Author: Tanay Jaipuria, Partner at Wing

Compiled by: Felix, PANews

Editor's Note: On May 25th, the Shanghai Stock Exchange website showed that Unitree Robotics' IPO on the STAR Market will undergo a review on June 1st, planning to raise $620 million, aiming to become the first A-share humanoid robot company.

Unitree's prospectus is highly noteworthy because it effectively presents the true current state of the robotics market development.

As the company with the highest global shipment volume of humanoid robots, Unitree is not only profitable but also maintaining rapid growth. This article will explore:

-

Unitree Robotics' products

-

The shift in revenue structure towards humanoid robots

-

Which companies are currently buying robots (and why)

-

The vertically integrated business model

-

Financial analysis

-

Model-layer development goals

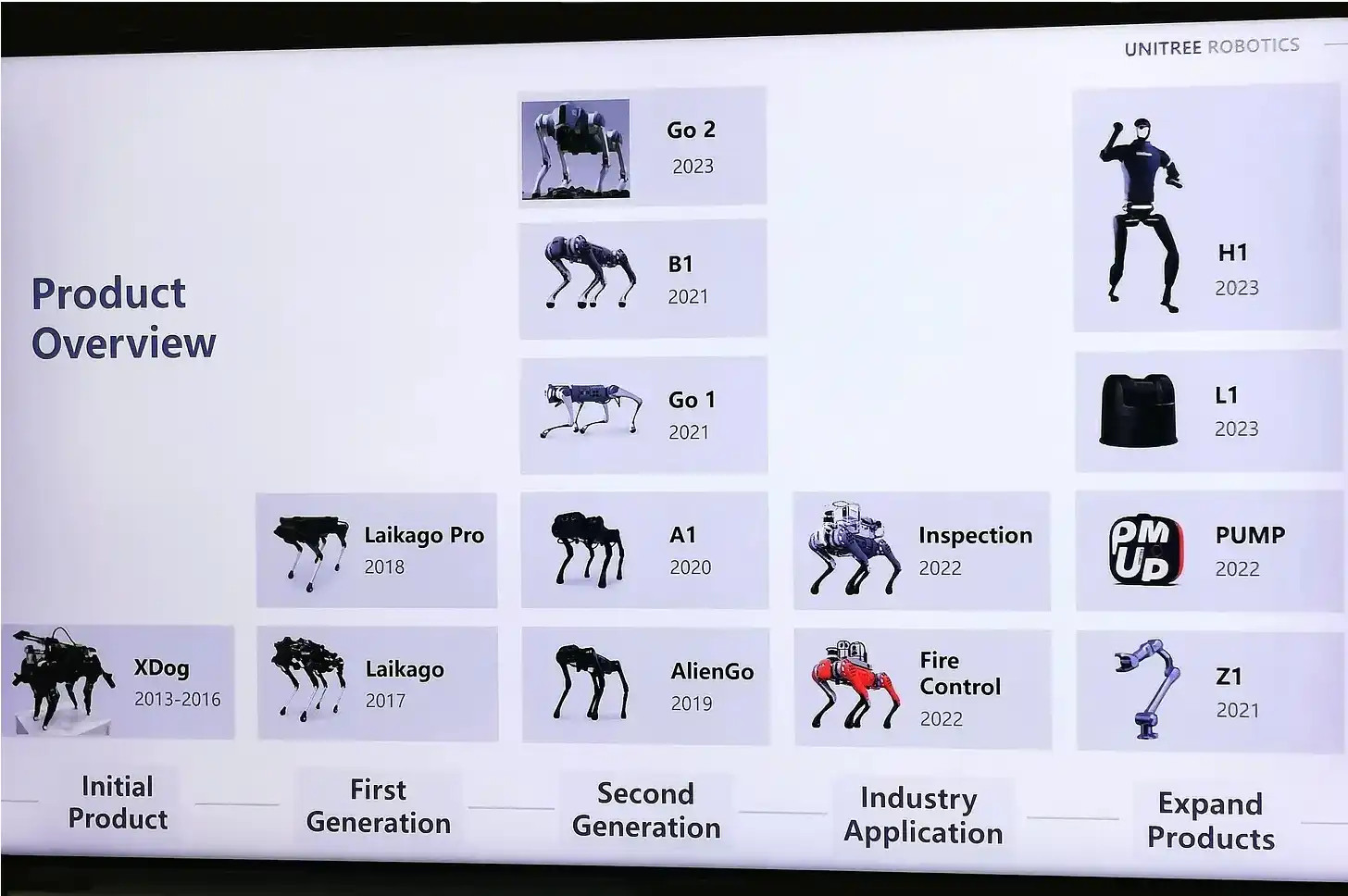

Unitree Robotics' Products

