At the beginning of 2025, the Bitcoin (BTC) market was filled with fervent optimism. Institutions and analysts collectively bet that the price would soar above $150,000 by year-end, even reaching $200,000+ or higher. But reality staged a "contrarian" drama: BTC plummeted over 33% from its October peak of approximately $126,000, entered a "bloodbath" mode in November (a 28% monthly drop), and stabilized around $92,000 on December 10th.

This collective miscalculation warrants a deep review: Why were the predictions so unanimous at the start of the year? Why did almost all major institutions get it wrong?

I. Initial Predictions vs. Current Reality

1.1 The Three Pillars of Market Consensus

At the beginning of 2025, the Bitcoin market was permeated with unprecedented optimism. Almost all major institutions set year-end target prices above $150,000, with some aggressive forecasts pointing directly to $200,000-$250,000. This highly consistent bullish expectation was built on three "certain" logics:

Cyclical Factor: The Halving Curse

Historically, price peaks have often occurred 12-18 months after a halving. After the 2012 halving, the price rose to $1,150 in 13 months; after the 2016 halving, it broke $20,000 in 18 months; after the 2020 halving, it reached $69,000 in 12 months. The market widely believed that the supply-side contraction effect would manifest with a lag, and 2025 was right in this "historic window."

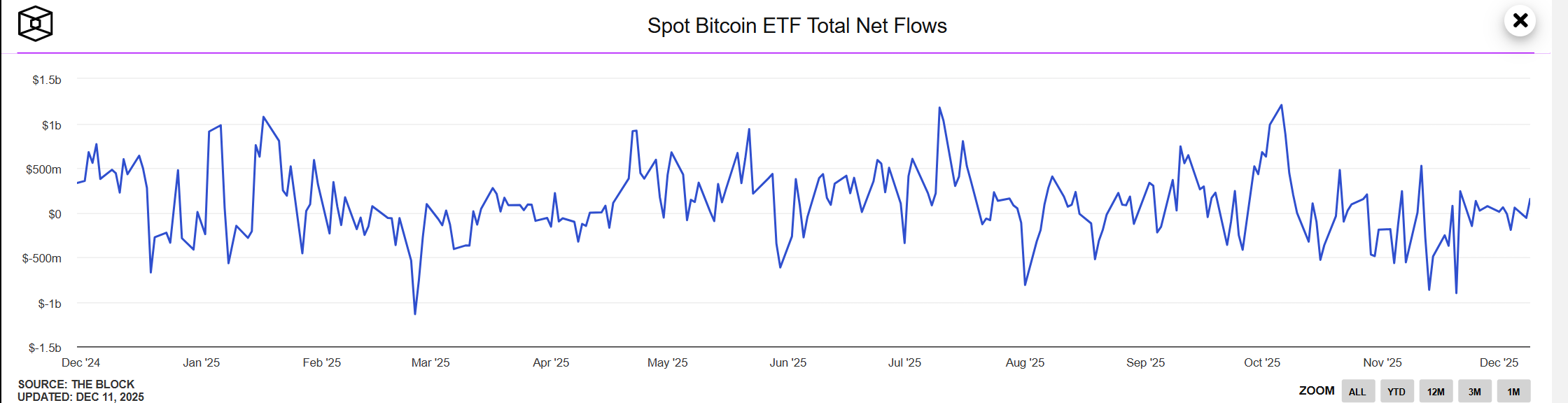

Capital Flow Expectations: The ETF Flood

The approval of spot ETFs was seen as the opening of the "institutional capital floodgates." The market expected cumulative net inflows to exceed $100 billion in the first year, with traditional funds like pensions and sovereign wealth funds making large-scale allocations. Endorsements from Wall Street giants like BlackRock and Fidelity made the "Bitcoin mainstreaming" narrative deeply convincing.

Policy Tailwinds: The Trump Card

The Trump administration's friendly stance towards crypto assets, including discussions on strategic Bitcoin reserve proposals and expectations of SEC personnel changes, was seen as long-term policy support. The market believed regulatory uncertainty would significantly decrease, clearing obstacles for institutional entry.

Based on these three logics, the average year-end target price from major institutions reached $170,000, implying an expected annual gain of over 200%.

