Author: Dhruvang Choudhari (AMINA Bank)

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: January 2026 presented a paradox: crypto prices fell by 25%, but the infrastructure supporting institutional adoption was accelerating. While Bitcoin dropped to a ten-month low of $73,000, BlackRock listed digital assets as a decisive investment theme for 2026.

While leveraged traders liquidated $2.2 billion in positions, the Depository Trust and Clearing Corporation (DTCC) launched production-level tokenization for U.S. Treasuries and stocks. While sentiment indices reached extreme pessimism, Y Combinator announced it would begin funding startups in USDC.

AMINA Bank's analysis points out that this is not a rejection of digital assets, but a repricing within an evolving global monetary system. The divergence between price action and structural progress defines the current phase of the cycle.

Full Text Below:

Introduction

January 2026 presented a paradox: crypto prices fell by 25%, but the infrastructure supporting institutional adoption was accelerating.

While Bitcoin dropped to a ten-month low near $73,000, BlackRock listed digital assets as a decisive investment theme for 2026. While leveraged traders liquidated $2.2 billion in positions, the Depository Trust and Clearing Corporation (DTCC) launched production-level tokenization for U.S. Treasuries and stocks. While sentiment indices reached extreme pessimism, Y Combinator announced it would begin funding startups in USDC.

The first two months of 2026 marked a decisive shift in the digital asset market. What initially seemed like chaotic selling was actually a broad macro repricing driven by sovereign risk, changes in the monetary system, and forced unwinding of global leverage. Unlike previous crypto downturns, this event did not originate from within the digital asset ecosystem itself. It emerged from the outside.

January and February revealed a paradox that is now central to the institutional crypto era. Market prices deteriorated sharply, yet regulatory clarity, infrastructure deployment, and institutional commitment advanced at an unprecedented pace. This divergence between price action and structural progress defines the current phase of the cycle.

This update analyzes how the macroeconomic shock disrupted crypto market structure, why Bitcoin faces an identity challenge as a macro asset, and how institutional capital continues to build amidst volatility rather than retreat from it.

Institutional Expansion Amid Market Weakness

Despite deteriorating spot prices, institutional participation accelerated rather than slowed. This acceleration reveals a fundamental shift in how mature allocators approach digital assets: infrastructure maturity now matters more than price momentum.

Tokenization as a Core Strategy

BlackRock formally listed digital assets and tokenization as decisive investment themes for 2026, alongside AI, as structural drivers for capital markets.

At Franklin Templeton, innovation leadership described 2026 as the beginning of a wallet-native financial system, where stocks, bonds, and funds are held directly in digital wallets, rather than through traditional custody frameworks.

Y Combinator sent a key signal, announcing that starting with the Spring 2026 batch, startups may receive funding in USDC on Ethereum, Base, and Solana. Stablecoin settlements now typically clear in less than a second at a cost below $0.01, offering a clear advantage over cross-border fiat rails.

Reduced Regulatory Friction

Regulatory developments quietly removed long-standing structural barriers. The SEC rescinded previous accounting guidance that hindered banks from offering digital asset custody services. Simultaneously, the Depository Trust and Clearing Corporation (DTCC) launched a production-level tokenization program for U.S. Treasuries, large-cap stocks, and ETFs, confirming the legal equivalence between tokenized securities and traditional securities.

This marks a shift from experimental adoption to an upgrade of internal financial infrastructure.

Regional Competition for Crypto Capital

Jurisdictions are increasingly deploying policy as a competitive lever.

Hong Kong announced zero-tax incentives on qualified digital asset income for funds and family offices, positioning itself as a major institutional crypto hub in Asia. As of January 2026, 11 licensed virtual asset trading platforms are operating.

Meanwhile, Dubai continues to execute its blockchain-first government strategy, aiming for on-chain processing of 50% of public sector transactions by the end of 2026. Crypto penetration in the UAE has reached approximately 39%, representing over 3.7 million users.

Macroeconomic Shock Shattering the Calm

Understanding why institutions continue to build requires understanding what drove the sell-off. The relative stability of 2025 fostered expectations that crypto had entered a low-volatility, institutionally-anchored phase. These assumptions were shattered in January.