Unitree Robotics was founded in 2016 in Hangzhou. Its founder, Wang Xingxing, is a self-taught robotics expert known for building the first quadruped robot in his apartment. The company currently has 480 employees, including about 175 R&D personnel.

The company primarily sells two major product lines:

-

Quadruped Robots (Robotic Dogs): Go2 (consumer and research grade), B2 (industrial grade), and A2.

-

Humanoid Robots: H1, H2, G1, and R1. You might have seen G1 in viral videos online; it is 1.32 meters tall and weighs 35 kilograms.

The company began international operations in 2018. Over 35% of its revenue comes from outside China, including a significant customer base in the US academic sector.

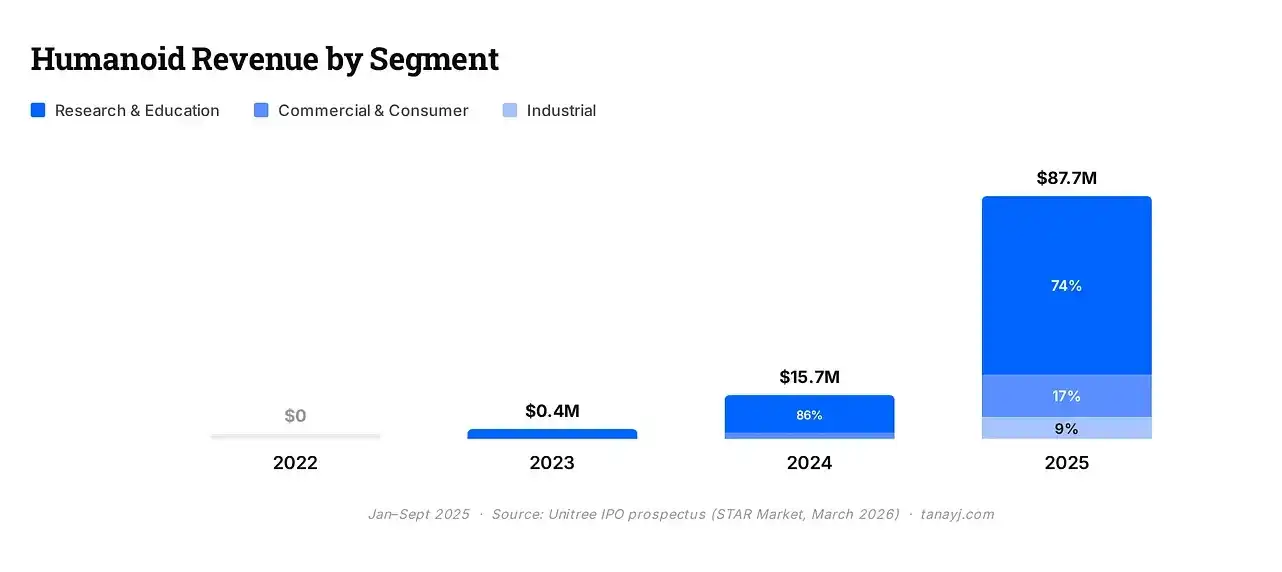

Transition to Humanoid Robots

Two years ago, Unitree Robotics was essentially a robotic dog company, mainly selling quadruped robots. In 2023, humanoid robots accounted for only 1.9% of its revenue.

