Europe’s top central bank is watching stablecoins with growing caution. What began as a niche crypto tool is now large enough to draw attention in Frankfurt.

Based on reports, the European Central Bank has warned that wider use of privately issued digital tokens tied to major currencies could chip away at traditional bank deposits across Europe.

The concern is simple. If households and firms start parking more of their cash in stablecoins instead of bank accounts, lenders could end up with less money to fund loans.

Deposit Flight Could Strain Eurozone Banks

According to an ECB working paper cited by Reuters and other outlets, stablecoins may pull funds out of the banking system if people see them as safe and easy to use for payments or savings.

Even small shifts can matter. Eurozone banks rely heavily on deposits to finance mortgages, business credit, and consumer loans.

If deposits fall, banks may have to look for other funding sources. Those often cost more. When funding becomes more expensive, lending can slow, or borrowing rates may climb. That ripple effect could be felt by households and companies across the region.

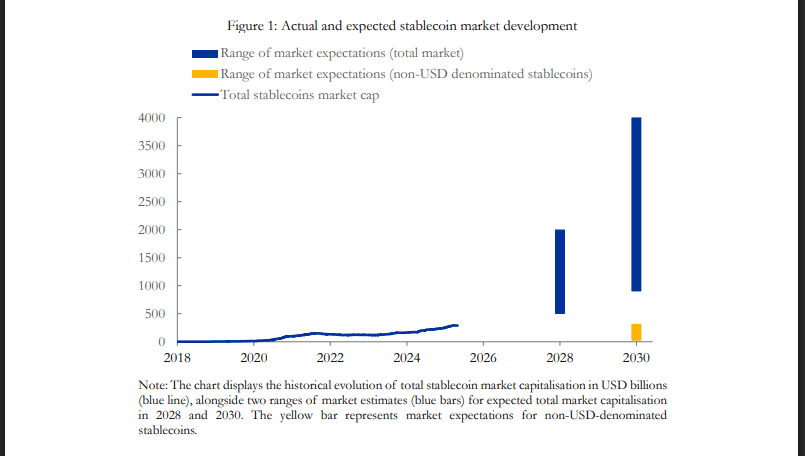

Source: ECB

Reports note that dollar-backed stablecoins are a particular worry. If Eurozone residents increasingly hold tokens linked to the US dollar, it may also weaken the role of the euro in daily transactions.

The ECB has long guarded its control over monetary policy. That control depends on how smoothly interest rate changes pass through the banking system.

It was stressed in the paper that a sharp rise in stablecoin adoption could weaken that transmission channel.

Monetary Policy Could Lose Some Bite

The ECB adjusts interest rates to cool inflation or support growth. Those decisions filter through banks, which adjust deposit and loan rates in response. If a chunk of savings sits outside the traditional system, that chain can be disrupted.

Based on reports, ECB researchers modeled scenarios where stablecoins capture a meaningful share of deposits. In such cases, the impact of rate hikes or cuts may become less predictable. Policy moves could take longer to influence spending and investment.

On Interference & Predictability

According to the report’s authors, they find that stablecoin adoption “interferes with multiple monetary policy transmission channels that would potentially weaken the predictability of policy actions.”

There is also a liquidity angle. During times of market stress, digital tokens can be moved quickly. Large outflows from banks into stablecoins, or back again, could amplify swings in funding conditions. That risk has been flagged before in global debates on crypto regulation.

The paper forms part of the ECB’s broader push to keep a close watch on stablecoins, a sector whose total market value has surged to more than $300 billion after more than doubling in the last three years. Forecasts suggest that figure could climb to $2 trillion by 2028.

European officials have not called for a ban. Instead, attention has focused on oversight. The European Union’s Markets in Crypto-Assets framework is already in place, setting rules for issuers and service providers.

Featured image from Unsplash, chart from TradingView