The narrative of the "execution line" first caught my attention in November within X and Substack circles. It originated from Mike Green's "$140k poverty line" theory, which went viral in the United States. I never expected that over a month later, this narrative would spread and mutate into the "execution line" in China, which is quite fascinating.

It's a pity my AI narrative radar (see here) wasn't ready at that time; otherwise, I would have loved to see if AI could track the spread and evolution of this narrative.

01

At the end of November, I read three articles by Mike Green on Substack:

These are three extremely long articles that make you feel like you're reading forever; the three combined have the word count of a small book.

I'll try to summarize them in plain language as follows:

The gist of the articles is: If you feel like the current economic data looks good, but your daily life is tight, and an annual salary of $100,000 still leaves you feeling poor, it's not your fault. It's because the ruler used to measure wealth and poverty is like Doraemon's self-deceiving ruler.

The articles present three main points:

1. The "Poverty Line" is actually like marking the boat to find the sword (a Chinese idiom meaning a futile approach).

The official U.S. poverty line is an annual income of $31,200 for a family of four; as long as your income exceeds $30,000, you are not considered poor.

But this ruler was created in 1963. The logic back then was simple: a family spent about one-third of their money on food, so by calculating the minimum food cost and multiplying it by 3, you got the poverty line.

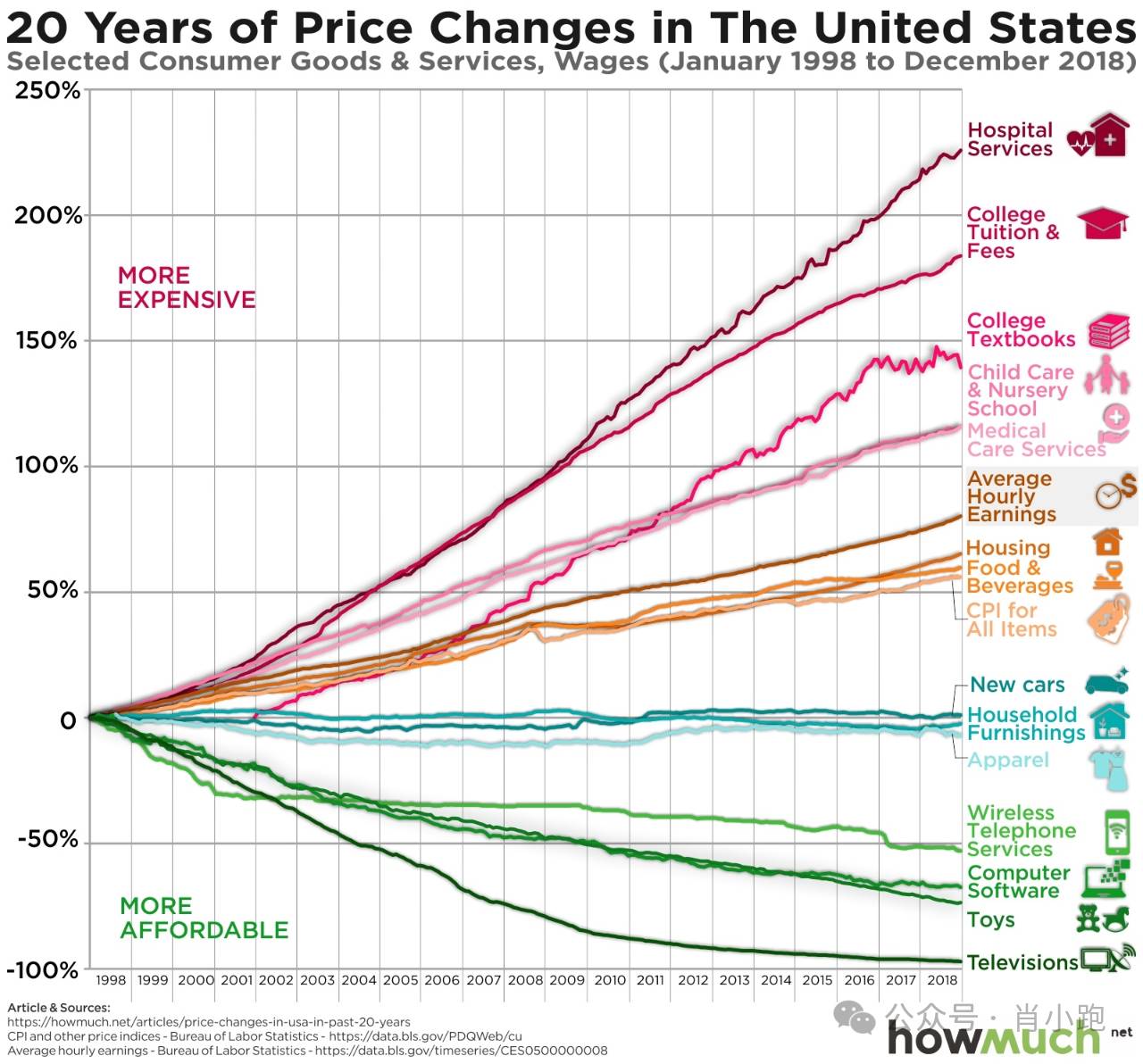

But the situation is vastly different now. You've probably all seen that famous chart—"Baumol's Cost Disease":

Food has become cheaper, but the costs of housing, healthcare, and childcare have skyrocketed. If you recalculate based on the 1963 standard of living—meaning the ability to normally "participate" in society (having a place to live, a car to drive, childcare, and access to healthcare when sick)—the real poverty line today is not $30,000-plus, but $140,000 (approximately 1 million RMB), just to live decently in this society.

2. The harder you work, the poorer you become.

There's a huge bug in the design of the U.S. welfare system: When your annual salary is $40,000, you are officially poor. The state gives you food stamps, covers your healthcare (Medicaid), and subsidizes childcare costs. Life is tight but there's a safety net.

But when you work hard and your salary increases to $60,000, $80,000, or even $100,000, disaster strikes: Your income is higher, but the welfare benefits are gone. Now you need to pay for expensive health insurance and rent in full.

The result is: A family with an annual income of $100,000 might have less disposable cash left at the end of each month than a family with an annual income of $40,000 (receiving welfare).

