Penulis Asli: ChandlerZ, Foresight News

Baru-baru ini, Hong Kong China mengumumkan melalui laporan pemerintah bahwa pihak berwenang sedang melakukan konsultasi mengenai implementasi kerangka pelaporan aset kripto (Crypto-Asset Reporting Framework, CARF) dari Organisasi untuk Kerja Sama dan Pembangunan Ekonomi (OECD) serta revisi terkait Standar Pelaporan Bersama (Common Reporting Standard, CRS).

Disebutkan bahwa sejak 2018, Hong Kong telah melakukan pertukaran informasi akun keuangan secara otomatis setiap tahun dengan yurisdiksi pajak mitra sesuai dengan CRS yang ditetapkan OECD, memungkinkan otoritas pajak terkait menggunakan informasi tersebut untuk penilaian pajak serta mendeteksi dan memerangi penggelapan pajak. Tujuan masa depan adalah memulai pertukaran informasi pajak terkait transaksi aset kripto secara otomatis dengan yurisdiksi pajak mitra terkait mulai tahun 2028, dan menerapkan aturan CRS versi baru yang telah direvisi mulai tahun 2029.

Selain itu, mulai 1 Januari 2026, Inggris dan lebih dari 40 negara lainnya menjadi yang pertama menerapkan aturan pengawasan pajak aset kripto baru, mewajibkan penyedia layanan kripto lokal mulai mengumpulkan data dompet kripto dan transaksi pengguna, sebagai persiapan untuk pertukaran informasi pajak lintas negara selanjutnya.

Mengambil contoh Inggris, bursa kripto yang beroperasi di Inggris harus mulai mengumpulkan catatan transaksi lengkap dan informasi detail semua klien Inggris. HMRC akan menggunakan data yang terkumpul untuk mencocokkan kembali formulir pajak pengguna guna memastikan kepatuhan pajak, pelanggar akan menghadapi sanksi. Pihak industri mencatat, data terkait di masa depan mungkin digunakan untuk identifikasi, anti-pencucian uang, dan investigasi kriminal, berdampak mendalam pada anonimitas dan lingkungan kepatuhan industri kripto.

"Pajak trading kripto jadi kenyataan?" Diskusi luas mulai muncul di pasar. Jika Hong Kong melaporkan, akankah Daratan China juga melaporkan? Akankah trading kripto juga dikenakan pajak tambahan di masa depan?

Apa itu Kerangka Perpajakan Global CARF

Kerangka Pelaporan Aset Kripto (CARF) adalah seperangkat standar internasional untuk transparansi informasi pajak aset kripto yang dikembangkan oleh OECD di bawah mandat G20, dengan tujuan inti untuk memasukkan transaksi aset kripto yang sebelumnya sulit ditembus oleh otoritas pajak dan sangat mudah beredar lintas batas, ke dalam jaringan informasi yang dapat dikumpulkan secara standar dan dipertukarkan secara otomatis antar otoritas pajak. OECD menyetujui dan menerbitkan aturan dan komentar CARF pada tahun 2022, memperjelas bahwa tujuan desainnya adalah mengumpulkan informasi terkait wajib pajak dengan口径 yang seragam, dan melakukan pertukaran otomatis tahunan dengan yurisdiksi tempat tinggal pajak wajib pajak, sehingga mengurangi risiko penggelapan dan kelalaian pelaporan pajak aset kripto lintas batas.

Dalam konteks CARF, aset kripto tidak sama dengan Bitcoin atau Ethereum dalam arti sempit; pembawa nilai digital yang dapat dipegang dan ditransfer secara terdesentralisasi tanpa memerlukan perantara keuangan tradisional termasuk dalam cakupannya; cakupannya sengaja dibuat lebih mendekati bentuk pasar nyata, mencakup stablecoin, derivatif yang diterbitkan dalam bentuk aset kripto, dan memasukkan sebagian NFT ke dalam ruang lingkup pengamatan yang dapat memicu risiko pajak serupa.