However, by the first three quarters of 2025, humanoid robots already made up over half of its revenue.

This shift was driven by product-market fit and aggressive marketing. The company's humanoid robots have appeared on CCTV's Spring Festival Gala for two consecutive years. In 2024, Jensen Huang also showcased a Unitree robot at the GTC conference.

Unitree robots performing on CCTV's Spring Festival Gala

This brand exposure has successfully translated into commercial and research demand—something most Chinese hardware companies have rarely achieved.

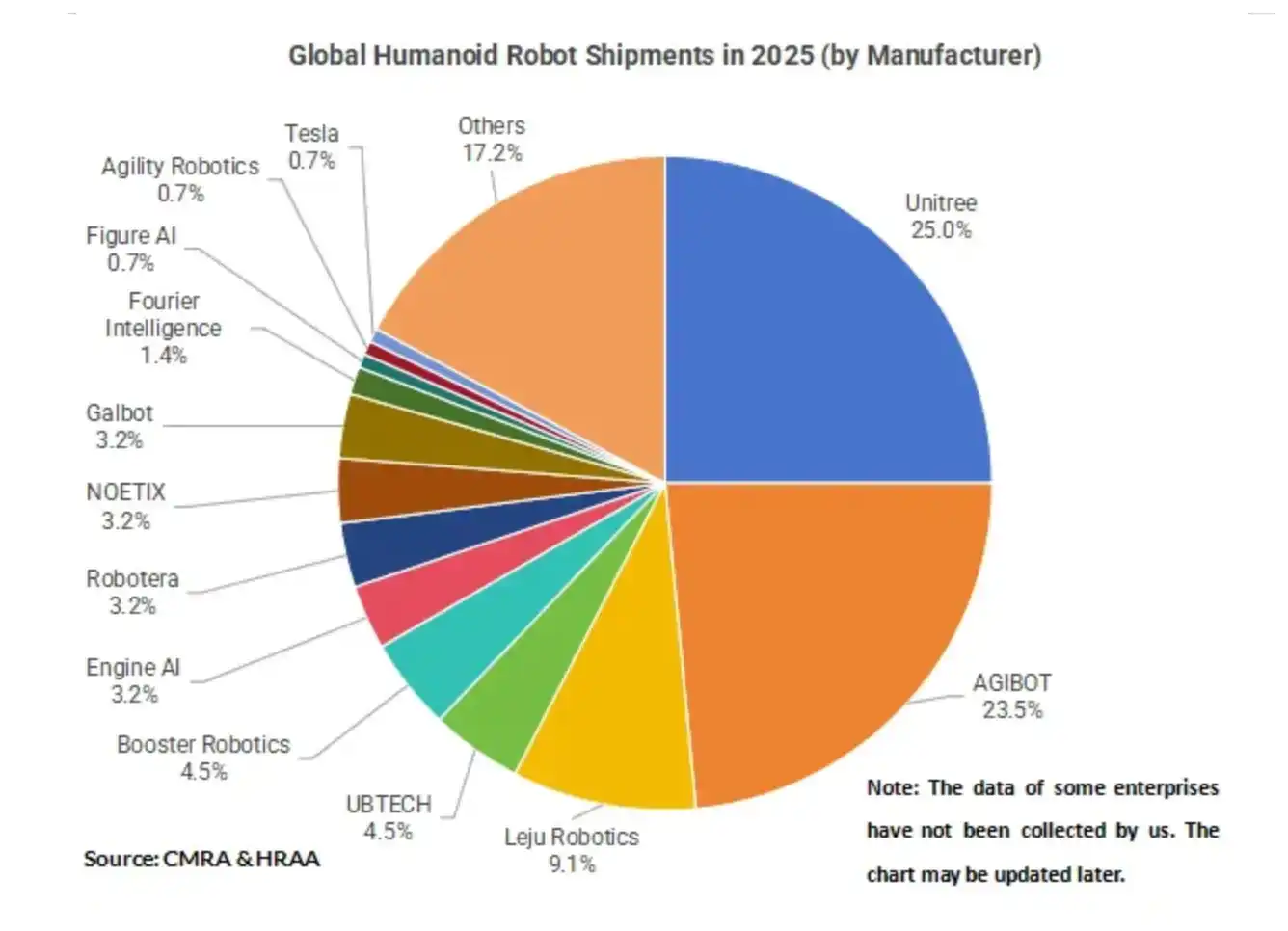

Unitree's shipment volume for humanoid robots is particularly impressive compared to other companies. Unitree sold approximately 5,500 humanoid robots in 2025, making it the world's largest seller of bipedal humanoid robots. AGIBot from China follows closely behind. In contrast, well-known US companies like Figure AI and Agility Robotics likely only sold a few hundred units each (or even less).

The prospectus sets a 5-year target of producing 75,000 humanoid robots and 115,000 quadruped robots annually. This is about 14 times the 2025 production volume for humanoid robots. This goal is ambitious but also highlights that the industry is still in its very early stages.

Who is Buying Robots

The prospectus categorizes buyers into three groups: Research & Education, Commercial & Consumer, and Industrial Applications.

The stark reality is that most current demand for humanoid robots is concentrated in research and education scenarios.

1. Research & Education: Accounts for 74% of humanoid robot revenue/unit sales. Academic buyers have been Unitree's primary customer segment since 2022 and remain the largest source of the company's total revenue.

2. Commercial & Consumer: Accounts for 17% of humanoid robot unit sales. Non-academic consumers buying these robots mostly use them for "display": acting as eye-catching promoters in retail spaces, tourist attractions, performances, and exhibitions. In the first nine months of 2025, consumer-level revenue increased nearly fourfold year-over-year, which sounds impressive but started from a very small base. Today, the most realistic application for a $25,000 humanoid robot seems to be standing at the entrance of a store in Shenzhen to attract customers.

