Should We Turn to the Stock Market in 2026? An Analyst's New Year Strategy

marsbitPublished on 2026-01-04Last updated on 2026-01-04

Abstract

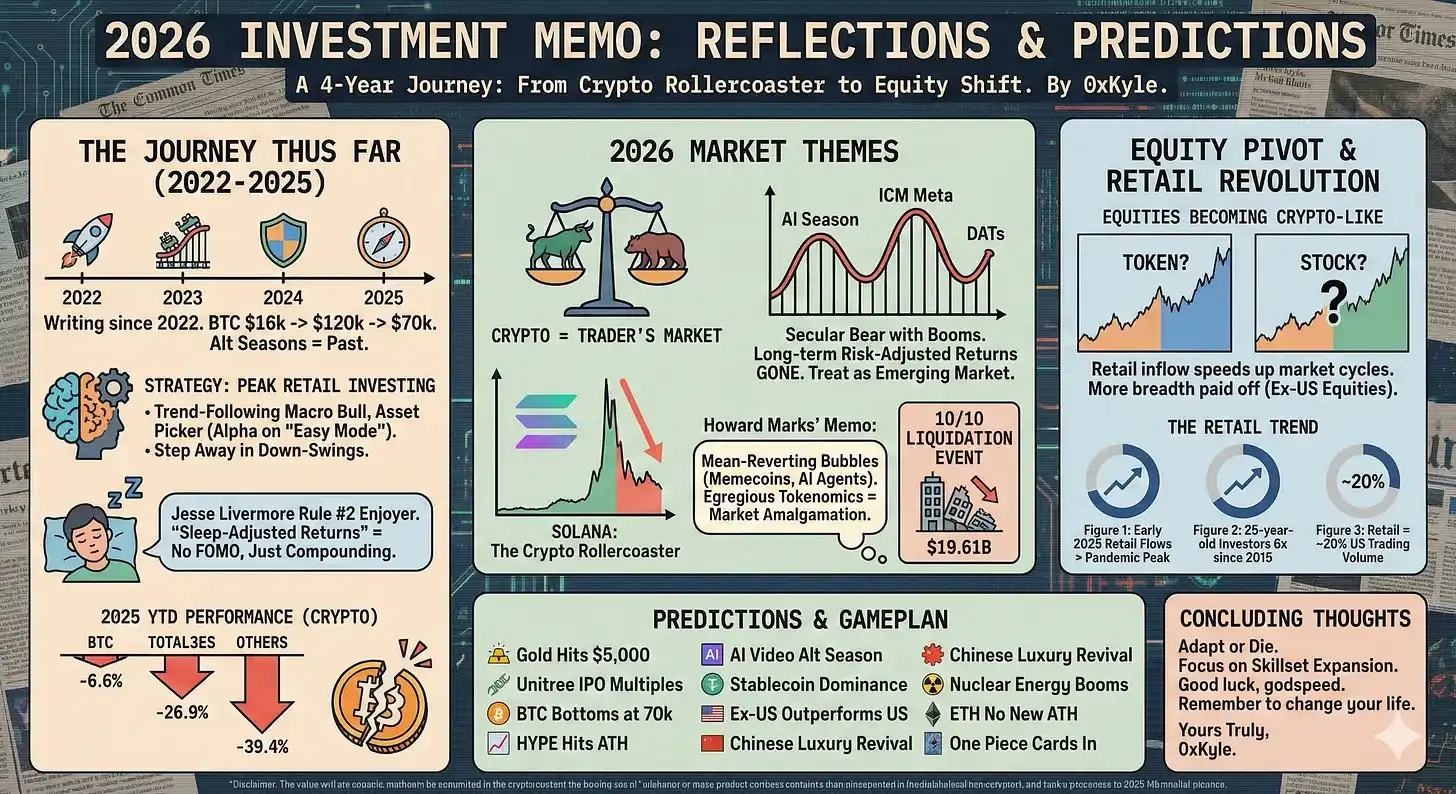

In his 2026 strategy, analyst Kyle from DeFiance Capital argues that the crypto market has become a structural bear market dominated by traders, not long-term holders. He highlights that most cryptocurrencies, including major ones like Solana, are highly volatile, lack sustainable value, and are unlikely to reach previous all-time highs again. Kyle advocates for investors to shift focus towards traditional equity markets, which are becoming more "crypto-esque" due to increased retail participation and narrative-driven trading. He emphasizes the importance of being a generalist, identifying strong narratives early, and adapting to high-volatility environments. Kyle also shares his personal move to small-cap stocks, which offer asymmetric returns similar to earlier crypto opportunities. His predictions include gold reaching $5,000, a potential Bitcoin bottom around $70,000, and continued outperformance of non-US equities. The piece concludes with a review of his mixed 2025 predictions and a call for adaptability in a rapidly changing investment landscape.

Editor's Note:

As structural changes in the crypto market gradually emerge, this annual review documents a trader's mental shift from 'single-track belief' to 'cross-market adaptation.' The author, Kyle, is a research analyst at Singapore-based crypto investment fund DeFiance Capital, specializing in long-term research on DeFi, Web3 gaming, and blockchain infrastructure.

In this article, he does not attempt to provide definitive answers but rather, from the perspective of a buyside researcher and trader, reviews the gains and losses of his 2025 judgments and confronts a more realistic question: in an era dominated by retail investors, accelerated narratives, and changing return structures, how should investors review, adapt, and reshape their investment frameworks?

The original text:

It's that time of year again. As 2025 draws to a close, I want to take this opportunity to look back on my journey. I started writing these memos back in 2022, so this will be the fourth annual review I've published. It feels like just yesterday that I started this Substack; time really flies.