Japan and the Unwinding of Global Leverage

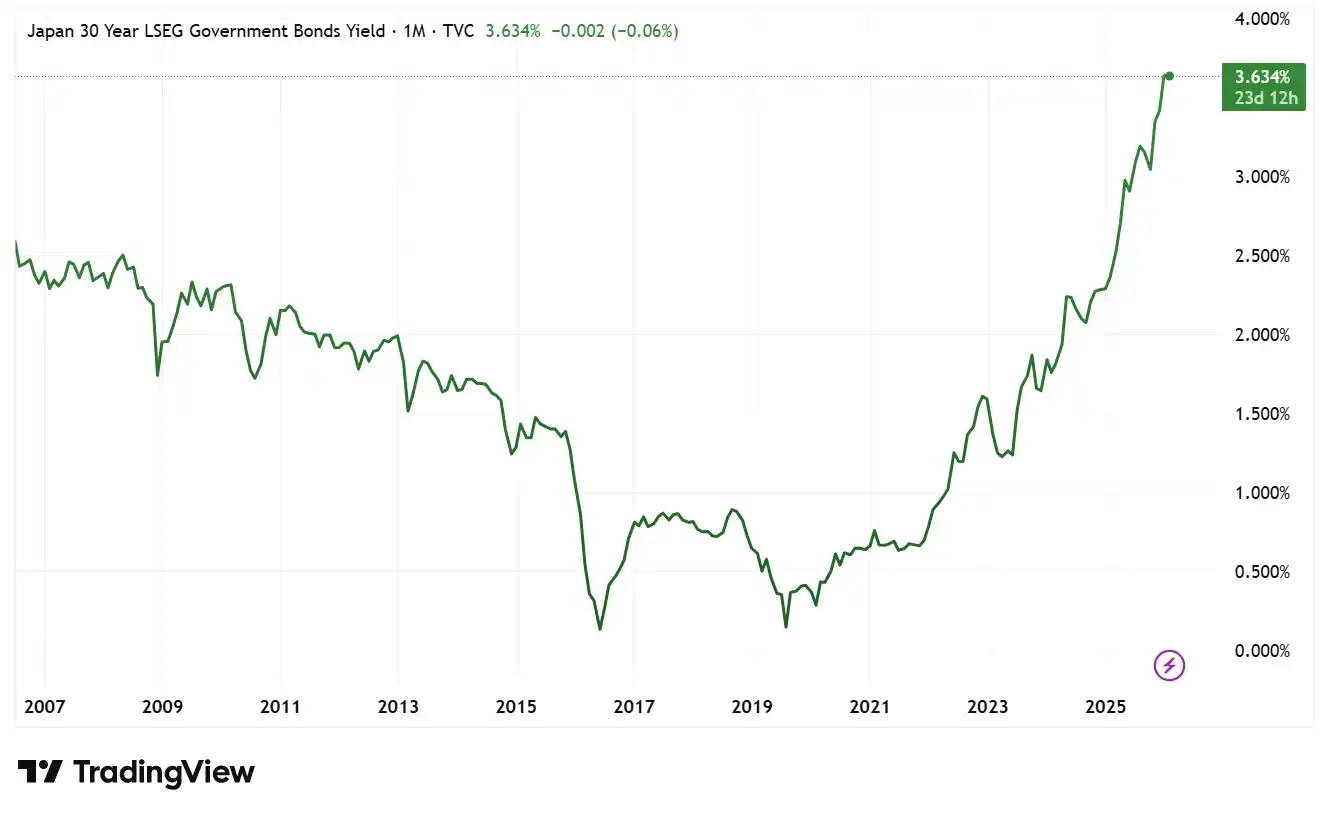

On January 20, 2026, the Japanese Government Bond (JGB) market entered a period of acute stress. The 30-year JGB yield surged over 30 basis points to 3.91%, its highest level in 27 years, following fiscal rhetoric from Prime Minister Sanae Takaichi that heightened concerns about debt sustainability. Japan's debt-to-GDP ratio has exceeded 250%, making it a focal point for global bond markets.

Figure 1: Japan 30-Year Government Bond Yield (Historical)

Source: TradingView

The immediate consequence was the rapid unwinding of the yen carry trade, one of the largest sources of cheap global leverage. As yen funding costs rose, investors were forced to liquidate risk assets to meet margin requirements. Bitcoin fell below $91,000 not due to crypto-specific weakness, but because it served as a liquidity proxy for balance sheet repair.

