Every Monday to Friday morning, focusing on macro trends, U.S. stocks, AI, precious metals, and crude oil, using data to review the market and trends to seize opportunities, presented by PANews.

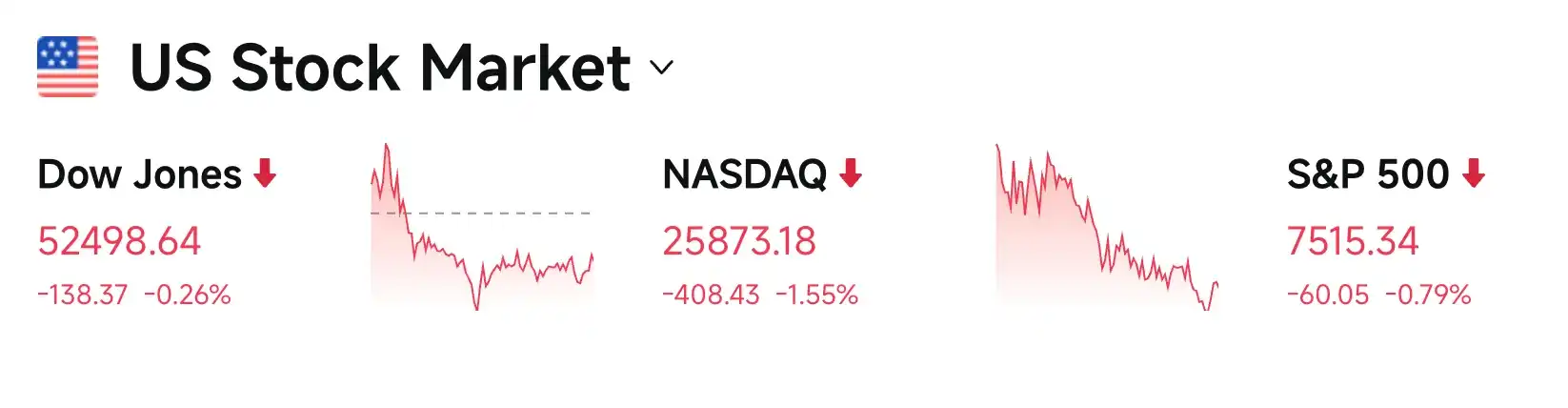

Last night and this morning, the sharp escalation of geopolitical conflicts and the Federal Reserve's unexpectedly hawkish stance led to a brutal 'stocks and bonds sell-off' in the market. Tech stocks were the hardest hit, dragging the Nasdaq Composite Index down sharply by 1.55% to 25,873.18 points, directly falling below its 50-day moving average. The S&P 500 and Dow Jones Industrial Average were not spared either, falling 0.79% and 0.26% respectively. Deeply intertwined anxiety over AI capital expenditure and macro safe-haven demand drove the VIX fear index up over 14%.

U.S. Conducts Fresh Airstrikes on Iran and Plans to Enforce Maritime Blockade, Crude Oil Soars 9%

The Middle East situation continues to dominate market sentiment, with the U.S. conducting airstrikes on Iran for three consecutive nights and planning to destroy a fortified underground nuclear facility named 'Gao Shan.' Furthermore, starting from 4 a.m. on July 15, the U.S. will implement a maritime blockade on all Iranian ports and coastal areas, and plans to impose a 20% transit fee on all cargo passing through the Strait of Hormuz. These remarks, coupled with rumors of a downed drone, instantly ignited the crude oil market.

Wall Street traders frantically restarted the 'NACHO (Never Again Channel Opening of Hormuz) trade,' betting that this global artery would not return to calm anytime soon. Amid panic, WTI crude oil surged over 9% in a single day, breaking through the $80 per barrel mark; Brent crude oil also strongly stood above $85, marking its biggest single-day gain since 2020. Despite the intensified conflict, Trump stated that there is still a possibility for both sides to reach an agreement.

Goldman Sachs warned that the core market contradiction has shifted from 'whether the channel opens' to 'who gets to decide.' Their base case scenario remains that oil prices will stay within the $75-$85 range. However, if energy infrastructure like offshore drilling platforms also comes under attack, oil prices breaking through $100 is not a fantasy. Although the UAE's daily crude production surged by 80% in June (reaching 3.8 million barrels) and OPEC lowered its future demand forecasts, these bearish factors appear insignificant in the face of the current supply disruption panic.