In the four years I've been writing, the cryptocurrency market has undergone earth-shaking changes. Bitcoin has risen from a low of $16,000 to a high of $120,000; the once 'altcoin season' is a thing of the past; and the entire industry has gone from being ridiculed after the FTX incident to being embraced by major global institutions.

Amidst all these changes, my money-making strategy hasn't changed much overall. I don't try to do anything complex or profound; essentially, my strategy can be broken down into two parts: first, follow the larger-scale macro bull market trend; second, obtain excess returns (alpha) through asset selection and allocate positions appropriately.

My strategy can be said to represent the 'peak form of retail investment': when I judge that the bull market is weakening and momentum is dissipating, I choose to exit; I only believe in obtaining alpha in 'easy mode' and果断 turning off this玩法 when 'hard mode' begins. In other words, I am a faithful practitioner of Jesse Livermore's second principle—except for the shorting part, I don't short.

Being able to accept 'average, or slightly above average' returns has allowed me to enjoy year-after-year compound growth without sacrificing leisure time. This is also one of the reasons why I think this strategy is very suitable for lazy retail investors like me, somewhat similar to pursuing 'sleep-adjusted returns.'

This strategy has an additional benefit—it has been especially helpful for me in this year's crypto market. Why? Because the average return itself has been quite dismal: Bitcoin is down 6.6% year-to-date (YTD), TOTAL3ES is -26.9%, and OTHERS have fallen to -39.4%. The average YTD return for the top 500 altcoins is almost certainly negative. Therefore, learning to exit in time during the downturn has allowed me to preserve a significant portion of the profits and losses that might otherwise have been 'given away for free.'

Entering 2026, I will basically continue the same strategy—next, I will expand on a few macro themes that I believe will run through 2026.

For the foreseeable future, the crypto market will be more of a trader's market

The crypto industry is in a structural bear market, interspersed with periodic booms: the AI行情 in January 2025, ICM Meta in May, and DATs from July to October. Essentially, the whole of 2025 was a process of gradually recognizing and being forced to face a simple reality—crypto assets no longer have the ability to provide long-term, risk-adjusted excess returns; structurally, the industry is closer to an 'emerging market,' due to a clear disconnect between capital formation mechanisms and shareholder value.

