The inflection point of the 2025 crypto market lies not in price, but in structure: the capital side shifted from retail to institution-led, the asset side upgraded from "crypto-native narratives" to an on-chain dollar system centered on stablecoins and RWA, and the institutional side moved from gray-area games to global regulatory normalization. Institutional capital became the marginal buyer through compliant channels such as spot ETFs, reducing market volatility but increasing sensitivity to macro interest rates; stablecoin annual transaction volume surged to become a global settlement infrastructure, while yield-bearing/algorithmic stablecoin failures exposed systemic fragility; RWA (especially on-chain U.S. Treasuries) scaled, promoting the integration of on-chain yield curves with traditional finance. Regulatory clarity further lowered barriers to institutional participation, pushing crypto from a speculative cycle towards a stage of modelable, configurable, and auditable infrastructure. Looking ahead to 2026, the core variables will be the cost of compliant capital, the quality of on-chain dollars, and the sustainability of real yields.

I. Institutions Become Marginal Buyers: Volatility Down, Interest Rate Sensitivity Up

In the early stages of the crypto market's development, price action and market rhythm were almost entirely dominated by retail traders, short-term speculative capital, and community sentiment. The market showed extremely high sensitivity to social media heat, narrative shifts, and on-chain activity indicators. This pricing mechanism, driven primarily by sentiment and narratives, was often summarized as "community beta." Under this framework, asset price increases were often not due to fundamental improvements or long-term capital allocation, but were driven by rapid FOMO sentiment accumulation; conversely, once expectations reversed, panic selling was quickly amplified in the absence of long-term capital to absorb it. This structure caused core assets like Bitcoin and Ethereum to exhibit highly non-linear price volatility characteristics for a considerable period: steep during uptrends, sharp during drawdowns, with market cycles driven by sentiment rather than capital constraints. Retail investors were both the main participants and key amplifiers of volatility in this process, their trading behavior more biased towards short-term price changes than risk-adjusted returns, thus keeping the crypto market in a state of high volatility, high correlation, and low stability for a long time.