3. Industrial Applications: Accounts for only 9% of humanoid robot unit sales. Unitree also acknowledges that industrial deployment is relatively limited due to immature technology, reflecting the current state of the art. Within this 9%, about 50%-70% is used for scenarios like corporate reception and tour guides. Therefore, comprehensively, the shipment volume of humanoid robots truly used for practical tasks like corporate reception and inspection constitutes only 3%-4%.

The prospects are more promising for quadruped robots (robotic dogs): only about one-third of sales come from research, over 40% from commercial use, and the remainder from industrial use. In this field, production application scenarios are already more mature. Its clients include State Grid, China Southern Power Grid, PetroChina, Sinopec, Baowu Group, and JD.com (JD.com is Unitree's largest customer). These companies use quadruped robots for genuine daily inspections of chemical plants, substations, coal mines, pipelines, etc.

Unitree quadruped robots used for inspection tasks

Vertically Integrated Business Model

One of the unique aspects of Unitree Robotics is its ability to independently design and manufacture most core components: high-torque motors, precision reducers, encoders, joint modules, intelligent controllers, high-precision sensors, dexterous hands, LiDAR, and cameras. According to McKinsey data, actuators (i.e., motors, reducers, and joint systems that drive robot movement) typically account for 40%-60% of the total Bill of Materials (BOM) cost for a humanoid robot.

Most companies in this field rely on external sourcing, while Unitree manufactures in-house. Externally purchased components account for only about 14%-18% of its total cost. It outsources only generic parts like battery cells, flash memory, and differentiated components like core computing boards.