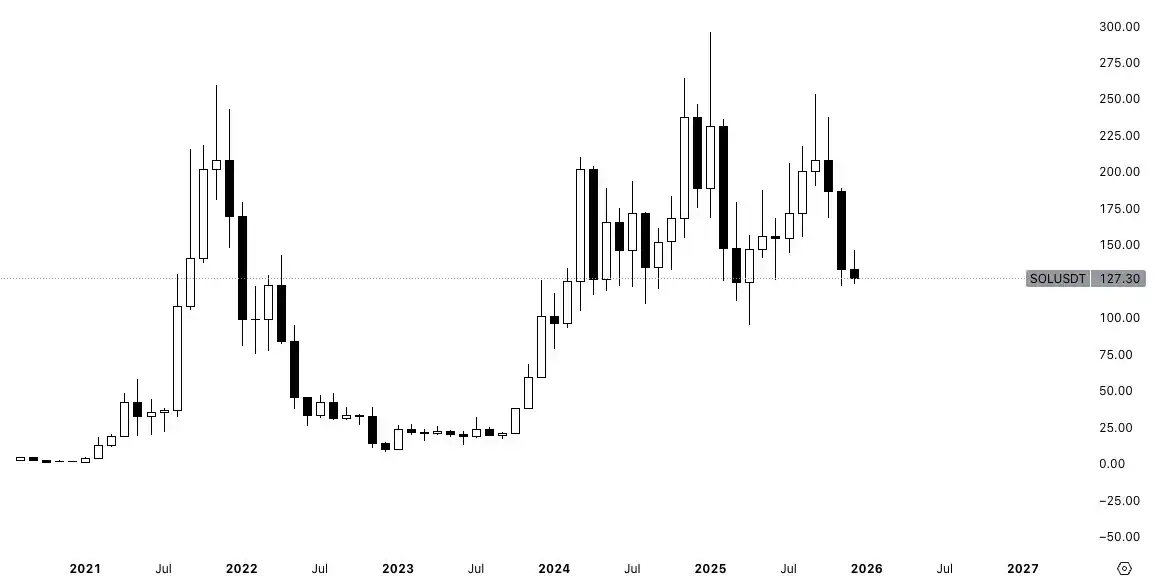

This chart of Solana, a top-ten crypto asset by market cap, almost集中体现了 all the problems faced by crypto asset investment. First, these assets are not long-term compound interest assets. They don't grow steadily year after year like the 'Magnificent 7' (Mag 7) tech stocks; their price movements are more like a 'roller coaster.' Although they have shown extremely astonishing gains—from a low of about $8 after the FTX crash to $296 a few months ago—the fact that Solana subsequently pulled back 50% from its high once again confirms a core judgment: these assets must be 'traded,' not 'held' long-term.

I still firmly believe that the crypto market will remain the only market capable of providing such astonishing returns in a relatively short period of time for the foreseeable future. But at the same time, it will also pull back just as violently. Because of this, I am highly skeptical that 99% of these assets will ever reach their all-time highs (ATH) again.