This is the origin of the "execution line" and the "execution line specifically targeting the middle class" narrative on Chinese social networks: Just like in a game where your health drops to a certain threshold and you get instantly killed by a skill, a one-hit KO; the middle class, stuck in the middle,刚好 step onto the node where welfare withdraws, tax burdens increase, and all kinds of rigid expenditures (health insurance, rent, childcare, student loans) fully press down. They lose subsidies while bearing high costs. Once they encounter unemployment, illness, or rent increases, they are locked in by the execution line.

3. The assets you own are actually quite inflated.

Because:

Your house is not an asset; it's prepaid rent: Did you get richer if your house appreciated from $200,000 to $800,000? No. Because if you sell it, you still have to spend $800,000 to buy a similar house to live in. You haven't gained additional purchasing power; your cost of living has just increased.

The inheritance you're waiting for is not a wealth transfer: The inheritance from the Baby Boomer generation won't be passed on to you; it will be passed on to nursing homes and the healthcare system. Nursing care (dementia care, nursing homes) in the U.S. now costs $6,000 to over $10,000 per month. An $800,000 house owned by parents will most likely turn into medical bills, collected by medical institutions and insurance companies.

Your class has become a caste: In the past, you could跨越阶级 through hard work. Now it depends on "admission tickets"—Ivy League degrees, recommendation letters from core circles. The inflation rate of these "assets" is even higher than that of houses. So an annual salary of $150,000 might allow you to survive, but it can't buy the ticket for your children to enter the upper class.

02

What exactly caused the great inflation of the U.S. poverty line (or, in our context—the great shift of the "execution line")?

Mike Green attributes it to three turning points in U.S. history:

Turning point 1: The deterioration and monopolization of unions in the 1960s, leading to decreased efficiency and increased costs.

Turning point 2: The great antitrust shift in the 1970s, where large companies疯狂兼并, controlled the market, and suppressed wages.

Turning point 3 (which everyone can probably guess): The China shock. But the article's viewpoint is not that China forcibly took away jobs, but that U.S. capitalists engaged in capital arbitrage—moving almost all factories away from the U.S. to profit from the differential.

But Teacher Green didn't just kill and not bury; he finally proposed a very hardcore solution called the "Rule of 65." The core idea is very familiar to us Chinese: "Fight the local tyrants and distribute the land"—(1) Increase taxes on corporations (but exempt investments from taxes); (2) Prevent large corporations from deducting interest on borrowed money for tax purposes,坚决打击 financial空转; (3) Reduce the burden on the workhorses:大幅降低 the payroll tax (FICA) for ordinary people, putting more cash in their hands. Where does the missing money come from? Make the rich pay more, remove the cap on social security taxes for the wealthy.

Chinese experience is absolutely practical.

03

Teacher Mike Green's views刷屏 enthusiastically among the U.S. middle-class masses. But it aroused collective resistance from the elite class and various economists.

