These AI-native companies share another common trait: they have extremely few personnel, many being solo founders. One or two people plus a group of agents can support a global company with real revenue. In Emily's speech on the second day, data showed that the density of solo founders on Atlas is close to 5,000 per million Americans, and more and more of them have annual incomes exceeding $100,000.

Emily used the term "solopreneur." This reminded me of the rapidly developing OPC (One Person Company) wave in China. John used Ronald Coase's theory of the firm to explain this phenomenon. Firms exist because the cost of internal coordination is lower than the cost of market coordination. But AI might be reversing this logic. When agents can help you find services, integrate software, and handle payments, external coordination costs drop dramatically. You no longer need a room full of employees to do what previously required an entire department.

From a Human Economy to an Agentic Economy

The AI economy described above, no matter how fast it grows or how global it becomes, still has humans as the transaction subjects. Humans are buying AI products; humans are starting businesses with AI tools. But the strongest signal I felt at this year's Sessions is Stripe's next major focus: another shift—the economic form where agents become market participants. This is Agentic Commerce.

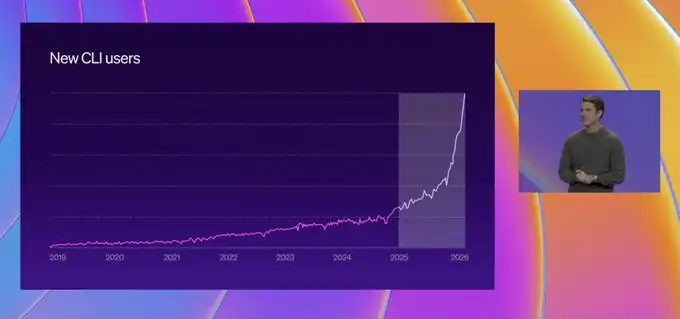

This shift is already quietly appearing in Stripe's own data. Products and business president Will Gaybrick presented a set of numbers. For years, the Stripe CLI (Command Line Interface) was used only by a small group of highly technical users, with usage barely changing. Starting in 2026, usage suddenly exploded. The reason is that agents don't need beautiful graphical interfaces; a clean CLI is often more useful. Maia's data shows that in 2025, traffic from agents reading Stripe documentation grew about tenfold. If the current trend continues, by year-end, agents will read more Stripe documentation than humans. The API documentation that Stripe has spent over a decade refining has found its newest, most loyal readers.

If the idea of agents spending money still sounds unfamiliar, think of two already-occurring scenarios.

The first is that shopping interfaces may be shifting to model chat windows. Consumers now commonly use ChatGPT, Gemini, or Instagram to research products. The distance between research and transaction is compressed into one interface. Relevant cases have also emerged in China, such as buying bubble tea within an AI app.

In the collective media interview, John Collison used his own experience buying a travel power adapter to explain why this compression is hard to reverse. If an agent completes the entire process from research to order placement, and the product arrives at home days later, he wouldn't go to another website to start filling in personal information from scratch, even if that website's product might be slightly better. Once a shopping agent completes the search process, the next natural step is checkout.

The second example is more interesting: OpenClaw. Anyone who followed the "lobster" wave knows it's currently one of the hottest open-source autonomous agent frameworks. Users give instructions to agents through messaging apps like Feishu, Telegram, WhatsApp, etc., and the agents autonomously execute tasks. The key is that OpenClaw can consume hundreds of yuan or even hundreds of dollars in token costs per day. It manages token consumption and usage itself. Although human authorization is still required in many cases, ultimately, it's the agent consuming the tokens, and tokens can be directly converted into money.

From agents managing token consumption to agents directly spending money is only one step away. At this year's conference, Stripe's demonstration crossed that step.

Demo: Agent Buying and Selling

On the main stage on the second day, a demo won multiple rounds of applause.

John Collison gave a simple instruction to an agent on stage: research how AI demand is affecting the energy market. The agent started searching and found that Alpha Vantage had an energy market dataset it needed, priced at 4 cents. The agent judged the price was within budget, then used a stablecoin wallet in the Tempo CLI to autonomously complete the purchase and download, because paying 4 cents with a credit card wasn't cost-effective. Then it generated a complete analysis report. That alone was astonishing. But then John told the agent: "Publish and sell this report. Set a price you think is reasonable so other agents can find and buy it." The agent checked the Alpha Vantage dataset's licensing terms, confirmed commercialization was allowed, then built a website, published the report, and generated an instruction file allowing other agents to purchase the data with a single request.

