Key takeaways:

XRP derivatives are dominated by bears as the funding rate turned deeply negative, and open interest remains stagnant.

XRP ETF volumes and declining XRP Ledger TVL show fading interest in the XRP ecosystem, reducing the chances of a near-term price rebound.

XRP (XRP) fell 9% over two days after being rejected at $2.18 on Tuesday. The slide below $2 created brief turmoil in derivatives markets as the cost of holding leveraged bearish positions jumped to a two-month high. Traders worry that XRP could weaken further given the slowdown in exchange-traded fund (ETF) activity and the decline in XRP Ledger deposits.

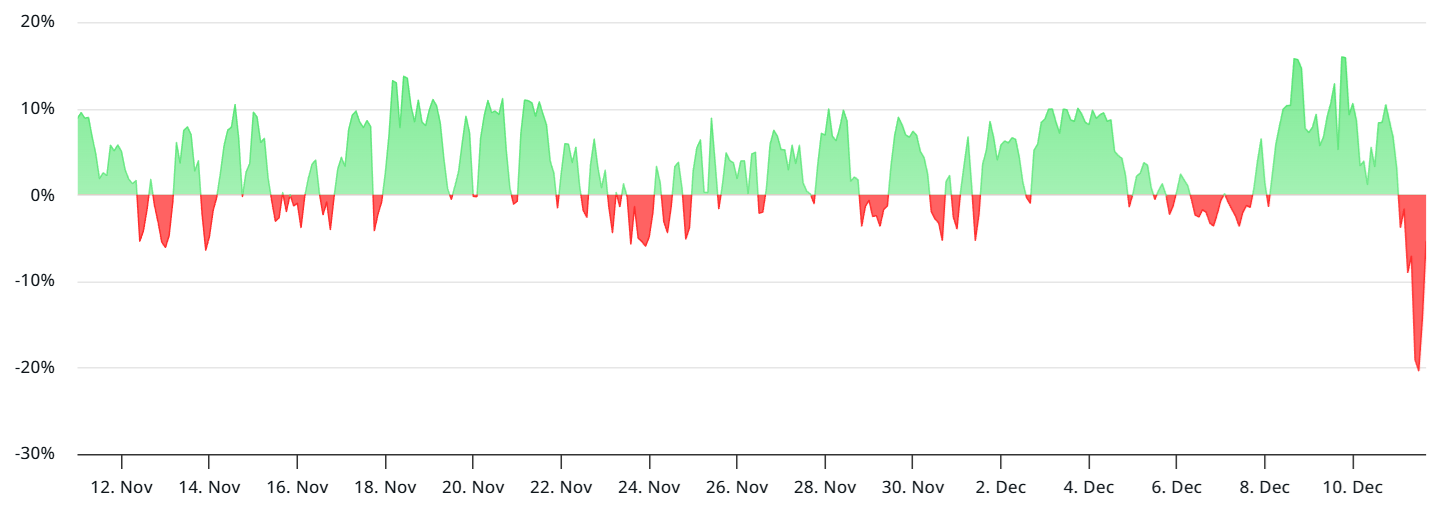

The funding rate on XRP perpetual futures fell to -20% on Thursday, the lowest since the Oct. 10 crash. Negative readings indicate that sellers (shorts) pay buyers (longs) to maintain open positions, signaling a near-total lack of demand from bullish traders. In more balanced conditions, the rate typically ranges from 6% to 12% to account for the cost of capital, with longs covering that fee.

Such deeply negative funding rates are rare and usually short-lived. Some analysts even view them as potential reversal signals, though most historical examples emerged during flash crashes rather than extended corrective phases. In addition, falling appetite for leverage has led some to question whether traders have simply stepped back from XRP.

Aggregate open interest in XRP futures stood at $2.8 billion on Thursday, unchanged from the prior week. Still, leveraged positions have not recovered the $3.2 billion level seen in late November. The data suggests XRP bears are reluctant to increase exposure, especially after the token has already dropped 45% since reaching $3.66 in July.

