As Q3 rolls out, blockchain infrastructure is entering its biggest coordinated transformation to date. It includes rising institutional demand rather than another race for retail adoption.

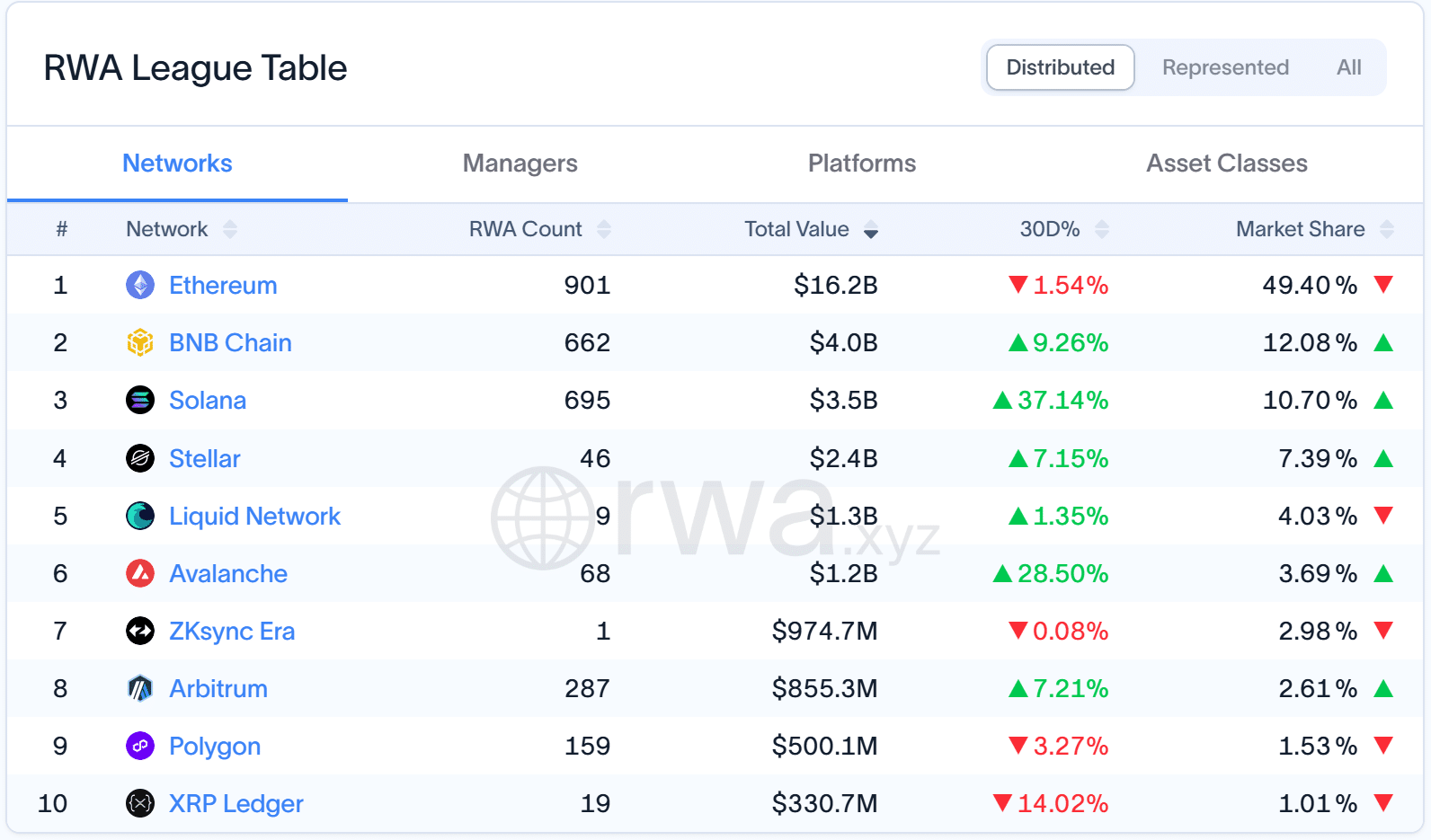

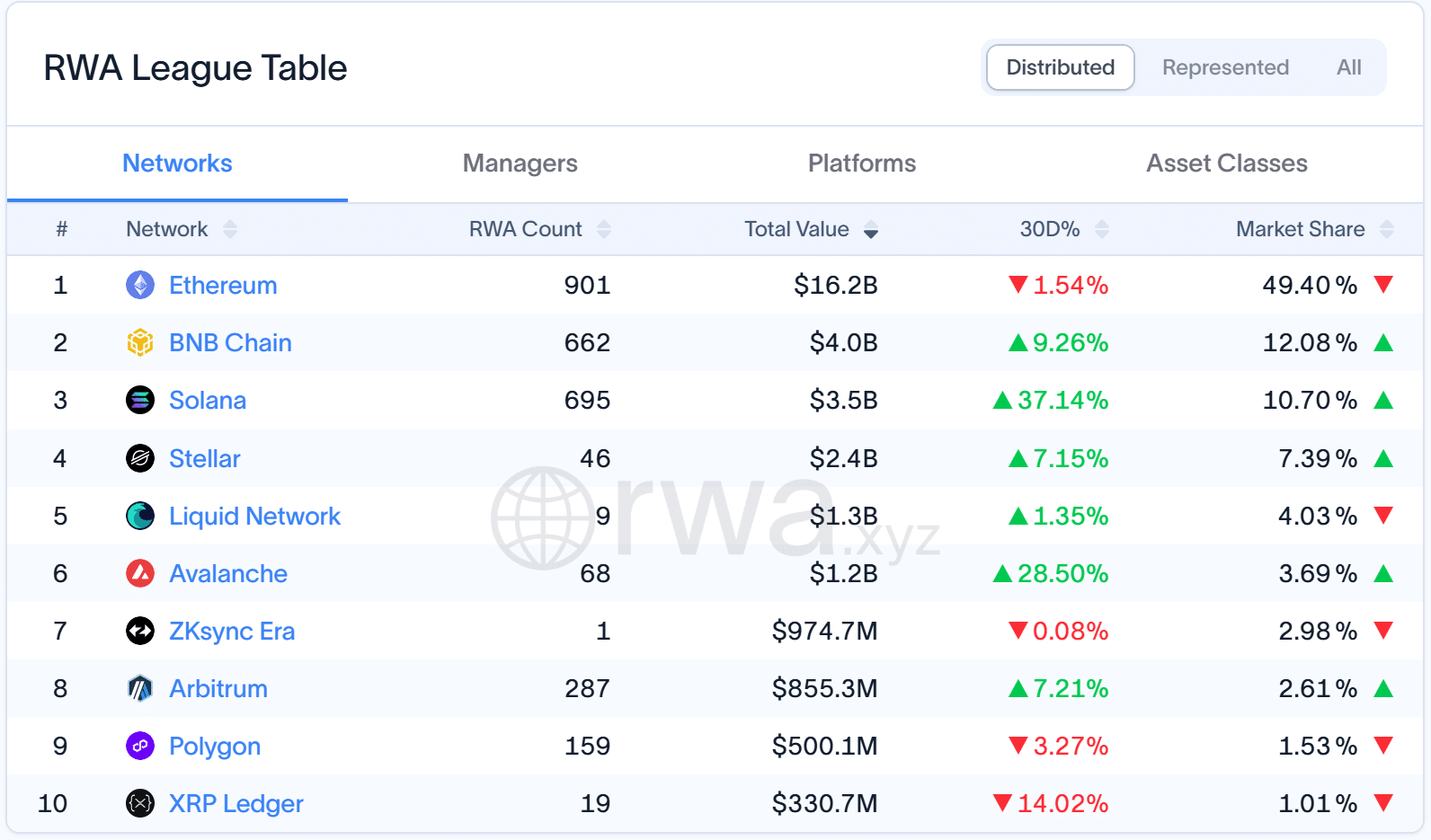

More than $30 billion in RWA now sits on public blockchains, exposing weaknesses in existing networks.

