声明:本文仅是历史数据的回溯分析,并不构成任何投资建议。

""

春节临近,A股市场已经开启“红包行情”。据报道,截至1月16日,今年两市已有近180只个股累计涨幅超20%,本周上证指数更是跳空高开后轻松突破3200点整数关口,创近期新高。而在加密市场,各类资产同样纷纷打开“上涨模式”,市场总市值已回升至9688.10亿美元,扭转了过去3个月以来的横盘趋势。其中,根据CoinMarketCap的数据,截至1月19日,BTC最近7天的涨幅达到了14.01%,目前,已连续5天站稳20000美元整数关口。

""

Wind数据显示,最近20年,A股在春节前后5个交易日的上涨概率均有80%,“红包行情”大概率会贯穿整个春节。那么,加密市场是否同样存在类似的“红包行情”?“红包行情”会持续多久?BTC在春节期间的赚钱效应如何?

""

为此,PAData回顾了BTC最近5年春节期间的市场数据,同时还回顾了近期热门代币最近3年春节期间的市场数据,统计发现:

""

1)最近5年,BTC在春节期间年年都有“红包行情”,涨幅最小也有5%左右,最大则超过16%。以此推测,今年BTC在春节期间出现“红包行情”的概率也非常大。

""

2)除夕当天买入BTC,此后任意一天卖出的平均收益率最高,达到9.4%。另外,如果在初四前买入,此后任意一天卖出的平均收益率也都能超过6.7%,但如果在初五以后买入,那么此后任意一天卖出的平均收益率就会大幅下跌至2%以下,且亏损的概率会大幅提高。

""

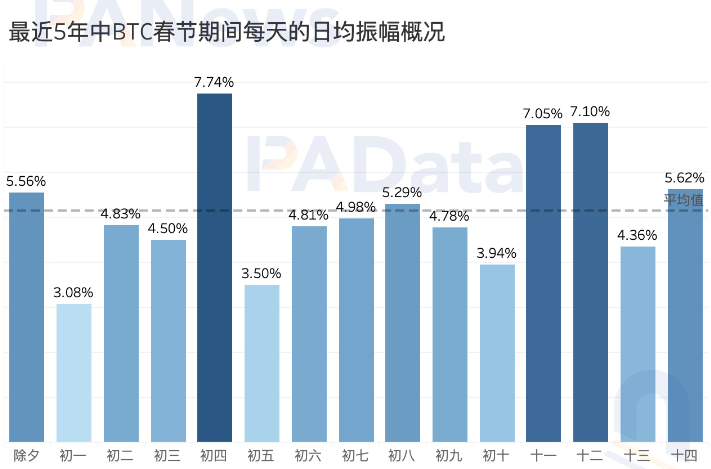

3)“红包行情”下,BTC的日均最大振幅与平时相当,并没有表现是更小的振幅和更高的涨幅。其中,初四、年初十一和年初十二的日均最大振幅都超过了7%,单日波动较大。

""

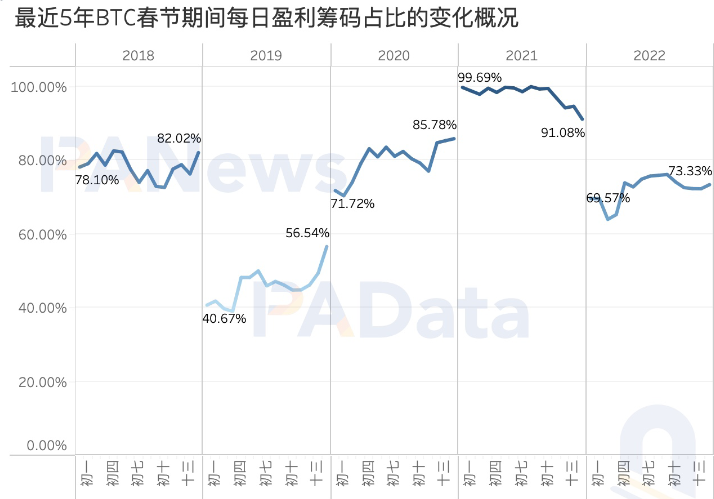

4)2019年和2020年春节期间,BTC盈利筹码占比的涨幅则都增加了15个百分点左右。在初二到初四期间,盈利筹码占比的增长都比较明显。

""

