Original Author: David, Shenchao TechFlow

In 2020, after reading a book, MicroStrategy founder Michael Saylor decided to buy $425 million worth of Bitcoin.

This book is called "The Bitcoin Standard", published in 2018, translated into 39 languages, with over a million copies sold, and revered by Bitcoin enthusiasts as the "bible".

The author, Saifedean Ammous, holds a Ph.D. in Economics from Columbia University, and his core argument is singular:

Bitcoin is a "harder" form of hard currency than gold.

Simultaneously, on the book's promotional page, Michael Saylor's endorsement reads verbatim:

"This book is a work of genius. After reading it, I decided to buy $425 million worth of Bitcoin. It had the greatest impact on MicroStrategy's way of thinking, leading us to shift our balance sheet to a Bitcoin standard."

But there is one chapter in this book that is not about Bitcoin. It explains why silver cannot become hard currency.

Eight years later, today, silver has just surged to a historical high of $117 per ounce, and the investment frenzy in precious metals continues, with even Hyperliquid and a host of CEXs starting to list precious metals contracts in various forms.

Often at times like these, there are always be people acting as whistleblowers or defectors to warn of risks, especially in an environment where everything is rising except Bitcoin.

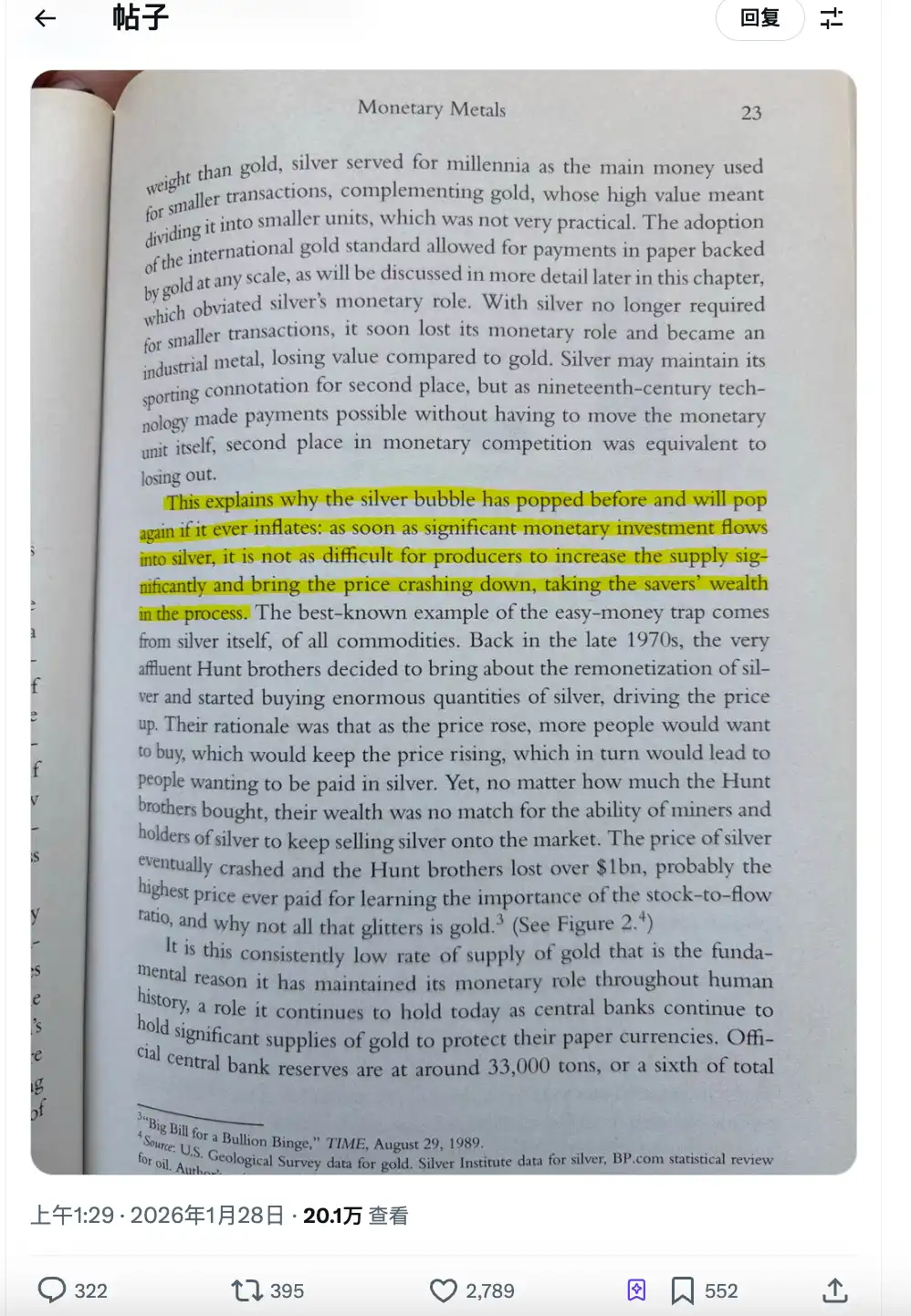

For example, a widely circulated post on Crypto Twitter today cited a screenshot from page 23 of this book, with a highlighted paragraph stating:

Every silver bubble has burst, and the next one will be no exception.

History of Silver Speculation

Before rushing to criticize, let's examine what this core argument actually is.

The core argument in this book is actually called stock-to-flow ratio. BTC OGs have probably heard of this theory.

