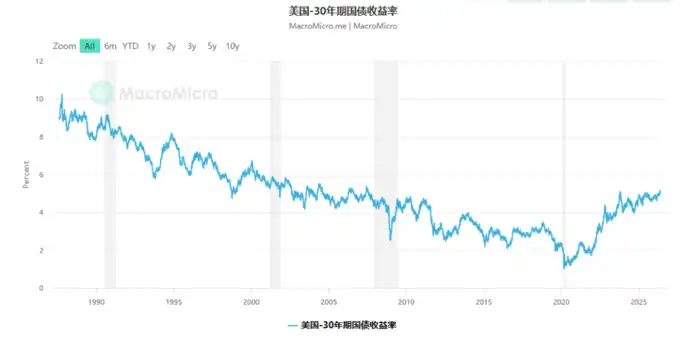

Доходность 30-летних казначейских облигаций США снова превысила 5%. На этот раз реакция рынка заметно отличается от 2023 года — инвесторы начинают по-настоящему принимать реальность того, что высокие процентные ставки сохранятся надолго.

Аналитики указывают, что за этим стоит более глубокий структурный сдвиг: три столпа, поддерживавшие низкую инфляцию и низкие процентные ставки в США на протяжении последних 50 лет — дешевый капитал, дешевая рабочая сила и дешевая энергия — одновременно разрушаются. А направление развития ИИ станет главной неизвестной в определении будущей динамики инфляции.

Доходность 30-летних казначейских облигаций США недавно снова превысила 5%. Колумнист Financial Times Рана Форухар в своей статье отмечает, что в отличие от кратковременного пробития уровня 5% в 2023 году и последующего быстрого отката, на этот раз реакция рынка явно иная — инвесторы, кажется, наконец начинают по-настоящему принимать реальность: США прощаются с эрой низких процентных ставок и вступают в новую фазу, характеризующуюся более устойчивым и разнообразным инфляционным давлением.

В статье цитируется недавний отчет главного экономиста Apollo Торстена Слёка, направленный клиентам, в котором говорится: «Инвесторы должны подготовить свои портфели к среде с высокими процентными ставками, сохраняющимися в краткосрочной, среднесрочной и долгосрочной перспективе».

За этим стоит более масштабная структурная история: три дешевых фактора, двигавших экономический рост США на протяжении последних 50 лет — дешевый капитал, дешевая рабочая сила и дешевая энергия — одновременно меняют направление.

Как появился «дешевый дивиденд» полувековой давности?

Снижение доходности 30-летних казначейских облигаций с двузначных процентов в начале 1980-х до примерно 1% во время пандемии — этот почти полувековой нисходящий тренд не был случайностью.

За ним стояла целостная макроэкономическая логика:

Дешевый капитал: десятилетия глобализации и технологический прогресс в обрабатывающей промышленности сдерживали цены на товары; нефтеэкспортирующие страны репатриировали в США крупные нефтедоллары, обеспечивая изобилие дешевых средств; реформы по приватизации пенсий породили огромный спрос на различные финансовые продукты; глобальные инвесторы争先恐后 покупали казначейские облигации США, поскольку ни одна страна не была безопаснее Америки.

Дешевая рабочая сила: аутсорсинг производств, ослабление профсоюзов, волна автоматизации и корпоративная культура «приоритета акционеров» (акцент на финансовом инжиниринге, пренебрежение инвестициями в сотрудников) совместно сдерживали рост заработной платы, особенно вознаграждения рабочих без высшего образования, постоянно поддерживая прибыльность предприятий.

Дешевая энергия: нефтедолларовая система в определенной степени подавляла инфляцию, глобальная торговля энергоресурсами в долларах также укрепляла глобальное положение американской валюты.

Эти три столпа совместно поддерживали полувековое процветание США с низкой инфляцией и низкими процентными ставками.

Три столпа одновременно ослабевают

Рана Форухар в своей статье отмечает, что каждый из вышеупомянутых поддерживающих факторов сейчас претерпевает изменения.

Капитал: С каждым аукционом по размещению казначейских облигаций США иностранные покупатели сокращают, а не увеличивают свои покупки. Деглобализация и решоринг (возврат производств) в краткосрочной перспективе будут подталкивать вверх цены на товары и услуги. В то же время подрываются основы нефтедолларовой системы.

Энергия: Напряженная ситуация на Ближнем Востоке продолжается, что наиболее непосредственно затрагивает страны-импортеры энергоресурсов в Азии. Но в более долгосрочной перспективе это, возможно, ускорит развитие стран Азии, в частности Китая, в сфере чистой энергетики — в то время как США отходят от климатических обязательств. Это означает, что долгосрочные потоки капитала могут переориентироваться с США на Китай.

Рабочая сила: В последние годы нехватка рабочей силы, масштабные забастовки (включая успешные действия в автомобильной промышленности), ужесточение иммиграционных ограничений, а также рост членства в профсоюзах в некоторых секторах (особенно среди «белых воротничков») способствовали росту заработной платы. Но эта тенденция частично нивелируется двумя факторами: во-первых, ростом стоимости корпоративного медицинского страхования, и компании стремятся компенсировать это за счет сдерживания зарплат; во-вторых, воздействием искусственного интеллекта.

Есть и медленные переменные: долг, геополитика и популизм

Помимо вышеуказанных явных факторов, существуют и несколько «медленных переменных»: растущий государственный долг, усиление геополитической напряженности и распространение популизма.

Общий эффект этих рисков таков: кредиторы требуют более высоких премий за риск, чтобы согласиться одолжить деньги — особенно на срок в несколько лет.

Это напрямую подталкивает вверх долгосрочные процентные ставки, то есть доходность 30-летних казначейских облигаций.

ИИ: Спаситель или новый источник инфляции?

Среди всех переменных направление развития искусственного интеллекта труднее всего предсказать, но его влияние может быть наиболее глубоким.

Рана Форухар предлагает два совершенно разных сценария:

Оптимистичный сценарий: Эффект повышения производительности от ИИ широко распространяется на различные отрасли и людей, создавая новые рабочие места и источники дохода. Модель лаборатории бюджета Йельского университета показывает, что в этом сценарии государственный долг США значительно сократится, а инфляция также снизится.

Пессимистичный сценарий: ИИ становится лишь инструментом для сокращения штата, сжатия издержек и расширения прибыли компаний, в то время как сама инфраструктура ИИ (потребляющая огромное количество чипов, земельных ресурсов, воды и электроэнергии) создает новое инфляционное давление, и чистый эффект заключается в повышении, а не снижении издержек. Правительству также придется вмешаться для помощи замещенным работникам, что приведет к росту долга.

В настоящее время гиганты ИИ в огромных объемах поглощают недвижимость, чипы, водные ресурсы и электроэнергию, что уже подталкивает вверх цены на эти ресурсы в экономике в целом. Окончательный результат станет ясен лишь через несколько лет.

Настоящий вызов для инвесторов

Вывод статьи прямой и отрезвляющий: большинство участников рынка провели всю свою карьеру в «эпоху дешевизны». Их интуиция, модели и ожидания были откалиброваны в условиях низких процентных ставок.

А сейчас эта среда меняется.

«Инерция ожиданий» — мощная сила. Когда в 2023 году доходность 30-летних казначейских облигаций превысила 5%, многие считали это лишь временной аномалией, которая вскоре откатится назад. Но на этот раз реакция рынка уже иная.

Корректировка означает отказ от старых ожиданий. Для инвесторов, привыкших к низким процентным ставкам, это непростая задача.