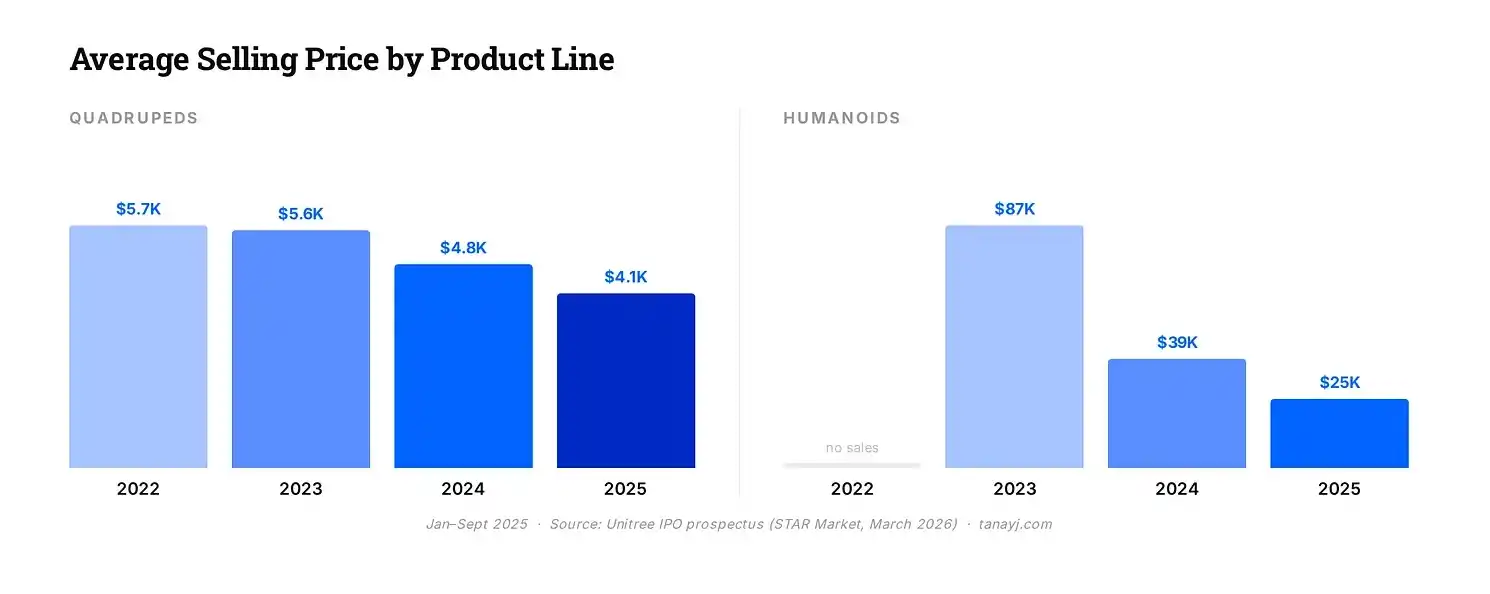

Thanks to this, the unit manufacturing cost for quadruped robots dropped from about $3,300 in 2022 to around $1,800 in mid-2025, a decrease of 46%. During the same period, the cost for humanoid robots also decreased from about $10,800 to $9,200.

