Tether has seen its Juventus buyout attempt rejected as majority stakeholder Exor has told the stablecoin giant its share is not for sale.

Tether Fails To Acquire Premier Italian Football Club Juventus

On Friday, Tether announced that it had submitted a proposal to acquire Juventus, one of the biggest football brands in the world. The stablecoin firm had previously acquired a 10% minority stake in the club, and with this new plan, it had intended to execute a full buyout.

The first stage had included a proposal to Exor, the holding company of the Agnelli family and majority stakeholder of Juventus. According to Reuters, Tether had offered the firm 2.66 euros per share, a notable premium above the then closing price of 2.19 euros.

In a press release, Exor has responded to Tether, saying that its board has unanimously rejected the bid for its 65.4% controlling stake in Juventus. “Exor reaffirms its previous, consistent statements that it has no intention of selling any of its shares in Juventus to a third party, including but not restricted to El Salvador-based Tether,” noted the company.

Founded in 1897, Juventus has established itself as one of the biggest football clubs globally, with a particularly memorable period of success coming during the 2010s, in which it won nine consecutive titles in the Serie A, the first division of Italian football.

With Exor turning down the deal, the USDT issuer will have to reconsider its approach to the club popularly dubbed as The Old Lady. So far, Tether hasn’t issued any statements in answer.

In the original announcement, Tether had announced that if the firm is able to acquire Exor’s stake, it will move to acquire the remaining shares of the club through a public tender offer at the same share price. This would put the total valuation of Juventus at about $1.17 billion.

Tether had also noted that in the event that the transaction is completed, it will also be prepared to invest 1 billion euros in the football club. “Tether is in a position of strong financial health and intends to support Juventus with stable capital and a long horizon,” said CEO Paolo Ardoino.

While The Old Lady enjoyed a strong period in the last decade, the 2020s haven’t been as kind. Since the 2019-20 season title win, Juventus hasn’t come close to becoming the Italian champion, with its best finish being third place during the 2023-24 season. Juventus also became part of a financial scandal in 2023, with Serie A punishing it with a 10-point deduction for false accounting. Thus, Tether’s interest has arrived when the club has been in a bit of a slump.

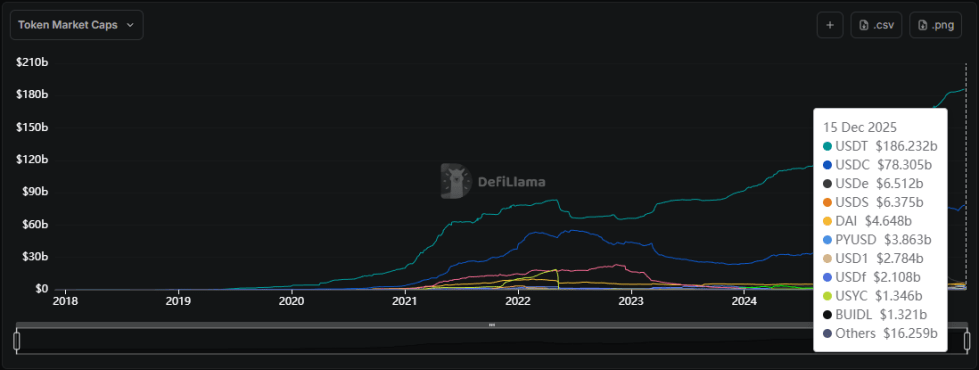

USDT, Tether’s stablecoin, has been experiencing growth recently, with its market cap hitting a new record of $186.23 billion, according to data from DefiLlama.

The trend in the market cap of USDT | Source: DefiLlama

Bitcoin Price

At the time of writing, Bitcoin is trading around $89,700, down 2.5% over the last week.

The price of the coin has retraced some of its recovery | Source: BTCUSDT on TradingView