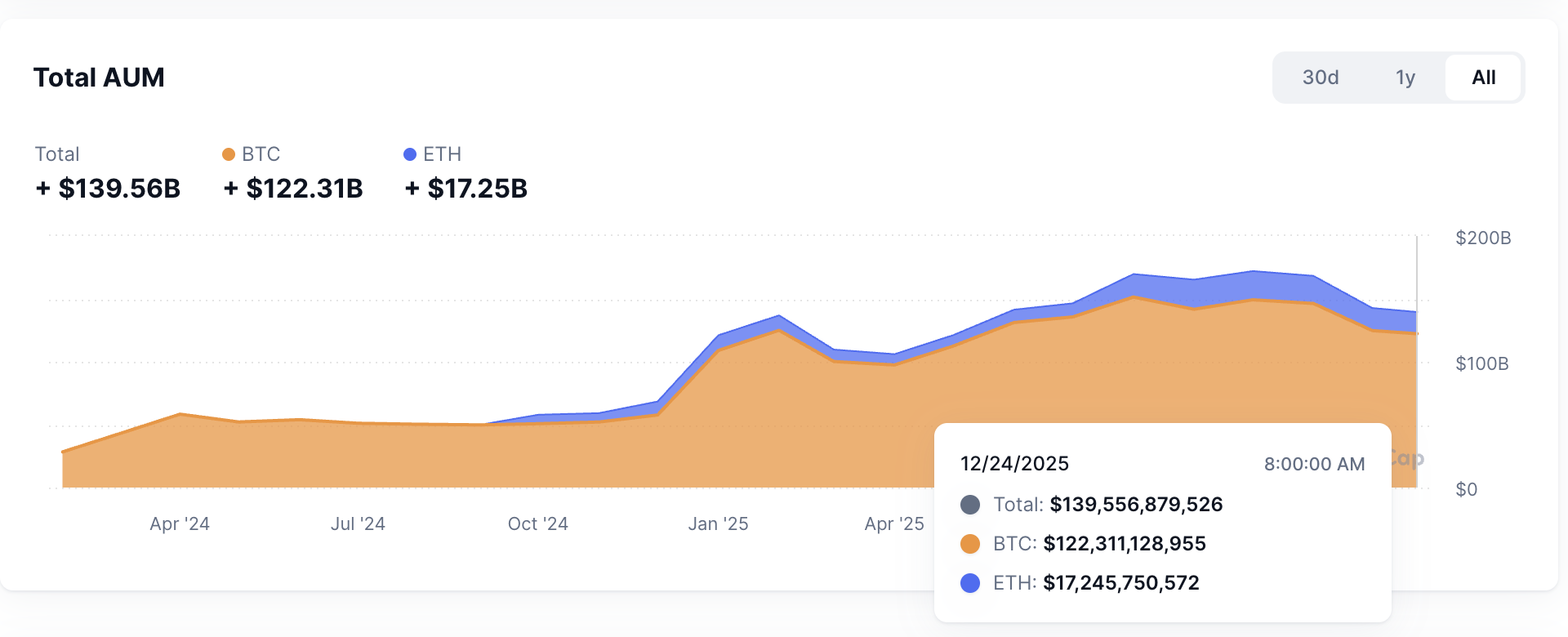

However, from 2024 to 2025, this long-standing market structure underwent a fundamental shift, with specific ETF AUM data as shown in the figure. With the successive approval and successful operation of U.S. spot Bitcoin ETFs, crypto assets gained a compliant channel for systematic allocation by large-scale institutional capital for the first time. Unlike previous "suboptimal paths" through trusts, futures, or on-chain custody, ETFs, with their standardized, transparent, and compliant structure, significantly reduced the operational and compliance costs for institutions entering the crypto market. Entering 2025, institutional capital was no longer just periodically "testing the waters" with crypto assets, but continuously absorbing positions through ETFs, regulated custody solutions, and asset management products, gradually evolving into the marginal buyer in the market. The key to this change lies not in the scale of capital itself, but in the transformation of the capital's nature: the source of new market demand shifted from sentiment-driven retail investors to institutional investors whose core logic is asset allocation and risk budgeting. When the marginal buyer changes, the market's pricing mechanism is reshaped accordingly. The primary characteristic of institutional capital is lower trading frequency and longer holding periods. Unlike retail investors who frequently enter and exit based on short-term price fluctuations and舆论 signals, the decisions of pension funds, sovereign wealth funds, family offices, and large hedge funds are typically based on medium to long-term portfolio performance, and their allocation process requires investment committee discussions, risk control reviews, and compliance assessments. This decision-making mechanism naturally inhibits impulsive trading and causes position adjustments to manifest more as gradual rebalancing rather than emotional chasing of rallies or selling off declines. Against the backdrop of increasing institutional capital share, the weight of high-frequency short-term trading in the market's transaction structure decreases, and price movements begin to reflect capital allocation directions more than immediate sentiment changes. This change is directly reflected in the volatility structure: although prices still adjust with macro or systemic events, extreme short-term amplitudes triggered by sentiment have significantly收敛, especially in core assets with the deepest liquidity like Bitcoin and Ethereum. The market overall began to exhibit a "static sense of order" closer to traditional assets; price movements no longer rely entirely on narrative jumps but gradually return to being constrained by capital.

Simultaneously, the second significant characteristic of institutional capital is its high sensitivity to macro variables. The core goal of institutional investment is not absolute return maximization, but the optimization of risk-adjusted returns, which dictates that its asset allocation behavior is inevitably deeply influenced by the macroeconomic environment. In the traditional financial system, interest rate levels, liquidity tightness, risk appetite changes, and cross-asset arbitrage conditions constitute the core input variables for institutional position adjustments. When this logic was introduced into the crypto market, the price action of crypto assets began to show stronger linkage with macro signals. Market practices in 2025 clearly showed that changes in interest rate expectations had a significantly enhanced impact on Bitcoin and the overall crypto assets. When major central banks, especially the Federal Reserve, adjusted their policy rate paths, institutional allocation decisions regarding crypto assets would also be reassessed accordingly. The logic behind this was not a change in confidence in crypto narratives, but a recalculation of opportunity cost and portfolio risk.

In summary, the process of institutions becoming the marginal buyers in the crypto market in 2025 marked the transition of crypto assets from a stage driven by "narratives and priced by sentiment" to a new stage driven by "liquidity and priced by macro factors." The decline in volatility does not mean the disappearance of risk, but rather a migration of the source of risk: from internal sentiment shocks to high sensitivity to macro interest rates, liquidity, and risk appetite. For research in 2026, this change has methodological significance. The analytical framework needs to shift from simply focusing on on-chain metrics and narrative changes to systematically studying capital structure, institutional behavior constraints, and macro transmission paths. The crypto market is being incorporated into the global asset allocation system, and its price no longer merely answers "what story the market is telling," but increasingly reflects "how capital is allocating risk." This transformation is one of the most profound structural changes of 2025.