Gold Plunges, Dollar and U.S. Treasuries Surge, Probability of July Rate Hike Nears 50%

Influenced by simultaneous increases in real interest rates and the dollar, gold plummeted nearly 3%, losing the psychological $4,000 per ounce level, with its safe-haven attributes temporarily yielding to dollar-denominated assets. The U.S. dollar index continued to strengthen, and U.S. Treasuries faced selling pressure. The 2-year Treasury yield soared 1.7%, breaking above 4.29%, a multi-year high; the 10-year Treasury yield also rose 1.4% to climb to 4.62%. Bloomberg analysts noted that inflation expectations fueled by the oil price surge have completely overshadowed gold's safe-haven appeal.

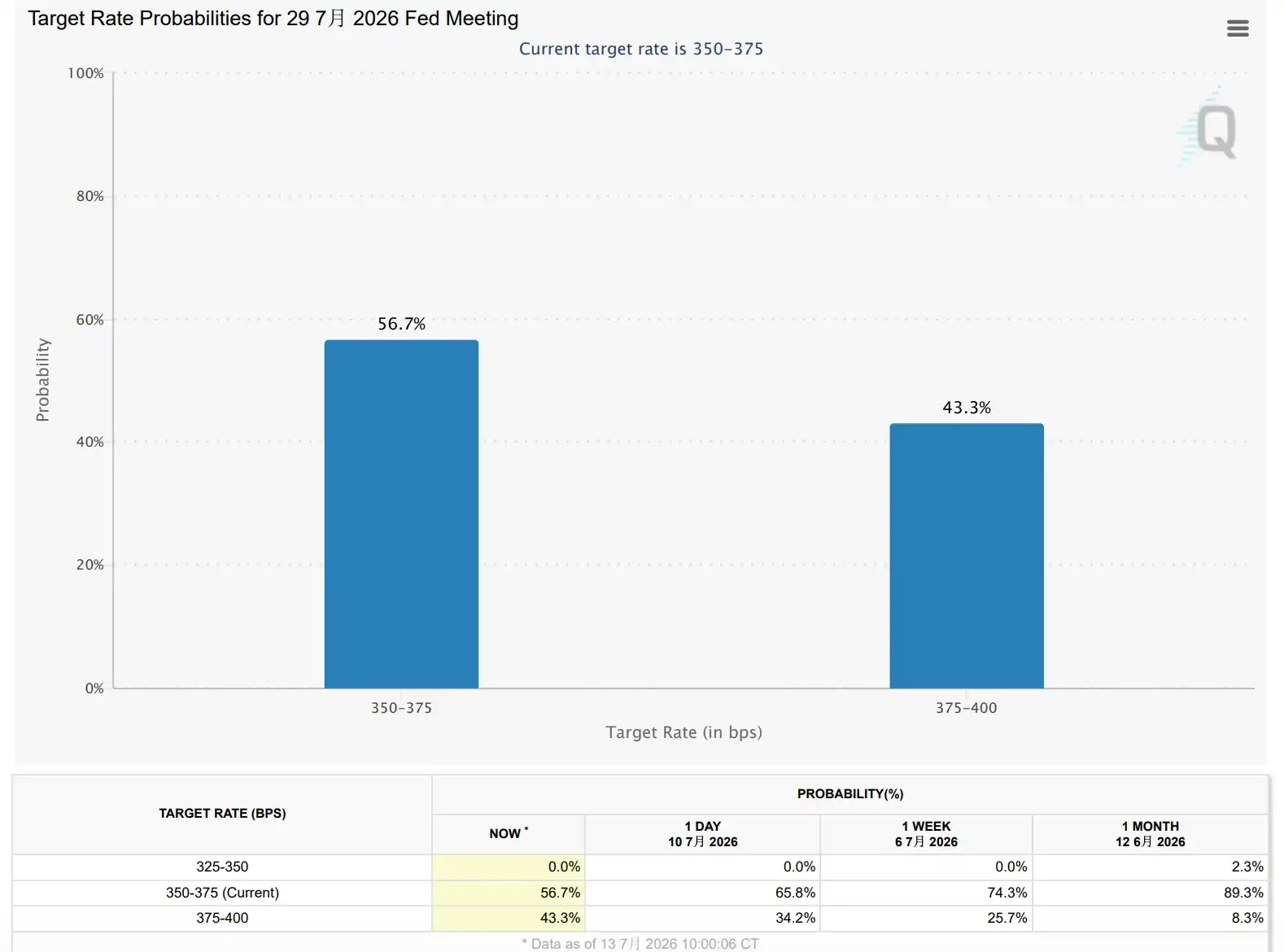

Interest rate swap markets indicate that the probability of a 25 basis point rate hike by the Federal Reserve in July is now close to 50%, up significantly from less than 40% previously; the probability of at least two rate hikes before year-end has also risen to 56%.

Federal Reserve Governor Waller stated that if future inflation data shows price pressures expanding again, the Fed might need to raise rates again in the near term. BMO Capital Markets believes the market now views the late-July FOMC meeting as a genuine policy inflection point.