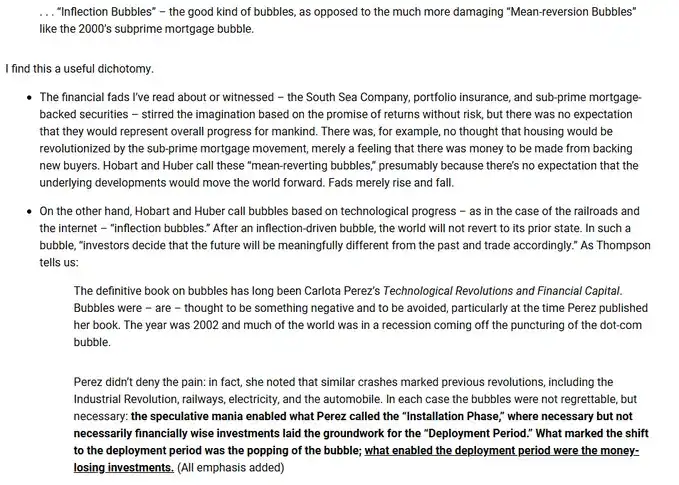

I quite agree with this mental model proposed by Howard Marks in his latest memo. The crypto market is full of such 'mean-reverting' bubbles, which are not built on any predictable basis for underlying development. Meme coins are the most typical example—these assets exist almost purely to generate returns. Essentially, what value do Fartcoin or SPX6900 bring to the world? And many other narratives in the crypto market are just meme coins with a coat of paint, trying to pretend they are 'valuable'—like so-called AI Agents.

Worse still, many tokens几乎亲手 dig their own graves,注定 making price movements a 'roller coaster': first, extremely poor tokenomics, leading to a large amount of supply being dumped on the market every month; second, the token itself has almost no value capture mechanism; third, the project doesn't even have the most basic revenue, let alone being an investable 'product.'

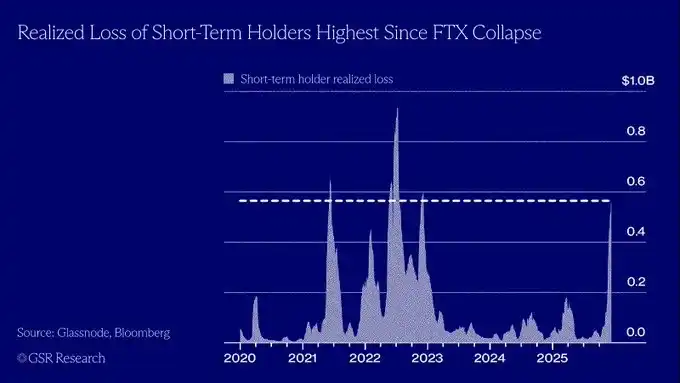

The current state of the market is the result of these structural problems集中爆发. All problems collapsed集中 on October 10—when the crypto market清算规模 reached $196.1 billion, becoming the largest liquidation event in history (the $99.4 billion event in April 2021 ranked second). After that, what we have seen is basically the typical scene of the 'late cycle': prices moving down again and again, constantly刷新 new lows.

Therefore, I have begun to gradually shift my focus from the crypto market to traditional equity assets like stocks. I believe that what is truly important in 2026 is not to continue深耕 a specific niche, but to become a generalist, not a specialist; to remain flexible, not bound to one market or track.

Looking back at the performance of different indices in 2025, it actually confirms this point well—this was a year where non-US markets (ex-US equities) performed prominently, and investors with a broader allocation perspective and more diversified exposure clearly obtained better returns.

Retail investment is a long-term trend that is driving changes in the traditional market structure