Throughput, settlement speed, compliance, and reliability have become immediate priorities. Therefore, major blockchains are redesigning their foundations instead of relying on incremental upgrades.

Ethereum [ETH], Solana [SOL], Base, and Avalanche [AVAX] each target different bottlenecks through protocol-level improvements.

However, they share the same objective of supporting institutional-scale financial activity. This synchronized rebuild signals that infrastructure quality is becoming the industry’s main competitive advantage.

As deployments continue through 2026 and 2027, capital, developers, and liquidity will increasingly favor networks that execute these upgrades successfully.

How major blockchains are rebuilding for institutional finance

The upgrade process has evolved beyond faster and better speeds. The need for greater reliability as an institutionally viable option was brought forth by institutions and banks. Institutions have come to expect and therefore demand predictable settlement times, regulatory compliance, and uninterrupted execution.

That expectation has highlighted weaknesses in all areas of current decentralized networks.

Hence, rather than simply applying patches or making incremental changes, many of the major decentralized networks are being redesigned at the foundation level.

Ethereum is leading that transition.

Development on Glamsterdam accelerated in late 2025 before active devnets launched in early 2026. The mainnet version will be deployed in H1 2026. The upgrade will raise gas limits from approximately 60 million to 200 million.

Notably, it introduces PBS (pre-blocked state). This will be enshrined in the Ethereum codebase, as well as block-level access lists. Both of these enhancements will provide increased settlement capabilities while preparing Ethereum to run parallel executions as per the Lean roadmap.

In contrast, Solana is solving a different challenge.