In just a few minutes, an agent completed the entire chain of research, procurement, production, compliance review, publication, pricing, and sales. It was both a buyer and a seller. After the demo, John said, "Agentic Commerce is already here."

Two other demos on the first day were equally impressive. Will Gaybrick built an API review application that lets agents obtain review services for users. Throughout the process, he didn't tell the agent any payment information. When executing the task, the agent automatically discovered the app used the Machine Payments Protocol (MPP) and autonomously completed a $2 payment. The human only authorized it once with a fingerprint. This zero-configuration ability for agents to discover and complete payments is the core design of MPP as a protocol. Developers don't need to write separate payment logic for agents; agents can find it themselves.

Immediately after, Gaybrick combined Metronome (a real-time metering engine), Tempo (a blockchain designed for payments), and stablecoins to demonstrate streaming payments. An app charged for AI token consumption in real-time, $3 per million tokens. Multiple agents ran simultaneously. A dashboard on the left showed token consumption rising, while micro-payments in stablecoins flowed in synchronously on the right. When opening the Tempo blockchain explorer, a total payment of $3.30 was composed of thousands of sub-cent micro-payments, each only one three-thousandth of a cent. Credit cards can't do this, ACH can't do this, UPI and Pix can't do this. Gaybrick announced on stage that this was the world's first streaming payment business.

The Return of Micro-payments and New Consumption Logic

Shopping through chat windows and OpenClaw are examples of agents spending on behalf of humans. But in the collective interview, Collison made a more ambitious judgment: agents might create entirely new demand.

He believes agents could make a business model discussed for years but never truly viable feasible: micro-payments. Humans aren't good at making extremely granular consumption decisions. Spotify replaced per-song payments with a $9.99 monthly subscription because no one wants to decide if a song is worth 15 cents every time they press play. Agents don't have this cognitive burden. If this judgment is correct, then a whole category of business models that failed due to human cognitive friction might suddenly become viable in front of agents. Maia expressed a similar view in a one-on-one conversation with me. She said she had just spoken with dozens of AI founders, and pricing was the most frequently mentioned topic when discussing agentic commerce.

Every transaction has a buyer and a seller. If the buyer becomes an agent, what should merchants do?

In an interview, I asked Stripe product lead Jeff Weinstein: Humans have a saying, "The customer is always right," and merchants need to please consumers. So how do you please an agent? Jeff's answer was to think of an agent as the best programmer you know. It wants perfect information, structured format, fast readability, and all the context needed for decisions. Human consumers like beautiful images and smooth animations; agents want raw structured data, precise logistics information, and the ability to complete transactions with the fewest steps.

In another conversation, Meta's VP of Product, Ginger Baker, more radically summarized this shift: payments will move from "moments" to "strategies." Human consumption is discrete. You go to a checkout counter, pull out your wallet, swipe a card, and the transaction is done. Agent consumption is continuous. You set a set of rules, like "groceries not exceeding $50 this week," "always prioritize this card," "any purchase over $500 requires human authorization." Then the agent autonomously and continuously consumes within the authorization framework you've set.

Security: Compute is the New Cash

If agents truly become a new type of consumer, they also bring new risks. These risks are fundamentally different from traditional SaaS transaction risks and those faced by human consumers.

During Sessions, I paid special attention to this topic and discussed it with several Stripe executives.

Stripe's head of data and AI, Emily Glassberg Sands, described three rapidly growing fraud patterns. The first is multi-account abuse. The same person repeatedly registers different accounts, each claiming a free tier. According to Stripe network data, one in six AI company registrations involves this type of abuse. The second is malicious consumption during free trials. This is especially deadly for AI companies because each trial burns real inference costs. She gave an example: a partner company's token cost to acquire each paying customer exceeded $500 because converting one customer required 25 free trials, 19 of which were fraudulent. The third she called "dine and dash." Customers heavily consume tokens and then refuse to pay at the end of the month. Emily also quoted a famous line: "Compute is the new cash." When traditional SaaS is abused, the marginal cost is almost zero. But for AI companies, every inference call is a real cost. Stolen tokens are stolen money.

However, there's a particular dilemma here that makes me hesitant. Many AI founders' method of dealing with abuse is to shut down free trials.

