撰文:Oliver,火星财经

当一个头顶「首个基于 BitVM 的 Layer 2」、「获华尔街巨头富兰克林邓普顿投资」等耀眼光环的明星项目——Bitlayer,正式宣布其代币 $BTR 即将 TGE 时,市场的情绪复杂而分裂。一方面,是顶级资本背书和宏大技术叙事带来的期待;另一方面,是经历了铭文热潮从顶峰跌落、无数「土狗 L2」一地鸡毛之后,整个市场弥漫的疲惫与怀疑。

这引出了一个所有人都想知道答案的尖锐问题:Bitlayer 此刻发币,究竟是想趁着比特币生态余温尚存,完成一轮精美的「收割」,还是它真的有能力、有资本,为这个看似陷入沉寂的生态吹响新一轮牛市的冲锋号?

要回答这个问题,我们必须超越表面的喧嚣,深入其技术内核、战略蓝图,乃至其联合创始人 Kevin He 的思考——一位亲历数轮牛熊、曾缔造百亿 TVL 生态的连续创业者,他的视野或许能为我们提供关键线索。

Bitlayer 的三张王牌——技术、经济模型与执行力

Bitlayer 并非一个轻率的投机项目,它的核心竞争力由三张紧密相连的王牌构成:坚实的技术、清晰的经济模型和可靠的执行力。

技术王牌:基于 BitVM 的安全叙事 它的核心在于对 BitVM 范式开创性的应用,回归本源的安全。联合创始人 Kevin He 指出,BitVM 的本质是基于比特币的乐观 Rollup (Optimistic Rollup),其精妙之处在于社区共识已逐渐从在比特币上构建复杂虚拟机的艰难尝试,转向了直接验证零知识证明 (ZK Proof) 的可行路径。这意味着挑战者只需在比特币主网上验证一个确定性的 ZK 证明,即可裁定欺诈行为。这一转变极大地降低了实现难度,并带来了两大根本性优势:它无需对比特币协议进行任何升级,便可基于 Taproot 等现有技术实现;同时,通过链上验证,它将 Layer 2 的安全性牢牢锚定在比特币主网之上,突破了传统扩容方案在安全与可编程性之间的两难困境。作为业内首家明确基于 BitVM 开发桥和 Layer 2 的团队,Bitlayer 已与 AntPool、F2Pool 等主流矿池达成战略合作,获得了近 40% 的比特币算力支持,这确保了在发生欺诈挑战时,挑战交易能够被优先打包上链——这是其他团队难以企及的、决定生死的核心优势。

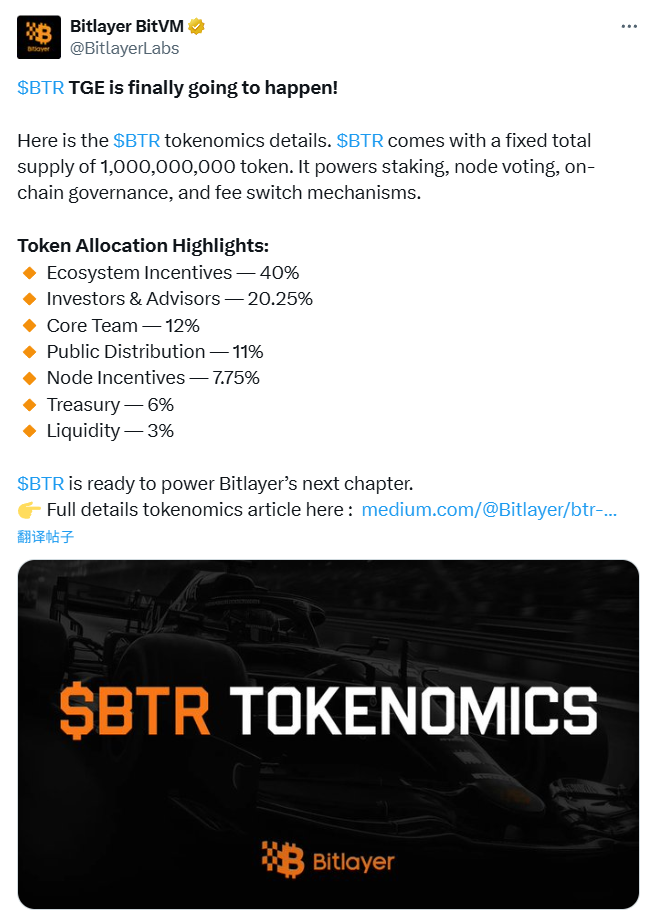

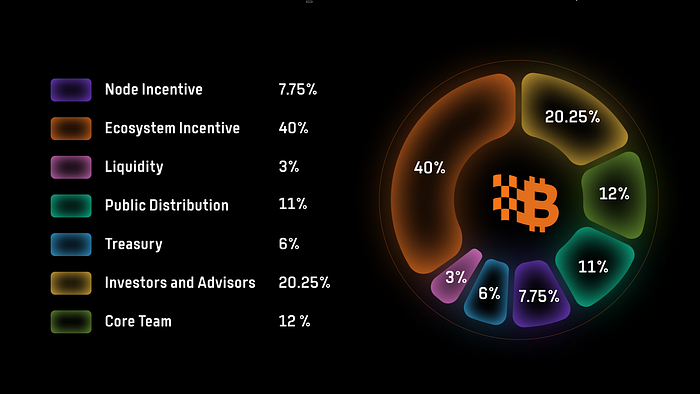

经济模型王牌:精心设计的 $BTR 代币经济学 这不仅是其战略意图的体现,更是其从「市梦率」向「市盈率」转变的清晰路径。$BTR 的总供应量固定为 10 亿枚,其分配策略明确地将重心放在了生态系统的长期建设和激励上。