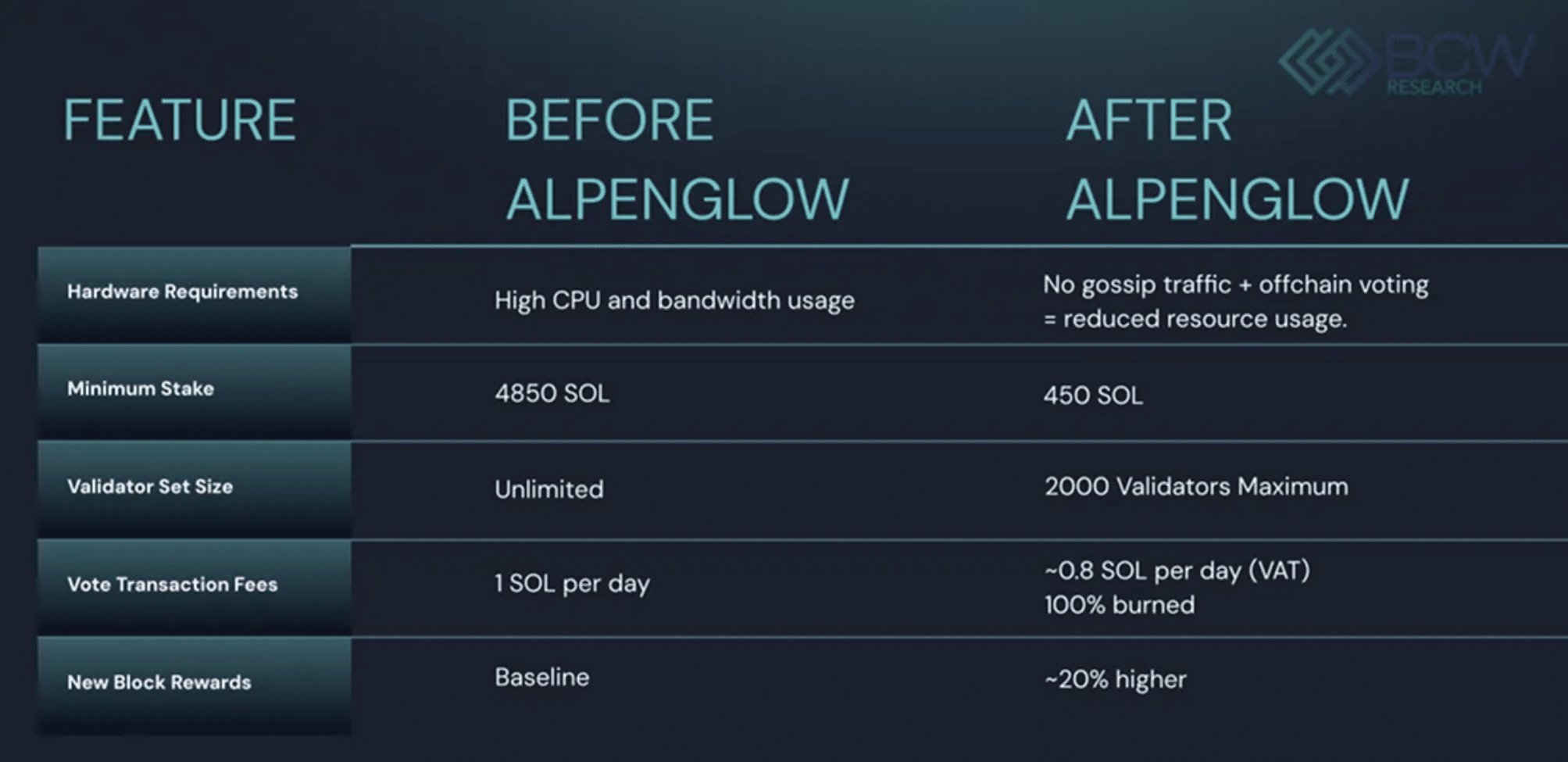

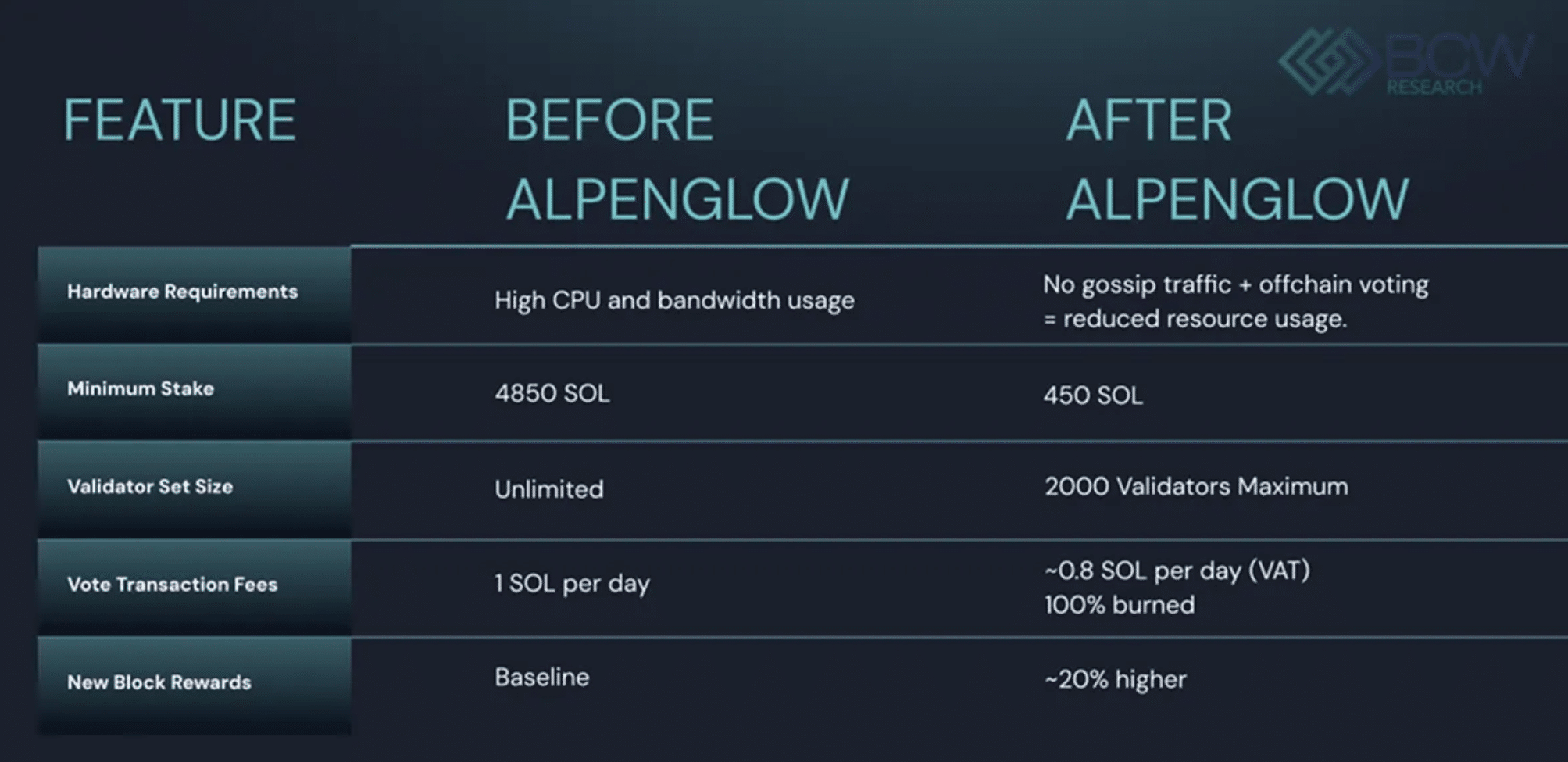

Alpenglow went into the production phase during 2025 and then proceeded through test nets in Q1 to Q2 2026. Solana plans to deploy Alpenglow on the mainnet in H2 2026.

Unlike Ethereum’s approach of initially enhancing its capacity, Solana is redesigning its consensus mechanism. Finality time decreases from 12.8 seconds down to about 100-150 ms.

Beyond reducing finality, Alpenglow removes vote transactions that currently consume nearly 75% of Solana’s network resources. These improvements should enhance the reliability of Solana during periods of prolonged institutional utilization.

Building infrastructure beyond speed

Once settlement and execution improve, infrastructure must support regulated financial activity. This new requirement has caused a shift in focus from development, deployment, and programmability towards compliance.