II. Maturation of the On-Chain Dollar System: Stablecoins Become Infrastructure, RWA Brings the Yield Curve On-Chain

If the large-scale entry of institutional capital in 2025 answered the question "who is buying crypto assets," then the maturation of stablecoins and real-world asset tokenization (RWA) further answered the more fundamental questions of "what to buy, what to use for settlement, and where the yield comes from." It is at this level that the crypto market completed a key leap from "crypto-native financial experiments" to an "on-chain dollar financial system" in 2025. Stablecoins evolved beyond mere mediums of exchange or safe-haven tools into the clearing and pricing foundation of the entire on-chain economic system; meanwhile, RWA represented by on-chain U.S. Treasuries began to scale, giving the on-chain world for the first time a sustainable, auditable low-risk yield anchor, fundamentally changing the yield structure and risk pricing logic of DeFi.

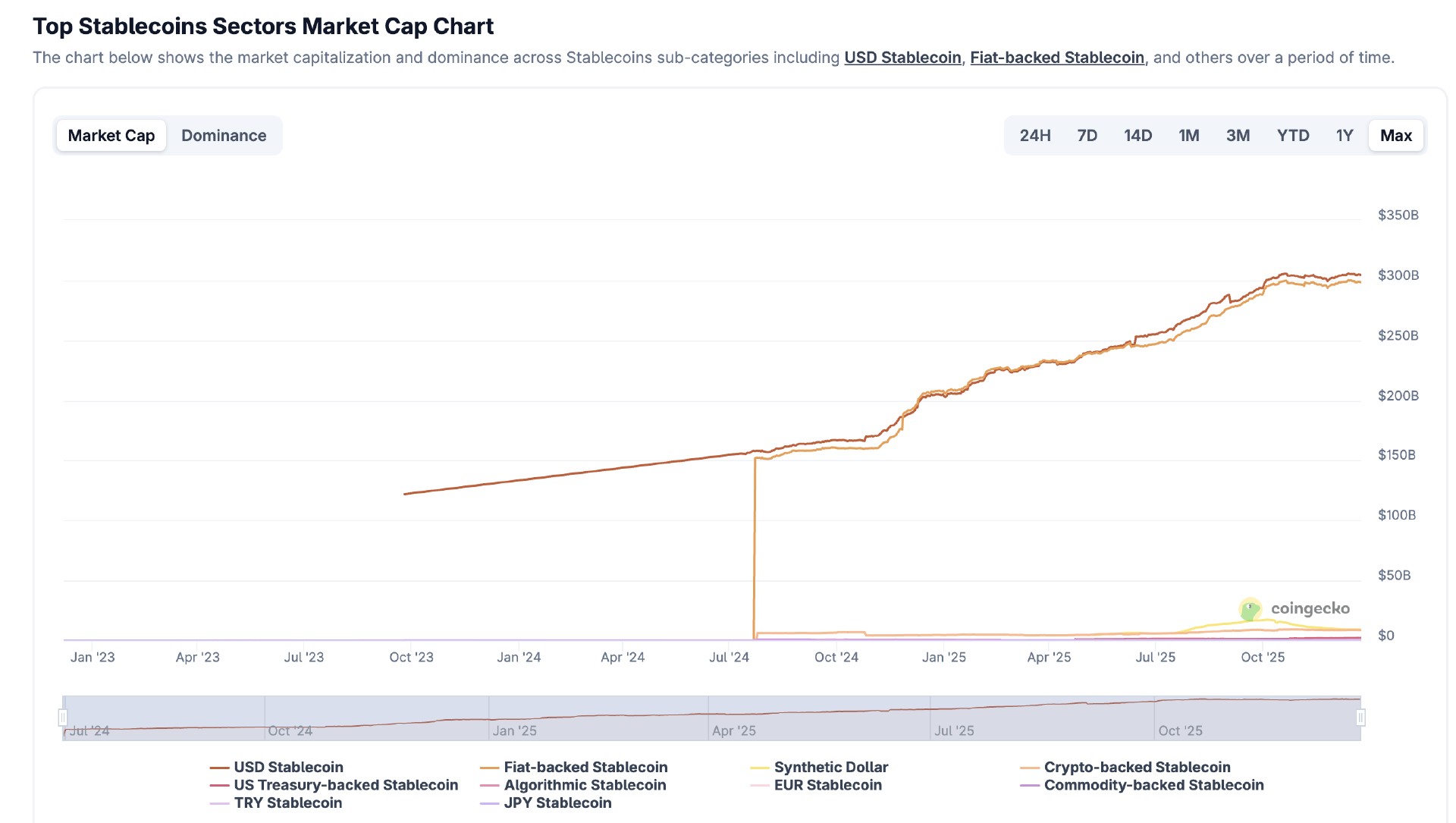

From a functional perspective, stablecoins had indisputably become the core infrastructure of on-chain finance in 2025. Their role had long surpassed "price-stable trading tokens" and had fully taken on multiple functions such as cross-border settlement, trading pair pricing, DeFi liquidity hub, and institutional capital entry/exit channel. Whether in centralized exchanges, decentralized trading protocols, or in RWA, derivatives, and payment scenarios, stablecoins constituted the underlying轨道 of fund flows. On-chain transaction volume data clearly showed that stablecoins had become an important extension of the global dollar system, with their annualized on-chain transaction volume reaching tens of trillions of U.S. dollars, far exceeding the payment systems of most individual countries. This fact meant that blockchain truly assumed the role of a "functional dollar network" for the first time in 2025, rather than just an ancillary system for high-risk asset trading. More importantly, the widespread adoption of stablecoins changed the risk structure of on-chain finance. After stablecoins became the default unit of account, market participants could trade, lend, and allocate assets without being directly exposed to the price volatility of crypto assets, significantly lowering the participation barrier. This was particularly critical for institutional capital. Institutions do not inherently seek the high volatility returns of crypto assets but value predictable cash flows and risk-controllable sources of yield. The maturity of stablecoins allowed institutions to obtain "dollar-denominated" exposure on-chain without bearing traditional crypto price risk, laying the foundation for the subsequent expansion of RWA and yield-bearing products.

Against this backdrop, the scaling of RWA, especially on-chain U.S. Treasuries, became one of the most structurally significant developments of 2025. Unlike early attempts dominated by "synthetic assets" or "yield mapping," RWA projects in 2025 began to introduce real-world low-risk assets directly on-chain in a manner closer to traditional financial asset issuance. On-chain U.S. Treasuries were no longer just conceptual narratives but existed in an auditable, traceable, and composable form, with clear cash flow sources,明确的期限结构, and directly linked to the risk-free interest rate curve in the traditional financial system.