Goldman Sachs noted that if the Fed resumes rate hikes, it would simultaneously suppress economic growth, increase financing costs for AI capital expenditures, and elevate market volatility, putting pressure on U.S. stock valuations for a repricing.

AI Trade Continues Cooling, U.S. Tech Sector Sees Sharp Volatility, Apple Hits New High Against the Trend

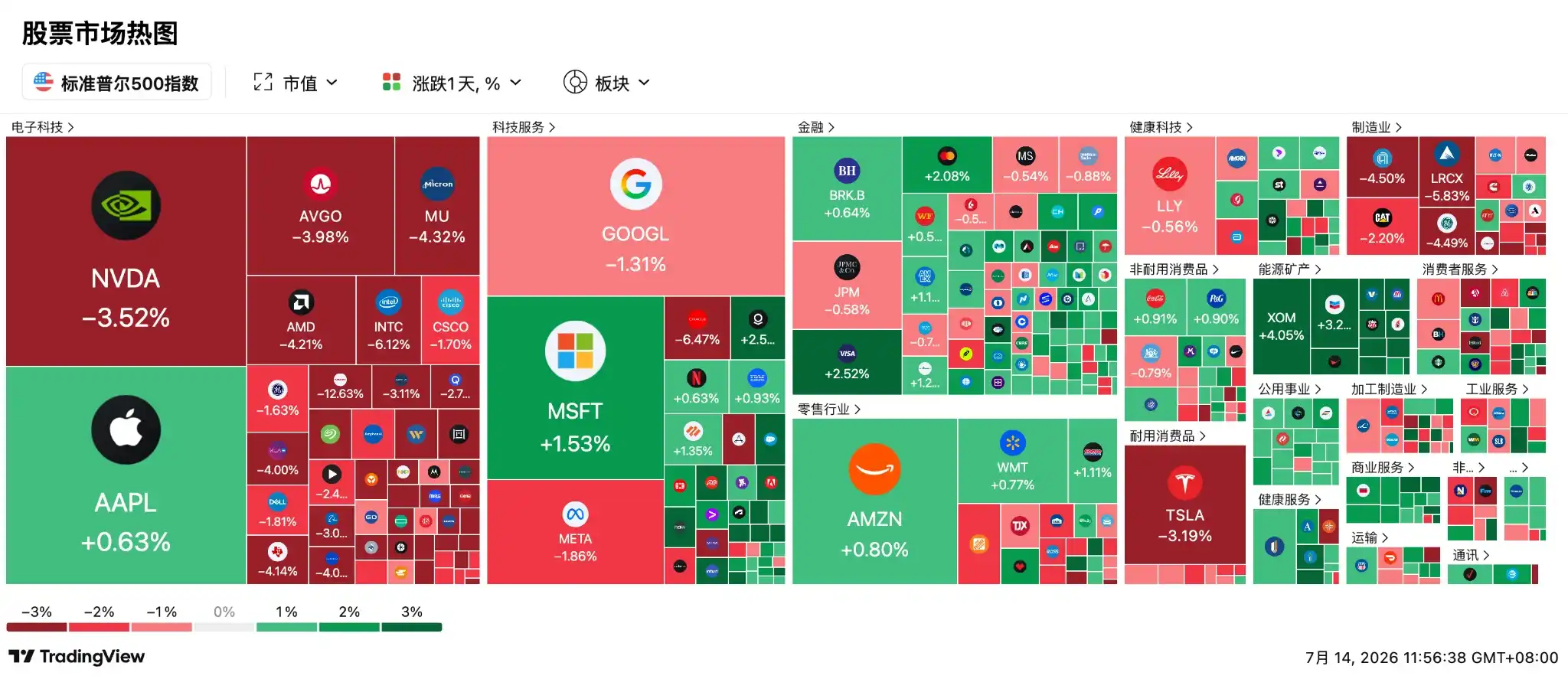

Under the triple pressure of U.S.-Iran geopolitical conflict, renewed hawkish Fed rate hike expectations, and concerns over the sustainability of AI capital expenditure, U.S. stock market internal structure experienced severe turbulence last night. Funds panic-sold from high-valuation chip and cloud service sectors, causing the Philadelphia Semiconductor Index to plunge 4% and the Nasdaq to lead the decline among major indices.

The semiconductor industry suffered heavy losses, with SK Hynix and Micron Technology leading the decline due to profit-taking and earnings forecast revisions. Nvidia and AMD fell between 3% and 5%. Market analysis suggests the AI 'computing power arms race' logic is facing a severe test, with investors beginning to reassess the profit realization capabilities of high-valuation tech stocks.

