如果美国国会议员未能在本财年截止日期(9月30日)前达成预算协议,联邦政府将面临部分停摆,导致多项非必要行政业务暂停运作,大量公务员被强制安排无薪休假或临时解雇。

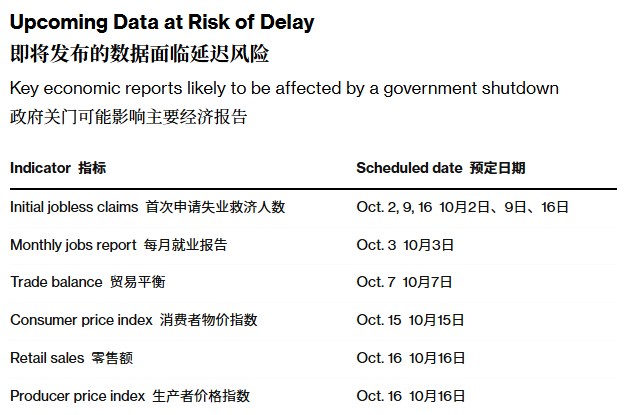

此次停摆的连锁反应之一,是美国关键经济数据的发布计划被迫中断。根据最新公布的应急预案,劳工统计局(Bureau of Labor Statistics, BLS)作为发布“黄金标准”经济指标的核心机构,将全面停止数据采集与处理工作。原定于10月3日公布的9月非农就业报告可能因此延期,后续的消费者价格指数(CPI)、零售销售及新住宅建设等关键数据亦面临延迟风险。 在当前特朗普政府政策动向高度不确定的背景下,就业、通胀与支出指标对判断经济走势具有至关重要的意义。若这些数据无法按时发布,美联储、市场投资者及企业决策者将失去重要参考依据,可能影响其下一步政策调整。例如,美联储在10月议息会议上是否继续降息,将因数据缺失而面临更复杂的判断环境。安永首席经济学家格雷戈里·达科(Gregory Daco)指出:“决策者不愿在浓雾笼罩的环境中盲目飞行。”

一、经济数据发布机制受冲击的具体影响

劳工统计局作为美国经济数据体系的核心机构,其发布的就业报告与CPI被广泛视为衡量经济健康程度的权威指标。

一旦政府停摆,该机构将按计划暂停所有业务活动,包括数据收集、统计分析与报告编制。尽管劳工部预估其整体停摆流程仅需半天即可完成,但劳工统计局涉及系统备份与数据保存的操作可能需要长达三天时间。这一延迟将直接打乱原定于10月初发布的多项经济日程。 在2013年政府停摆期间,劳工统计局曾被迫推迟发布当年9月的就业报告与CPI数据。而2018-2019年的停摆因前期资金预留而未影响数据发布,但本次局势更为严峻。首当其冲的是定于10月3日公布的非农就业报告,其次是10月10日的CPI数据,以及人口普查局负责的零售销售与新房开工量统计。这些数据的缺失将使得市场难以评估消费动力、通胀压力及房地产行业的实时动态。

二、第三方数据源的辅助作用与局限性

尽管政府数据暂停发布,部分第三方机构提供的经济指标仍可提供参考,如ADP研究所的私营部门就业报告、全美房地产经纪人协会的成屋销售数据等。然而,这些数据通常覆盖范围有限,方法论也与官方统计存在差异,其权威性和全面性难以替代政府报告。桑坦德美国资本市场首席美国经济学家斯蒂芬·斯坦利(Stephen Stanley)强调,尽管美联储可通过调研企业联系人获取局部信息,但缺乏宏观汇总数据将大幅增加决策难度。 值得注意的是,第三方数据多侧重于特定行业或区域,无法形成对国家经济全景的准确刻画。例如,ADP就业报告仅涵盖私营部门,而政府发布的非农数据还包括政府雇员与关键行业分布,后者对政策制定更具指导意义。

三、对美联储政策与市场预期的影响

美联储在9月会议中实施了年内首次降息,其决策主要依据劳动力市场降温与通胀趋缓的信号。

若10月议息会议前无法获得最新就业与CPI数据,部分官员可能倾向于推迟进一步行动,以规避误判风险。斯坦利指出:“尽管存在替代数据源,但缺乏长期依赖的宏观指标将显著增加政策制定的复杂性。”此外,企业投资与消费者信心也可能因数据真空而趋于保守,进一步抑制经济增长动能。 美国商会首席政策官尼尔·布拉德利(Neil Bradley)认为,政府停摆虽不足以直接导致经济衰退,但会加剧商业环境的不确定性。企业在面临供应链调整、投资规划等问题时,往往依赖定期发布的宏观数据作为参考,其缺失将延长决策周期,甚至引发市场波动。

四、历史经验与应对策略的启示

从历史经验看,政府停摆对经济数据发布的影响并非首次,但每次引发的挑战各有不同。在2013年停摆事件中,数据延迟导致当季经济评估严重偏差,美联储不得不依赖滞后指标与调查性数据补足信息缺口。此次若停摆长期化,经济分析机构可能需加强高频数据(如周度失业申请、信用卡消费记录)的监测,以构建临时性判断框架。 为降低未来类似风险的冲击,建议优化数据发布机制的应急方案,例如提前备份关键数据集、建立跨机构协作流程,或探索部分指标在停摆期间的简化发布模式。此外,增强第三方数据与官方统计的互补性,也有助于提升经济监测体系的韧性。