Declining XRP ETF activity and fading TVL on XRP Ledger

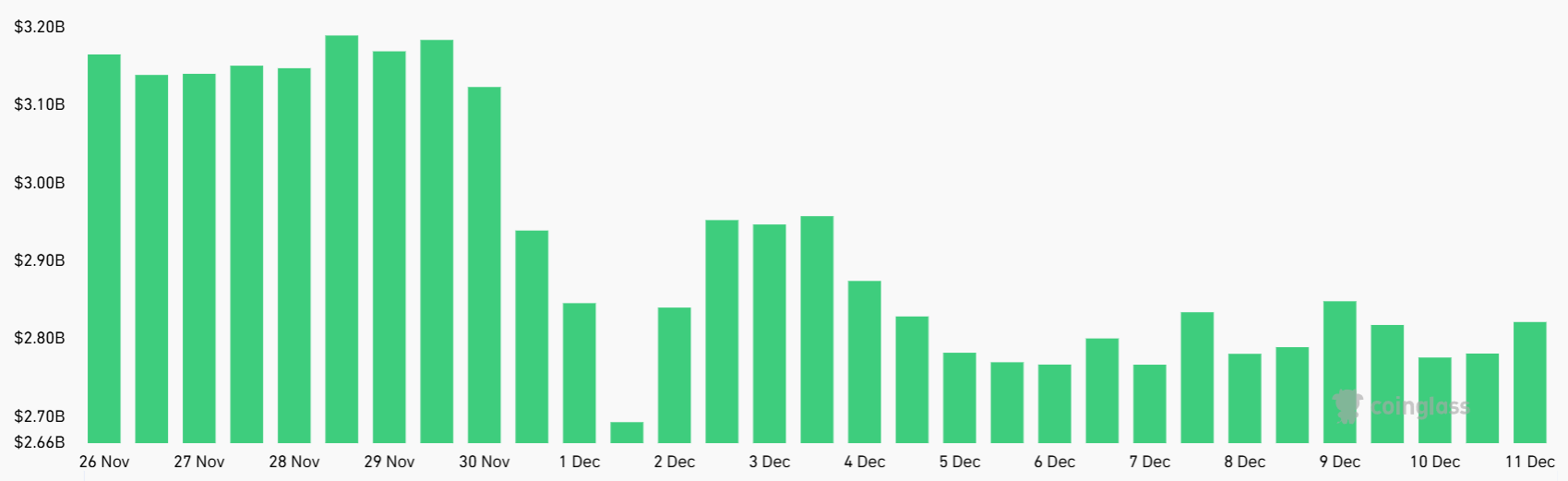

Part of the muted appetite for bullish XRP positions can be tied to declining activity in the US-listed XRP ETFs. Traders entered November with strong expectations, but inflows and trading activity dropped sharply after just three weeks, leaving assets under management stuck near $3.1 billion, according to CoinShares data. For comparison, Solana ETFs hold $3.3 billion in assets.

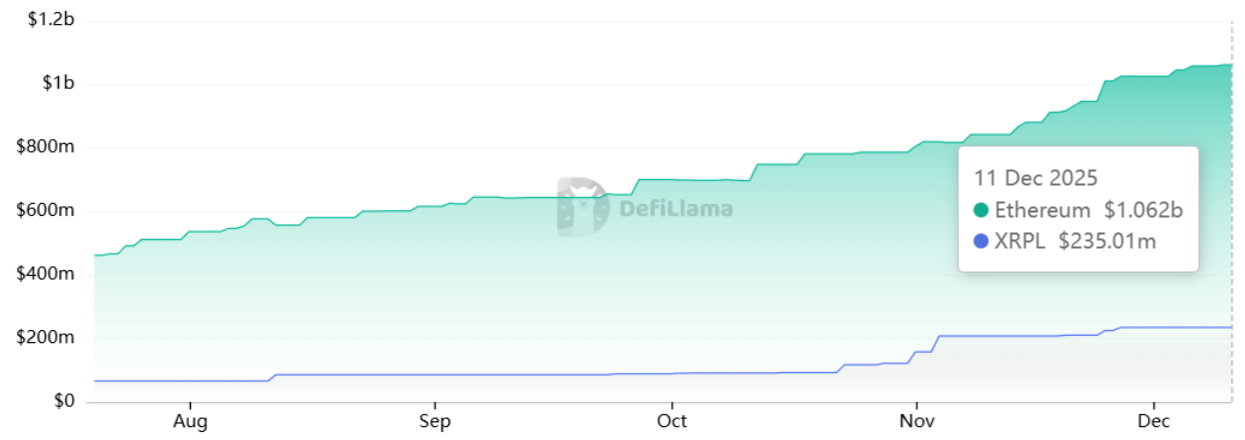

Daily volume on US-listed XRP ETFs rarely exceeds $30 million, which significantly dampens interest from institutional desks. Fading demand for the XRP Ledger is another source of frustration for holders. Even the Ripple-backed stablecoin Ripple USD (RLUSD) relies primarily on the Ethereum network rather than XRP’s infrastructure.

More than $1 billion worth of RLUSD has been issued on Ethereum, compared with just $235 million on the XRP Ledger. More concerning, TVL on the XRP Ledger has dropped to its lowest level of 2025 at $68 million, signaling declining engagement with the chain’s decentralized applications (DApps). In contrast, the Stellar blockchain holds $176 million in TVL, despite XLM’s market capitalization being 93% smaller than XRP’s $121.8 billion.

Related: XRP price may grow ‘from $2 to $10’ in less than a year–Analyst

XRP remains under pressure as competing blockchains such as BNB Chain and Solana continue to strengthen their positions in the DApps ecosystem. The limited activity on XRP Ledger creates a reinforcing cycle in which investors have fewer incentives to hold XRP, especially when compared with the native staking yields available on BNB and SOL.

So far, there is no clear evidence that any pickup in XRP Ledger activity would translate into direct benefits for XRP holders.

XRP derivatives point to increased confidence among bears, while onchain metrics and ETF flows show fading interest, particularly from institutional investors. As a result, the odds of sustained bullish momentum for XRP appear low in the near term.

This article is for general information purposes and is not intended to be and should not be taken as, legal, tax, investment, financial, or other advice. The views, thoughts, and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.