There are indeed many data flaws in his articles. For example, using data from affluent areas (Essex County, top 6% in U.S. housing prices) as the national average; assuming all children go to expensive daycare centers (over $30,000 per year), while in reality most American families still take care of their own children; some concepts are also somewhat混淆, such as equating "average expenditure" with "minimum survival needs."

Later, Green went on many podcasts to explain himself: This $140,000 does not refer to the traditional poverty of "not having enough to eat," but rather the "decent living threshold" for an ordinary family to live without relying on government subsidies and still save some money.

Although Teacher Green's math seems to be indeed miscalculated, the critics didn't win either, because regardless of what the exact poverty line is, people's "feeling of poverty" is very real. And the "feeling of being executed" is becoming more and more real—whether for Americans or Chinese.

Why? I think the real reason is still "Baumol's Disease."

"Baumol's Cost Disease" was proposed by economist William Baumol in 1965 to describe an economic phenomenon:

Some industries (like manufacturing) rely on machines and technology, becoming more and more efficient, with unit costs getting lower and lower; but some industries (like education, healthcare) rely mainly on people, and efficiency is difficult to significantly improve—one lesson still takes an hour, one doctor seeing one patient also takes time, impossible to speed up multiples like a factory.

So here's the problem: Wages across society will rise along with those high-efficiency industries. To prevent teachers and doctors from jumping to higher-paying industries, schools and hospitals also have to raise wages. But their efficiency hasn't improved much, yet wages have risen, resulting in higher and higher costs and prices rising accordingly.

In other words: Industries that can be sped up by machines have lifted overall wages. Industries that cannot提速 have to raise salaries to retain people, but efficiency hasn't changed, so they become more expensive. This is "Baumol's Cost Disease."

This is why on the chart at the beginning of the article: The lines representing industrial goods like TVs, phones, and toys go downward, becoming cheaper and cheaper; while the lines representing education, healthcare, and childcare costs soar.

The logic behind this is actually very realistic:

In any field that can be replaced by machines and automation, efficiency will only get higher. For example, mobile phones, although the price doesn't seem to have dropped much, their performance is worlds apart from a few years ago, with computing power and storage multiplying several times. This is essentially a kind of "invisible price reduction" brought by technology. Not to mention Chinese manufacturing, photovoltaics, EVs, and lithium batteries, where automation is increasing, and costs are driven straight to the floor price.

But the problem lies in those places where "machines cannot replace people." When I was little, the nanny who took care of me could look after four kids by herself. Even today, she can still only look after four at most, and because today's parents have higher demands, she might even be able to look after fewer children. This means that the production efficiency of the service industry hasn't changed for decades, and has even regressed.

However, the service industry (specifically in the U.S.) has to raise wages for nannies and nurses to prevent them from running off to deliver food or work in factories. They have to keep up with the income level of the whole society. The coffee beans in a coffee shop aren't worth much, but the exorbitant price you pay is mostly for the staff's labor, rent, and utilities. Efficiency hasn't increased, but wages have to rise, so the cost can only be passed on to consumers. (Note: This specifically refers to the U.S.)

Therefore, the American middle-class families being "executed" are not poor to the point of not having enough to eat. They have cars, iPhones, and various video memberships, but when facing "service-based expenditures" like buying a house, seeing a doctor, or raising children, their wallets are instantly emptied. So, it's not that the American people have truly become poorer; it's that the American people's money becomes less and less sufficient in the face of those "inefficient but outrageously expensive" services.

Writing here, I know everyone has been wanting to ask: Does China have an execution line? Does China's execution line execute the middle class? Has China's poverty line also become higher?

The answer is most likely no.

So our "execution line" might not appear. I discussed this with Dean Liu in the "Wall Crack Forum" podcast episode: "When China Becomes an Industrial Cthulhu, What's Left of Trade? Higher Productivity, Why Lower Wages?"

The situation in China, we Chinese should all know: Chinese society is more sensitive to service prices. For things that are not "production tools," people are generally unwilling to pay, especially for services. In the expenditure structure of labor force reproduction, certain service expenditures have been长期压得很低 in China, even to the extent that "this part of the wage doesn't have to be paid." When services are undervalued and the welfare stage is different, the wage system naturally presents a structure completely different from the West.

This creates a奇妙的现象: One can always "survive" no matter what. Because the cost of living can be pressed extremely low.

Therefore, China might not have an "execution line," but that doesn't mean there isn't an invisible threshold. For example, how low can the dignity of service providers be pressed? How high can the intensity be raised?

So it still comes back to that saying: Everything comes at a cost.