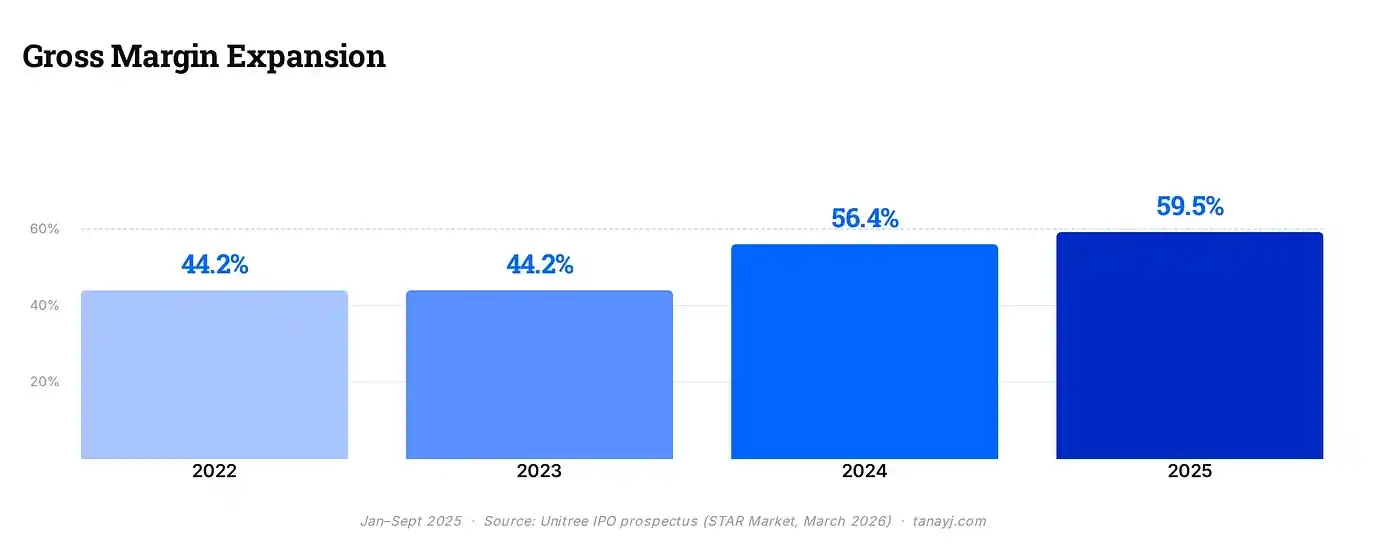

Interestingly, as shown in the chart below, although the Average Selling Price (ASP) for both quadruped and humanoid robots has declined year by year, their gross margin has actually increased throughout the period due to their highly vertical integration strategy: soaring from around 45% in 2022-2023 to nearly 60% in 2025.

Note: Unitree sold only 5 humanoid robots in 2023, so the ASP for that year is not representative.

Financial Overview

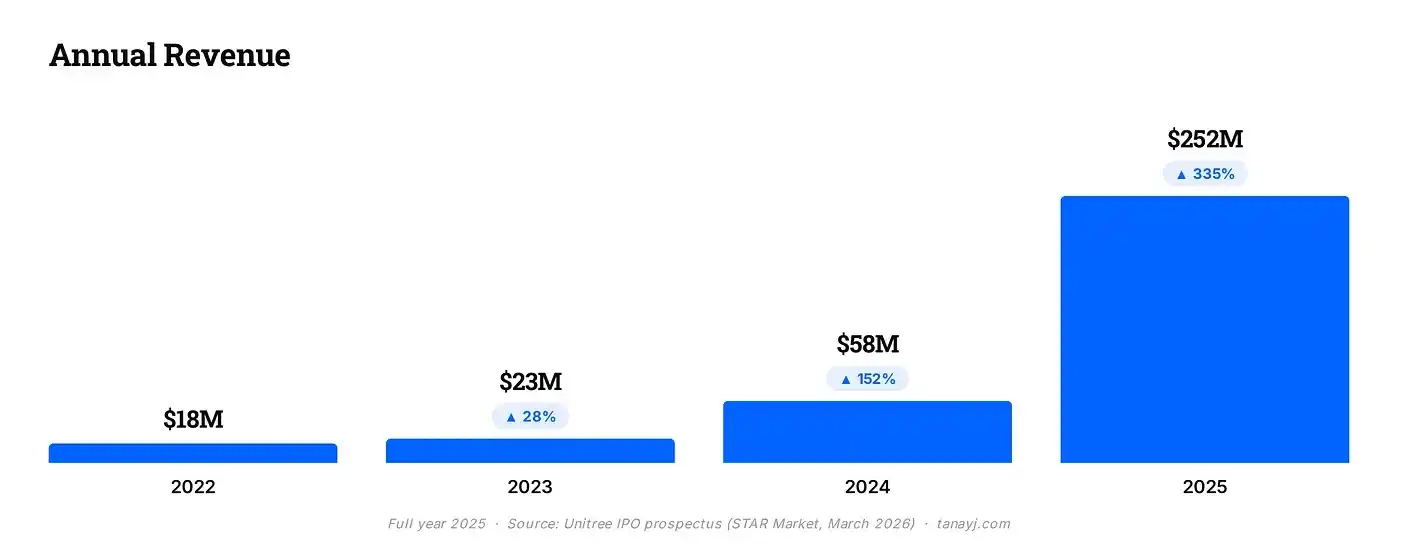

Driven by strong growth in the humanoid robot business, the company's revenue skyrocketed from $58 million in 2024 to approximately $252 million in 2025, an increase of 335%. For most of its history, international sales accounted for over 55% of revenue. In 2025, domestic Chinese market revenue surpassed exports for the first time, although overseas export revenue still doubled year-over-year in absolute terms.