Sesuai dengan cakupan objeknya, kewajiban pelaporan CARF berpusat pada perantara pasar yang menyediakan layanan kunci untuk transaksi dan pertukaran. Pemikiran OECD adalah menempatkan titik patuh pada mata rantai yang paling berkondisi menguasai nilai transaksi dan informasi pihak lawan, setiap entitas atau individu yang dengan cara komersial mempertemukan atau mengeksekusi transaksi pertukaran aset kripto terkait (termasuk pertukaran antara aset kripto dan mata uang fiat, serta pertukaran antar aset kripto) pada prinsipnya dapat dianggap sebagai Penyedia Layanan Aset Kripto Pelapor, dan menanggung kewajiban pengumpulan data, uji tuntas, dan pelaporan.

Apa hubungan antara CARF dan CRS yang sebelumnya hangat dibahas?

Memahami CARF tidak terlepas dari menempatkannya kembali dalam sistem pertukaran informasi pajak global yang lebih besar untuk dibandingkan. Gelombang pembayaran pajak tambahan untuk saham Hong Kong dan AS yang sebelumnya hangat dibahas, terjadi di bawah mekanisme CRS (Common Reporting Standard).

Dalam sepuluh tahun terakhir, transparansi pajak lintas batas terutama mengandalkan standar CRS. Negara-negara meminta bank, pialang, dana, dan lembaga keuangan lainnya untuk mengidentifikasi pemegang akun yang bukan residen pajak negara mereka, dan melaporkan informasi kunci seperti saldo akun, bunga, dividen, dan keuntungan pelepasan kepada otoritas pajak negara mereka setiap tahun, yang kemudian dipertukarkan secara otomatis dengan negara lain oleh otoritas pajak.

China mulai menerapkan CRS secara penuh pada September 2018, dan melakukan pertukaran informasi akun keuangan residen dengan lebih dari 100 negara dan wilayah. Setelah data dilaporkan, otoritas pajak mengirim pemberitahuan berdasarkan data CRS dll., meminta pengguna menjelaskan situasi dan membayar pajak tambahan.

CRS berjalan relatif matang dalam sistem keuangan tradisional, tetapi transaksi, pertukaran, dan transfer aset kripto banyak terjadi di luar sistem rekening bank, terutama membentuk jaringan peredaran nilai independen antara platform perdagangan terpusat, dompet terkelola, dan transfer on-chain, membuat hanya mengandalkan CRS sulit mencapai tembusan dengan intensitas yang sama. Sedangkan CARF melengkapi struktur pasar on-chain dan aset kripto yang awalnya sulit dicakup oleh CRS.

OECD, saat meluncurkan CARF, juga melakukan revisi sistemik pertama terhadap CRS. Di satu sisi memasukkan produk uang elektronik dan mata uang digital bank sentral (CBDC) dan produk keuangan baru lainnya ke dalam cakupan CRS, di sisi lain juga menyesuaikan口径 untuk jalur investasi tidak langsung dalam aset kripto melalui derivatif atau kendaraan investasi, untuk menghindari pasar menghindari pelaporan dan pertukaran informasi melalui struktur produk. Secara keseluruhan, CARF bertanggung jawab atas dimensi transaksi dan penyedia layanan di pasar asli aset kripto, sedangkan CRS yang direvisi terus bertanggung jawab atas eksposur risiko terkait yang mungkin dibawa dalam sistem akun keuangan, keduanya bersama-sama membentuk puzzle pertukaran otomatis yang lebih lengkap.

OECD mencatat, setelah format transmisi teknis dan panduan pendukung untuk CARF dan CRS yang direvisi disempurnakan, pertukaran otomatis lintas batas pertama diperkirakan dimulai pada tahun 2027; sebelum itu, banyak yurisdiksi akan lebih dulu menerapkan persyaratan pengumpulan dan pelaporan data di ujung domestik, sebagai persiapan basis data untuk pertukaran lintas batas selanjutnya.

Di tingkat UE, DAC8 telah disetujui oleh negara anggota pada Oktober 2023 dan diterbitkan dalam Laporan Resmi pada bulan yang sama, desain sistemnya didasarkan pada standar internasional CARF OECD, bertujuan untuk memasukkan informasi pengguna aset kripto ke dalam pertukaran otomatis antar otoritas pajak negara anggota.

Akankah Daratan China Juga Bergabung?