Translated into plain language: for something to become "hard currency," the key is how difficult it is to increase its production.

Gold is hard to mine. Global above-ground gold stock is about 200,000 tons, with annual new production less than 3,500 tons. Even if the gold price doubles, miners cannot suddenly dig up twice as much gold. This is called "supply rigidity".

Bitcoin is more extreme. The total supply is capped at 21 million coins, halving every four years, and no one can change the code. This is scarcity created by algorithm.

What about silver?

The gist of that highlighted passage is: Silver bubbles have burst before and will burst again. Because once large amounts of money flood into silver, miners can easily increase supply, driving the price down, and evaporating the wealth of savers.

The author also gives an example: the Hunt brothers.

In the late 1970s, Texas oil tycoons the Hunt brothers decided to hoard silver, attempting to corner the market. They bought billions of dollars worth of silver and futures contracts, driving the price from $6 to $50, setting a then-historic high for silver prices.

And then? Miners frantically sold silver, exchanges raised margin requirements, and the silver price crashed. The Hunt brothers lost over $1 billion and eventually went bankrupt.

Therefore, the author's conclusion is:

Silver's supply elasticity is too high,注定 it cannot become a store of value. Every time someone tries to hoard it as "hard currency," the market will teach them a lesson with increased production.

When this logic was written in 2018, silver was $15 per ounce. Nobody cared much.

Is This Silver Rally Different?

For the above logic about silver to hold true, there is a prerequisite: when the silver price rises, supply can keep up.