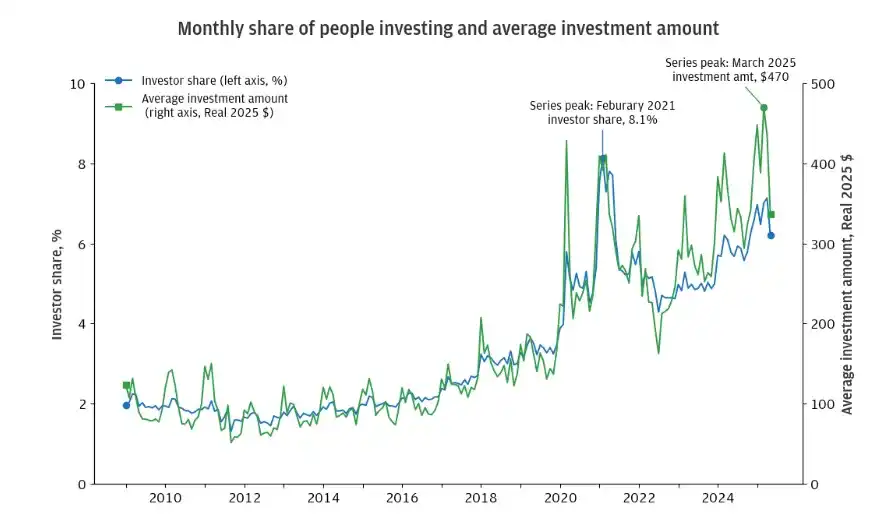

I believe that the trend of retail investment will only continue to expand. The reason is that investment has been highly 'democratized,' with retail investors from all over the world beginning to participate. The barriers to entry into this 'movement' are constantly lowering, making investable assets truly 'globalized.' Today, the tentacles of capital flow have spread to every corner of the world: an American retail investor can invest in Korean stocks based on the AI narrative; a Singaporean Grab driver can invest in Polish listed companies, and so on.

From this perspective, this is actually a bearish factor for the crypto market. For a long time, cryptocurrency has been seen as an 'Internet asset layer' that anyone, anywhere can participate in. But when investment itself has become so accessible, why would retail investors choose to invest in those digital assets with weak value support and dominated by speculation, instead of being able to buy 'almost anything'?

Digression over. The continued growth of retail investment is itself a fairly obvious judgment, and it is almost difficult to refute it at the data level at present. But what I really want to emphasize is the issue of 'scale.' Many people may intuitively agree that retail is entering the market on a large scale, but they underestimate the深层 impact of more retail entering the market.

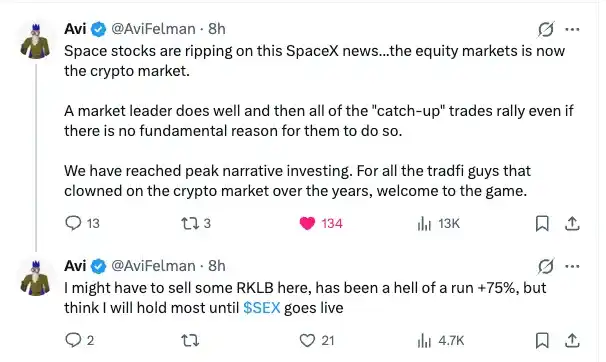

Driven by the continuous inflow of retail funds, the stock market as a whole is becoming more and more 'like the crypto market.' One thing I've always liked about the crypto market is that it can 'fast-forward' through a complete market cycle in a very short time—we often go through all stages from accumulation to distribution in just a few months, or even weeks. And now, I am seeing similar signs in the stock market.

Look at the chart below, can you tell which one is a token and which one is a stock?

That's right, they are all stocks. Although not all stocks exhibit this characteristic, it is undeniable that more and more aspects of the stock market are becoming more 'crypto-esque.'

The world of the stock market is extremely vast, and this is just a subtle but ongoing trend change that I have observed.

If you are in the crypto market, consider switching to the stock market

Against the backdrop of持续走低 volatility in the crypto market, many people have already started转向 the stock market; there has also been a lot of discussion on timelines, debating whether 'traders from the crypto market' have some kind of advantage in stock investing. My view is: just because you are 'from crypto' does not mean you naturally have an advantage in the stock market. Of course, some skills may indeed help with the migration—such as the ability to adapt to high-volatility environments—but ultimately, you still need to learn and adjust to truly adapt to the stock market.

I am actually in the same situation myself. I do not claim to be good at stock investing; on the contrary—writing these contents on a Substack that I know will be read by hedge fund managers with decades of traditional market experience, I actually have a strong 'imposter syndrome.'

But this is not completely meaningless. Precisely because I believe that as retail participation continues to increase, market behavior will become more emotional and more disorderly, I further judge that资深 crypto traders who have been in the crypto market for a long time, mainly博弈 with retail investors, may still find some kind of advantage. Take 'narrative trading' as an example—if you are sharp enough, it is entirely possible to capture the multiple themes that drove returns this year—such as Hyperscalers, aerospace, storage, FinTech, etc.

Besides, what other choice do I have? I don't expect the crypto market to continue to bring rich returns as it did in the past.摆在我面前的 are无非 two paths: either 'trap myself' in the 1-2 trades that can multiply several times that may not even appear in a year; or, expand and upgrade my skill boundaries.