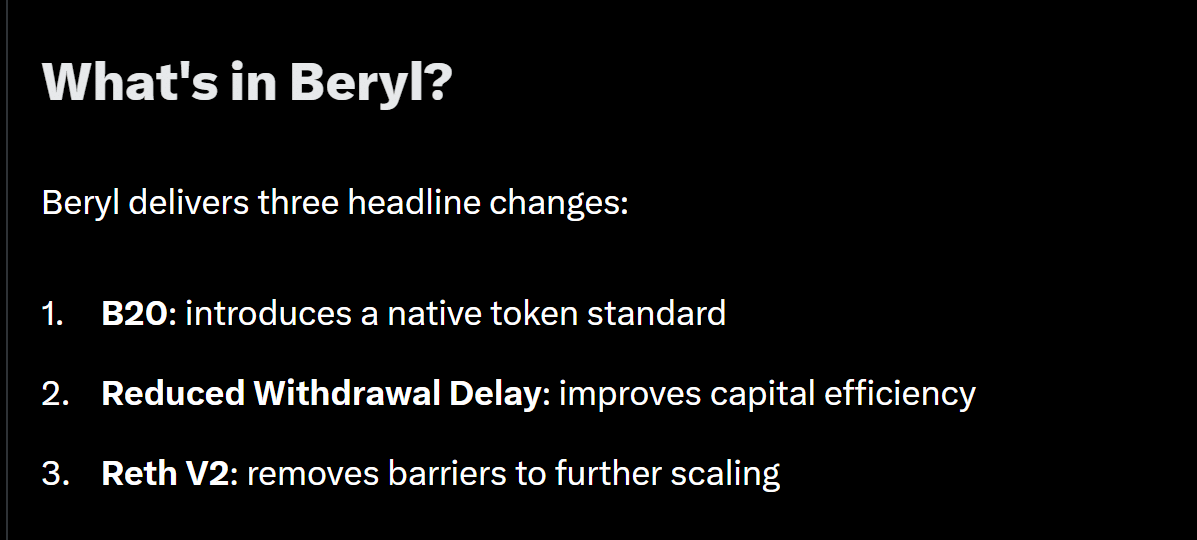

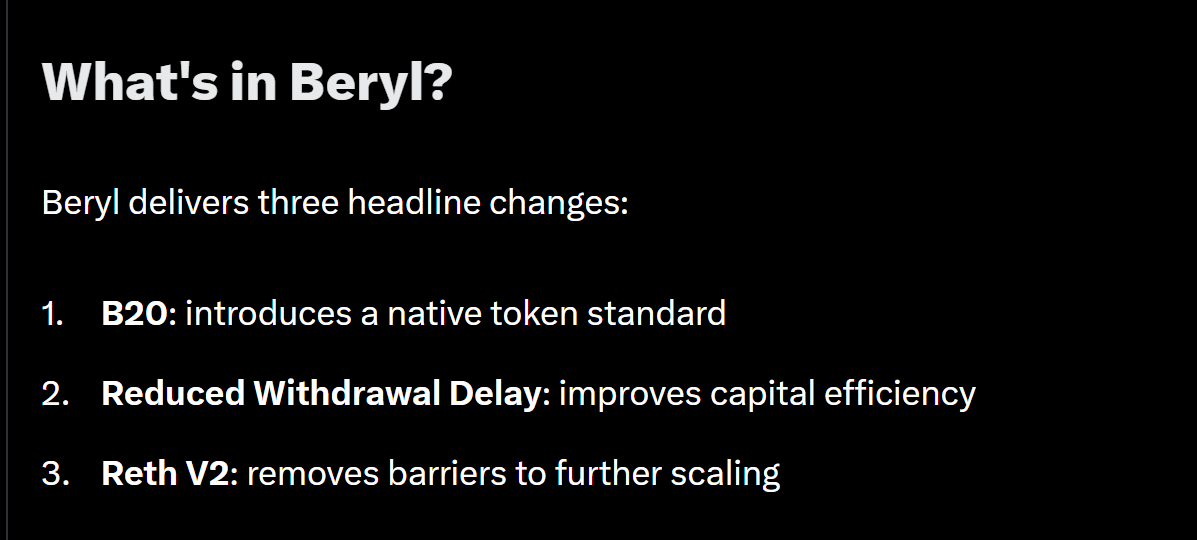

Base began developing Beryl in late 2025, with deployment scheduled for Q3 2026.

In addition to creating better ways to sequence information and provide access to this information via Beryl, it also includes a standardized form of tokens called the B20 token standard.

This standard can include stablecoins issued under regulatory conditions, tokenization of other types of assets, and equity issuance using compliant mechanisms built into the protocol.