Emily said that when she asked everyone who claimed to have "solved" this problem how they did it, she found their solution was simply to remove the free tier. But Jeff thinks this creates another problem. Agents are becoming the primary way new services are discovered. If an agent can't trial a service on its own, it will just skip to another URL. Emily added that if the call to action presented to an agent is "join a waitlist" or "contact sales," the agent will leave immediately. Shutting down self-service registration to prevent fraud might mean handing the most important growth channel to competitors.

Stripe's answer to this dilemma is its fraud prevention system, Radar. Radar's logic is simple: every time a transaction is completed on Stripe, Radar learns from it. Transaction data from 5 million businesses flows into a shared risk identification network. If one company encounters a certain fraud pattern, all companies benefit. Last month, Radar blocked over 3.3 million high-risk free trial registrations across eight high-growth AI companies.

Jeff also proposed a counterintuitive view: agent shopping might ultimately be safer than humans shopping on web pages. Trust verification for human web shopping relies on inference: how long a user stays on a site, whether their click path is normal, etc. Agent transactions can have programmatic authentication. Stripe's Shared Payment Tokens tokenize payment credentials, so agents never touch raw credit card numbers. Users authorize via biometrics and can set transaction limits, time windows, and merchant whitelists. When trust mechanisms shift from inference to verification, the security baseline might actually improve.

Ecosystem, Protocols, and a Piece of History

By now, it should be clear: without a well-functioning ecosystem, Agentic Commerce is impossible. At Stripe Sessions 2026, I met someone from the food industry. He said his purpose for attending was to see if Agentic Commerce could be a new opportunity for his company—that's the seller's perspective.

So this can't be done by Stripe alone; it requires an ecosystem.

Wandering the Sessions exhibition hall for two days, I saw booths for numerous companies across the financial industry chain. Stripe also launched or joined a series of protocols with upstream and downstream partners, connecting different parts of the ecosystem: buyers and sellers, humans and machines, machine and machine. The Machine Payments Protocol (MPP) allows agents to discover and complete payments via HTTP. The Agentic Commerce Suite lets consumers make purchases directly within AI apps from Google, Meta, OpenAI, and Microsoft. The Universal Commerce Protocol (UCP) is a cross-platform commerce protocol initiated by Shopify, joined by Meta, Amazon, Salesforce, and Microsoft. Stripe joined the UCP General Council. A group of companies that are both partners and competitors agreed to co-create a shared protocol because fragmentation would make it difficult for agents to consume seamlessly across platforms, which benefits no one.

Speaking of protocols, I saw a special Stripe partner in the exhibition hall: Visa. In my view, Visa is essentially a protocol platform.

Noticing Visa immediately reminded me of a book I love: "One from Many" by Visa founder Dee Hock. A core theme in the book is how banks, money, and credit cards should be redefined in the electronic age. Money no longer has to be coins and paper; it can also be institutionally guaranteed, network-recorded data flowing globally. In the late 1960s, the BankAmericard issued by Bank of America expanded nationally, and a flood of interstate consumers crashed the old system. Hock realized the problem was organizational. Dozens of competing banks needed to share infrastructure, but existing organizational forms couldn't allow them to both cooperate and compete. He used decentralized design principles to make all banks equal members of the new organization, with Bank of America relinquishing exclusive control of the system. This organization was later renamed Visa.

So two companies from different eras are doing similar things. Is there some lineage between them?

With any agent, the answer is easy to find. Patrick Collison has publicly paid tribute to Hock. After Hock's death in 2022, Patrick called him "a badly underrated innovator" who deeply influenced him and his brother. A clearer signal is the hiring decision: Visa's authoritative academic historian, David Stearns, later joined Stripe.

There's also a detail that will make anyone familiar with payment history smile. On stage, Tempo blockchain CTO Georgios Konstantopoulos showed the validator lineup. One of the names was Visa. The Visa created by Hock is now a participating node in a blockchain network incubated by Stripe. The student built a new network; the teacher became a node within it.

When Patrick traced Stripe's intellectual origins at the conference's opening, he said he started as a Lisp programmer. The core idea of Lisp is "code as data." He translated this into Stripe's own language: "Stripe's fundamental idea is that money is data. When we launched Stripe in 2011, this wasn't the industry's orthodox view." Hock approached the nature of money from organizational theory, concluding that money is merely a "guarantee for the exchange of value." The medium carrying it could be anything. The Collisons approached from programming language, directly equating money with data: data that can be programmed, called via API, and operated by agents. The two said the same thing in different languages. On stage that day, Ginger Baker put it even more bluntly: "Isn't money just another form of digital content?"