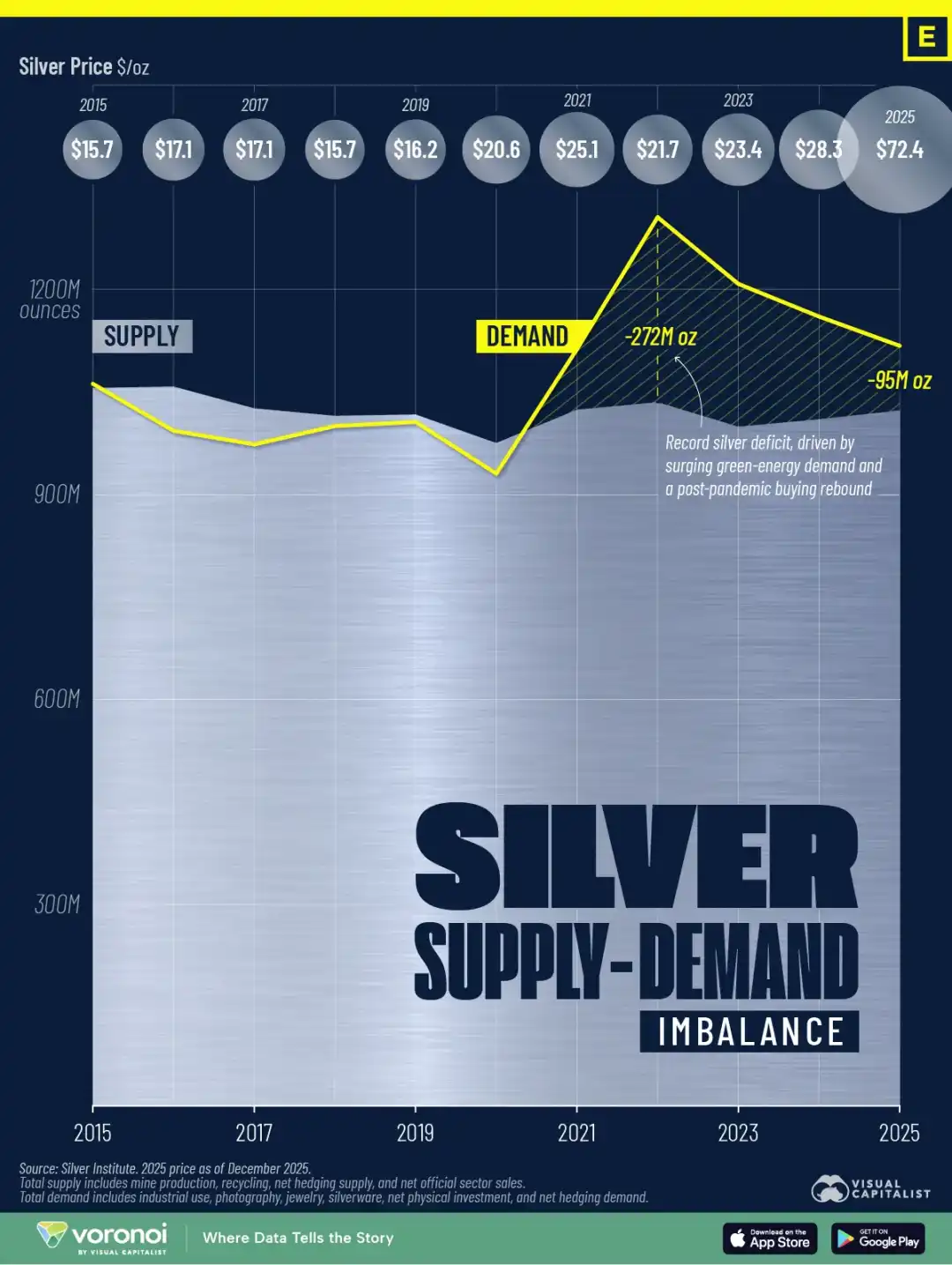

However, data from the last 25 years tells a different story.

Global silver mine production peaked in 2016 at approximately 900 million ounces. By 2025, this number had dropped to 835 million ounces. The price increased 7-fold, yet production shrank by 7%.

Why did the logic of "price rise leads to production increase" not work?

One structural reason is that about 75% of silver is produced as a by-product of copper, zinc, and lead mining. Miners' production decisions depend on the prices of these base metals, not on silver. Even if the silver price doubles, if the copper price doesn't rise, mines won't open more.

Another reason might be time. The cycle from exploration to production for a new mine project is 8 to 12 years. Even if started immediately, no new supply would be seen before 2030.

The result is a supply deficit for five consecutive years. According to Silver Institute data, from 2021 to 2025, the cumulative global silver deficit is close to 820 million ounces, almost equivalent to a full year's global mine production.

Simultaneously, silver inventories are also bottoming out. The London Bullion Market Association's deliverable silver inventory has dropped to only 155 million ounces. The silver lease rate has surged from the normal 0.3%-0.5% to 8%, meaning someone is willing to pay an 8% annualized cost just to secure physical silver.

There is also a new variable. Starting January 1, 2026, China implemented export restrictions on refined silver, allowing only state-owned large factories with an annual production capacity of over 80 tons to obtain export licenses. Small and medium-sized exporters are directly shut out.

In the era of the Hunt brothers, miners and holders could use increased production and selling to smash the price.

This time, the supply side might be running out of ammunition.

Speculation, but also Hard Demand

When the Hunt brothers hoarded silver, silver was a monetary speculative asset. Buyers thought: the price will rise, hoard it and wait to sell.

The driving force behind the 2025 silver rally is completely different.