Specific Company Actions and Stock Price Movements:

-

SK Hynix ADR plunged 9% on its second trading day, with its domestic Korean stock price plummeting 15% in a single session, dragging down the global AI memory sector. The trigger for the crash was a bearish research report: Korea Investment & Securities pointed out that SK Hynix's high-bandwidth memory (HBM) contracts are long-term agreements with locked-in prices, meaning even if chip prices skyrocket now, they can only sell at the previously agreed lower prices. This has led to their Q2 profit expectations being far below market consensus. This 'fame without fortune' situation triggered a frantic sell-off by profit-takers.

-

The AI memory chain adjusted across the board, with SanDisk plunging over 12%, Western Digital down about 8%, Seagate down nearly 7%, and Micron down over 4%. As part of plans to expand U.S. domestic chip manufacturing investment, Micron took a stake in silicon wafer manufacturer GlobalWafers. Wall Street firm Wedbush believes the future AI bottleneck will shift from 'chip shortage' to 'silicon wafer shortage,' and Micron is preemptively securing core raw materials, building a deep moat.

-

GPU and AI chips also pulled back, with Nvidia falling 3.52%. The market is beginning to worry that cloud computing giants might not be able to afford so many expensive AI chips. However, Morgan Stanley maintains its $300 price target, insisting competitors' custom chips cannot yet challenge Nvidia's dominance. AMD also tumbled 4.21%, but institutions like Bank of America remain bullish against the trend, raising their price target to $620, citing AMD's server processors gaining significant market share, with promising Q3 shipment volumes. TSMC fell nearly 3%, announcing continuous expansion of advanced packaging bases, with the Chiayi park potentially becoming the world's largest advanced packaging production base. Additionally, Broadcom fell about 3%, Marvell down nearly 7%, Arm down about 8%, ASML down nearly 3%, with Applied Materials, KLA, and Lam Research all down about 4%.

-

Intel slumped 6.12%, failing to recover even after announcing a €5 billion investment to expand AI capacity in Ireland.

-

Apple rose against the trend by 0.63% to $316.91, hitting a new all-time high. Top Goldman Sachs analysts noted that Apple, not deeply entrenched in the AI data center 'money-burning war,' has instead become the safest haven. Coupled with the upcoming foldable iPhone launch and recent price increases across its product line, Apple's valuation premium relative to the S&P 500 has reached its highest point in 15 years.

-

SpaceX fell for a second consecutive day, with cumulative losses nearing 9%, approaching its $135 IPO price. High valuation and massive losses led some investors to cash out. However, the good news is the U.S. Federal Aviation Administration (FAA) has given the green light, with the 13th Starship test flight scheduled for this Thursday.

-

U.S. solar giant Sunrun enters the 'selling computing power' arena. Amid the high demand and shortage of AI computing power, the company's CEO announced plans to transform millions of U.S. households with rooftop solar installations into 'distributed AI data centers.' Users can earn hundreds of dollars per month simply by contributing their home's micro computing nodes.

Key Events to Watch Next:

-

July 14, 20:30: U.S. June CPI Inflation Data. This is the undisputed most crucial data of the week. The market expects the year-on-year growth rate to drop from 4.2% to 3.8%. If the data comes in hotter than expected, the 'rate hike' mentioned by Fed governors could become a reality, sending U.S. Treasury yields soaring again and likely triggering another round of tech stock sell-offs.

-

July 14, 22:00: Fed Chair Waller's Congressional Hearing. As the grand finale of 'Super Tuesday,' after reviewing the latest CPI data, Waller will provide his first insights to Congress. Whether his testimony leans towards maintaining the status quo or strongly advocating for rate hikes will directly set the tone for the final direction of the FOMC meeting two weeks later.

-

July 14: Key Bank Earnings Season Kicks Off. JPMorgan Chase, Bank of America, Citigroup, Wells Fargo, and Goldman Sachs Group will release results. Amid current concerns over high interest rates and economic slowdown, whether these Wall Street giants can maintain their net interest income will be a benchmark for testing the resilience of the U.S. financial system.

-

July 15, 4:00 a.m.: U.S. Military Officially Reinstates Maritime Blockade on Iran. Trump's sanction hammer officially falls. The actual intensity of the blockade in these hours and Iran's response will directly determine the fate of navigation through the Strait of Hormuz.

-

July 16: TSMC Q2 Earnings Report and SpaceX's 13th Starship Test Flight. TSMC's earnings are more than just a financial report; they reveal the state of global AI advanced packaging capacity, directly verifying whether the AI boom is a bubble or real gold. Meanwhile, the outcome of SpaceX's launch will determine if this aerospace unicorn can achieve a new round of valuation re-rating.