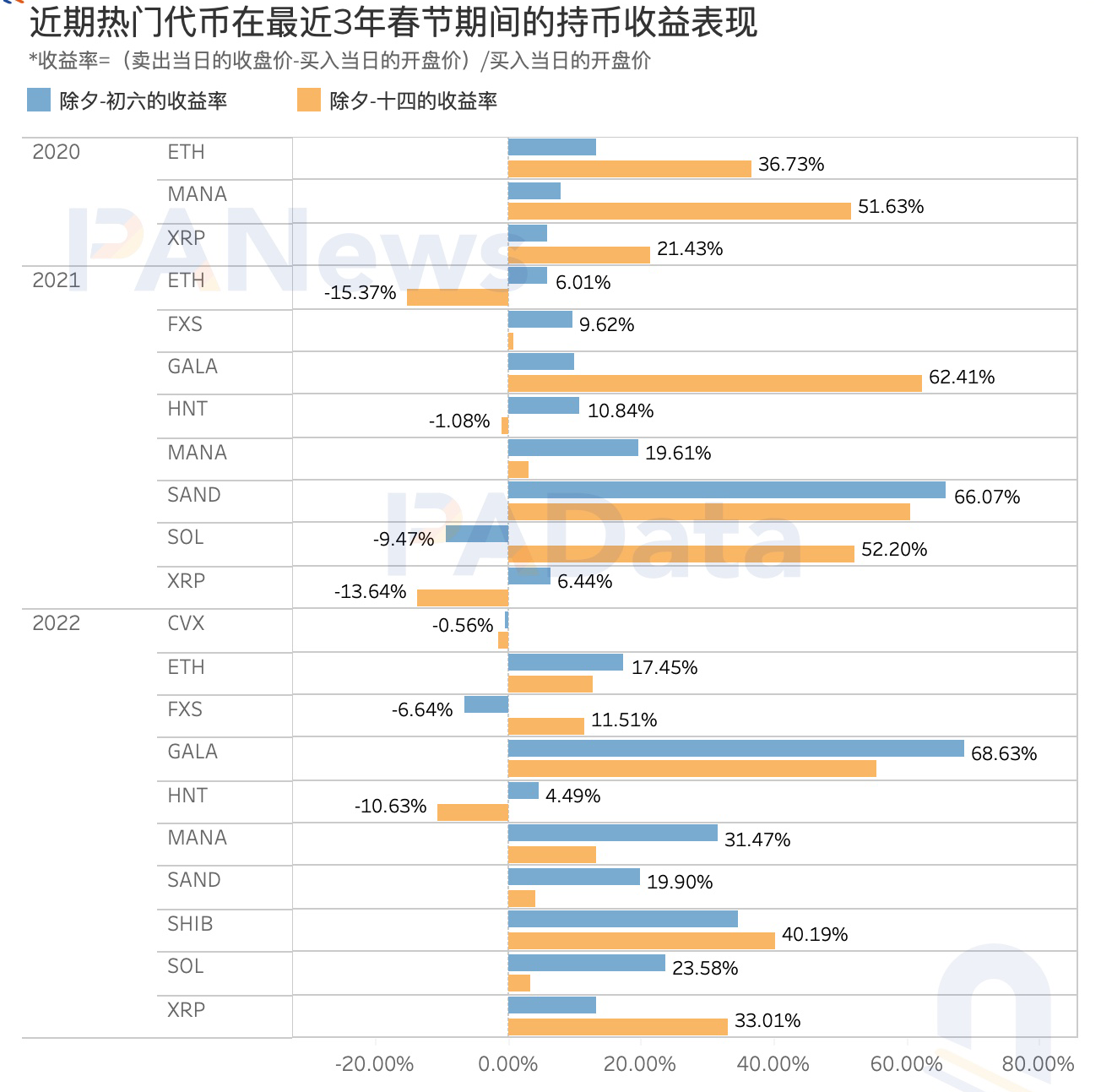

5)最近3年,10种样本热门资产如果在除夕以开盘价买入,在初六以收盘价卖出的话,平均收益率约为16.79%。如果在除夕以开盘价买入,在年初十四以收盘价卖出的话,平均收益率约为20.01%。但热门资产波动性大,部分资产在春节期间持币仍有亏损。

""

BTC除夕买入后不同周期的平均收益超9%,春节期间仍要警惕单日高波动

""

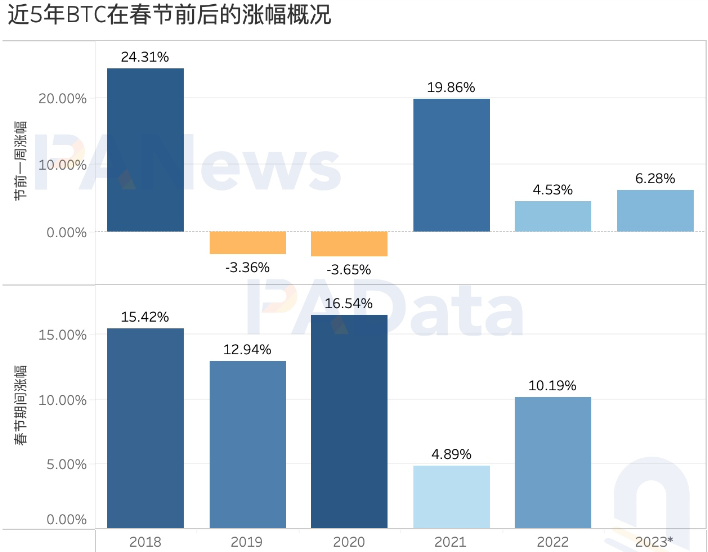

最近5年,BTC在除夕前7天内(不含除夕当日)涨跌不一。其中,BTC在2018年、2021年和2022年除夕前7天内币价上涨,而在2019年和2020年同期则下跌。如果从上涨趋势出现的次数来看,最近5年,BTC春节前出现“红包行情”的概率为60%,而且节前“红包行情”的力度有下降趋势。今年,BTC在春节前已经开始上涨,截至1月17日的除夕前4天内,涨幅约为6.28%,略高于去年。

""

但是,最近5年,BTC在春节期间(除夕至年初十四)则年年上涨,“红包行情”的涨幅最小也有5%左右。其中,BTC在2018年、2019年、2020年和2022年春节期间的涨幅都超过了10%,最高涨幅超过16.5%。从上涨趋势出现的次数来看,最近5年,BTC春节期间出现“红包行情”的概率为100%,这意味着,以此推测,今年BTC在春节期间出现“红包行情”的概率也非常大。