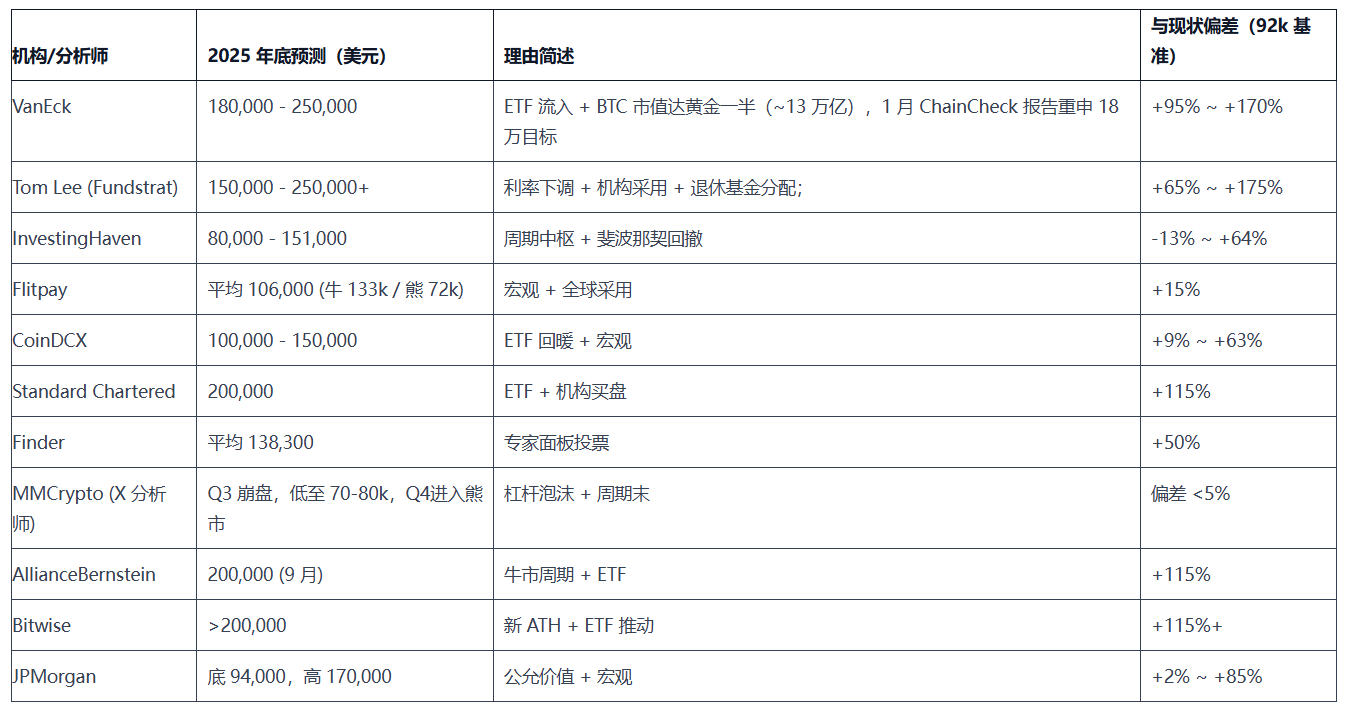

1.2 Panorama of Institutional Predictions: Who Was Most Aggressive?

The table below summarizes the initial predictions from 11 major institutions and analysts, contrasting them with the current price ($92,000), making the deviation clear:

Prediction Distribution Characteristics:

- Aggressive Camp (8 institutions): Target price $150k+, average deviation over 80%, represented by VanEck, Tom Lee, Standard Chartered

- Moderate Camp (2 institutions): JPMorgan gave a prediction range, Flitpay provided bull/bear scenarios, reserving room for downside

- Contrarian Camp (1 institution): Only MMCrypto explicitly warned of crash risk, becoming the only accurate predictor

Notably, the most aggressive predictions came from the most well-known institutions (VanEck, Tom Lee), while the accurate prediction came from a relatively niche technical analyst.

II. Roots of Misjudgment: Why Institutional Predictions Failed Collectively

2.1 The Consensus Trap: When "Good News" Loses Marginal Effect

9 institutions unanimously bet on "ETF inflows," forming a highly homogenous prediction logic.

When a factor is fully recognized by the market and reflected in the price, it loses its marginal driving force. By early 2025, the expectation of ETF inflows was completely priced in—every investor knew this "positive," and the price had already reacted in advance. The market needed "better than expected," not "as expected."

Full-year ETF inflows fell short of expectations, with ETFs seeing net outflows of $3.48-$4.3 billion in November. More critically, institutions overlooked that ETFs are a two-way street—when the market turns, they not only fail to provide support but become a highway for capital flight.