TL;DR: either adapt, or be eliminated.

Anyway, by my own standards, the current performance is not bad. What is shown above is the year-to-date (YTD) return of my various investment portfolios. Even if it may sound a bit conceited, I still want to further explain: why I think that, as a trader from the crypto market, my current ability to achieve such performance is not accidental.

1. Catching strong narratives can greatly amplify returns

Back to the point I mentioned earlier—this is one thing I truly think 'crypto traders' are good at: identifying core narratives and building positions around these narratives. A few more examples:

Hyperscale computing power / data centers (IREN / HUT)

Aerospace (ASTS / RKLB / PL)

Financialization (HOOD / SOFI)

Storage (SNDK / SK Hynix)

Robotics (TER)

Nuclear energy (OKLO)

Quantum computing (IONQ / QBTS)

Metals (silver / gold), etc.

I am still working on improving my ability to identify themes in advance, but honestly, a large part of it is second-order thinking. Stock selection comes later, and after the emergence of AI, the advantage at the information level has been greatly leveled.加上 more and more retail investors entering the market, I believe narrative trading will once again become an important force in the market.

2. Learn 'what to trade'

I am well aware that I have no advantage in 'trading news' or 'gaming earnings reports.' But frankly, if you choose the right table in this game, there is still a lot of alpha to be captured.

In the past 10 years, the crypto market was such a table—ignored by the mainstream, thus孕育了 extremely asymmetric returns. And now, with the rise of retail dominance, similar tables are beginning to appear in the stock market: small and mid-cap companies (market cap below $10 billion).

I have started to 'get my hands dirty' here, and it's really interesting. You can see very familiar return curves, such as:

DAVE (up about 35x since 2023)

RKLB (up about 12x since September 2024)

I am still refining the process of finding such stocks, and the workflow is still in a very early stage. But for now, this might be the most suitable table for me to participate in.

3. Coping with volatility

A trait often mentioned about crypto traders has indeed been a great help here. Unlike coins, these stocks at least have fundamentals—if you can withstand a 40% drawdown on a coin that 'has not yet generated revenue,' then of course you can do the same for a company that actually has a business.

My biggest weakness so far

Ironically, what the crypto market has taught us is precisely 'not to hold long-term'—and this has also become a double-edged sword.

After experiencing TRUMP, LUNA, and countless events typical of crypto traders, I find that my biggest weakness is: selling immediately at the slightest sign of trouble. To some extent, it's like PTSD; once I feel the price is 'a bit high,' I immediately start reducing positions, expecting a market-wide pullback like the one in February this year.

This is still something I am trying to 'un-train.'

Some predictions

Don't take it too seriously, just some things I think have a not-low probability of happening.

1. Gold rises to $5000

I think gold is in a structural bull market. In recent weeks, precious metals (gold, silver, platinum) have all performed very well, and I暂时 don't see any reason for this trend to stop.

2. Unitree IPO soars on first day (2-4x)

In my opinion, robotics is one of the most disruptive applications of AI, but it is severely underestimated. The AI circle炒 new models and new applications every day, but the attention to the highly adjacent field of robotics is明显不足. Even though Figure's robot release received a lot of coverage, it is still far from the heat of general AI / sci-fi AI technology. I really think Rewkang's judgment about robotics makes sense.

3. Bitcoin bottoms around $70,000

I think it is very possible that BTC will bottom out soon—as for whether it can make new highs, that is a completely different question. From the current trading structure, the downside risk is limited, but I同样 can't see the upside catalyst.

4. HYPE makes new highs, other altcoins continue to fluctuate

For reference: my current holdings are a micro-cap project with a market cap below $10 million, and Shuffle. I no longer hold HYPE, but I am looking for opportunities to re-enter recently.