The gross margin is close to 60% and has been increasing in recent years, as detailed below.

For comparison: most hardware companies have gross margins in the 30%-40% range, while software companies typically achieve 70%-80%. For a company selling physical robots, Unitree's gross margin is quite high, entirely thanks to their vertical integration model and the strong differentiation of their current products.

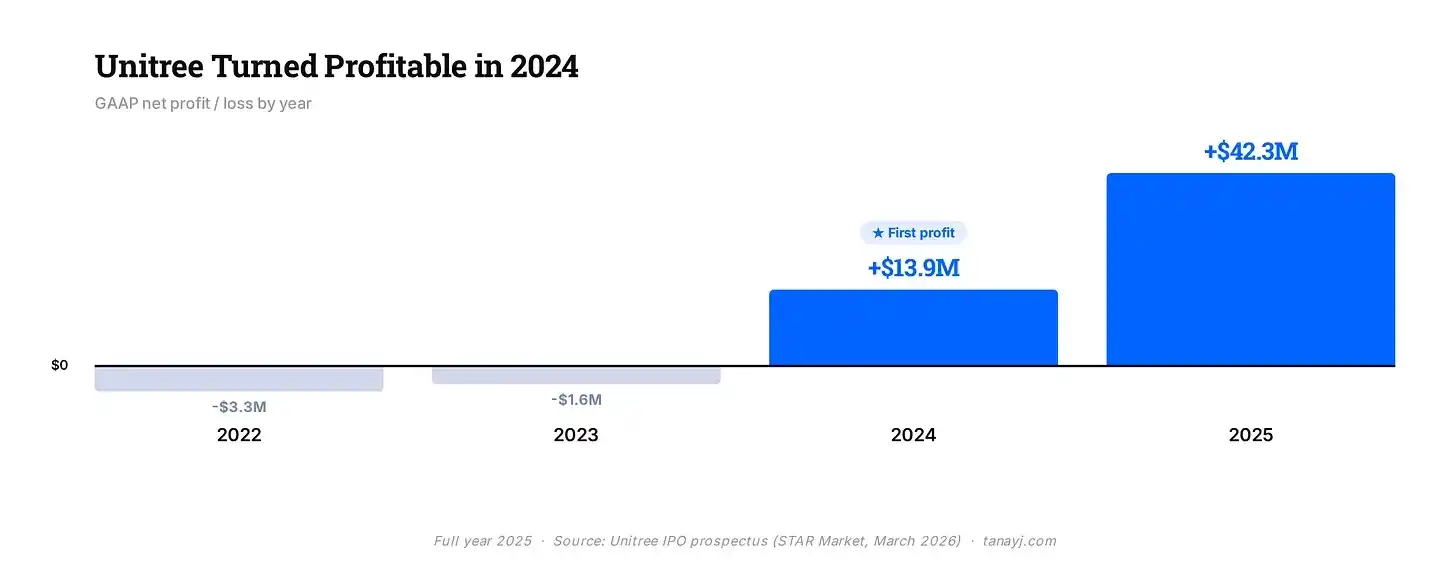

The company became profitable in 2024 (under US GAAP) with a profit margin of about 18%, and close to 35% on an adjusted basis.

Unitree Robotics' target valuation in this IPO is approximately $6 to $7 billion.