However, precisely as stablecoins and RWA expanded rapidly, 2025 also集中暴露 the other side of the on-chain dollar system, namely its potential systemic fragility. Particularly in the yield-bearing and algorithmic stablecoin sectors, multiple de-pegging and collapse events served as wake-up calls for the market. These failures were not isolated incidents but集中反映 the same type of structural problems: implicit leverage from recursive re-staking, opacity in collateral structure, and high concentration of risk in a few protocols and strategies. When stablecoins were no longer solely backed by short-term Treasuries or cash equivalents but pursued higher yields through complex DeFi strategies, their stability no longer came from the assets themselves but from implicit assumptions about持续的市场繁荣. Once this assumption was broken, de-pegging was no longer a technical fluctuation but could evolve into a systemic shock. Multiple events in 2025 showed that the risk of stablecoins lies not in "whether they are stable," but in "whether the source of stability can be clearly identified and audited." Yield-bearing stablecoins could indeed provide returns significantly higher than the risk-free rate in the short term, but these returns were often built on leverage stacking and liquidity mismatch, and their risks were not fully priced. When market participants treated these products as "cash-like" equivalents, risk was systemically amplified. This phenomenon forced the market to re-examine the role positioning of stablecoins: are they payment and settlement tools, or financial products embedded with high-risk strategies? This question was raised with real costs for the first time in 2025.

Therefore, looking ahead to 2026, the research focus is no longer "whether stablecoins and RWA will continue to grow." From a trend perspective, the expansion of the on-chain dollar system is almost irreversible. The真正关键的问题 lies in "quality stratification." The differences between different stablecoins in terms of collateral asset transparency, term structure, risk isolation, and regulatory compliance will be directly reflected in their cost of capital and usage scenarios. Similarly, the differences between different RWA products in legal structure,清算机制, and yield stability will determine whether they can become part of institutional-grade asset allocation. It is foreseeable that the on-chain dollar system will no longer be a homogeneous market but will form a clear hierarchical structure: products with high transparency, low risk, and strong compliance will obtain lower funding costs and wider adoption; while products relying on complex strategies and implicit leverage may be marginalized or even phased out. From a more macro perspective, the maturation of stablecoins and RWA has embedded the crypto market into the global dollar financial system for the first time. The on-chain world is no longer just an experimental field for value transfer, but an extension of dollar liquidity, yield curves, and asset allocation logic. This transformation, mutually reinforced by the entry of institutional capital and the normalization of the regulatory environment, jointly pushes the crypto industry from cyclical speculation towards infrastructure development.