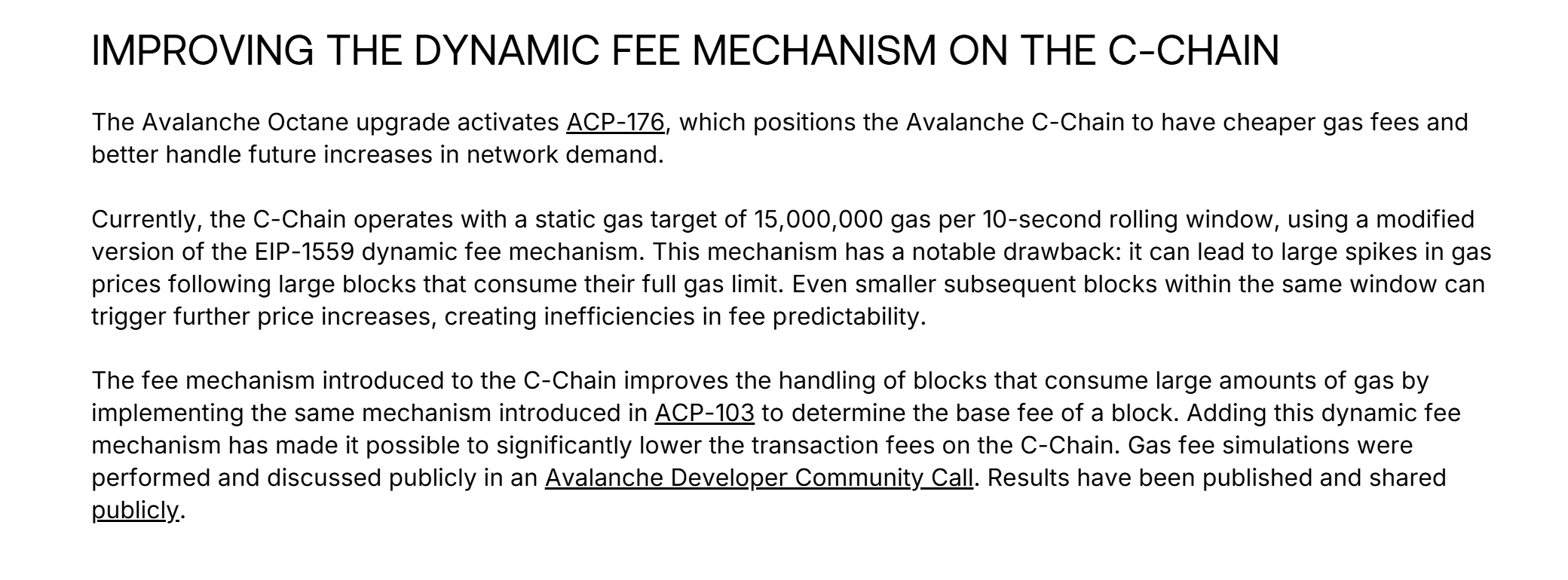

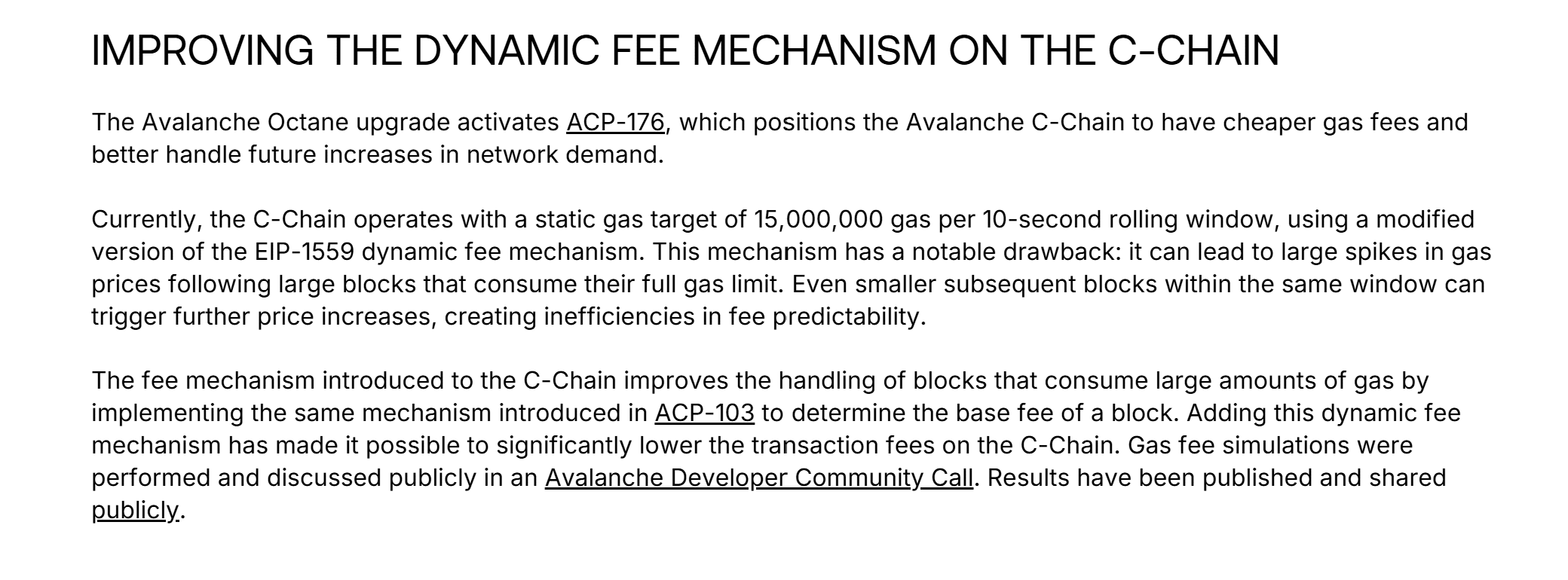

Octane on Avalanche was ramped up during the first quarter of 2026 after the Etna upgrade. Deployments continue to occur from the middle of Q2 through to Q3 of 2026.

Octane upgrades allow for greater transaction processing speeds while decreasing the cost of deploying an enterprise application. These advancements have made it possible to create an institutional blockchain specifically designed to operate for extended periods of time.

While Bitcoin [BTC] represents the most conservative path within the industry, OP_CAT (Opcode Concatenate) gained significant traction during 2025. The larger community continues to test OP_CAT through 2026. Activation of OP_CAT is predicted to occur by either late 2026 or early 2027.

Rather than redesigning Bitcoin, OP_CAT expands scripting while preserving its security model. Together, these timelines show institutions are no longer demanding faster blockchains alone. They increasingly require infrastructure built for long-term financial activity.

Scaling for institutional demand

The infrastructure race now enters its most important stage.

Technical upgrades alone will not determine long-term leadership because institutions ultimately allocate capital based on proven execution.

Although every major network is strengthening scalability, compliance, and reliability, adoption continues favoring ecosystems already supporting regulated financial activity.

Ethereum retains the largest share of tokenized assets and stablecoin issuance, benefiting from mature compliance standards, deep liquidity, and established settlement infrastructure.

Base further strengthens that advantage through its compliant token framework, simplifying regulated asset issuance.

Meanwhile, Solana continues narrowing the gap through stronger stablecoin growth and improved finality, while Avalanche attracts institutions seeking dedicated blockchain environments.

Those improvements broaden competition without immediately displacing existing leaders.

As these upgrades move from deployment to production throughout 2026 and 2027, institutions will increasingly judge networks by operational resilience rather than theoretical performance.

The blockchain that consistently delivers reliable settlement, regulatory compatibility, and uninterrupted service during periods of market stress is likely to attract the greatest share of future tokenized capital, regardless of which network processes transactions the fastest.

Final Summary

- Blockchain infrastructure upgrades, led by Ethereum [ETH], are shifting competition toward institutional readiness instead of transaction speed.

- Blockchain networks, including Ethereum, will increasingly compete on reliability, compliance, and real-world institutional adoption.