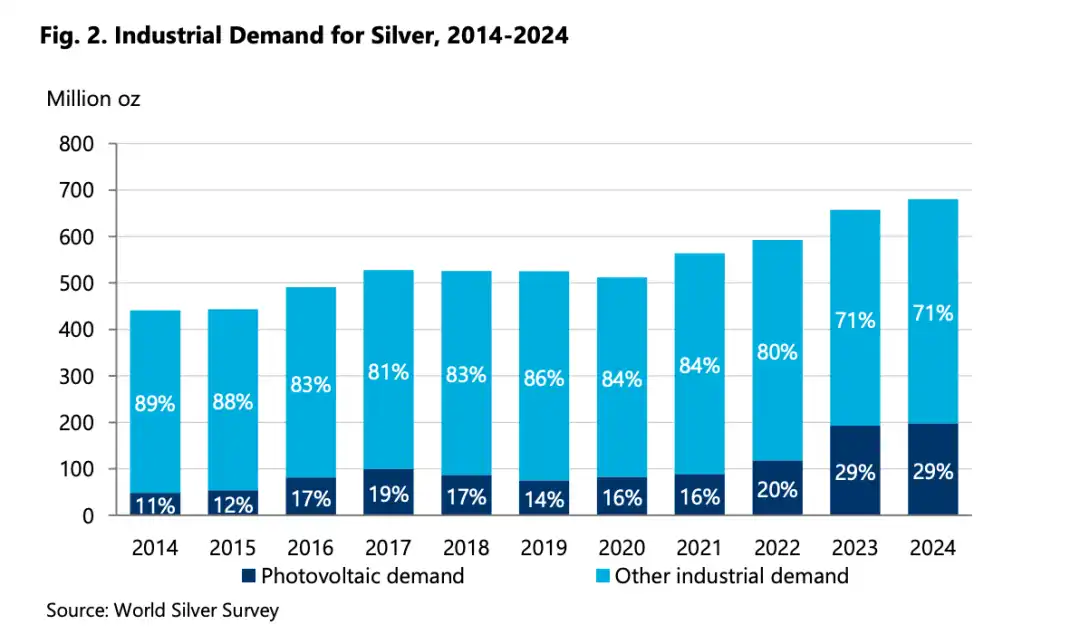

First, look at some data. According to the World Silver Survey 2025 report, industrial demand for silver reached 680.5 million ounces in 2024, a historical high. This number accounts for over 60% of total global demand.

What is industrial demand buying?

Photovoltaics (PV). Every solar panel requires silver paste for its conductive layer. The International Energy Agency predicts global PV installed capacity will quadruple by 2030. The PV industry is already the single largest industrial consumer of silver.

Electric Vehicles (EVs). A traditional internal combustion engine vehicle uses about 15-28 grams of silver. An electric vehicle uses 25-50 grams, with high-end models using even more. Battery management systems, motor controllers, charging interfaces—silver is needed everywhere.

AI and Data Centers. Servers, chip packaging, high-frequency connectors—silver's conductivity and thermal conductivity are irreplaceable. This demand began accelerating in 2024, and the Silver Institute specifically listed "AI-related applications" in its report.

In 2025, the U.S. Department of the Interior listed silver on its "Critical Minerals" list. The last time this list was updated, it added lithium and rare earth elements.

Of course, sustained high silver prices will bring about a "silver thrifting" effect, such as some PV manufacturers already reducing the amount of silver paste per panel. But the Silver Institute's prediction is that even considering thrifting, industrial demand will remain near record levels for the next 1-2 years.

This is essentially rigid demand, a variable that Saifedean might not have foreseen when writing "The Bitcoin Standard".

A Book Can Also Provide Psychological Comfort

The Bitcoin "digital gold" narrative has been largely silent recently in the face of actual gold and silver.

The market has dubbed this year the "Debasement Trade": a weakening dollar, rising inflation expectations, geopolitical tensions, with funds flooding into hard assets for safety. But this wave of safe-haven money chose gold and silver, not Bitcoin.

For Bitcoin maximalists, this requires an explanation.

Hence, the aforementioned book becomes a kind of classical reference for answers and position defense: silver is rising now because of a bubble, wait for it to crash, then you'll know who was right.

This is more like a narrative self-rescue.

When the asset you hold underperforms the market for a whole year, you need a framework to explain "why I am still right."

Short-term price is not important, long-term logic is. The logic for silver is wrong, the logic for Bitcoin is right, so Bitcoin must outperform, it's just a matter of time.

Is this logic self-consistent? Yes. Can it be falsified? Difficult.

Because you can always say "not enough time has passed."

The problem is, the real world doesn't wait. Brothers holding Bitcoin and altcoins, still坚守 in the crypto circle, are really anxious.

Bitcoin theory written 8 years ago cannot automatically cover the reality of not rising 8 years later.

Silver is still soaring, and we sincerely wish Bitcoin good luck.