When 90% of analysts are telling the same story, that story has already lost its alpha value.

2.2 Cycle Model Failure: History Doesn't Simply Repeat

Institutions like Tom Lee and VanEck heavily relied on the historical pattern of "price peaks 12-18 months post-halving," believing the cycle would automatically play out.

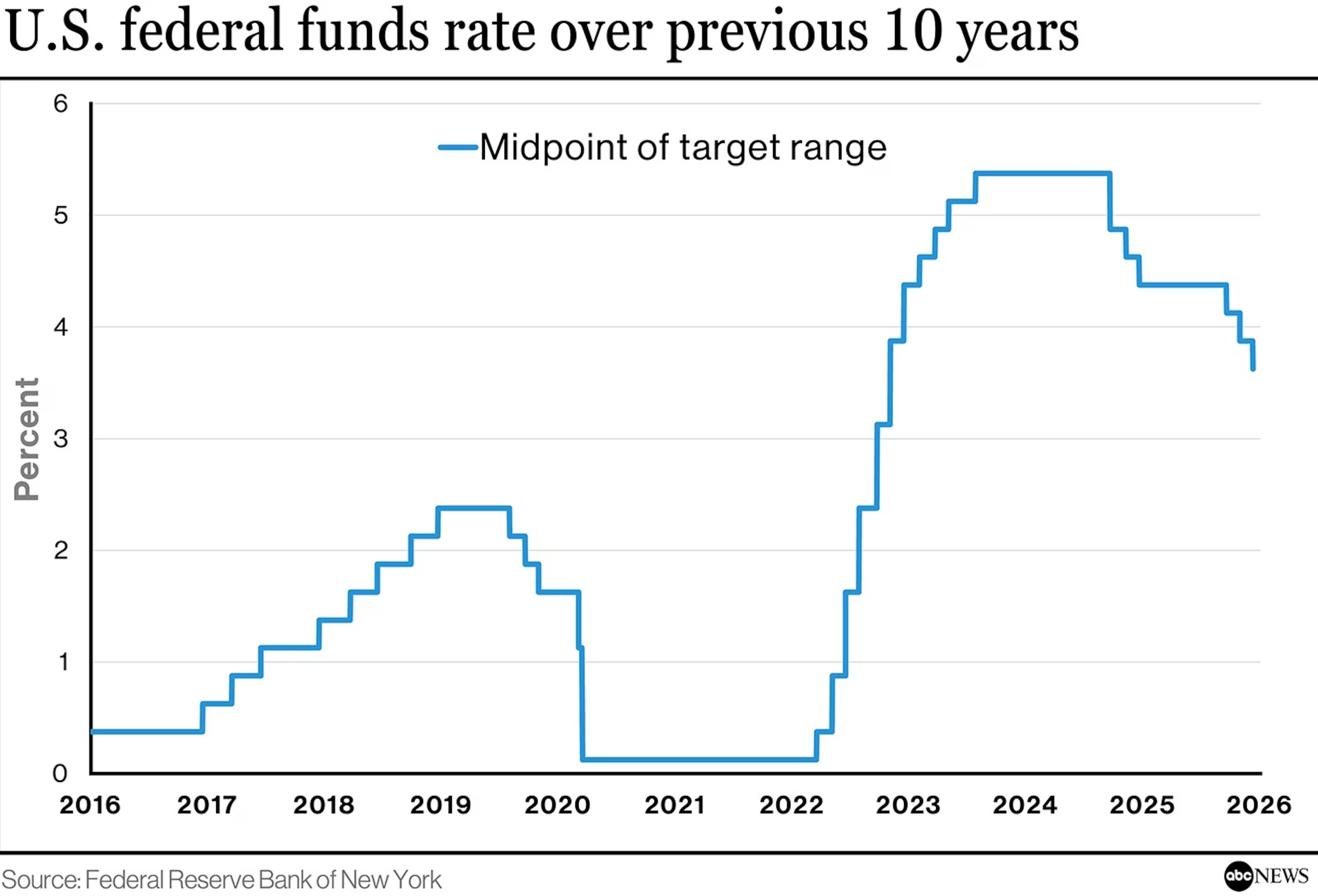

Radically Changed Environment: The macro environment in 2025 was fundamentally different from past cycles:

- 2017: Global low interest rates, loose liquidity

- 2021: Pandemic stimulus, central bank money printing

- 2025: Aftermath of the most aggressive rate-hiking cycle in 40 years, Fed maintaining a hawkish stance

Expectations for Fed rate cuts plummeted from 93% at the start of the year to 38% by November. This kind of abrupt shift in monetary policy had never occurred in historical halving cycles. Institutions treated the "cycle" as a deterministic rule, ignoring that it is essentially a probability distribution and highly dependent on the macro liquidity environment.