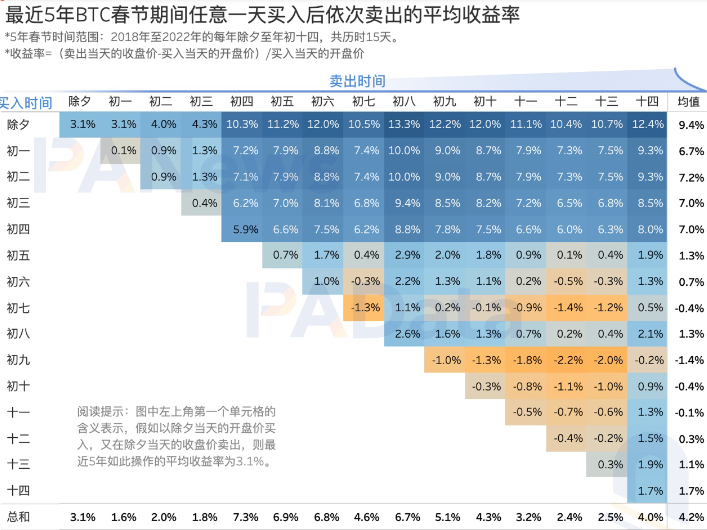

假如在春节期间买入BTC,那么投资者能在趋势行情下获得多大的“红包”呢?PAData统计了自除夕开始,一直到年初十四,共历时15天的春节假期期间,BTC不同持币周期的收益情况。下图纵向时间表示买入日期,买入价格为当天开盘价,横向时间表示卖出日期,卖出价格为当天收盘价,数值为最近5年同一交易周期的平均理论收益。

""

首先,如果以买入时间为观察标准(横向来看),那么,除夕当天买入BTC,此后任意一天卖出的平均收益率最高,达到9.4%。另外,如果在初四前买入,此后任意一天卖出的平均收益率也都比较高,都能超过6.7%。不过,如果在初五以后买入,那么此后任意一天卖出的平均收益率就会大幅下跌,最高不超过2%,且如果在初七、初九、初十、年初十一买入的话,此后任意一天卖出的平均收益率均为负,也即有很大概率会亏损。

其次,如果以卖出时间为观察标准(纵向来看),那么无论此前哪天买入,在初四当天卖出的平均收益率最高,约为7.3%。另外,无论此前哪天买入,在初五、初六和初八当天卖出的平均收益率也比较高,能达到6.8%左右。

""

最后,如果不以某一买卖日期为观察标准,即将所有时间周期放在一起比较,那么,最近5年平均收益最高的交易模式是,在除夕当天以开盘价买入,在初八当天以收盘价卖出,如此交易的平均收益率约为13.3%。另外,在“除夕——初四”“除夕——初五”“除夕——初六”“除夕——初七”“除夕——初九”“除夕——初十”“除夕——十一”“除夕——十二”“除夕——十三”“除夕——十四”“初一——初八”“初二——初八”这12个交易模式近5年的平均收益率也都超过了10%。但值得注意的是,如果在初六以后买入,那么45种交易模式中有23种近5年的平均收益率都为负,也即亏损的概率达到51%。

""

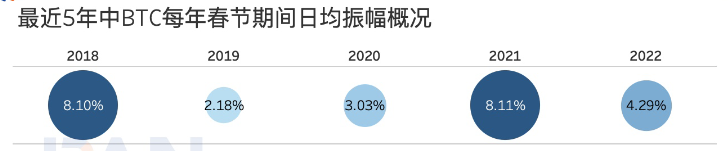

不过,在春节期间的“红包行情”下,投资者仍要警惕单日高波动造成的风险。根据统计,最近5年春节期间(除夕至年初十四)的日均最大振幅差异较大,2018年和2021年都达到了8.1%左右,而2019年、2020年和2022年则都不到4.5%。

从单日的近5年日均最大振幅来看,春节期间的均值为5.14%。这一水平与PAData过往多次观察到的BTC季度日均最大振幅接近,即“红包行情”下,BTC的一段时间内的日均振幅与平时相当,并没有表现是更小的振幅和更高的涨幅。其中,初四、年初十一和年初十二近5年的日均最大振幅都超过了7%,属于单日波动较大的时间。而初一、初五和初十近5年的日均最大振幅都在5%以下,属于单日波动较小的时间。

""

在“红包行情”中,处于盈利状态的筹码在增加吗?这在一定程度上能表现盈利地址的相应变化。可以看到,在2018年、2019年、2020年和2022年这4年中,春节期间的盈利筹码占比处于总体增长趋势,但是,2018年和2022年涨幅都不太明显,都只增加了约4个百分点,而2019年和2020年的涨幅则都很明显,都增加了15个百分点左右。综合来看,在初二到初四期间,盈利筹码占比的增长都比较明显,此后有所波动。

