作者:Elsa

翻译:白话区块链

Web3 游戏行业自成立以来经历了显著的演变。最初由“边玩边赚”(P2E)模式驱动,如今该行业正转向更平衡的“边玩边赚”方式,优先考虑游戏的吸引力和赚钱的潜力。这种转变解决了纯 P2E 模式的可持续性问题,尤其是在游戏公会起着关键作用的发展中国家。

当我们审视 2024 年 Web3 游戏的发展状况时,这些基础性的转变为我们分析当前市场趋势、玩家行为和经济影响奠定了基础…

1、玩家基础动态

自 2023 年以来,Web3 游戏的玩家数量逐渐下降。玩家基础从 2023 年的 603 万人缩减到目前大约 100 万月活跃用户。

2024 年 1 月是上半年玩家数量最多的月份,约有 173 万玩家。值得注意的是,与 2021 年 11 月行业峰值时的约 2100 万玩家相比,现在的玩家数量是当时的二十分之一。

2、玩家分类和活动情况

当前数据显示,绝大多数游戏地址处于不活跃状态。只有 1,970 个地址被归类为活跃地址,而 1,450 个则被归类为不活跃的投资者地址。值得注意的是,只有 14 个地址在所有 Web3 游戏中被认定为铁杆玩家。这种分布描绘出一个只有少量核心高参与度用户的市场。

3、游戏合约的区块链分布

在活跃的游戏智能合约数量方面,Polygon 以约 12,400 个合约领先。BNB Chain 紧随其后,但合约数量仅为 Polygon 的十分之一左右。以太坊和 Avalanche 落后较多,每个区块链上仅有几百个游戏合约。这种分布的原因包括交易成本、速度和生态系统支持等因素。

4、游戏中的Token标准

在所有游戏合约地址中,ERC20 Token最为常见,其数量是 ERC721 Token的三倍多。ERC1155 Token则最少,约有 1,890 万个实例。

5、游戏表现和用户参与度

在过去的六个月里,一些游戏表现非常出色,例如 Matr1x、Cellula 和 Yuliverse。它们的活跃独立钱包数量名列前茅,用户参与度非常高。

6、游戏中的资产铸造情况

CryptoMines 在资产铸造量方面领先,约有 2,480 万个 NFT,其次是 Bomb Crypto 和 Flowerpatch。

新的游戏资产铸造量每月波动,2023 年 12 月达到高峰,约有 318,000 个新资产。

尽管 2024 年初的牛市推动了资产价格上涨,但链上数据显示,游戏行业仍处于冷却期,没有显著的实际增长。

7、游戏活动模式

对游戏活动的分析显示,在 UTC 时区的下午时段参与度最高,交易频率超过 9500 万次。这一时间段对应美国的早晨和亚洲的晚上。活动量在 UTC 夜间最低,下降到峰值水平的约三分之二。

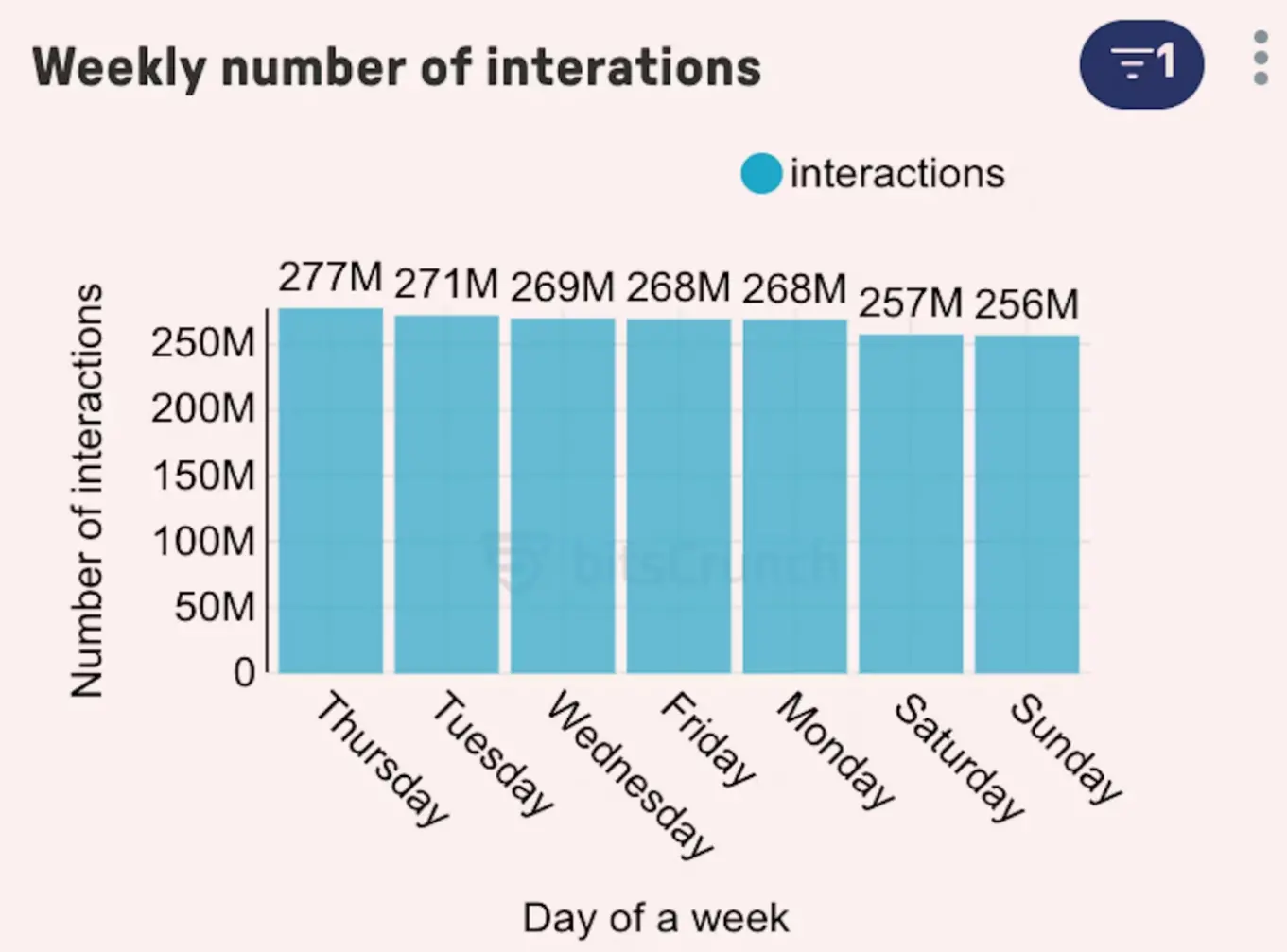

每周的模式显示,星期四是链上交易最活跃的日子,平均约为 2.77 亿次,其次是星期二和星期三。周末的活动明显较低。

注:本文图片来源:bitsCrunch