The Hong Kong Monetary Authority (HKMA) has handed out its first stablecoin licenses, and the winners are Standard Chartered’s JV and HSBC.

HKMA Has Released First Stablecoin Licenses After A Delay

According to HKMA’s website, two entities have now become registered stablecoin issuers in Hong Kong: Anchorpoint Financial Limited and The Hongkong and Shanghai Banking Corporation Limited.

Hong Kong launched its stablecoin bill called the Stablecoins Ordinance back in August 2025, establishing a licensing regime for stablecoin issuers. Under this law, parties interested in issuing fiat-tied cryptocurrencies in the Chinese city have to first obtain a license from the HKMA.

Major names quickly lined up to apply for a license. This included HSBC and Anchorpoint Financial Limited. The latter is a joint venture (JV) created by Standard Chartered, Animoca Brands, and Hong Kong Telecom. In total, the HKMA ended up receiving applications from 36 entities. Despite the high interest, though, Eddie Yue, the financial regulator’s chief executive, said in February that a “very small number” of licenses would be granted in the first wave.

Yue also said that these licenses would arrive in March, but in the end, no licenses were issued during that month, suggesting a delay from the HKMA. However, today, on April 10th, the first batch has finally gone out.

With just two licenses being handed out, Yue indeed set up the correct expectations. As mentioned earlier, Standard Chartered’s JV and HSBC are the applicants who have received the first approval. Thus, these banks have a head start over the rest when it comes to stablecoins in the region.

Hong Kong’s stablecoins advance is just one example of positive regulation that these fiat-tied tokens have seen the world over in the past year. One of the most important wins for the sector has been the GENIUS Act signed into law by United States President Donald Trump last year.

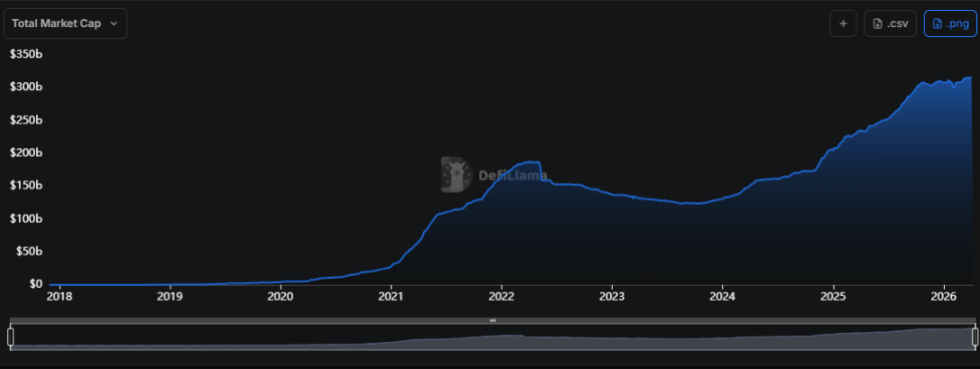

Because of all the regulatory momentum and adoption, the stablecoins sector has performed relatively well amid the wider downturn in the digital assets market. As data from DefiLlama shows, stablecoins have seen their combined market cap move sideways at all-time highs (ATHs) since Q4 2025. In the same period as this flat phase in these fiat-tied tokens, Bitcoin has gone down by more than 42%.

The trend in the market cap of the stablecoins over the years | Source: DefiLlama

While the stablecoin market cap is significant in size, the vast majority of it is covered by just two assets pegged to the US Dollar: USDT and USDC. Moves like the euro-pegged token from a consortium of major European banks could shake up this dominance, but it only remains to be seen how the landscape will evolve.

Bitcoin Price

At the time of writing, Bitcoin is floating around $72,200, up more than 8% in the last seven days.

Looks like the price of the coin has surged recently | Source: BTCUSDT on TradingView