III. Regulatory Normalization: Compliance Becomes a Moat, Reshaping Valuation and Industry Organization

In 2025, global crypto regulation entered a stage of normalization. This change was not reflected in a single law or regulatory event, but in a fundamental shift in the overall "survival assumption" of the industry. For many years prior, the crypto market had always operated in a highly uncertain institutional environment. The core question was not growth or efficiency, but "is this industry allowed to exist?" Regulatory uncertainty was seen as part of the systemic risk, and capital entering often had to reserve additional risk premiums for potential compliance shocks, enforcement risks, and policy reversals. Entering 2025, this long-unresolved issue was阶段性解决 for the first time. As major jurisdictions in Europe, the US, and the Asia-Pacific陆续形成 relatively clear and enforceable regulatory frameworks, market focus began to shift from "whether it can exist" to "how to scale under compliance premises." This shift had a profound impact on capital behavior, business models, and asset pricing logic.

Regulatory clarity first significantly lowered the institutional门槛 for entering the crypto market. For institutional capital, uncertainty itself is a cost, and regulatory ambiguity often意味着 unquantifiable tail risks. In 2025, as key links such as stablecoins, ETFs, custody, and trading platforms were gradually纳入明确监管范围, institutions were finally able to assess the risks and returns of crypto assets within existing compliance and risk control frameworks. This change did not mean that regulation became looser, but rather became predictable. Predictability itself is a prerequisite for the large-scale entry of capital. Once regulatory boundaries were defined, institutions could absorb these constraints through internal processes, legal structures, and risk models, without treating them as "uncontrollable variables." As a result, more long-term capital began to enter the market systematically, with participation depth and allocation scale increasing simultaneously. Crypto assets were gradually incorporated into a broader asset allocation system. More importantly, regulatory normalization changed the competitive logic at the enterprise and protocol levels.

The profound impact of regulatory normalization lies in its reshaping of the industry's organizational form. As compliance requirements were gradually implemented in issuance, trading, custody, and settlement, the crypto industry began to show stronger trends of centralization and platformization. More products chose to complete issuance and distribution on regulated platforms, and trading activities concentrated towards venues with licenses and compliant infrastructure. This trend does not mean the disappearance of decentralization ideals, but rather that the "entry points" for capital formation and flow are being reorganized. Token issuance gradually evolved from无序的点对点销售 to a more process-oriented, standardized operation closer to traditional capital markets, forming a new form of "Internet capital marketization." In this system, issuance, disclosure, lock-up periods, distribution, and secondary market liquidity are more tightly integrated, and market participants' expectations of risk and return也随之更加稳定. This change in industry organization is directly reflected in the adjustment of asset valuation methods. In previous cycles, crypto asset valuation heavily relied on metrics like narrative strength, user growth, and TVL, with relatively limited consideration of institutional and legal factors. Entering 2026, as regulation became a quantifiable constraint, valuation models began to introduce new dimensions. Regulatory capital占用, compliance costs, legal structure stability, reserve transparency, and the accessibility of compliant distribution channels gradually became important variables affecting asset prices. In other words, the market began to impose "institutional premiums" or "institutional discounts" on different projects and platforms. Entities that could operate efficiently within the compliance framework and internalize regulatory requirements as operational advantages were often able to obtain funding support at lower capital costs; while models relying on regulatory arbitrage or institutional ambiguity faced valuation compression or even marginalization risks.

IV. Conclusion

The inflection point of the 2025 crypto market is essentially three things happening simultaneously: the migration of capital from retail to institutions, the formation of assets from narratives to an on-chain dollar system (stablecoins + RWA), and the落地 of rules from gray areas to normalized regulation. These three factors together pushed crypto from a "high-volatility speculative product" towards "modelable financial infrastructure." Looking ahead to 2026, research and investment should focus on three core variables: the transmission strength of macro interest rates and liquidity to crypto, the quality stratification of on-chain dollars and the sustainability of real yields, and the institutional moat constituted by compliance costs and distribution capabilities. Under the new paradigm, the winners will not be the projects that tell the best stories, but the infrastructure and assets that can持续扩张 under the three constraints of capital, yield, and rules.