5. Hyperliquid is one of the few projects with 'quality altcoin' characteristics

No high inflation; has some value capture / interest alignment mechanism; the product grows steadily quarter by quarter, not a flash in the pan

When 99% of altcoins are uninvestable, I expect funds to flow to one of the 'cleanest' assets of this cycle.

There will be an on-chain / altcoin season, but the theme is AI video

This may sound contradictory to my previous judgment, but as I said—crypto is still the easiest place for short-term 'mean-reverting bubbles,' like the ICM in May, which was a行情 that only lasted 1-2 months. I believe such 'local outbreaks' will always exist; the key is: exit before everything collapses again.

6. Stablecoins land on a large scale, CRCL goes above $200

There is a lot of discussion about stablecoins currently, and infrastructure is advancing, but we have not yet seen the moment when large banks真正 'enter the game.' Tempo is still under construction, and large banks are preparing for it (but not fully ready yet). I believe 2026 will be a year of持续强化 stablecoin dominance.

One thing I纠结 about: Trump and the world are in a rate-cutting cycle, which is not friendly to stablecoin companies, but may increase the velocity of money.

Non-US equity indices continue to outperform US stocks, self-explanatory.

7. Some other predictions

Recovery of Chinese luxury consumer stocks (Pop Mart, Lao Feng Xiang, etc.)

AI bubble cools down, returns shift to other sectors

Nuclear energy sector continues to perform well

ETH cannot return to its historical high

Pokémon cards 'fade,' One Piece cards 'take over' (especially against the backdrop of Pokémon's 30th anniversary)

The only DATs that survive are MSTR and BMNR

More token-level mergers and acquisitions in the crypto field

Crypto tries to tokenize stocks (after realizing in 2025 that the DAT path of 'tokens becoming stocks' doesn't work)

Crypto gambling sector takes off (disclaimer: I hold Shuffle)

Crypto bear market continues into 2026

2025 Action Plan Review

As a conclusion, we will review the memo I released the previous year to see how the judgments at that time played out.

1. My macro scenario judgment

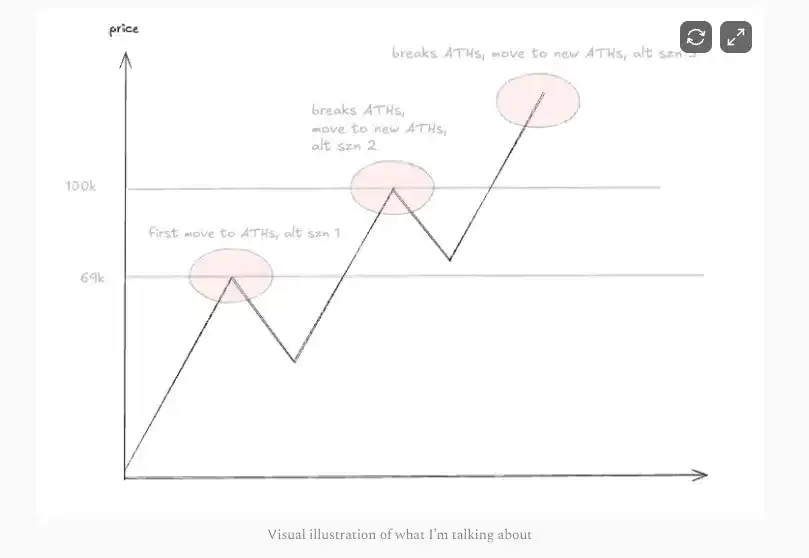

In the 2025 memo, I drew this chart and attached the following judgments:

BTC rises, and the increase will be higher than in 2024

Altcoins: offense-oriented, know when to switch to defense, but overall less defensive than in 2024

Looking back, I can only say it was partially fulfilled, but overall it was a not-so-good prediction because it did not consider 'path dependence.' We did hit new highs in September, but look at the current position. This one can only be considered勉强 passed.

2. AI

Yes, this theme still exists. But as the tweet above shows, we have experienced several rotations. If you read my analysis on AI tokens (link omitted), I still think the next wave is coming soon.