If money is data, then the consumers of data will naturally become consumers of money.

Side Plot: Stripe's Content Gene

At this point, the story of the AI economy is nearing its end. But let's take a small detour—Stripe can almost be seen as a peer to content creators.

This company isn't just good at financial services; it's also good at content products. Its publishing brand, Stripe Press, has excellent taste; many know it for publishing "Poor Charlie's Almanack." Its podcast, "A Cheeky Pint," is also distinctive and has a large audience. Google CEO Sundar Pichai, Anthropic CEO Dario Amodei, and a16z co-founder Marc Andreessen have all been on the podcast.

During Sessions, I met Stripe Press senior editor Tammy Winter and designer Pablo Delcan. Tammy joked that "Stripe is a publishing house with a multi-billion-dollar company attached." Pablo Delcan talked about his understanding of taste. He said taste is the result of long-term accumulation; it takes time to settle. Regarding design trends, he believed that without abandoning the concepts of simplicity and clear communication, the new challenge is how to add a degree of complexity through detail and precision.

Speaking of books, Tammy told me that within Stripe Press, the series published for founders and builders is called the "Turpentine" series. These books focus on know-how, tools, techniques, maintenance, and the practical matters that make work function. They aren't abstract theory but aim to help readers solve specific operational problems.

The name comes from a story supposedly about Picasso: when art critics get together, they talk about form, structure, and meaning; when artists get together, they talk about where to buy cheap turpentine. This series wants to be the founder's cheap turpentine. If you think about it, for AI companies going global, Stripe's financial services are another kind of turpentine. You don't have to worry about payments, compliance, or foreign exchange; you can focus on building the product.

This side plot may seem unrelated to the main storyline, but there's a connection at the base level. Stripe also has a magazine called "Works in Progress," whose core question is how the economy grows. Its podcast interviews leaders in the AI economy. Sessions itself, in a way, is like an economics lecture. On the morning of the second day, John Collison spent an entire presentation talking about economic data, Coase's theory of the firm, and the Solow Paradox. I suspect that a financial services company caring so much about economics is precisely because understanding structural economic changes is how it discovers its next product opportunities.

As a podcast enthusiast, when I met John Collison on the first day of the conference, my first question wasn't about finance but about the podcast. I asked him, after interviewing so many different people, is there an underlying question that runs through all the conversations? He thought for a moment and said what he's truly interested in is how these people's companies actually operate, what competitive equilibrium they're in, and how they understand their own businesses.

Coincidentally, there was a small twist at the end of the first day. The scheduled closing fireside chat was Patrick interviewing OpenAI co-founder Greg Brockman, but just before going on stage, the guest changed to Sam Altman. Patrick explained, after all, "AI is a rapidly changing field."

So surprise turned to delight. The entire audience cheered.

The two have known each other for nearly 19 years. Altman was one of Stripe's earliest angel investors when the Collison brothers were still under 20. Because of this, Altman appeared very relaxed throughout the conversation.

Approaching the end, Patrick asked a personal question: why did he invest in two teenagers back then? Altman said he remembered they wanted to build a product solving a problem they had personally encountered, and he also saw that this opportunity could scale because many others needed the same thing.

I think his answer about the podcast and his answer about investment point to the same thing: find real demand, solve real problems. During the conversation, Altman divided OpenAI's transformation into three stages: from a research lab, to a product company, to a "token factory" supplying intelligence to the world. Each stage corresponds to a different mission. Stripe is similar. In 2010, the problem two young Irish men solved was "online payment collection is too hard." Along the way, they solved the same problem for 5 million users. In 2026, they identified a new problem: the customers of these businesses might soon no longer be human.

Holding a podcast in one hand and a publishing house in the other, discussing Coase theory and the Solow Paradox on stage, laying out protocols and APIs in the exhibition hall, Stripe isn't just creating the AI economy; it's also documenting it. At the conference, I had a thought that might sound a bit crazy: Stripe holds transaction data equivalent to nearly 2% of global GDP. It can see where every dollar of AI revenue comes from, where it goes, and how fast it grows. If Solow had such a heart rate monitor back then, perhaps he wouldn't have had to wait ten years to find computers in the statistics.

Maybe one day, Stripe could provide a model for the AI economy. Not a large language model, but a Nobel-level economic model. Who says this is impossible? Just a few years before DeepMind founder Demis Hassabis won the Nobel Prize, who could have imagined it?