When the environmental variables change fundamentally, historical models inevitably fail.

2.3 Conflict of Interest: Structural Bias in Institutions

Top institutions like VanEck, Tom Lee, and Standard Chartered had the largest deviations (+100% or more), while niche players like Changelly and MMCrypto were the most accurate. Institution size often inversely correlates with prediction accuracy.

Root Cause: These institutions are stakeholders themselves:

- VanEck: Issues Bitcoin ETF products

- Standard Chartered: Provides crypto asset custody services

- Fundstrat: Serves clients holding crypto assets

- Tom Lee: Chairman of Ethereum treasury BMNR

Structural Pressures:

- Being bearish is biting the hand that feeds. If they published bearish reports, it would be tantamount to telling clients "our products aren't worth buying." This conflict of interest is structural and unavoidable.

- Clients needed "$150k+" targets to justify holdings. The clients served by these institutions mostly entered the market at mid-bull cycle highs, with cost bases in the $80,000-$100,000 range. They needed analysts to give "$150k+" targets to prove their decisions were correct and to provide psychological support for holding or even adding to positions.

- Aggressive predictions get more media coverage. Headlines like "Tom Lee Predicts Bitcoin at $250k" obviously get more clicks and shares than conservative predictions. The exposure from aggressive predictions directly translates into institutional brand influence and business traffic.

- Famous analysts find it hard to reverse their historical stance. Tom Lee gained fame for accurately predicting Bitcoin's rebound in 2023, building a public image as a "bullish standard-bearer." In early 2025, even if he had reservations internally, it would be difficult to publicly reverse his optimistic stance.

2.4 Liquidity Blind Spot: Misjudging Bitcoin's Asset Properties

The market has long been accustomed to analogizing BTC as "digital gold," believing it is a hedge against inflation and currency devaluation. But in reality, Bitcoin behaves more like Nasdaq tech stocks, being extremely sensitive to liquidity: When the Fed maintains a hawkish stance and liquidity tightens, BTC's performance resembles high-beta tech stocks more than safe-haven gold.

The core contradiction lies in the inherent conflict between Bitcoin's asset characteristics and a high-interest-rate environment. When real interest rates remain high, the appeal of zero-yield assets systematically declines. Bitcoin generates no cash flow and pays no interest; its value relies entirely on "someone being willing to buy it at a higher price in the future." In a low-rate era, this wasn't a problem—after all, money in the bank earned little, so why not take a gamble.

But when the risk-free rate reaches 4-5%, the opportunity cost for investors rises significantly, and Bitcoin, a zero-yield asset, lacks fundamental support.

The most fatal misjudgment was that almost all institutions presupposed "the Fed's rate-cutting cycle is about to begin." The market pricing at the start of the year was for 4-6 rate cuts annually, totaling 100-150 basis points. But the data by November gave the complete opposite answer: rekindled inflation risks, collapsed rate cut expectations, the market shifting from expecting "rapid cuts" to pricing in "higher for longer." When this core assumption collapsed, all the optimistic predictions built on "loose liquidity" lost their foundation.

Conclusion

The collective failure of 2025 tells us: Precise prediction is itself a false proposition. Bitcoin is influenced by multiple variables like macro policy, market sentiment, and technical factors; no single model can easily capture this complexity.

Institutional predictions are not worthless—they reveal mainstream market narratives, capital expectations, and sentiment direction. The problem is, when predictions become consensus, consensus becomes a trap.

True investment wisdom lies in: Using institutional reports to understand what the market is thinking, but not letting them decide what you should do. When VanEck, Tom Lee, and others are collectively bullish, the question you need to ask is not "Are they right?" but "What if they are wrong?". Risk management always takes precedence over return prediction.

History repeats, but never simply copies. The halving cycle, ETF narrative, policy expectations—these logics all failed in 2025, not because the logic itself was flawed, but because the environmental variables fundamentally changed. Next time, the catalyst will have a different name, but the essence of market over-optimism will not change.

Remember this lesson: Independent thinking is more important than following authority, contrarian voices are more valuable than mainstream consensus, and risk management is more critical than precise prediction. This is the moat for long-term survival in the crypto market.