Model-Layer Vision

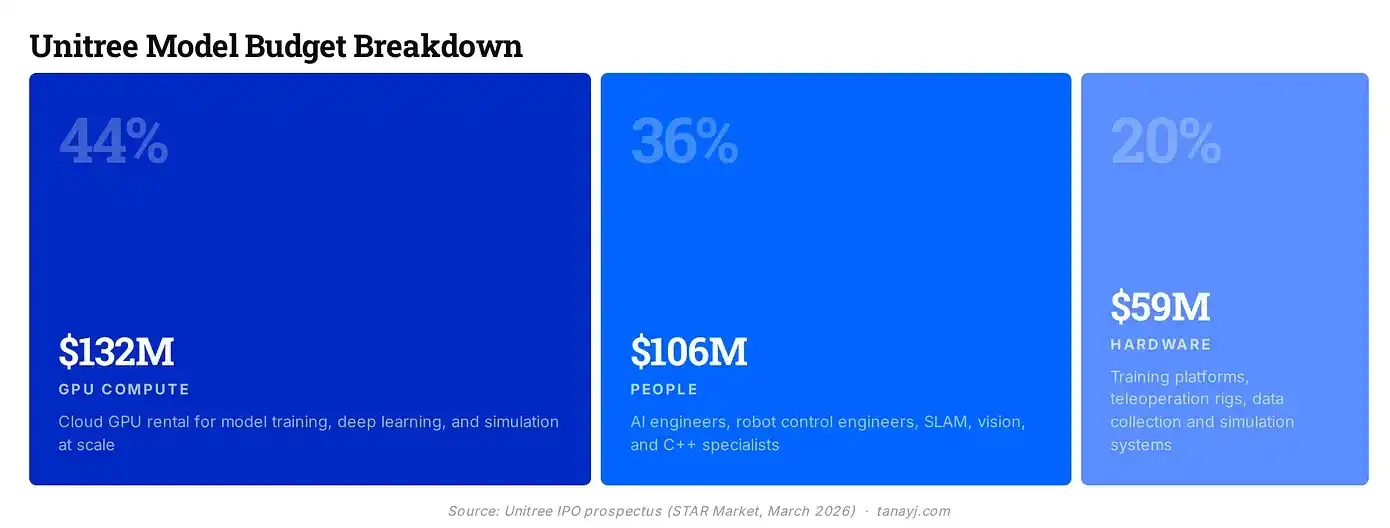

Unitree plans to invest nearly half of its IPO proceeds into software development. Of the $620 million raised, about $300 million is designated for AI model training over the next three years, equating to roughly $100 million per year for developing an "Embodied Large Model."

The prospectus describes two parallel model architectures:

-

The first is the VLA (Vision-Language-Action) Model: This model directly maps visual and language inputs to motion commands, enabling robots to generalize and handle unfamiliar tasks without manually written code instructions.

-

The second is the WMA (World Model + Action) Model: Unitree sees this as the more promising approach. The WMA model can construct internal simulations of physical reality. The robot predicts what will happen before taking action, rather than learning purely through trial and error.

Unitree has already released initial versions of these two models. In September 2025, Unitree open-sourced UnifoLM-WMA-0; in January 2026, it open-sourced UnifoLM-VLA-0.

Unitree also detailed the approximate expenditure breakdown for this model, as shown below:

Unitree's current lead in hardware is undeniable. However, the company recognizes that to maintain a lasting moat in robotics, it may be necessary to also control the model layer: the "brain" system that determines what the robot does and how it moves. Furthermore, its software ambitions serve as a hedge against hardware commoditization (low-price competition). Unitree has built a moat in hardware manufacturing.

However, if actuators and joint modules eventually become standardized components like batteries in electric vehicles, the industry's defenses and competitive barriers will inevitably shift to the model layer.

Conclusion

Unitree Robotics has a profitable hardware business, a solid manufacturing moat, and more humanoid robots than any other company, all at highly competitive prices. However, as reflected in the actual uses of humanoid robots, widespread commercial adoption is still in its infancy. "Display-type" applications dominate consumer demand, while industrial deployment remains relatively limited.

Unitree Robotics offers a glimpse into the current state of the robotics market, and more breakthroughs in models, hardware, and application scenarios are anticipated in the future.

Related Reading: An Overview of Over 30 Humanoid Robot Companies: Who Will Stand Out in 2026?