巨额生态激励: 高达 40% 的代币被指定用于生态激励。这是一笔巨大的「战争基金」,表明 Bitlayer 计划投入巨额资源来引导和培育其生态系统,以在竞争激烈的 L2 市场中吸引开发者和用户。

明确的代币效用: $BTR 被赋予了多重核心功能,包括质押以维护网络安全、参与链上治理决定协议未来,以及一个至关重要的费用开关机制。该机制未来可将协议收入的一部分用于奖励质押者或回购销毁,直接将代币价值与网络经济活动挂钩。

执行力王牌:经验丰富的团队与顶级资本 一个宏大的愿景终究需要一个有能力的团队来实现。Kevin He 的履历本身就是一张有力的信任状:他曾带领团队缔造 HECO 生态链日交易量四百万笔、TVL 突破百亿美元的高光时刻。这支由他领导的、近六十人的成熟团队,加上 Framework Ventures、ABCDE Capital 和富兰克林邓普顿等顶级资本的背书,共同构成了 Bitlayer 将蓝图变为现实的坚实基础。

宏大叙事下的战场——比特币生态的真实温度

Bitlayer 的雄心壮志,需要在一片真实的战场上检验。这片战场——比特币生态,正处于一个狂欢后的「贤者时间」,但远非死寂。它呈现出一种复杂的、多层次的图景,冰与火同时存在。

正如 Kevin He 所观察到的,东西方市场对生态现状的观感存在显著温差。华人社区因早期对铭文热潮的期待过高,在潮水退去后普遍感到悲观;而欧美市场则依然保持着相当的活跃度。他认为,评判 BTC 生 températures 不能简单套用以太坊的标准。BTC 生态的独特性在于,其巨量的金融活动,如借贷、衍生品交易等,长期存在于链下。真正的机会,在于将这些数万亿美元的链下活动,安全、高效地迁移到链上。这才是 BTCFi 的星辰大海,而当前的瓶颈正是基础设施不足。

铭文和符文热潮虽然降温,但它作为一次成功的「压力测试」,留下了两份宝贵的遗产:它用真金白银验证了需求,证明市场对在比特币上发行和交易资产的巨大渴望;同时,它也暴露了瓶颈,让所有人认识到 Layer 2 是生态发展的必需品。

因此,在市场冷静期,真正的建设者并未停歇,一场激烈的「基础设施竞赛」正在多个战线上悄然展开。

在协议层,创新仍在深化。苦等两年的 RGB 协议终于上线主网,代表了原生智能合约的探索方向。BRC 2.0 升级则试图为庞大的 BRC-20 资产嫁接 EVM 兼容性。此外,像 SAT 20 这样坚持建设两年之久的原生协议,也终于上线了主网 SatoshiNet。

在应用和基础设施层,竞争同样激烈。各类 Layer 2 解决方案正在加速交付。除了 Bitlayer,基于 BitVM 2 构建的比特币桥 Fiamma 也已上线主网,加入了信任最小化跨链方案的竞争。而像 Spark 这样专注于支付和结算的原生 L2 也在不断推进。

在资产和市场层面,生态也并未完全冰封。以「节点猴」NodeMonkes 为首的老牌比特币 NFT 系列在近期表现出强劲的回暖势头。在符文领域,尽管龙头 $DOG 表现平平,但多个符文在更长的时间维度上表现优异,并且 $DOG 成功上架 Kraken 等主流交易所,标志着符文资产正逐步获得更广泛的认可。

总而言之,当前的比特币生态并非一片死寂,而是进入了一个去伪存真、苦练内功的阶段。Bitlayer 正是在这样一个建设者们竞相角逐的时代背景下,携其独特的技术路线和雄厚资本入场。

是收割还是破晓?答案藏在执行的细节里

现在,我们可以更清晰地回答最初的问题。Bitlayer 是来「收割」的吗?这种风险真实存在。BitVM 是一项前沿且极其复杂的技术,面临巨大的技术执行风险。同时,在 Merlin Chain 等对手通过激进空投抢占了巨额 TVL 的背景下,市场竞争异常激烈。

然而,Bitlayer 成为「新希望」的可能性,其轮廓也愈发清晰。这份希望不再基于一个模糊的梦想,而是建立在一系列坚实的支柱之上:

-

清晰的路线图: 它拥有一条从市场验证到安全实现再到构建高频交易环境的清晰规划。

-

务实的商业模式: 它选择从服务机构和用户的生息刚需入手,而非凭空创造需求。

-

可靠的领导力: 它由一位久经沙场的领导者掌舵,为项目的执行力提供了保障。

-

契合比特币精神的安全哲学: 它所秉持的对信任最小化的极致追求,最有可能赢得比特币核心社区和长期持有者的最终信任。

$BTR 的发行,不是故事的结局,而是发令枪响。那 40% 的庞大生态激励基金,将是 Bitlayer 实现其三阶段路线图的燃料。最终的答案,不在于 TGE 那一刻的币价,而在于 Bitlayer 能否稳健地交付其技术承诺,并用好这笔「战争基金」,培育出一个真正能将比特币链下价值迁移至链上的繁荣生态。

对于我们这些观察者而言,Bitlayer 的征途,将是衡量比特币生态能否完成从「数字黄金」到「可编程金融基础设施」这惊险一跃的最佳样本。