To be fair, this is more of a short-term judgment. What I said at the time did happen—before they all fell 99%. My picks ALCH / DIGIMON / AI16Z all had very bright performances,同样也是在随后 -99% 之前完成的. This one counts as passed.

3. DeFi

Core holdings: AAVE / ENA / Morpho / Euler / USUAL

Auxiliary directions: stablecoin / payment-related tokens

Can only say: mediocre. Many of these标的 never made new highs after January 25th; this portfolio as a whole was a poor choice. AAVE briefly made new highs, but for a very short time; ENA and Euler basically peaked for the year on January 25th; USUAL直接 crashed; the only winner was Morpho.

This one failed.

4. L1交易

I know this section will be criticized by many, but my judgment at the time was: L1 trading would make a strong comeback. Hype was the obvious choice, and Sui, from $1, $2, to $4, was heavily shorted by the market. I still believe that the L1 narrative itself is one of the directions ignored by the market, and Hype's 10x move is proof that such opportunities exist.

Core holdings: SUI / Hype

Auxiliary holdings: Abstract

Result: complete failure. SUI peaked around $4; as for Hype, although it did have a run, its current price is basically back to the level of January 2025. And frankly, this标的 itself is a bit 'edgy'—it is more like a Perp DEX than an L1. In hindsight, I'm not quite sure what I was thinking either.

5. NFT tokens & gaming coins

Core holdings: Pengu / Anime (Azuki)/ Spellborne / Treeverse

Auxiliary holdings: Prime / Off the Grid (if token launched)/ Overworld

The only winner here is Pengu, although it fell 90% at one point in January, it subsequently had an 8x run. More importantly, Pengu is the only NFT project that真正 gained mainstream attention.

But from the perspective of the overall portfolio, this basket still failed.

6. Other narratives

These are just directions I follow, not particularly bullish, but find interesting:

Data tokens: Kaito / Arkm

Meme: only like PEPE, the others... basically 'cooked'

DePIN: PEAQ / HNT

Ordinals

Dino alts: XRP, etc.

Old DeFi: CRV / CVX

I didn't give a clear judgment at the time, so these won't be evaluated.

7. Prediction review

Prediction: DePIN will be landed by a 'serious company' in a 'serious way,' possibly through acquisition.

Not sure if it happened. Maybe readers can add? Racking my brains, I don't really think it happened.

Prediction: Binance, as a top exchange, will lose market share, not to Hyperliquid, but to Bybit / OKX.

Did not fully materialize, but I would say Binance's reputation and market position have明显下滑ed, especially after 10/10.

Prediction: Metaverse tokens will gain new life with breakthroughs in VR.

No.

Prediction: ICOs become popular again.

This hit very漂亮. Cobie's ICO platform was acquired by Coinbase for $375 million, enough to show that ICOs have become the 'new trend' again.

Prediction: ETH on-chain season will never come.

I was correct on this point.

Prediction: Sui goes double digits (at least $10).

Haha, impossible.

Prediction: ETH ETF approved for staking rewards, thus催生 a new round of yield products and yield aggregators, similar to 2021.

This one did come true.

Prediction: A heavyweight artist will use NFTs and tokens to manage and incentivize fans.

Did not happen.

Prediction: Bitcoin to $200,000.

I wish.

Prediction: After Aptos, more L1 CEOs / founders will leave.

Sadly, this one did happen. Nowadays we see more and more 'departures,' often accompanied by that classic meme: 'vesting cliff is here.'

Prediction: Base loses in the on-chain competition, replaced by another L1; Solana remains领先.

As of now, I would say Base is still in a winning position alongside Solana.

Conclusion

The above basically outlines my overall layout思路 as I step into 2026. I also expect that a significant portion of these judgments will, like my 2025 action plan, undergo considerable changes over time.

Good luck to all, fair winds, and I'll see you on the other side, ladies and gentlemen.

If you make life-changing profits on this road, remember—truly change your life.

Sincerely,

0xKyle