近期热门代币最近3年春节期间平均收益达20%,但日均振幅超过BTC的2倍

""

BTC作为加密市场中市值占比最大的资产,其上涨通常代表着大盘上涨,即其他代币也很有可能出现上涨。因此,除了回溯BTC过去5年的“红包行情”以外,PAData还回溯了近期热门资产过去3年的春节行情。

""

热门资产指最近7天涨幅最高的30种资产和搜索量最高的30种资产,去重后共录得52种。包括WKC、AGIX、MANA、FXS、HNT、FTT、CVX、SAND、FET、APT、COMP、CRV、SOL、AAVE、AVAX、SHIB、OP、CSPR、FTM、NEAR、FLOW、ENJ、ICP、GALA、PI、KAVA、SNX、JASMY、IMX、FIL、XRPC、HOT、HEX、LRC、HBAR、CELO、XTZ、BTC、DOT、CRO、ETH、QUACK、BONK、QNT、MATIC、XOLO、DOGE、ADA、BNB、DPR、LUNC、XRP。这些资产最近7天内的币价涨幅在7%-200%之间,平均涨幅约34%。

""

PAData进一步在涨幅最高和搜索量最高的资产中选择了各自排名前5的资产(如果市值过小则省略后递推选择后续排名的资产)作为观察样本,以期透过样本为展望其他热门资产提供一定的基础。

""

根据统计,最近3年,10种样本热门资产如果在除夕以开盘价买入,在初六以收盘价卖出的话,平均收益率约为16.79%。其中,2020年样本资产在此种交易模式下的平均收益率为9%,2021年为15%,2022年为21%,呈逐年增长趋势。

""

最近3年,10种样本热门资产如果在除夕以开盘价买入,在年初十四以收盘价卖出的话,平均收益率约为20.01%。其中,2020年样本资产在此种交易模式下的平均收益达37%,2021年约19%,2022年为16%,呈逐渐下降趋势。

总的来看,最近3年春节期间,MANA、GALA、SAND、SHIB这4种资产在“除夕——初六”“除夕——年初十四”2种交易模式下的收益都是正的,而ETH、HNT、SOL、XRP、CVX、FXS这6种资产在2种交易模式中存在1种收益为负的情况。热门资产“红包行情”的稳定性不高,这或受到热门资产的波动较大的影响。

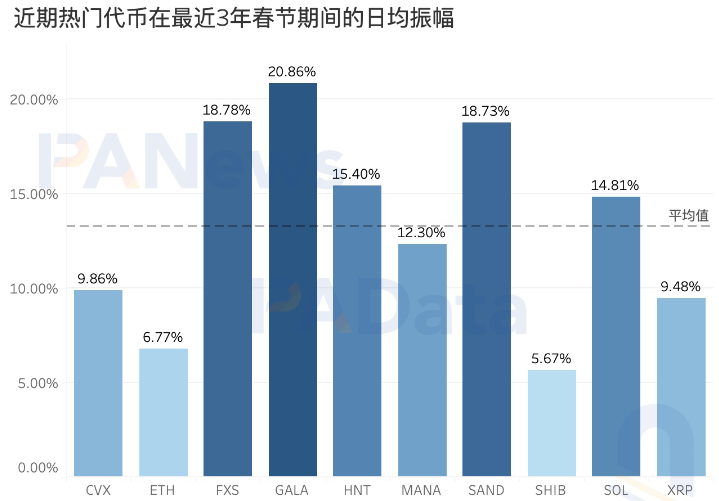

""

根据统计,10种样本热门资产最近3年春节期间的日均最大振幅约为13.27%,大约是BTC的2.5倍左右。其中,FXS、GALA和SAND最近3年春节期间的日均最大振幅都超过了18%,显著高于其他资产。可见,热门资产的波动性显著高于BTC,其“红包行情”下的投资风险也可能高于BTC。