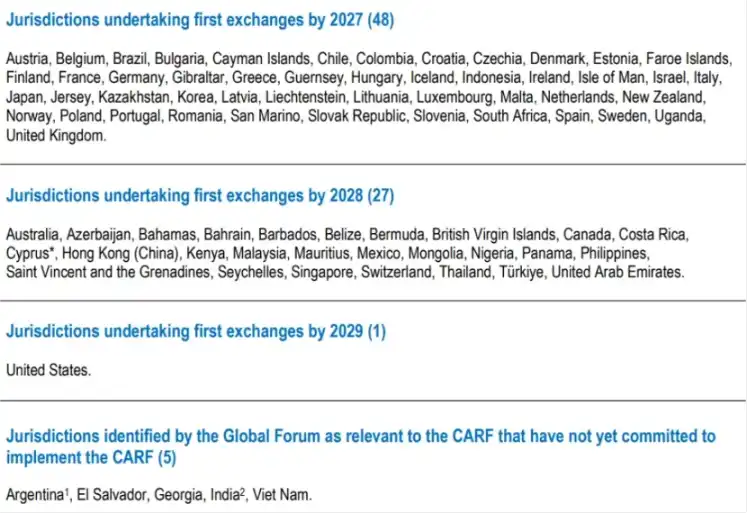

Per awal Desember 2025, 76 negara/wilayah di seluruh dunia telah berkomitmen untuk mengadopsi CARF. Inggris dan UE akan menjadi yang pertama menerapkan kerangka ini (mulai mengumpulkan data pada 2026, pertukaran pertama pada 2027); Singapura, UAE, dan Hong Kong China menyusul, berencana mengumpulkan data pada 2027, dan menerapkan sepenuhnya pada 2028; Swiss menunda waktu implementasi hingga 2027, masih menilai secara hati-hati objek pertukaran; proposal bergabungnya CARF oleh IRS AS masih dalam tahap tinjauan internal.

Ini berarti China tidak berada dalam daftar pertukaran pertama, data CARF tidak akan dipertukarkan secara otomatis kepada otoritas pajak China melalui mekanisme CARF.

China dalam sistem pertukaran otomatis CRS telah mengumpulkan pengalaman sistem dan pemungutan yang matang, menunjukkan bahwa dalam desain hukum,口径 uji tuntas, tata kelola pertukaran data, dan keamanan informasi dan lainnya memiliki infrastruktur dasar untuk menerima standar internasional.

Masalahnya, titik patuh CARF terutama berada pada penyedia layanan aset kripto yang diatur, sedangkan Daratan China telah lama menerapkan pemikiran pengaturan yang kuat bahkan melarang terkait bisnis mata uang virtual, tidak ada sistem platform perdagangan berlisensi yang dapat dimasukkan secara normal ke dalam CARF secara lokal.

Kemajuan Hong Kong dalam CARF dapat meningkatkan intensitas identifikasi tempat tinggal pajak klien dan pelaporan informasi oleh penyedia layanan kripto di Hong Kong, tetapi ini tidak secara otomatis berarti informasi terkait akan mengalir kembali ke otoritas pajak Daratan China. Apakah terjadi pertukaran lintas batas, masih tergantung pada apakah Daratan China memilih untuk berpartisipasi dan membangun hubungan yang dapat dipertukarkan dengan yurisdiksi terkait, serta pengaturan kedua pihak dalam pembatasan penggunaan data, perlindungan privasi, dan koneksi teknis.

Namun, juga perlu ditekankan, belum bergabung tidak berarti dapat diabaikan. Bahkan tanpa melalui jalur pertukaran otomatis CARF, informasi pajak lintas batas masih dapat mengalir dalam kerangka perjanjian pajak yang ada dan kerja sama pemungutan internasional, melalui permintaan kasus per kasus, penegakan hukum bersama, atau cara kerja sama lainnya. Seiring dengan dimulainya pengumpulan data transaksi dan transfer aset kripto secara sistemik oleh yurisdiksi utama global, petunjuk yang dapat digunakan otoritas pajak akan lebih lengkap, dan kemampuan identifikasi risiko lintas batas juga akan meningkat secara bersamaan.

Bagi individu dan lembaga, perubahan paling realistis adalah, selama jalur operasi utama bergantung pada platform perdagangan terpusat, layanan kustodian, atau pintu masuk/keluar mata uang fiat, jejak data transaksi dan keterlacakan akan semakin kuat, paparan kepatuhan akan berubah dari peristiwa probabilistik menjadi normal.