Warsh Nomination and Monetary Repricing

This pressure escalated on January 30th with the nomination of Kevin Warsh as the next Federal Reserve Chair. Warsh's long-standing preference for higher real interest rates and a significant reduction of the Fed's balance sheet was interpreted as a clear shift away from accommodative monetary policy.

Within 24 hours, the total cryptocurrency market capitalization fell by about $430 billion. Bitcoin fell approximately 7% in a single trading session, while Ethereum and high-beta altcoins experienced double-digit percentage pullbacks. This move reflected a repricing of global dollar liquidity expectations, not speculative panic.

Price Action and Bitcoin's Identity Crisis

The macro shock revealed an uncomfortable truth about Bitcoin's evolution as an institutional asset. The last week of January produced one of the most severe single-day dislocations of the institutional era.

On January 29th, Bitcoin fell from $96,000 to $80,000, a drop of approximately 15% in a single day. The crypto derivatives market liquidated over $2.2 billion in leveraged positions. The significance of this move lies not in its magnitude, but in its correlation characteristics.

Bitcoin failed to decouple from stocks, instead trading in sync with high-beta tech stocks. During a global deleveraging event, it behaved not as a defensive asset, but as a liquidity-sensitive risk instrument.

By early February, sentiment indicators reflected extreme pessimism. The Crypto Fear & Greed Index dropped to 19, and key technical levels, including the 0.786 Fibonacci retracement at $85,400, were decisively broken. The high $70,000s range became the market's primary structural support zone.

Figure 2: Bitcoin Price Decline Driven by Global Macro Events (Jan-Feb 2026)

Source: AMINA Bank

The correlation characteristics raise fundamental questions about Bitcoin's role in institutional portfolios. If it behaves as a high-beta tech proxy rather than a defensive hedge during stress, the allocation thesis must adjust accordingly. Yet, institutional commitment continues regardless, suggesting mature allocators are pricing Bitcoin's long-term structural role, not its short-term correlation behavior.

Protocol Evolution and Competitive Differentiation

While prices fell and macro conditions worsened, foundational layer development continued unabated. This demonstrates a key feature of the current cycle: infrastructure development has decoupled from price momentum.

Ethereum remains focused on scaling through execution efficiency, censorship resistance, and MEV mitigation. The upcoming Glamsterdam upgrade aims to increase the gas limit to 200 million, approaching a throughput of nearly 10,000 TPS theoretically.

Solana is pursuing aggressive performance enhancements. Its Alpenglow upgrade aims to reduce transaction finality from 12.8 seconds to approximately 100-150 milliseconds, positioning it as one of the fastest settlement layers in production.

These technical advancements continue regardless of market sentiment, reflecting long-term capital commitment and engineering development independent of price action.

Security Losses Highlight Operational Risks

Even as institutional infrastructure matures, security incidents highlight ongoing operational vulnerabilities. January 2026 recorded over $370 million in stolen funds, the highest monthly total in nearly a year. Over $311 million in losses stemmed from phishing and social engineering attacks, not smart contract failures.

The single largest event, exceeding $280 million, involved AI-generated voice impersonation targeting hardware wallet users. These incidents emphasize a structural shift in risk. Human and operational vulnerabilities now represent the primary attack surface for institutional crypto participants.

This pattern reinforces why custody frameworks operating under regulatory oversight offer competitive advantages beyond compliance. Operational security protocols, institutional-grade key management, and insurance frameworks have become mandatory requirements.

Conclusion

The retracement of January-February 2026 is not a rejection of digital assets, but a repricing within a changing global monetary system. Crypto now reacts directly to sovereign bond markets, central bank leadership, and geopolitical escalation. This sensitivity introduces volatility, but it also confirms integration.

Simultaneously, institutional adoption, regulatory clarity, and protocol development advanced during the sell-off. Tokenization shifted from narrative to deployed infrastructure, wallet-native finance from theory to implementation.

Early 2026 did not mark a collapse of the crypto market. It marked its first real stress test of institutional maturity. While prices failed the test, the underlying infrastructure passed with flying colors.

The divergence between price action and structural progress will not persist indefinitely, as institutional deployment, regulatory clarification, and infrastructure maturity will ultimately be reflected in market valuations.